1) When the stated rate of interest exceeds the effective rate, the present value of the

note receivable will be less than its face value.

2) In most situations, an auditor issues a qualified opinion or disclaims an opinion.

3) Verifiability and predictive value are two ingredients of faithful representation.

4) The objective of financial reporting is the foundation of the conceptual framework.

5) A controlling interest occurs when one corporation acquires a voting interest of more

than 50 percent in another corporation.

6) The present value of an ordinary annuity is the present value of a series of equal rents

withdrawn at equal intervals.

7) A company discloses gain contingencies in the notes only when a high probability

exists for realizing them.

8) While IFRS requires an impairment test at each reporting date for long-lived assets,

it requires no such test for intangibles once a legal or useful life has been determined.

9) The asset turnover ratio is computed by dividing net sales by ending total assets.

10) Examples of taxable temporary differences are subscriptions received in advance

and advance rental receipts.

11) The SEC requires that companies report to it certain substantive information that is

not found in their annual reports.

12) Under IFRS, bond issue costs are recorded as an asset.

13) Both U.S. GAAP and IFRS permit the use of the LIFO method to account for

inventories.

14) Under the accrual basis of accounting, net income is usually the same as net cash

flow from operating activities.

15) The FASB concluded that if a company sells its product but gives the buyer the

right to return the product, revenue from the sales transaction shall be recognized at the

time of sale only if all of six conditions have been met. Which of the following is not

one of these six conditions?

a.The amount of future returns can be reasonably estimated

b.The seller’s price is substantially fixed or determinable at time of sale

c.The buyer’s obligation to the seller would not be changed in the event of theft or

