1) When a multi-product factory operates at full capacity, decisions must be made about

what products to emphasize. In making such decisions, products should be ranked

based on:

A) selling price per unit

B) contribution margin per unit

C) contribution margin per unit of the constraining resource

D) unit sales volume

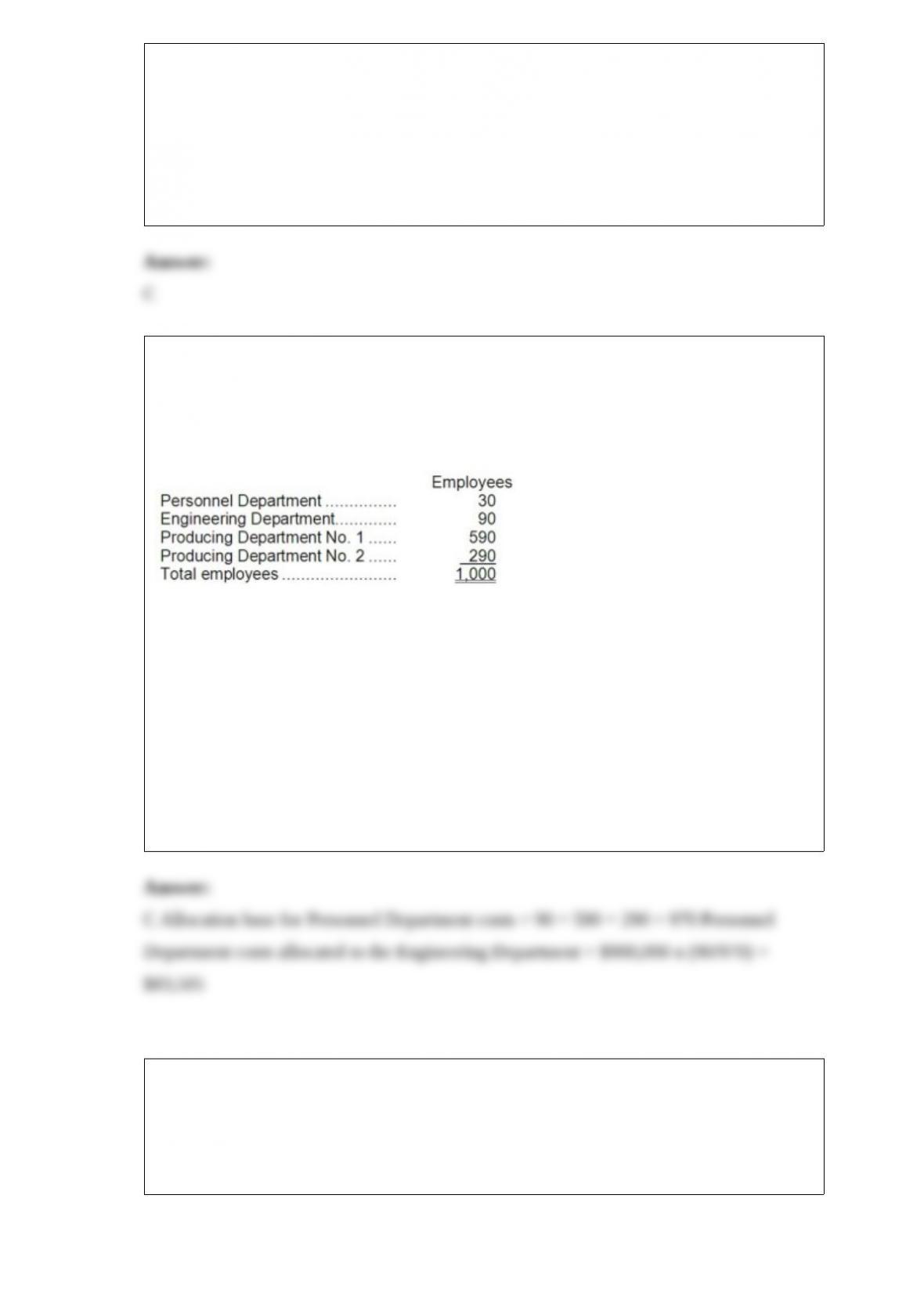

2) Anderson Corporation has two service departments and two producing departments.

