King Corporation has a defined benefit pension plan. One of its employees has vested

benefits under the plan, which will pay him $40,000 annually for life starting with the

first payment of $40,000 on the day he retires at the age of 65. The employee has just

reached the age of 50. King consulted standard mortality tables to come up with a life

expectancy of 80 for this employee. The implicit interest rate under the plan is 9%.

Required:

a. What will be the present value of the pension obligation at the time of the employee’s

retirement?

b. What is the present value of the pension obligation at the current time?

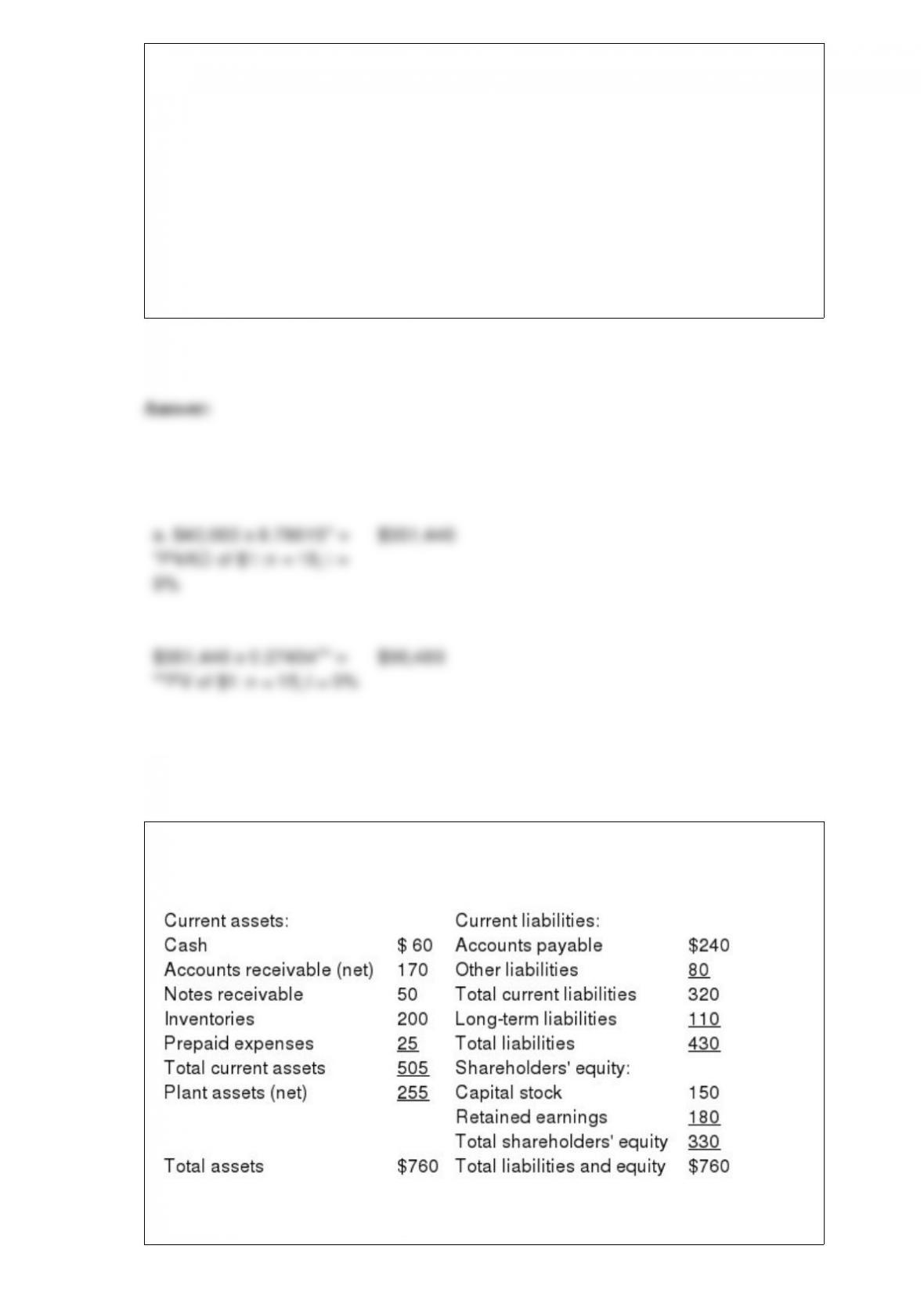

The following partial balance sheet ($ in thousands) for Paisano Seafood Inc. is shown

below.

