1) For a Voluntary Health and Welfare Organization, what entry is prepared when the

restriction on a cash donation is met?

A) Debit Unrestricted Net Assets, Credit Restricted Net Assets

B) Debit Unrestricted Fund Balance, Credit Restricted Fund Balance

C) Debit Restricted Fund Balance, Credit Unrestricted Fund Balance

D) Debit Temporarily Restricted Net Assets – Reclassifications out, Credit Unrestricted

Net Assets – Reclassifications in

2) The acquisition of treasury stock by a subsidiary from noncontrolling shareholders at

a price above book value

A) decreases the parent’s share of subsidiary book value and decreases the parent’s

ownership percentage

B) decreases the parent’s share of subsidiary book value and increases the parent’s

ownership percentage

C) increases the parent’s share of subsidiary book value and decreases the parent’s

ownership percentage

D) increases the parent’s share of subsidiary book value and increases the parent’s

ownership percentage

3) Approved or authorized expenditures that provide legislative control over the

expenditure budget are referred to as

A) appropriations

B) allotments

C) allocations

D) encumbrances

4) Everything else held constant, if the tax-exempt status of municipal bonds were

eliminated, then

A) the interest rates on municipal bonds would still be less than the interest rate on

Treasury bonds

B) the interest rate on municipal bonds would equal the rate on Treasury bonds

C) the interest rate on municipal bonds would exceed the rate on Treasury bonds

D) the interest rates on municipal, Treasury, and corporate bonds would all increase

5) US government bonds have no default risk because

A) they are backed by the full faith and credit of the federal government

B) the federal government can increase taxes to pay its obligations

C) they are backed with gold reserves

D) they can be exchanged for silver at any time

6) An enterprise has eight reporting segments. Five segments show an operating profit

and three segments show an operating loss. In determining which segments are

classified as reporting segments under the operating profits test, which of the following

statements is correct?

A) The test value for all segments is 10% of consolidated net profit

B) The test value for profitable segments is 10% or more of those segments reporting a

profit, and the test value for loss segments is 10% or more of those segments reporting a

loss

C) The test value for loss segments is 10% of the greater of (a) the absolute value of the

sum of those segments reporting losses, or (b) 10% of consolidated net profit

D) The test value for all segments is 10% of the greater of (a) the absolute value of the

sum of those segments reporting profits, or (b) the absolute value of the sum of those

segments reporting losses

7) Under the Uniform Probate Code, the personal representative must inform the heirs

and devisees of his or her appointment and provide other selected information within

how many days of the appointment?

A) 10 days

B) 20 days

C) 30 days

D) 60 days

8) Differences in ________ explain why interest rates on Treasury securities are not all

the same

A) risk

B) liquidity

C) time to maturity

D) tax characteristics

9) On October 4, 2010, Sooty Corporation borrowed 250,000 British pounds from a

London bank, evidenced by an interest-bearing note payable due in one year. The note

was payable in pounds. Exchange rates for pounds were:

October 4, 2010$1.59

December 31, 2010$1.55

October 4, 2011$1.61

What exchange gain or loss appeared on Sooty’s 2011 income statement?

A) a loss of $15,000

B) a loss of $5,000

C) a gain of $15,000

D) a gain of $5,000

10) The following are transactions for the city of Salem.

a.Incurred salaries of $44,000 to be paid next month.

b.Tax bills totaling $500,000 mailed to city residents.

c.Paid salaries above.

d.Computer equipment received in the amount of $11,000, to be paid in 30 days.

Required:

Analyze the above transactions by using the accounting equation for a governmental

fund.

11) Parnaby has 25,000 common stock shares outstanding and its 100%-owned

subsidiary Sandal has 5,000 common stock shares outstanding. Parnaby and Sandal do

not have any potentially dilutive securities outstanding. The separate net incomes for

Parnaby and Sandal is $150,000 and $75,000 respectively. Diluted EPS for the

consolidated company is

A) $5.00

B) $6.00

C) $7.50

D) $9.00

12) According to FASB Statement 141R, which one of the following items may not be

accounted for as an intangible asset apart from goodwill?

A) A production backlog

B) A talented employee workforce

C) Noncontractual customer relationships

D) Employment contracts

13) Which of the following statements is true?