damage of the product

d.The buyer is obligated to pay the seller upon resale of the product

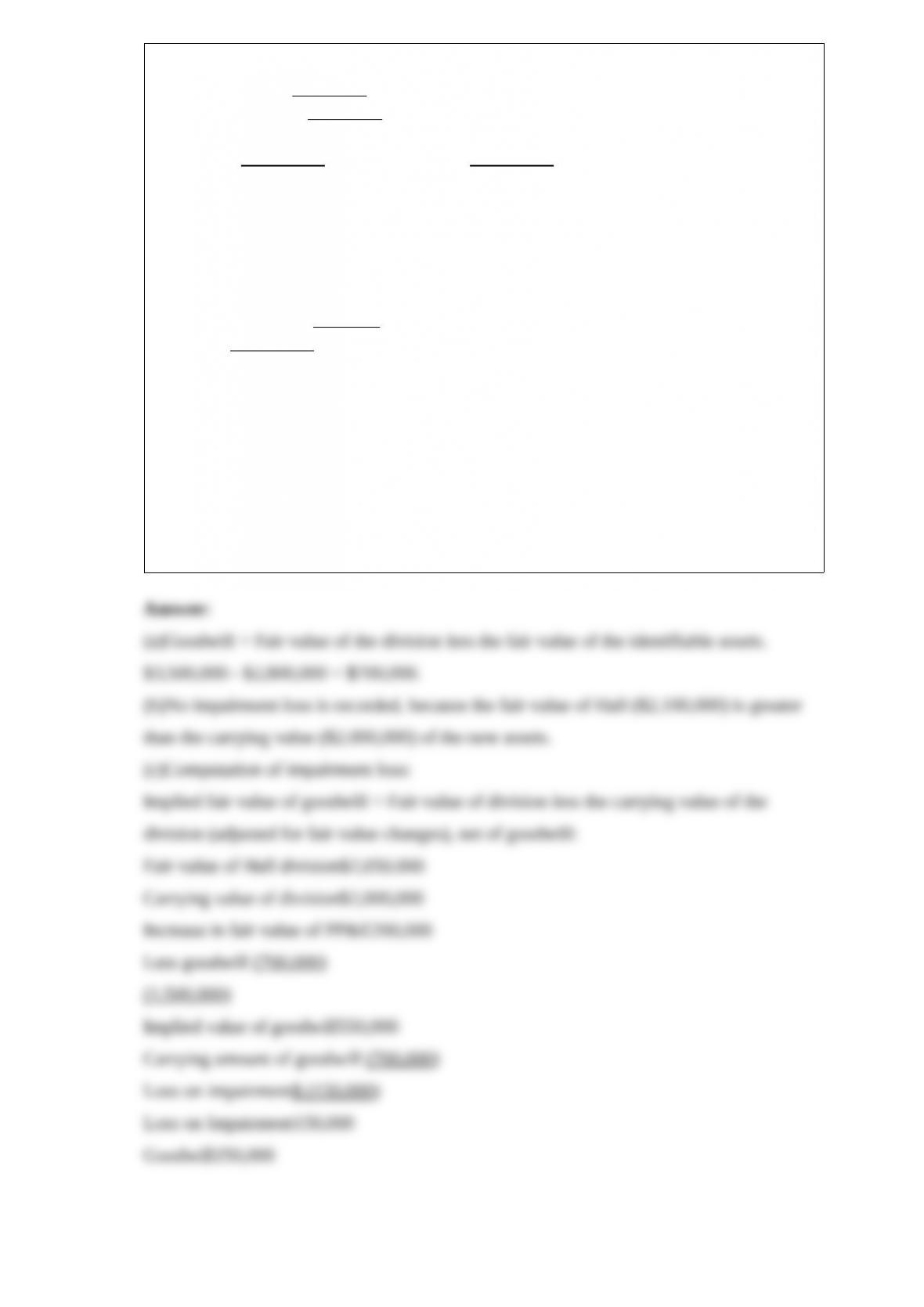

16) Leon Corp. purchased Spinks Co. 4 years ago and at that time recorded goodwill of

$480,000. The Sinks Divisions net assets, including goodwill, have a carrying amount

of $1,150,000. The fair value of the division is estimated to be $1,200,000.

Instructions

(a)Explain whether or not Leon Corp. must prepare an entry to record impairment of the

goodwill. Include the entry, if necessary.

(b)Repeat instruction (a) assuming that the fair value of the division is estimated to be

$1,070,000 and the implied goodwill is $360,000.

17) Sawyer Corporation has a machine (Machine A) that it acquired on 1/1/14 for

$540,000. On 12/31/14 such machines have a selling price and fair value of $621,000.

When used in production, such machines have an estimated useful life of 10 years with

no salvage value. Use the straight-line method.

Brown Corporation has a machine (Machine B) that it acquired on 1/1/14 for $729,000.

On 12/31/14 such machines have a selling price and fair value of $540,000. When used

in production, such machines have an estimated useful life of 10 years with no salvage

value. Use the straight-line method.

On 12/31/14 Brown gave Machine B plus $81,000 cash to Sawyer in return for

Machine A.

Given the assumptions in 10 above, at what amount will Machine B be recorded on

Sawyer’s books?

a.$469,565

b.$729,000

c.$540,000

d.$631,566

18) Which assumption or principle requires that all information significant enough to

affect a decision of reasonably informed users should be reported in the financial

statements?

a.Matching

b.Going concern

c.Historical cost

d.Full disclosure

19) Financial statements for Kiner Company are given below:

Kiner Company

Balance Sheet

January 1, 2015

AssetsEquities

Cash$ 640,000Accounts payable$ 304,000

Accounts receivable576,000

Buildings and equipment2,400,000

Accumulated depreciation

buildings and equipment(800,000)Common stock1,840,000

Patents 288,000Retained earnings 960,000

$3,104,000$3,104,000

Kiner Company

Statement of Cash Flows

For the Year Ended December 31, 2015

Increase (Decrease) in Cash

Cash flows from operating activities

Net income$800,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Increase in accounts receivable$(256,000)

Increase in accounts payable128,000

Depreciationbuildings and equipment240,000

Gain on sale of equipment(96,000)

Amortization of patents 32,000 48,000

Net cash provided by operating activities848,000

Cash flows from investing activities

Sale of equipment192,000

Purchase of land(400,000)

Purchase of buildings and equipment (768,000)

Net cash used by investing activities(976,000)

Cash flows from financing activities

Payment of cash dividend(240,000)

Sale of common stock 640,000

Net cash provided by financing activities 400,000

Net increase in cash272,000

Cash, January 1, 2015 640,000

Cash, December 31, 2015$912,000

Total assets on the balance sheet at December 31, 2015 are $4,432,000. Accumulated

deprecia-tion on the equipment sold was $224,000.