Quick assets total:

a. $60.

b. $230.

c. $280.

d. $305.

On February 1, 2016, Pearson Corporation became the lessee of equipment under a

five-year, noncancelable lease. The estimated economic life of the equipment is eight

years. The fair value of the equipment was $600,000. The lease does not meet the

definition of a capital lease in terms of a bargain purchase option, transfer of title, or the

lease term. However, Pearson must classify this as a capital lease if the present value of

the minimum lease payments is at least

a. $600,000.

b. $540,000.

c. $450,000.

d. $405,000.

JFS Co. changed from straight-line to double-declining-balance depreciation. The

journal entry to record the change includes:

a. A credit to accumulated depreciation.

b. A debit to accumulated depreciation.

c. A debit to a depreciable asset.

d. The change does not require a journal entry.

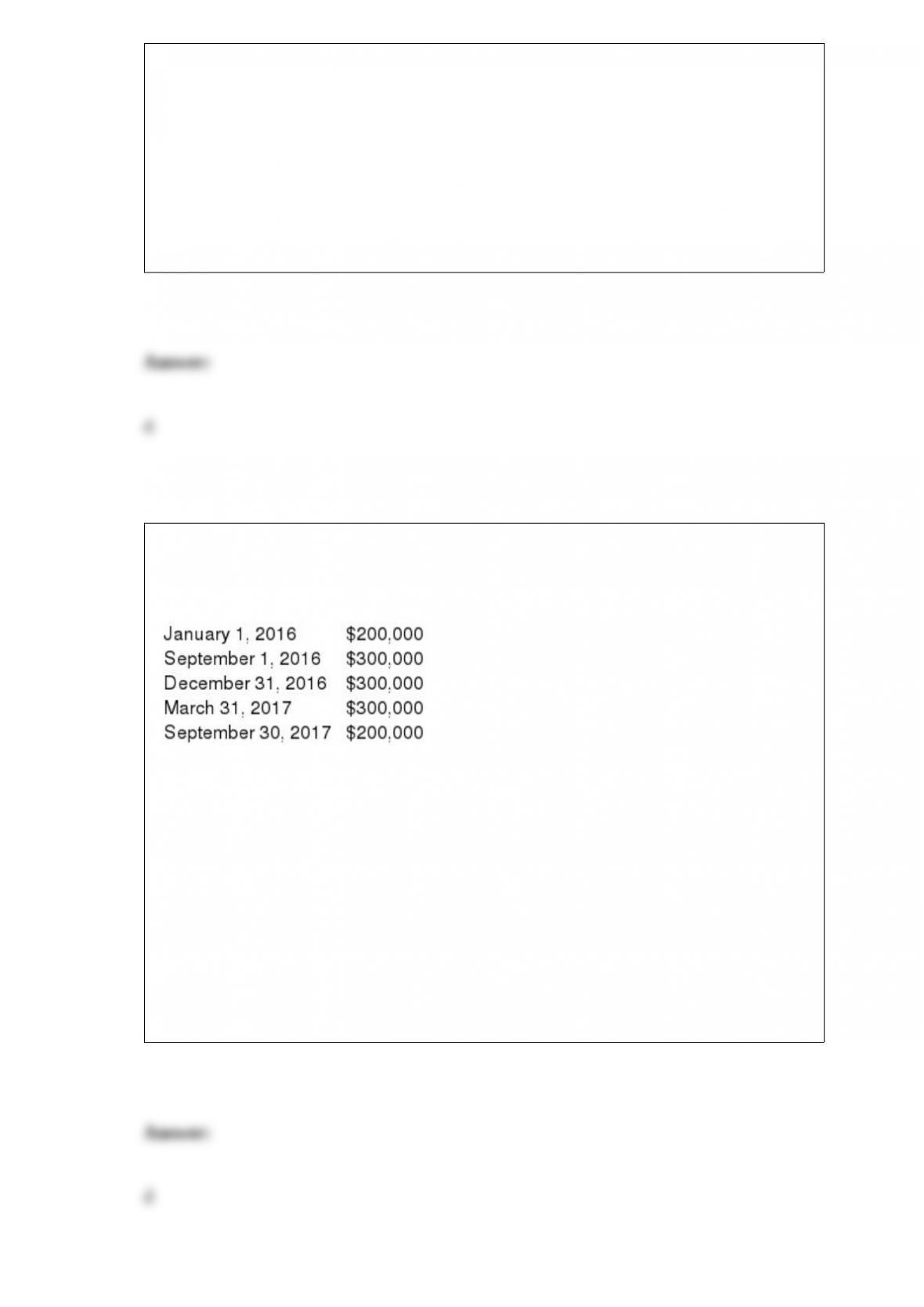

On January 1, 2016, Kendall Inc. began construction of an automated cattle feeder

system. The system was finished and ready for use on September 30, 2017.

