1) The extent of tests of details of balances cannot be reduced when transaction-related

audit objectives have been satisfied by tests of controls or substantive tests of

transactions.

A) True

B) False

2) For a firm that practices good internal controls in the sales and collections cycle, the

function of indicating credit approval should be recorded on which of the following

documents?

A) sales order

B) sales invoice

C) customer order

D) remittance advice

3) One of the primary objectives in examining the repairs and maintenance accounts is

to obtain evidence that:

A) expenditures of equipment have not been charged to expense

B) the actual amount recorded is the same as the budgeted amount

C) expenditures for equipment have been recorded in the proper period

D) revenue expenditures made on behalf of equipment have been recorded in the proper

period

4) In using sampling distribution for attributes, which one of the following must be

known to evaluate the sample results?

A) Estimated dollar value of the population

B) Standard exception of the values in the population

C) Actual exception rate of the attribute in the population

D) Sample size

5) Rule 101, Independence, applies to covered members in a position to influence an

attest engagement.

A) True

B) False

6) PCAOB Standard 5 indicates that material fraud by senior management is a material

weakness.

A) True

B) False

7) The

A) Auditing standards applicable to financial statements of private companies

B) Compilation and review standards

C) Professional conduct

D) Auditing standards applicable to financial statements of private and public

companies

8) The receipt of raw materials is a part of the acquisition and payment cycle.

A) True

B) False

9) Controls which apply to a specific element of the system are called:

A) user controls

B) general controls

C) systems controls

D) applications controls

10) In the application of statistical techniques to the estimation of dollar amounts, a

preliminary sample is usually taken primarily for the purpose of estimating the

population:

A) mode

B) range

C) median

D) variability

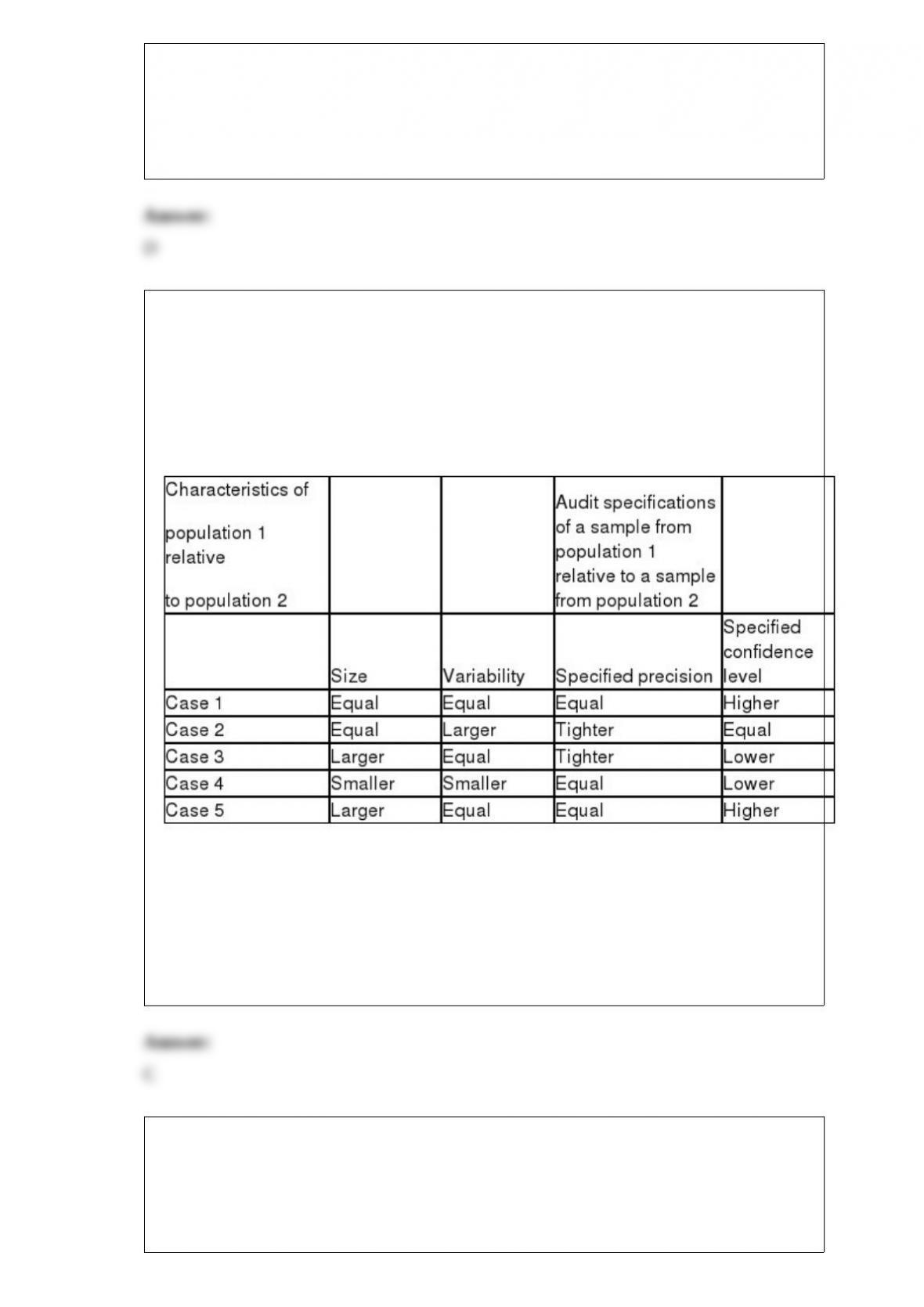

11) An audit partner is developing an office-training program to familiarize his

professional staff with statistical decision models applicable to the audit of dollar-value

balances. He wishes to demonstrate the relationship of sample sizes to population size

and variability and the auditor’s specifications as to precision and confidence level. The

partner prepared the following table to show comparative population characteristics and

audit specifications of two populations.