A) A liquid asset is one that can be quickly and cheaply converted into cash

B) The demand for a bond declines when it becomes less liquid, decreasing the interest

rate spread between it and relatively more liquid bonds

C) The differences in bond interest rates reflect differences in default risk only

D) The corporate bond market is the most liquid bond market

14) Anthony Company declared and paid $20,000 of dividends during 2011 . The

schedule of dividends follows:

Date Dividend Declared & Paid Amount Paid

March 31, 2011$5,000

June 30, 2011$5,000

September 30, 2011$5,000

December 31, 2011$5,000

Anthony Company was acquired on June 1, 2011 by Google Company. Google

acquired 100 percent of Anthony Company. Both companies have a December 31 fiscal

year end. What is the amount of preacquisition dividends in 2011?

A) 0

B) $5,000

C) $10,000

D) $15,000

15) Firms must conduct impairment tests more frequently than annually when

A) other shareholders hold more than 50% interest

B) a more-likely-than-not expectation exists that a reporting unit will be sold or

disposed of

C) a specific unit does not have publicly traded stock

D) using the equity method

16) Which of the following is a true statement regarding the recording of a transaction

which involves foreign currency?

A) A transaction is always settled in the currency in which it is denominated

B) A transaction is always measured in the currency in which it is denominated

C) A transaction is always settled in the currency in which it is measured

D) A transaction is always recorded in the currency in which it is denominated

17) The proper sequence of events is

A) purchase order, appropriation, encumbrance, expenditure

B) purchase order, encumbrance, expenditure, appropriation

C) appropriation, encumbrance, purchase order, expenditure

D) appropriation, purchase order, encumbrance, expenditure

18) Sandpiper Inc. acquired a 30% interest in Shore Corporation for $27,000 cash on

January 1, 2011, when Shore’s stockholders’ equity consisted of $30,000 of capital stock

and $20,000 of retained earnings. Shore Corporation reported net income of $18,000 for

2011 . The allocation of the $12,000 excess of cost over book value acquired on January

1 is shown below, along with information relating to the useful lives of the items:

Overvalued receivables (collected in 2011)$(600)

Undervalued inventories (sold in 2011)2,400

Undervalued building (6 years’ useful life remaining at January 1, 2011)3,600

Undervalued land900

Unrecorded patent (8 years’ economic life remaining at January 1, 2011)3,200

Undervalued accounts payable (paid in 2011) (300)

Total of excess allocated to identifiable assets and liabilities9,200

Goodwill 2,800

Excess cost over book value acquired$12,000

Required:

Determine Sandpiper’s investment income from Shore for 2011 .