The costs of the Personnel Department are allocated to other departments on the basis

of the number of employees in the departments. Departments and number of employees

are as follows:

Costs in the Personnel Department total $900,000 per year. Under the step-down

method, the costs of the Personnel Department are allocated before the costs of the

Engineering Department are allocated. The amount of this cost allocated to the

Engineering Department under the step-down method is closest to:

A.$0

B.$81,000

C.$83,505

D.$92,046

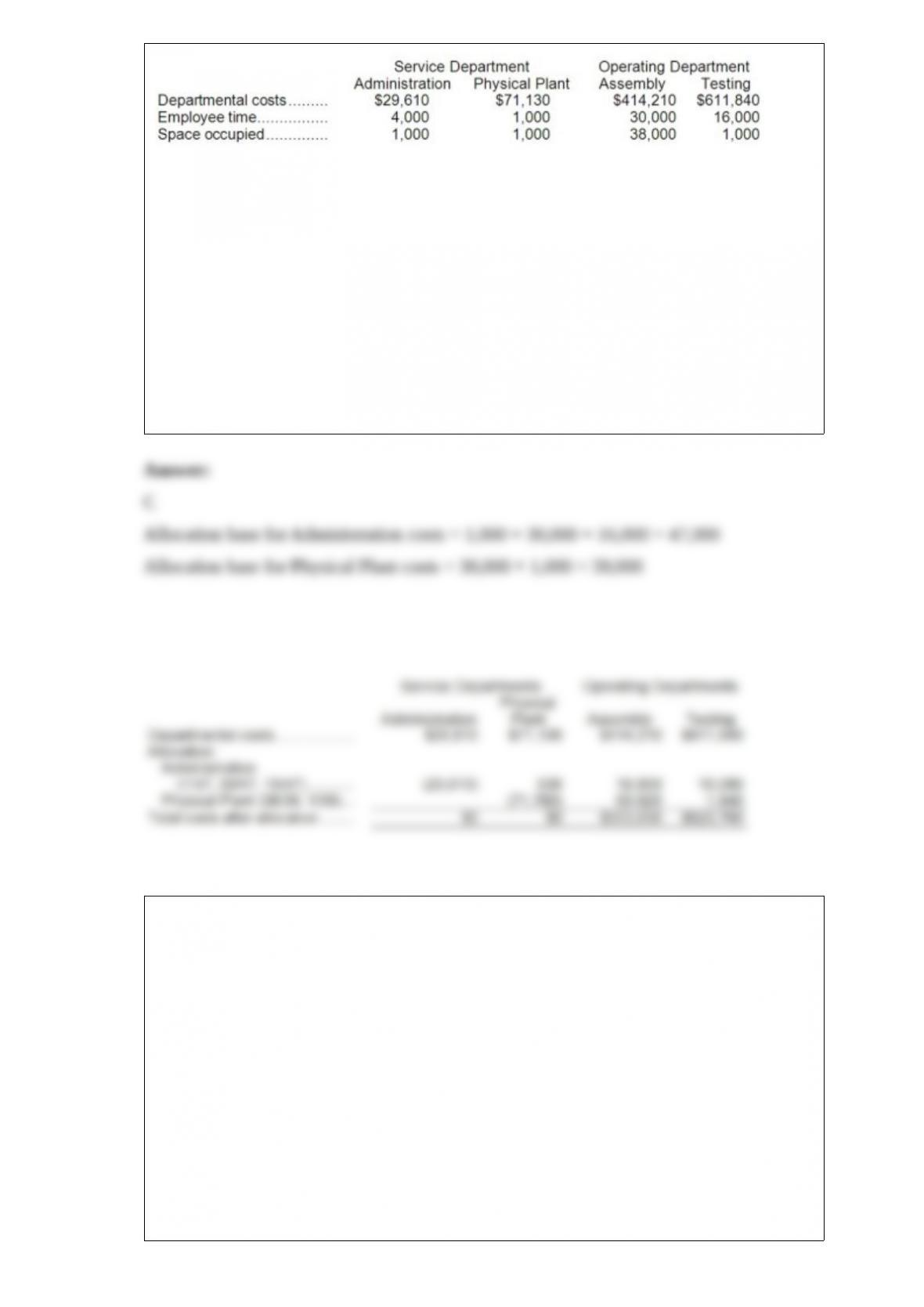

3) Cieslak, Inc., allocates service department costs to operating departments using the

step-down method. The company has two service departments, Administration and

Physical Plant, and two operating departments, Assembly and Testing. Data concerning

those departments follow:

Administration Department costs are allocated first on the basis of employee time and

Physical Plant Department costs are allocated second on the basis of space occupied.

The total Testing Department cost after allocations is closest to:

A.$623,963

B.$622,864

C.$623,760

D.$613,680

4) Roberts Corporation manufactures home cleaning products. One of the products,

Quickclean, requires 2 pounds of Material A and 5 pounds of Material B per unit

manufactured. Material A is purchased from the supplier for $0.30 per pound and

Material B is purchased for $0.50 per pound. The finished goods inventory on hand at

the end of each month should equal 4,000 units plus 25% of the next month’s sales. The

raw materials inventory on hand at the end of each month (for either Material A or

Material B) should equal 80% of the following month’s production needs.

The production budget calls for 26,000 units of Quickclean to be manufactured in June

and 32,000 units of Quickclean to be manufactured in July. On May 31 there will be

41,600 pounds of Material A and 104,000 pounds of Material B in inventory.

Assume that on January 1 the inventory of Quickclean was 8,000 units. Expected sales

in January are 14,000 units and expected sales in February are 18,000 units. The

number of units needed to be produced in January would be:

A.10,500

B.14,000

C.14,500

D.15,000

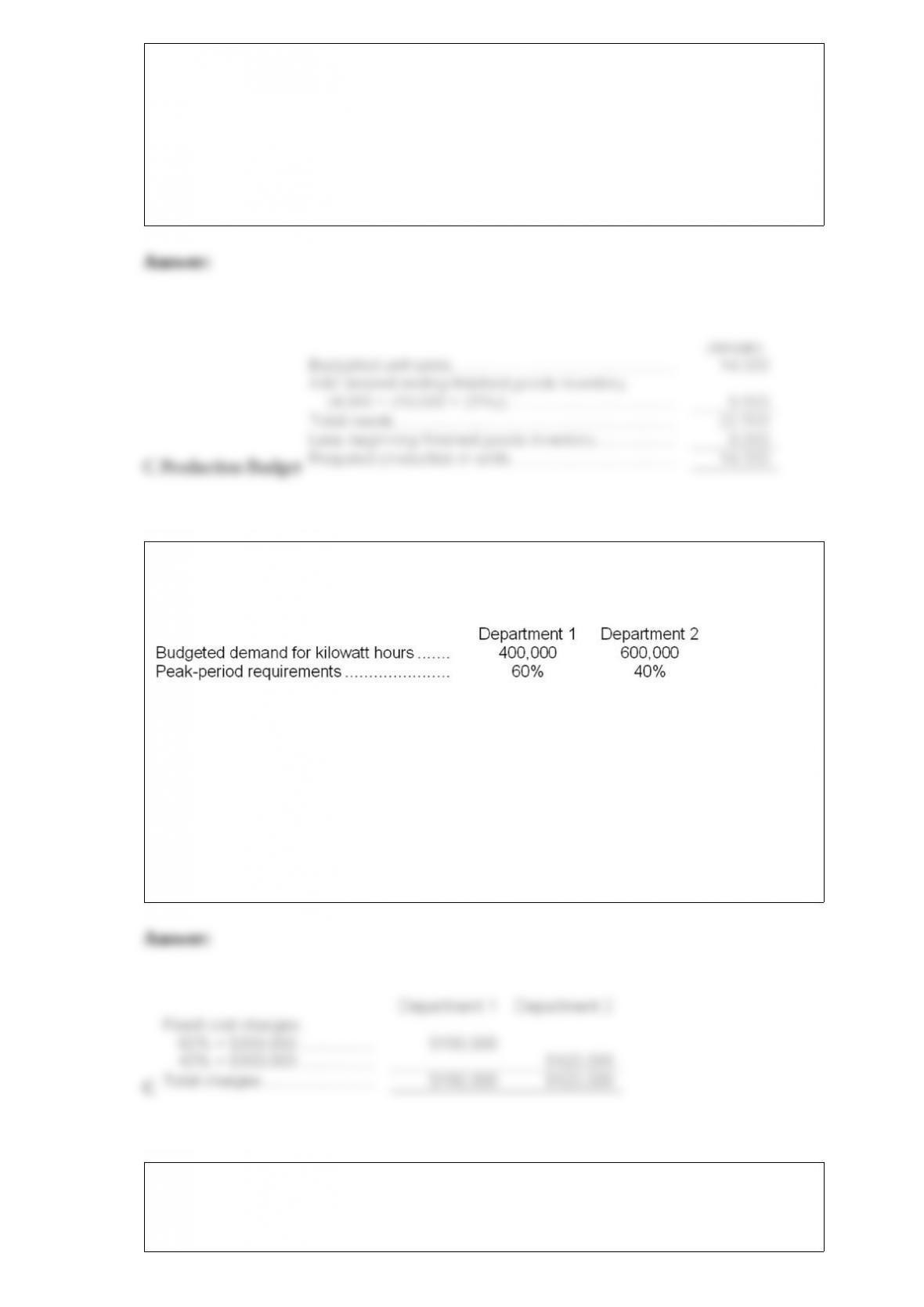

5) Charlie Company has provided the following data concerning power consumption in

the company’s two operating departments:

The company has a Power Services department which provides electrical power for the

operating departments. Fixed costs in Power Services are budgeted at $300,000 for the

year and are incurred in order to support peak-period power requirements. How much

of this cost should be charged to Department 1?

A.$120,000

B.$150,000

C.$180,000

D.$0

6) The standards for product F28 call for 2.7 pounds of a raw material that costs $16.50

per pound. Last month, 4,100 pounds of the raw material were purchased for $70,520.

The actual output of the month was 1,300 units of product F28. A total of 3,500 pounds

of the raw material were used to produce this output.

Required:

a. What is the materials price variance for the month?

b. What is the materials quantity variance for the month?

c. Prepare journal entries to record the purchase and use of the raw material during the

month. (All raw materials are purchased on account.)

7) What would the annual cost of additional supervision have to be in order for Hadley

to be indifferent between making or buying the component? (Assume everything else

remains the same.)