Expenditures on the project were as follows:

Kendall borrowed $750,000 on a construction loan at 12% interest on January 1, 2016.

This loan was outstanding throughout the construction period. The company had

$4,500,000 in 9% bonds payable outstanding in 2016 and 2017. Average accumulated

expenditures for 2017 was:

a. $ 536,000.

b. $1,236,000.

c. $1,200,000.

d. $1,036,000.

Which of the following Statements of Financial Accounting Concepts defines the 10

elements of financial statements?

a. SFAC 4.

b. SFAC 3.

c. SFAC 5.

d. SFAC 6.

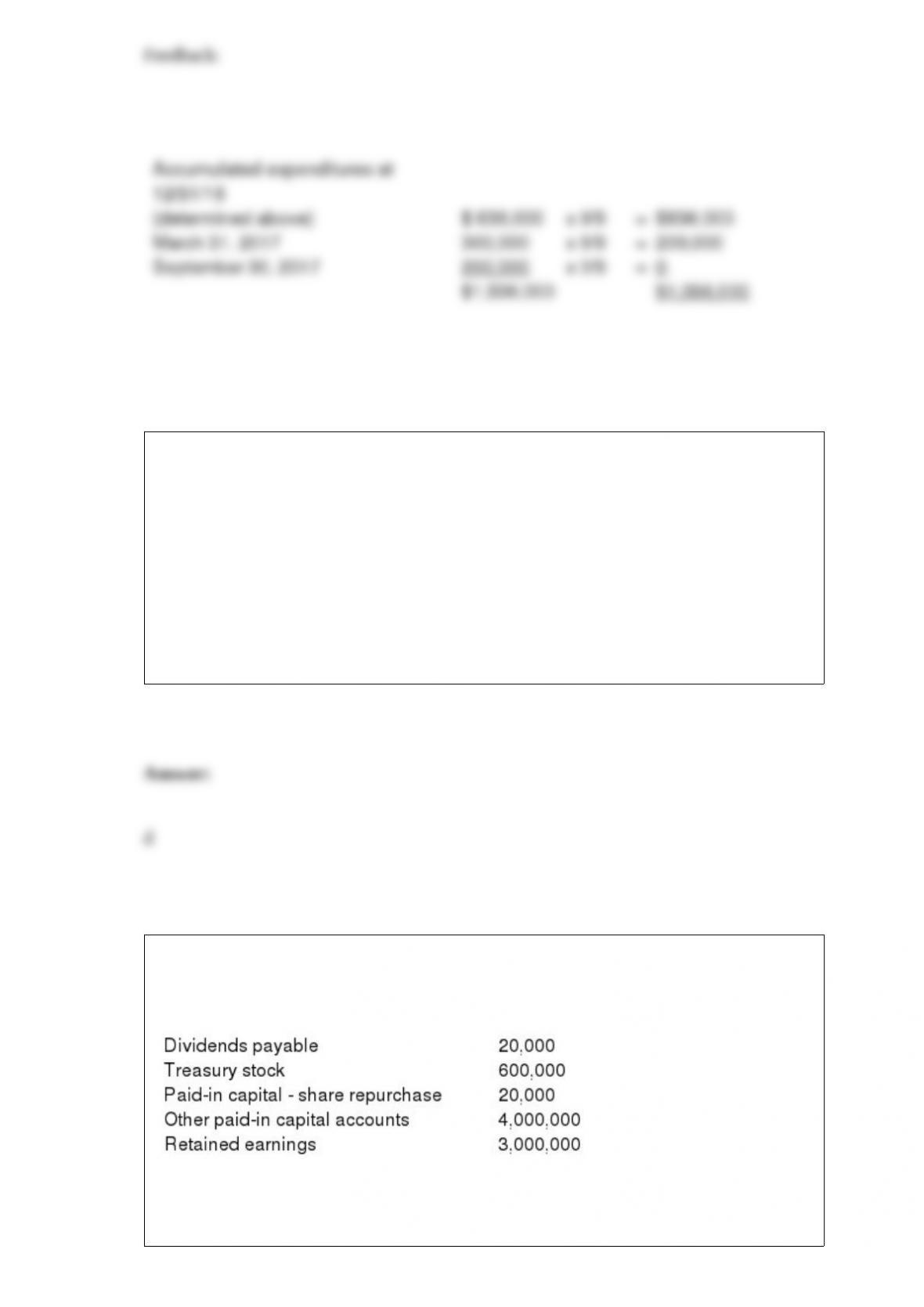

What was shareholders’ equity as of December 31, 2016?