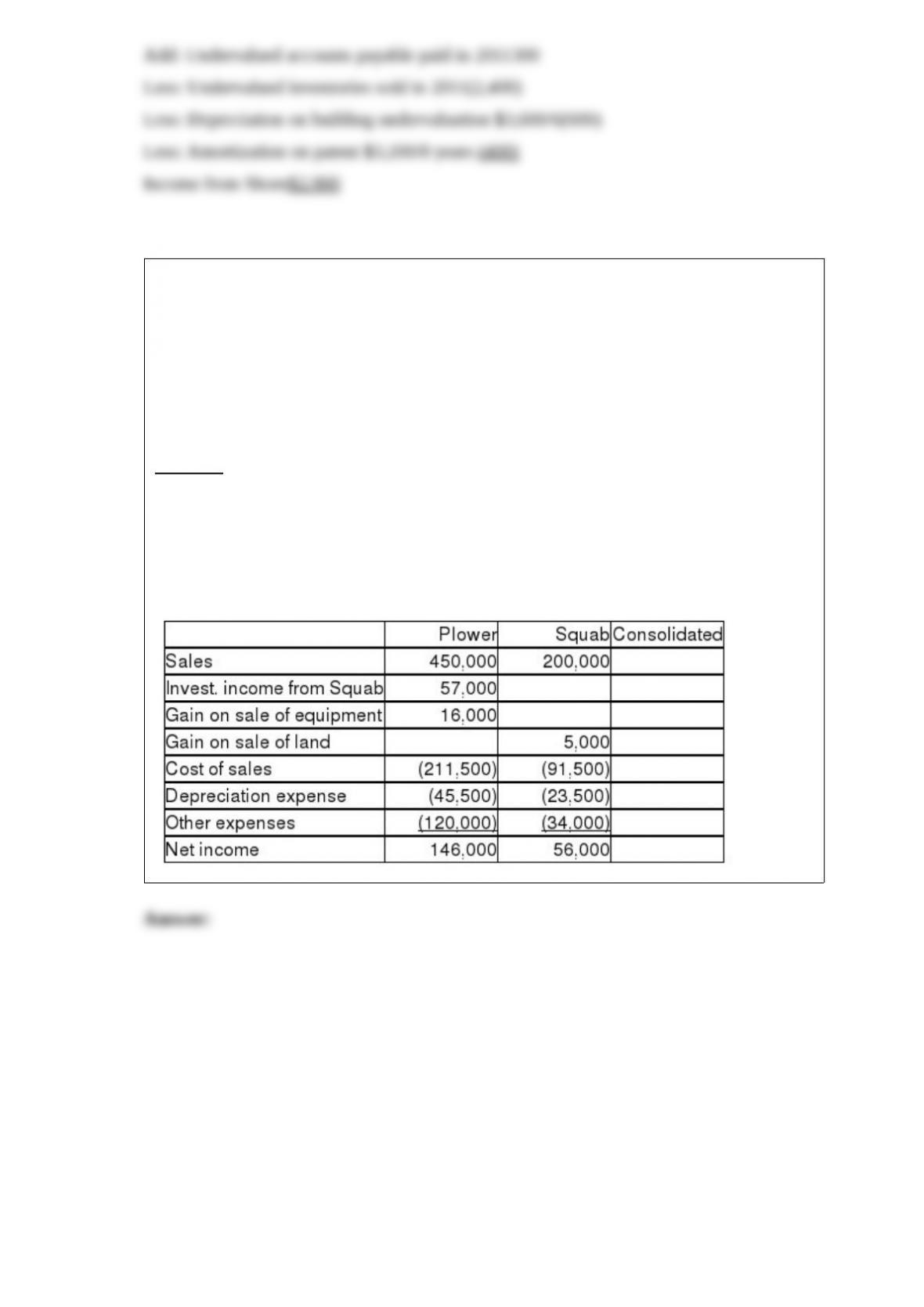

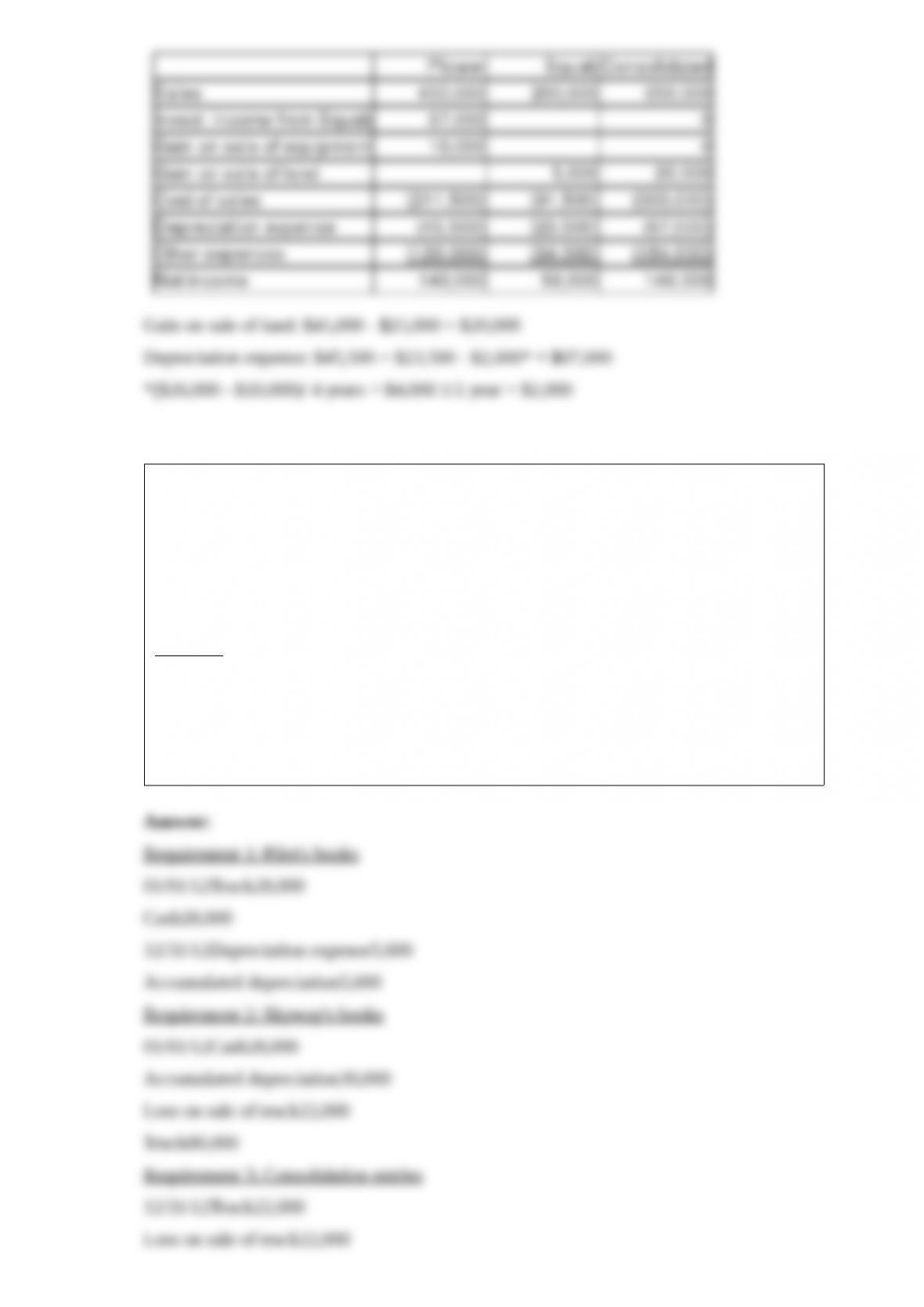

19) Plower Corporation acquired all of the outstanding voting common stock of the

Squab Corporation several years ago when the book values and fair values of Squab’s

net assets were equal.

On April 1, 2010, Plower sold land that cost $25,000 to Squab for $40,000. Squab

resold the land for $45,000 on December 1, 2012 .

On July 1, 2012, Plower sold equipment with a book value of $10,000 to Squab for

$26,000. Squab is depreciating the equipment over a four-year period using the

straight-line method. The equipment has no salvage value.

Required:

The first two columns in the working papers presented below summarize income

statement information from the separate company financial statements of Plower and

Squab for the year ended December 31, 2012 . Fill in the consolidated working paper

columns to show how each of the items from the separate company reports will appear

in the consolidated income statement for the year ended December 31, 2012 .

20) Several years ago, Pilot International purchased 70% of the outstanding stock of

Skyway Incorporated, at a time when Skyway’s book values were equal to its fair

values. On January 1, 2009, Skyway purchased a truck for $80,000 which had no

salvage value with a useful life of 8 years, depreciated on a straight-line basis. On

January 1, 2012, Skyway sold the truck to Pilot Corporation for $28,000. The truck was

estimated to have a five-year remaining life on this date, and no salvage value. All

affiliates use the straight-line depreciation method.

Required:

Prepare all relevant entries with respect to the truck.

1>Record the journal entries on Pilot’s books for 2012 .

2>Record the journal entries on Skyway’s books for 2012 .

3>Prepare the consolidation entries required for Pilot and subsidiary for 2012 as a result

of this transaction.

