1) A static planning budget is suitable for planning but is inappropriate for evaluating

how well costs are controlled.

2) Residual income should not be used to evaluate a profit center.

3) In traditional costing, some manufacturing costs may be excluded from product

costs.

4) If two companies produce the same product and have the same total sales and same

total expenses, operating leverage will be higher in the company with a higher

proportion of fixed expenses in its cost structure.

5) The practice of assigning the costs of idle capacity to products results in more stable

unit product costs.

6) The cash budget is typically prepared before the direct materials budget.

7) The formula for computing the predetermined overhead rate is:

Predetermined overhead rate = Estimated total manufacturing overhead cost / Estimated

total amount of the allocation base

8) In a special order situation, any fixed cost that could be avoided if the special order

were not accepted would be irrelevant.

9) Muecke Inc. is working on its cash budget for April. The budgeted beginning cash

balance is $40,000. Budgeted cash receipts total $150,000 and budgeted cash

disbursements total $158,000. The desired ending cash balance is $50,000.

To attain its desired ending cash balance for April, the company needs to borrow:

A.$18,000

B.$0

C.$50,000

D.$82,000

10) A product sells for $10 per unit and has variable expenses of $6 per unit. Fixed

expenses total $45,000 per month. How many units of the product must be sold each

month to yield a monthly profit of $15,000?

A.6,000 units

B.3,750 units

C.15,000 units

D.10,000 units

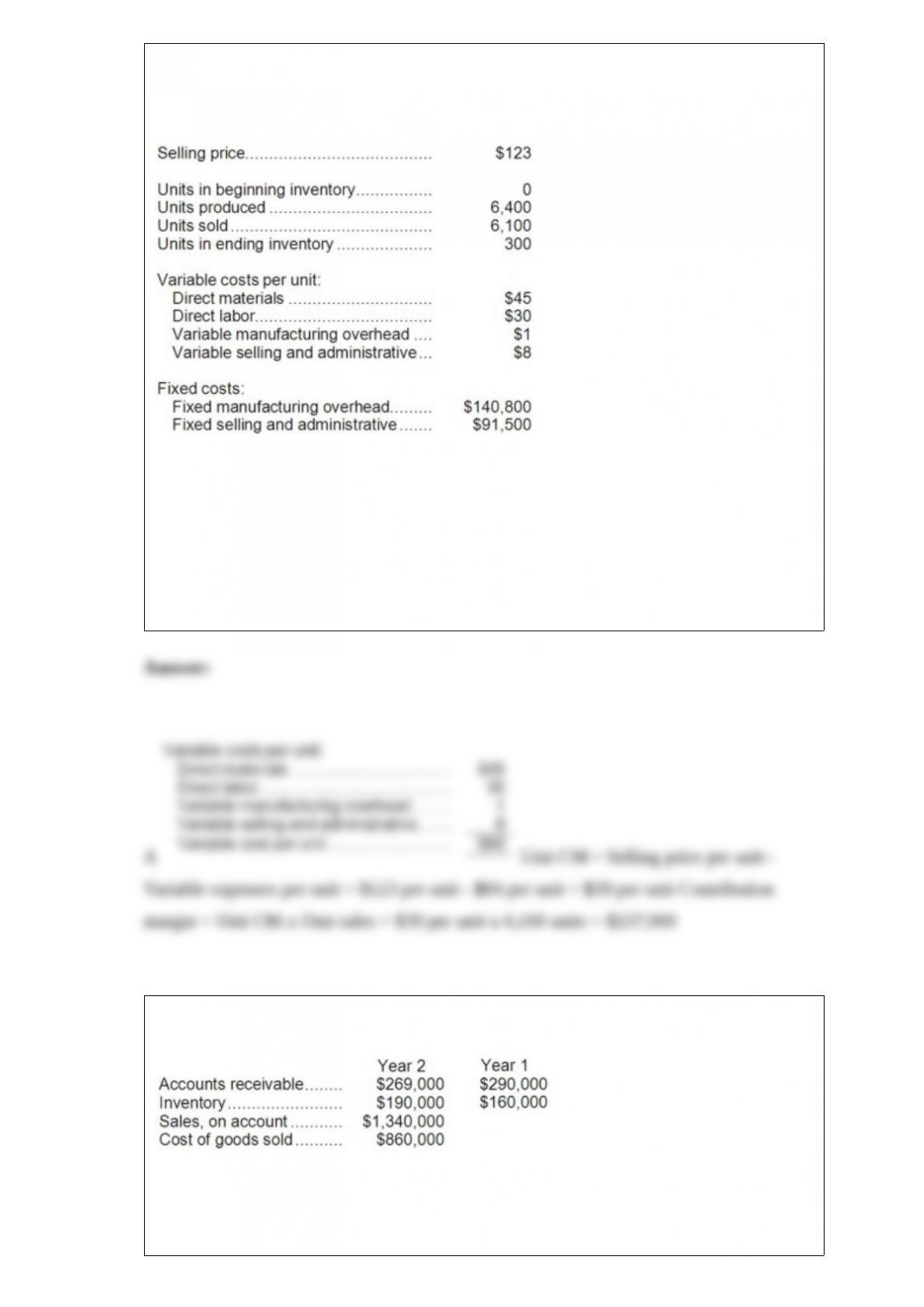

11) Hatfield Corporation, which has only one product, has provided the following data

concerning its most recent month of operations:

The total contribution margin for the month under variable costing is:

A.$237,900

B.$97,100

C.$152,500

D.$286,700

12) Louie Corporation has provided the following data:

The company’s operating cycle for Year 2 is closest to:

A.81.0 days

B.150.5 days

C.79.2 days

D.9.7 days

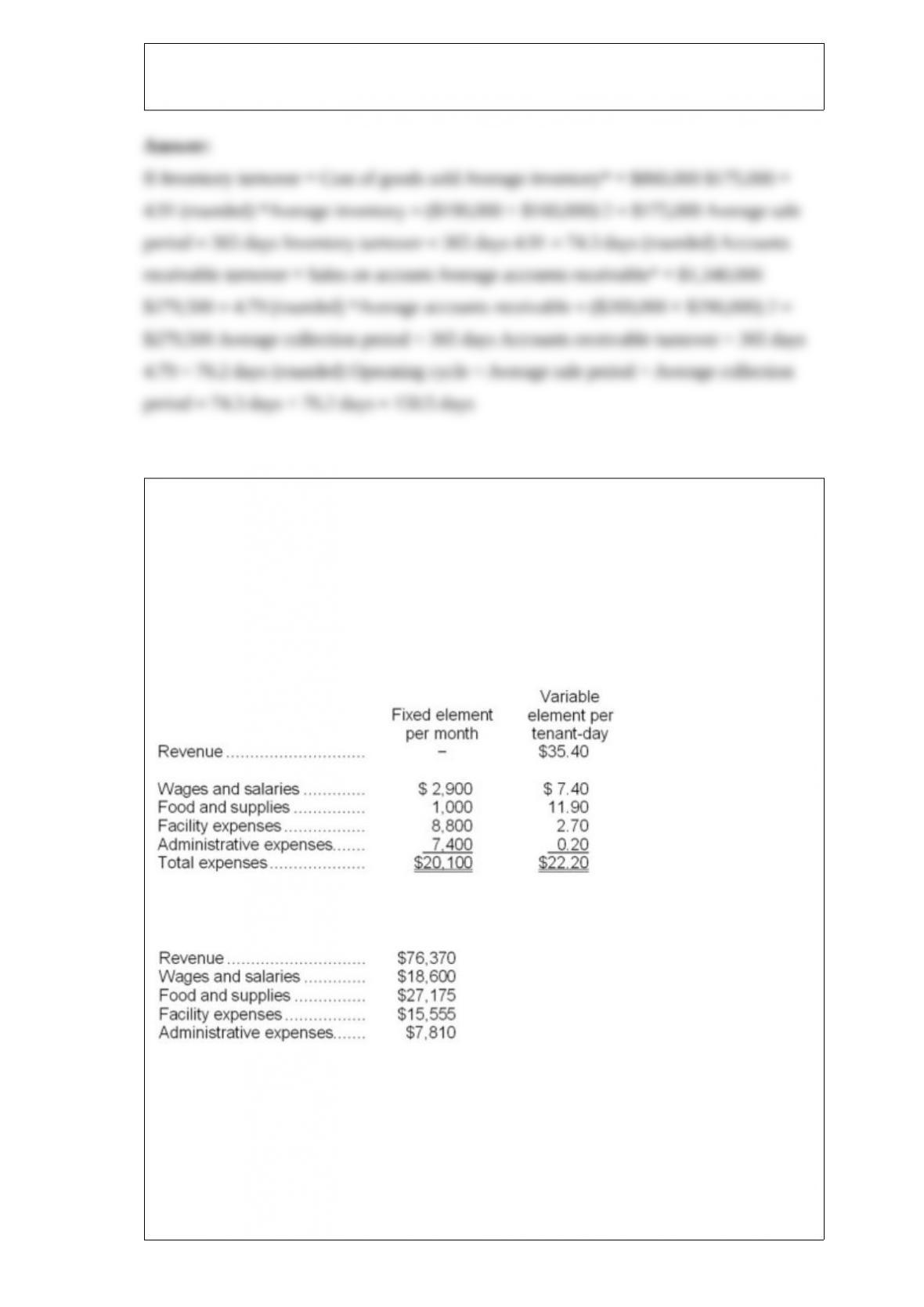

13) Nicolini Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During October, the kennel budgeted

for 2,200 tenant-days, but its actual level of activity was 2,250 tenant-days. The kennel

has provided the following data concerning the formulas used in its budgeting and its

actual results for October:

Data used in budgeting:

Actual results for October:

The administrative expenses in the planning budget for October would be closest to:

A.$7,636

B.$7,810

C.$7,850

D.$7,840

14) The cost of goods manufactured for July is:

A.$210,000

B.$205,000

C.$208,000

D.$207,000

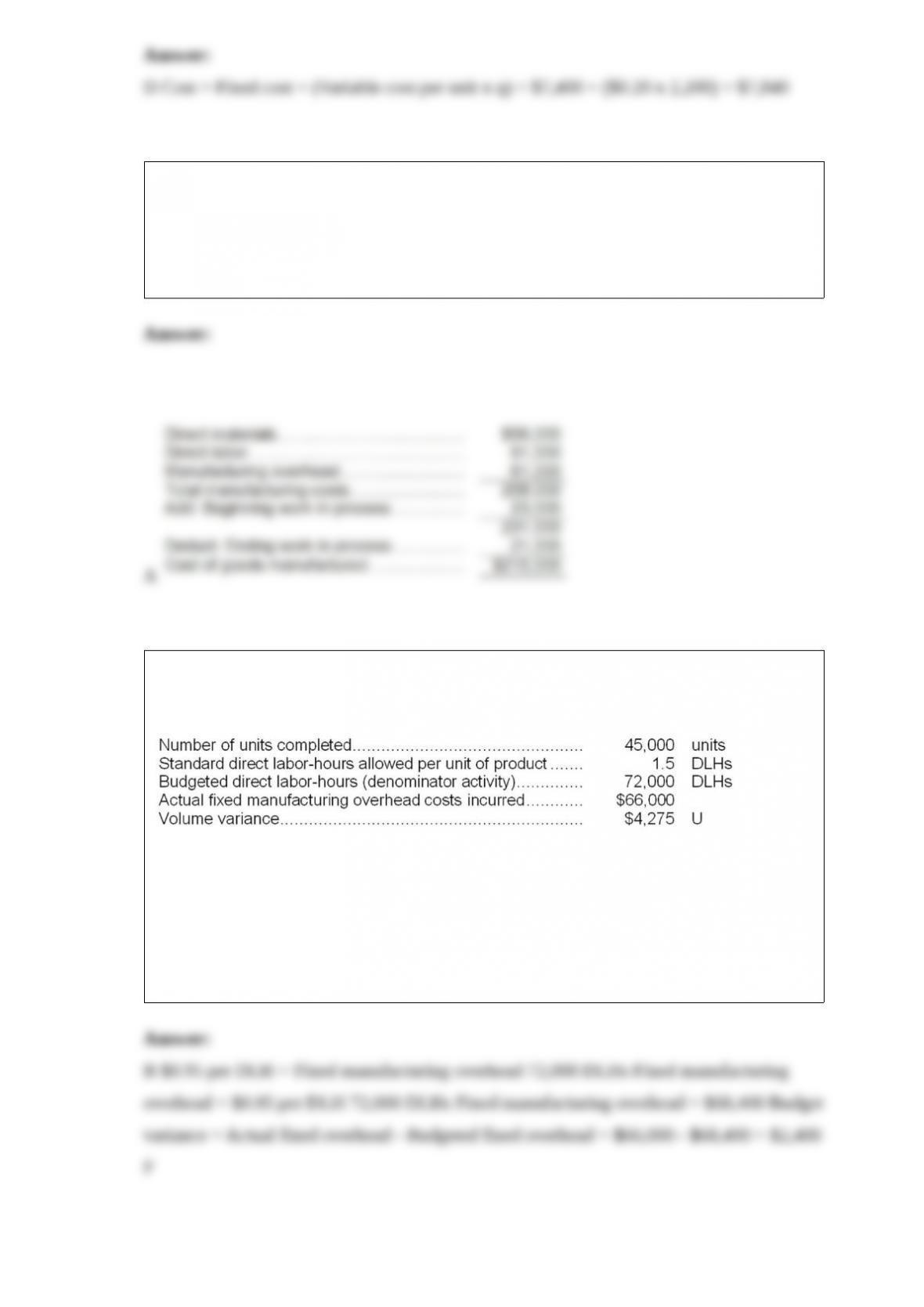

15) The Murray Corporation makes and sells a single product. The company recorded

the following activity and cost data for May:

The fixed component of the predetermined overhead rate is $0.95 per direct labor-hour.

The fixed manufacturing overhead budget variance for May was:

A.$2,400 U

B.$2,400 F

C.$6,000 U

D.$6,000 F

16) The LFG Corporation makes and sells a single product, Product T. Each unit of

Product T requires 1.4 direct labor-hours at a rate of $9.80 per direct labor-hour. The

direct labor workforce is fully adjusted each month to the required workload. LFG

Corporation needs to prepare a Direct Labor Budget for the second quarter of next year.

The company has budgeted to produce 24,000 units of Product T in June. The finished

goods inventories on June 1 and June 30 were budgeted at 600 and 800 units,

respectively. Budgeted direct labor costs for June would be:

A.$332,024

B.$329,280

C.$235,200

D.$326,536

17) The net present value of the entire project is closest to:

A.$255,230

B.$167,777

C.$153,617

D.$252,000

18) How many units of product O24M should be produced each month?

A.0

B.276

C.1,304

D.620