A) $20,000

B) $19,000

C) $18,000

D) $17,000

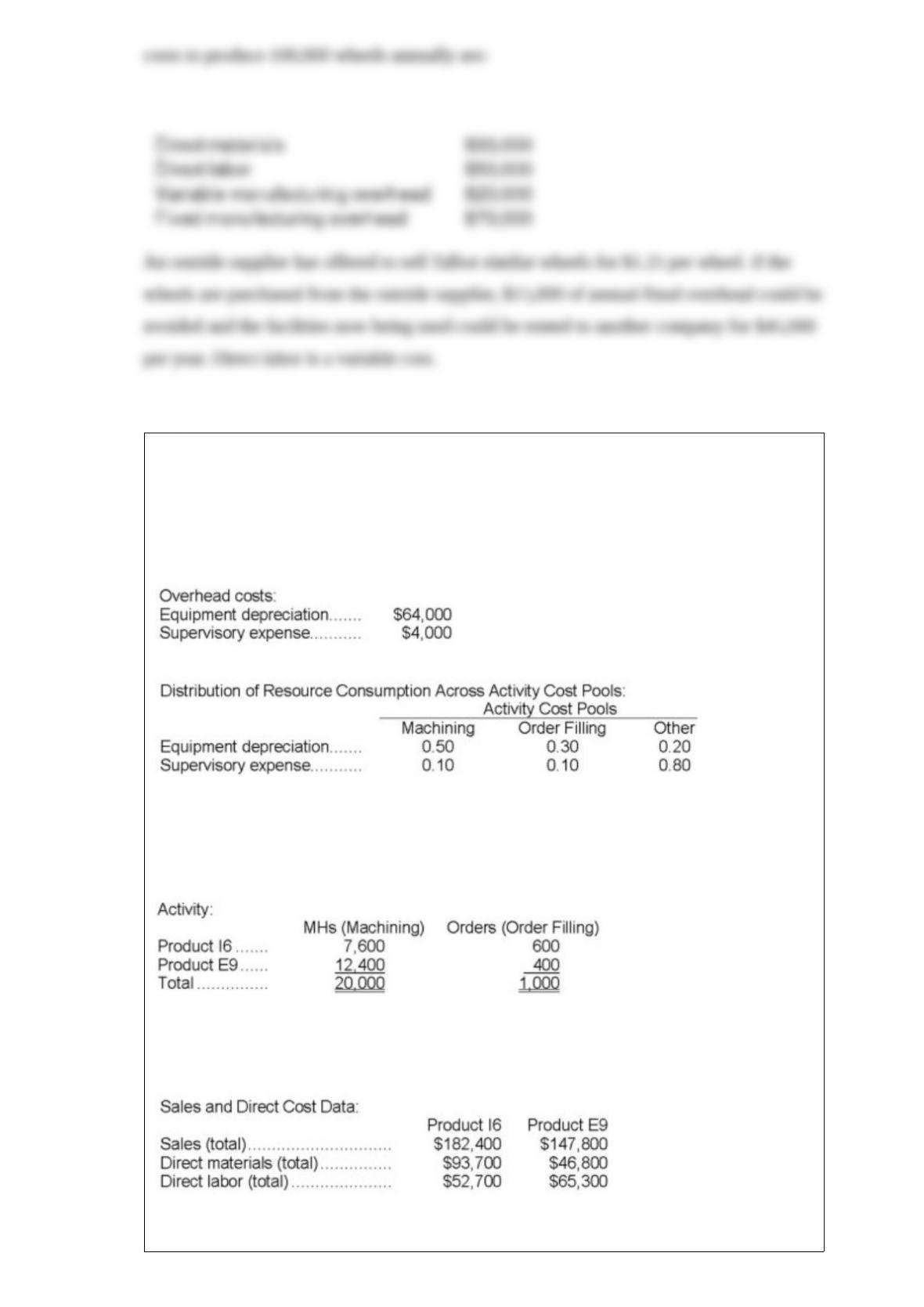

8) Vontungeln Corporation uses activity-based costing to compute product margins. In

the first stage, the activity-based costing system allocates two overhead

accounts-equipment depreciation and supervisory expense-to three activity cost

pools-Machining, Order Filling, and Other-based on resource consumption. Data to

perform these allocations appear below:

In the second stage, Machining costs are assigned to products using machine-hours

(MHs) and Order Filling costs are assigned to products using the number of orders. The

costs in the Other activity cost pool are not assigned to products.

Finally, sales and direct cost data are combined with Machining and Order Filling costs

to determine product margins.

What is the overhead cost assigned to Product I6 under activity-based costing?