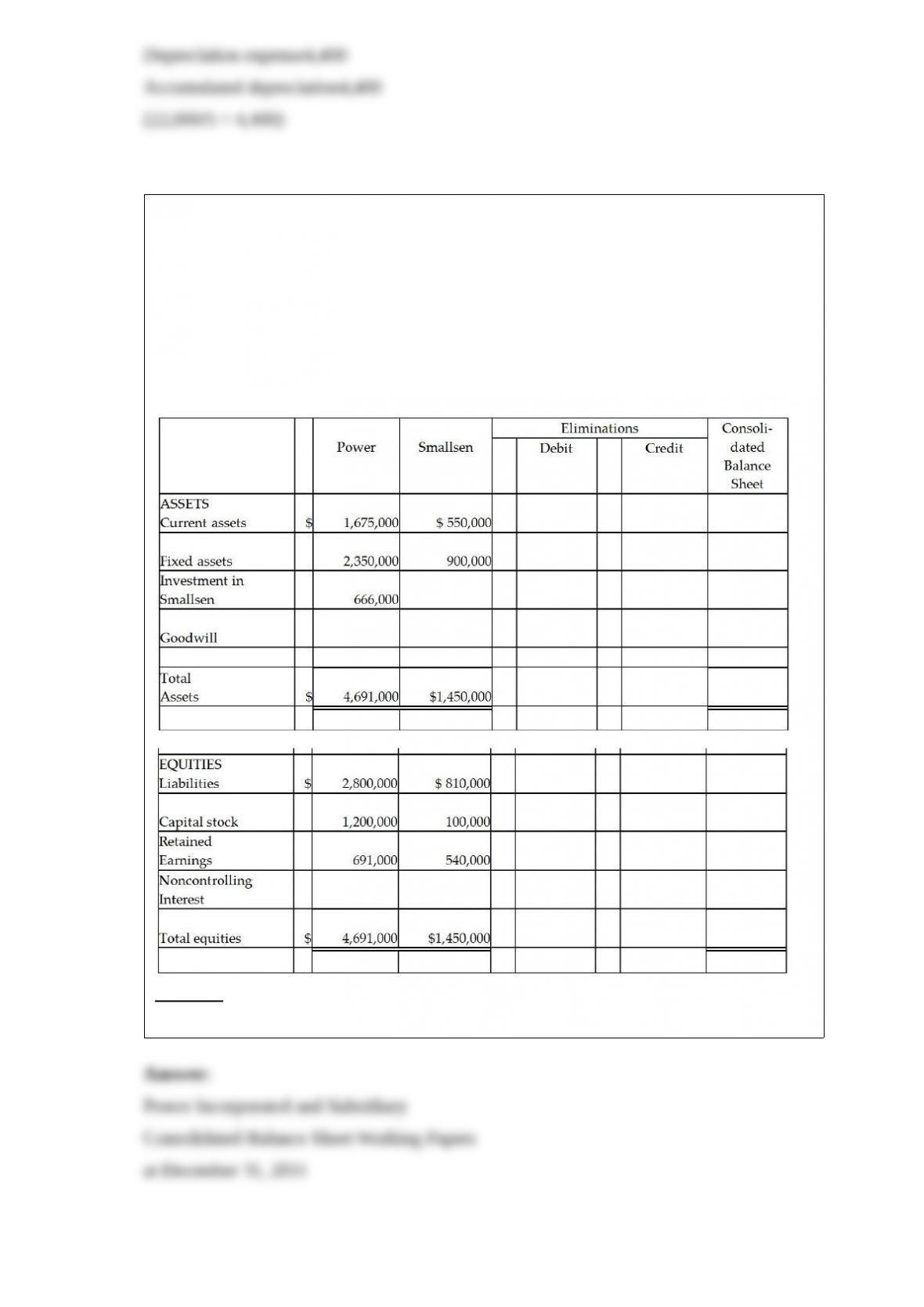

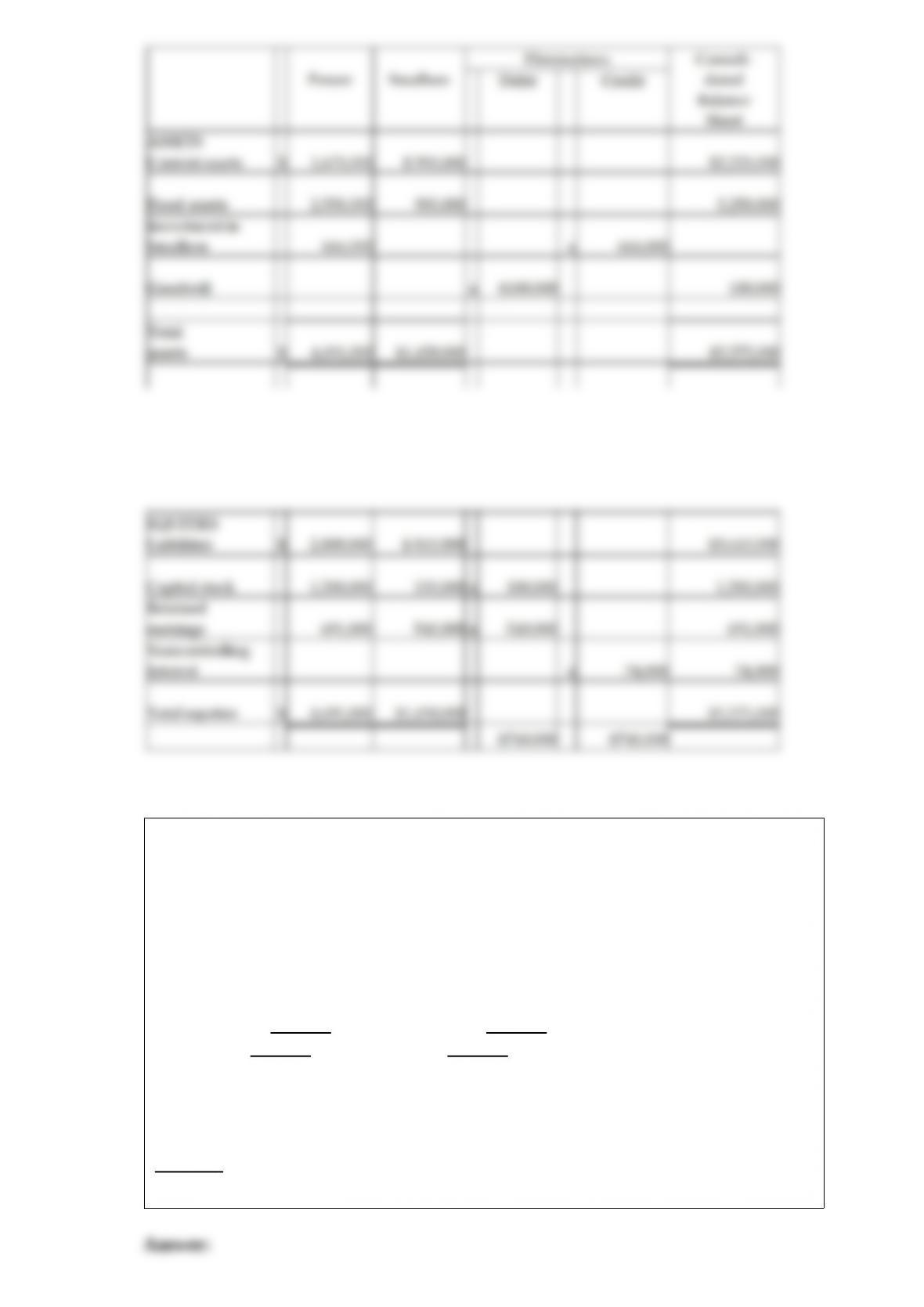

21) On January 2, 2011, Power Incorporated paid $630,000 for a 90% interest in

Smallsen Company. Smallsen’s equity at that time amounted to $600,000, and their

book values for assets and liabilities recorded approximated their fair values. Smallsen

did not issue any additional stock in 2011 . At December 31, 2011, the two companies’

balance sheets are summarized as follows:

Power Incorporated and Subsidiary

Consolidated Balance Sheet Working Papers

at December 31, 2011

Required: Complete the consolidation worksheet for Power Incorporated and

Subsidiary at December 31, 2011 .

22) The Catt, Dogg, and Eustus partnership was dissolved by the partners in early

2011 . On March 1, the partners prepared the following financial statement before

commencement of final liquidation:

Cash$80,000Accounts payable$125,000

Accounts Receivable160,000Notes payable70,000

Inventory130,000Loan from Dogg5,000

Loan to Catt10,000Catt, capital (20%)130,000

Loan to Eustus15,000Dogg, capital (20%)95,000

Plant assets-net210,000Eustus, capital(60%)180,000

Total assets$605,000Total liab./equity$605,000

Liquidation events in March were as follows:

– Receivables recorded at $120,000 were collected at $110,000;

– Inventory recorded at cost of $80,000 was sold for $60,000;

– Plant assets with a book value of $100,000 were sold for $140,000.

Required:

Determine how the available cash on March 31, 2011 should be distributed.