Based on the information presented above, you are to indicate for the specified case

from the table the required sample size to be selected from population 1 relative to the

sample from population 2 . In case 4, the required sample from population 1 is:

A) larger than the required sample size from population 2

B) equal to the required sample size from population 2

C) smaller than the required sample size from population 2

D) indeterminate relative to the required sample size from population 2

12) Which one of the following procedures would not be appropriate for an auditor in

discharging his responsibilities concerning the client’s physical inventories?

A) confirmation of goods in the hands of public warehouses

B) supervising the taking of the annual physical inventory

C) carrying out physical inventory procedures at an interim date

D) obtaining written representation from the client as to the existence, quality, and

dollar amount of the inventory

13) Any public accounting firm can be a member of the

A) True

B) False

14) The two major balance-related audit objectives in testing payroll liabilities are

accuracy and cutoff.

A) True

B) False

15) The total of the individual account balances in the accounts receivable subsidiary

ledger should equal the:

A) total sales for the period

B) balance of the sales account in the general ledger

C) total sales less the total cash received for the period

D) balance of the accounts receivable account in the general ledger

16) Which of the following statements is most correct regarding the primary purpose of

audit procedures?

A) to detect all errors or fraudulent activities as well as illegal activities

B) to comply with auditing standards promulgated by the PCAOB for publicly held

clients

C) to gather corroborative audit evidence about management’s assertions regarding the

client’s financial statements

D) to determine the amount of errors in the balance sheet accounts in order to adjust the

accounts to actual

17) Auditors may identify conditions during fieldwork that change or support a

judgment about the initial assessment of fraud risks. Which of the following is not a

condition which should alert an auditor that the initial assessment should be changed?

A) preliminary assessment of control risk has been modified

B) discrepancies in the accounting records

C) unusual relationships between the auditor and management

D) missing or conflicting evidence

18) The Statements on Auditing Standards issued by the Auditing Standards Board:

A) interpret generally accepted auditing standards

B) are the equivalent of laws for audit practitioners

C) must be followed in all situations

D) are optional guidelines which an auditor may choose to follow or not follow when

conducting an audit

19) The starting point for the verification of the balance in the general bank account is

to obtain a bank cut-off statement.

A) True

B) False

20) Which of the following is not a term related to evaluating results in audit sampling

until after a sample is tested and evaluated?

A) Sample exception rate

B) Estimated population exception rate

C) Computed upper exception rate

D) Exception

21) The Sarbanes-Oxley Act requires:

A) all public companies to issue reports on internal controls

B) all public companies to define adequate internal controls

C) the auditor of public companies to design effective ICFR

D) the auditor of public companies to provide recommendations to correct material

weaknesses

22) Audit contracts (engagement letters):

A) may be either oral or written

B) must be written

C) must be written and notarized

D) must be written if the client is regulated by the Securities and Exchange

Commission

23) If the auditor decides not to confirm accounts receivable, the auditor should:

A) always use alternative procedures to audit the accounts receivable

B) include copies of customer statements in the audit files

C) document the reasons for such a decision in the audit files

D) include copies of customer sales invoices in the audit files

24) An auditor should perform alternative procedures to substantiate the existence of

accounts receivable when:

A) no reply to a positive confirmation request is received

B) no reply to a negative confirmation request is received

C) collectability of the receivables is in doubt

D) pledging of the receivables is probable

25) Audit documentation is the joint property of the auditor and the audit client.

A) True

B) False

26) The capital acquisition and repayment cycle does not include:

A) payment of interest

B) payment of dividends

C) payment of vendor invoices

D) acquisition of capital through interest-bearing debt

27) The shipping point is critical because it is the first point at which company assets

are released to another party.

A) True

B) False

28) Match five of the terms (a-h) with the definitions provided below (1-5):

a.Audit documentation

b.Audit procedures

c.Audit objectives

d.Analytical procedures

e.Budgets

f.Reliability of evidence

g.Sufficiency of evidence

h.Persuasiveness of evidence

________ 1> Use of comparisons and relationships to assess the reasonableness of

account balances.

________ 2> Detailed instructions for the collection of a type of audit evidence.

________ 3> The degree to which evidence can be considered believable or

trustworthy.

________ 4> Contains all the information that the auditor considers necessary to

conduct an adequate audit and to provide support for the audit report.

________ 5> This is determined by the amount of evidence obtained.

29) Who is generally responsible for opening receipts when a company uses a lockbox

to speed the handling of cash receipts?

A) company personnel

B) temporary employees in the town where the lockbox is located

C) bank employees

D) company controller