As of December 31, 2016, Warner Corporation reported the following:

During 2017, half of the treasury stock was resold for $240,000; net income was

$600,000; cash dividends declared were $1,500,000; and stock dividends declared were

$500,000.

a. $7,020,000.

b. $6,440,000.

c. $6,420,000.

d. $6,400,000.

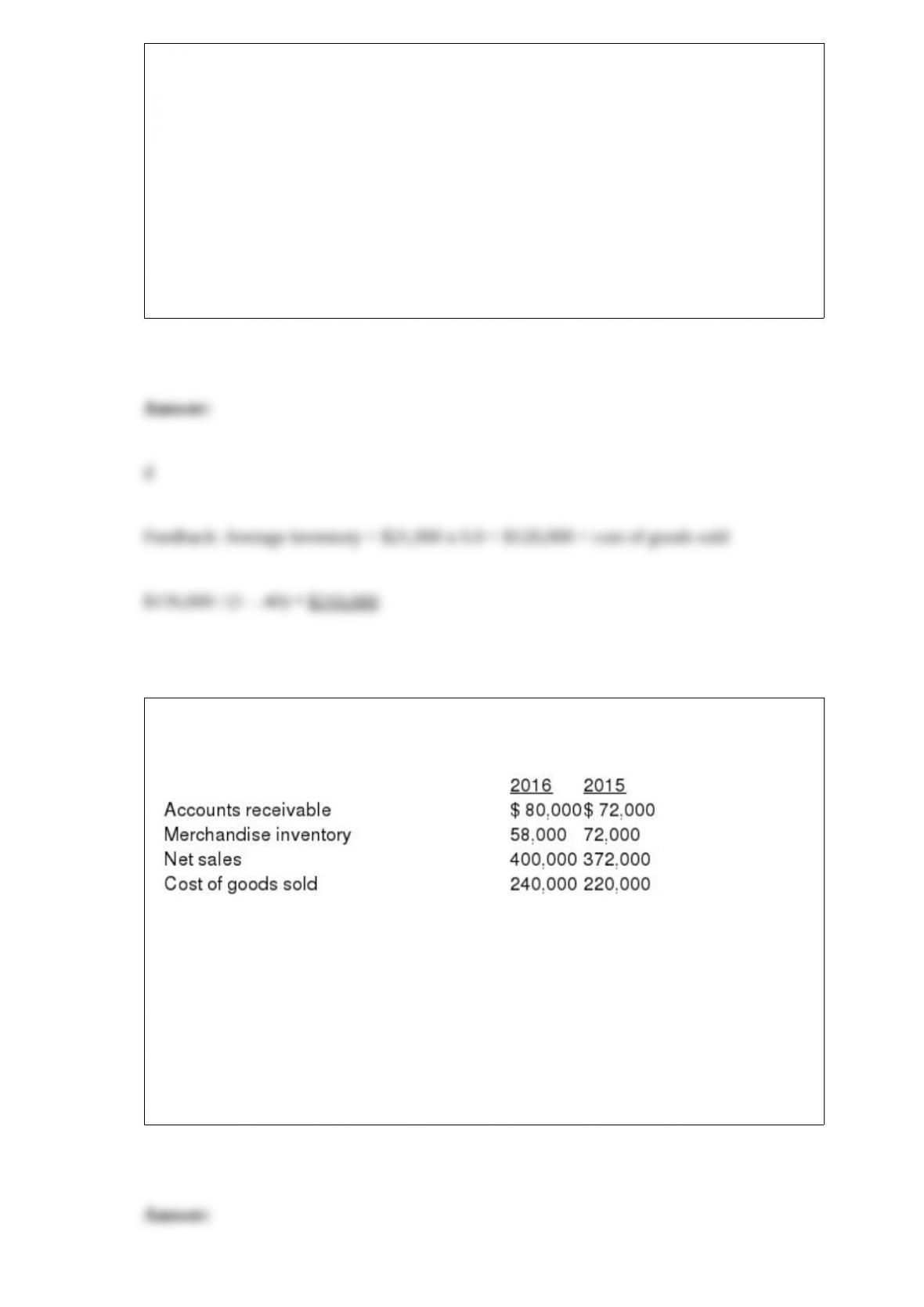

Robertson Corporation’s inventory balance was $22,000 at the beginning of the year

and $20,000 at the end. The inventory turnover ratio for the year was 6.0 and the gross

profit ratio 40%. What were net sales for the year?

a. $126,000.

b. $200,000.

c. $120,000.

d. $210,000.