A.$11,760

B.$24,072

C.$34,000

D.$12,312

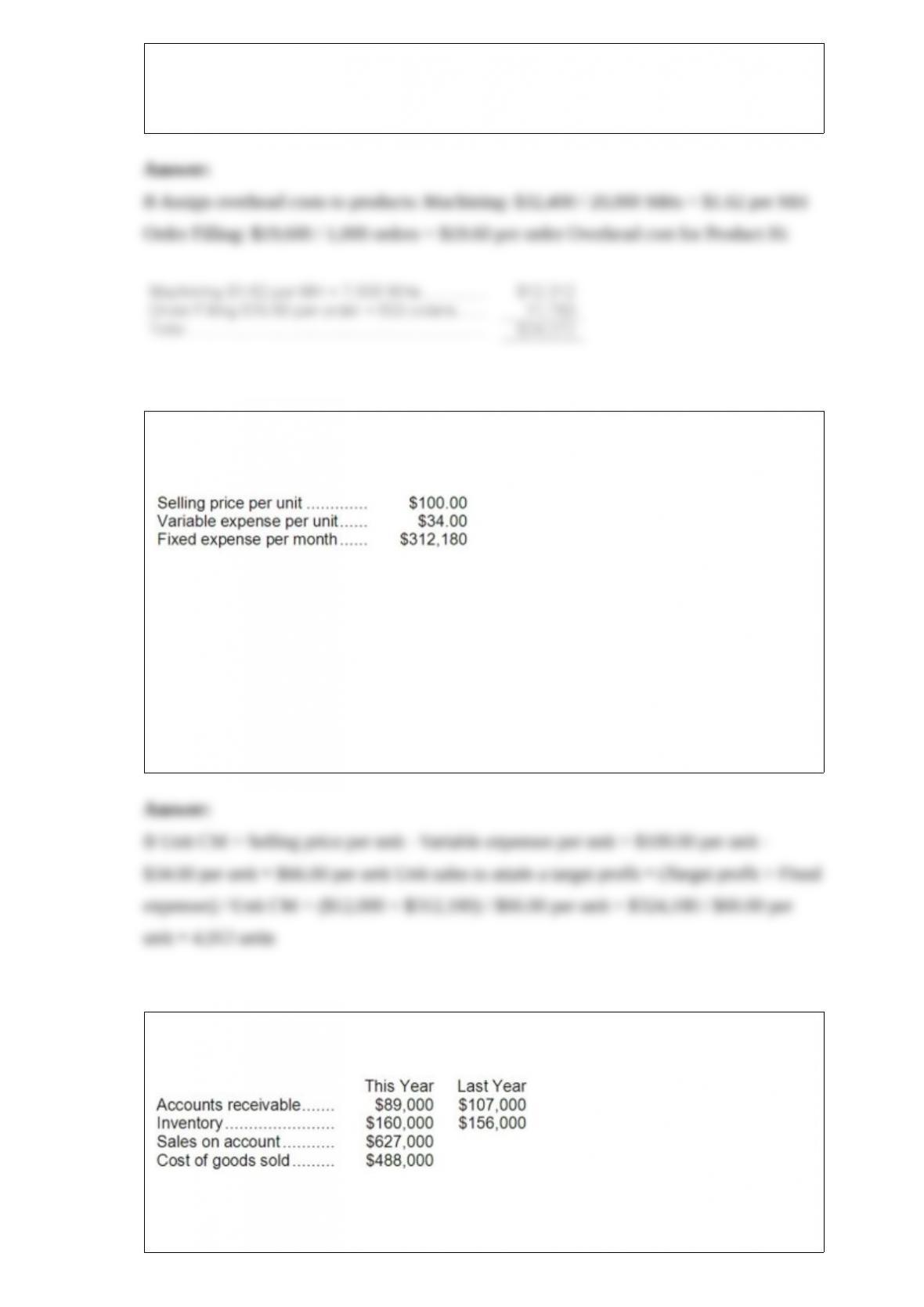

9) Upchurch Corporation produces and sells a single product. Data concerning that

product appear below:

Assume the company’s target profit is $12,000. The unit sales to attain that target profit

is closest to:

A.3,242 units

B.4,912 units

C.9,535 units

D.5,896 units

10) Kopas Corporation has provided the following data:

The inventory turnover for this year is closest to:

A.3.09

B.0.98

C.1.03

D.3.05

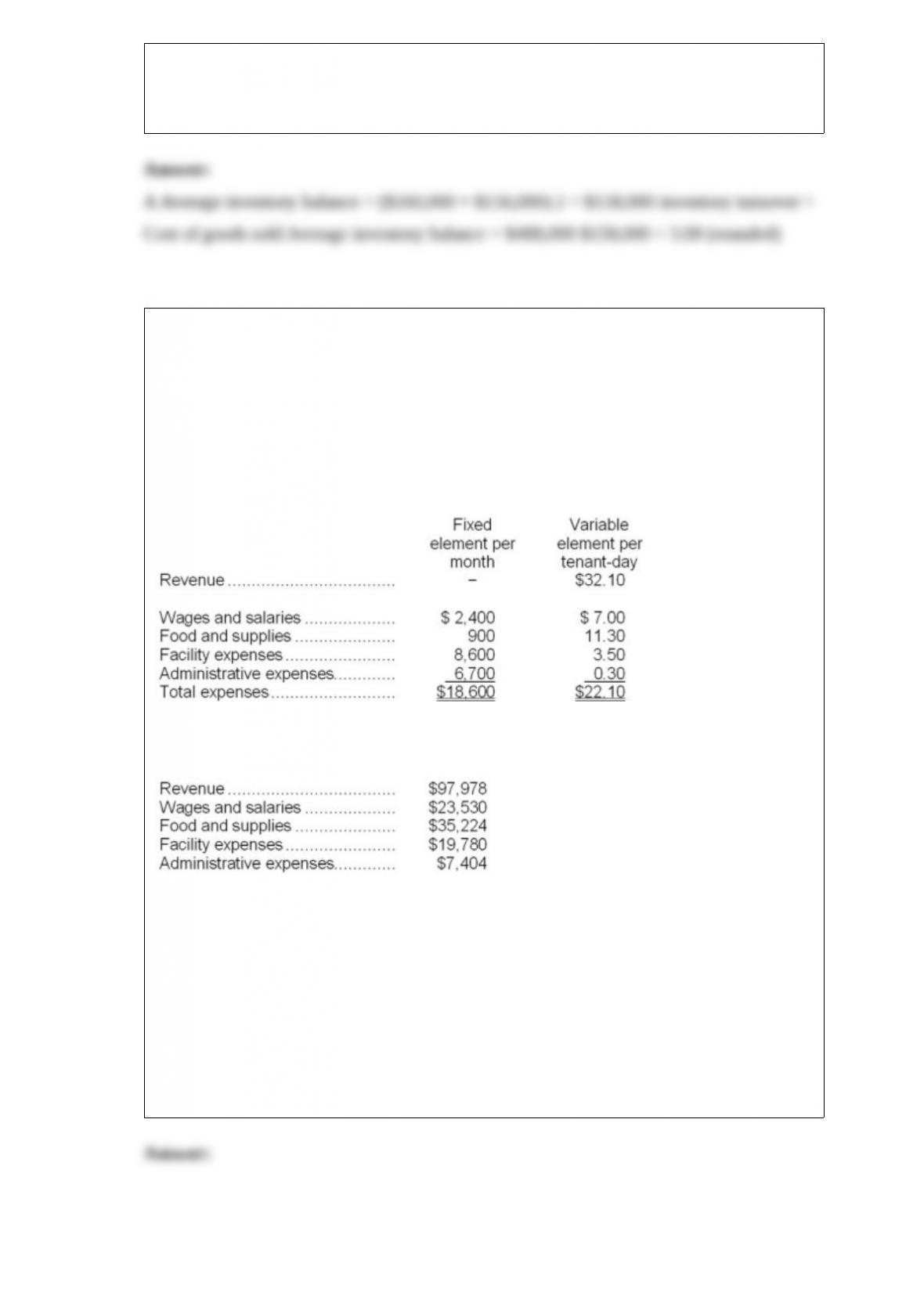

11) Pearse Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During December, the kennel budgeted

for 3,000 tenant-days, but its actual level of activity was 2,980 tenant-days. The kennel

has provided the following data concerning the formulas used in its budgeting and its

actual results for December:

Data used in budgeting:

Actual results for December:

The overall revenue and spending variance (i.e., the variance for net operating income

in the revenue and spending variance column on the flexible budget performance

report) for December would be closest to:

A.$640 F

B.$840 F

C.$640 U

D.$840 U

12) The Maxwell Corporation has a standard costing system in which variable

manufacturing overhead is assigned to production on the basis of standard

machine-hours. The following data are available for July:

Actual variable manufacturing overhead cost incurred: $22,620

Actual machine-hours worked: 1,600 hours

Variable overhead rate variance: $3,420 Unfavorable

Total variable overhead spending variance: $4,620 Unfavorable

The standard number of machine-hours allowed for July production is:

A.1,500 hours

B.1,600 hours

C.1,700 hours

D.2,270 hours