Excerpts from Huckabee Company’s December 31, 2016 and 2015, financial statements

are presented below:

Huckabee’s 2016 receivables turnover (rounded) is:

a. 3.69.

b. 5.00.

c. 5.26.

d. 3.16.

Jack Corporation purchased a 20% interest in Jill Corporation for $1,500,000 on

January 1, 2016. Jack can significantly influence Jill. On December 10, 2016, Jill

declared and paid $1 million in dividends. Jill reported a net loss of $6 million for the

year. What amount of loss should Jack report in its income statement for 2016 relative

to its investment in Jill?

a. $1,000,000.

b. $1,200,000.

c. $1,400,000.

d. $1,500,000.

When an accounting change is reported under the retrospective approach, prior years’

financial statements are:

a. Revised to reflect the use of the new principle.

b. Reported as previously prepared.

c. Left unchanged.

d. Adjusted using prior period adjustment procedures.

GAAP that covers revenue recognition for multiple-element arrangements requires that

a seller recognize revenue for a particular part if:

a. The part has value on a stand-alone basis.

b. Customer acceptance of the part is not contingent on successful delivery of a later

part.

c. The part constitutes at least a “preponderance of the fair value” of the total

arrangement.

d. Both the part has value on stand-alone basis and customer acceptance of the part is

not contingent on successful delivery of a later part are required.

Purple Cab Company had 50,000 shares of common stock outstanding on January 1,

2016. On April 1, 2016, the company issued 20,000 shares of common stock. The

company had outstanding fully vested incentive stock options for 5,000 shares

exercisable at $10 that had not been exercised by its executives. The average market

price of common stock was $12. The company reported net income in the amount of

$269,915 for 2016. What is the basic earnings per share (rounded)?

a. $4.10.

b. $3.86.

c. $3.60.

d. $4.15.

($ in 000s)

‘ƒPBO balance, January 1 $ 960

Service cost 150

‘ƒ Interest cost 90

Prior service cost 24

Gain from change in actuarial assumption (44)

Benefits paid (72)

‘ƒPBO balance, December 31 $1,108

Plan assets balance, January 1 $600

Actual return on plan assets 40

‘ƒ Contributions 2016 120

Benefits paid (72)

Plan assets balance, December 31 $688

Because the plan is underfunded, Dharma Initiative will report a net pension liability:

‘ƒPBO balance, December 31 $1,108

Plan assets balance, December 31 (688)

Net pension liability $ 420

Costs and prices regularly fall every year in the microcomputer industry. Briefly

indicate your recommendation and rationale for an inventory method for a firm about to

enter this industry.

Dr. Privacy, Inc. specializes in shredding office documents and destroying computer

hard drives for various clients in the U.S. In June 2016, it enters into a contract with the

U.S. government to properly discard computer hard drives. The contract specifies a

fixed fee of $50,000 for the first 25,000 hard drives, and an additional $5,000 for each

incremental 10,000 drives. The company estimates a 65% chance of handling 25,000

drives or fewer, 30% chance of handling more than 25,000 drives but fewer than 35,000

drives, and 5% chance of handling more than 35,000 drives but fewer than 45,000

drives. Required: Assuming that the company determines transaction price as the

expected value of the consideration, what is Dr. Privacy’s estimate of the transaction

price for this contract?

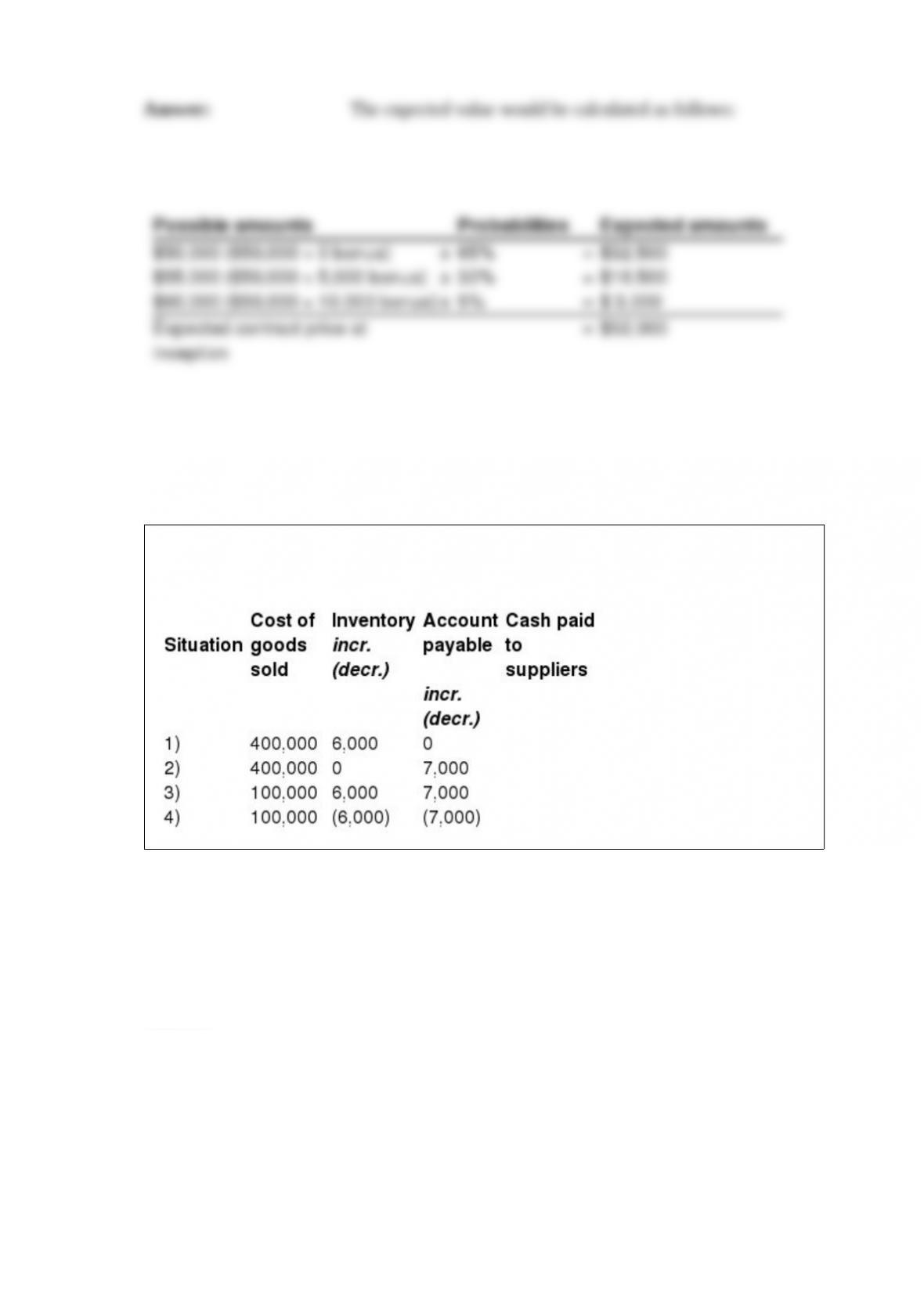

Prepare the summary entries necessary to determine the amount of cash paid to

suppliers for each of the four independent situations below.

Suppan Service began the year with a net pension liability of $56 million (underfunded

pension plan). Pension expense for the year included the following ($ in millions):

service cost, $20; interest cost, $12; expected return on assets, $8; amortization of net

gain, $4.

Required:

Prepare the appropriate general journal entry to record Suppan’s pension expense.

Unrealized holding gains and losses on securities available for sale would have the

following effects on accumulated other comprehensive income:

Briefly explain how you would arrive at the monthly payment for a 48-month loan

where the first payment is due one month from the loan date. In your explanation,

include the use of present or future value tables.

Jmart Corporation included the following disclosure note in a recent annual report:

RESTRICTED STOCK (in part)

‘¦we issued 100,000 shares of restricted stock at market prices ranging from $46.00 to

$60. ‘¦The restricted stock generally vests over three years, during which time we will

recognize total compensation expense of approximately $6 million.

ÂÂÂÂÂÂÂÂÂÂÂÂÂÂÂÂ

Required:

1) Based on the information provided in the disclosure note, determine the weighted

average market price of the restricted stock issued.

2) How much compensation expense did Jmart report for the year following the year in

which the restricted stock was issued?