Capital stock (plus any additional paid-in capital) at December 31, 2015 was

a.$1,600,000

b.$1,840,000

c.$1,040,000

d.$2,480,000

20) The income statement reveals

a.resources and equities of a firm at a point in time

b.resources and equities of a firm for a period of time

c.net earnings (net income) of a firm at a point in time

d.net earnings (net income) of a firm for a period of time

21) Application of the full disclosure principle

a.is theoretically desirable but not practical because the costs of complete disclosure

exceed the benefits

b.is violated when important financial information is buried in the notes to the financial

statements

c.is demonstrated by the use of supplementary information explaining the effects of

financing arrangements

d.requires that the financial statements be consistent and comparable

22) On May 31, 2015, Armstrong Company paid $3,500,000 to acquire all of the

common stock of Hall Corporation, which became a division of Armstrong. Hall

reported the following balance sheet at the time of the acquisition:

Current assets$ 900,000Current liabilities$ 600,000

Noncurrent assets 2,700,000Long-term liabilities500,000

Stockholders equity 2,500,000

Total liabilities and

Total assets$3,600,000stockholders equity$3,600,000

It was determined at the date of the purchase that the fair value of the identifiable net

assets of Hall was $2,800,000. At December 31, 2015, Hall reports the following

balance sheet information:

Current assets$ 800,000

Noncurrent assets (including goodwill recognized in purchase)2,400,000

Current liabilities(700,000)

Long-term liabilities (500,000)

Net assets$2,000,000

It is determined that the fair value of the Hall division is $2,200,000. The recorded

amount for Halls net assets (excluding goodwill) is the same as fair value, except for

property, plant, and equipment, which has a fair value of $200,000 above the carrying

value.

Instructions

(a)Compute the amount of goodwill recognized, if any, on May 31, 2015 .

(b)Determine the impairment loss, if any, to be recorded on December 31, 2015 .

(c)Assume that the fair value of the Hall division is $2,050,000 instead of $2,200,000.

Prepare the journal entry to record the impairment loss, if any, on December 31, 2015 .

23) The activity method of depreciation

a.is a variable charge approach

b.assumes that depreciation is a function of the passage of time

c.conceptually associates cost in terms of input measures

d.all of these answers are correct

24) Lexington Company sells product 1976NLC for $60 per unit. The cost of one unit

of 1976NLC is $54, and the replacement cost is $52. The estimated cost to dispose of a

unit is $12, and the normal profit is 40%. At what amount per unit should product

1976NLC be reported, applying lower-of-cost-or-market?

a.$24

b.$48

c.$52

d.$54

25) Lyons Company deducts insurance expense of $126,000 for tax purposes in 2014,

but the expense is not yet recognized for accounting purposes. In 2015, 2016, and 2017,

no insurance expense will be deducted for tax purposes, but $42,000 of insurance

expense will be reported for accounting purposes in each of these years. Lyons

Company has a tax rate of 40% and income taxes payable of $108,000 at the end of

2014 . There were no deferred taxes at the beginning of 2014 .

What is the amount of the deferred tax liability at the end of 2014?

a.$50,400

b.$43,200

c.$18,000

d.$0

26) The accountant for Marlin Corporation has developed the following information for

the company’s defined-benefit pension plan for 2015:

Service cost$500,000

Actual return on plan assets250,000

Annual contribution to the plan920,000

Amortization of prior service cost125,000

Benefits paid to retirees60,000

Settlement rate10%

Expected rate of return on plan assets8%

The accumulated benefit obligation at December 31, 2015, amounted to $3,250,000.

Instructions

(a)Using the above information for Marlin Corporation, complete the pension work

sheet for 2015 . Indicate (credit) entries by parentheses. Calculated amounts should be

supported.

(b)Prepare the journal entry to reflect the accounting for the company’s pension plan for

the year ending December 31, 2015 .

Marlin Corporation

Pension Work Sheet2015

General Journal Entries Memo Entries

Annual OCIPension Projected

PensionGain /Asset /BenefitPlan

ExpenseCashPSCLossLiabilityObligationAssets

Bal., Dec. 31, 2014625,000 1,250,000(4,000,000)2,750,000

Service Cost

Interest Cost

Actual return

Unexpected

gain/loss

Amortization

of PSC

Contributions

Benefits

Gain/loss amort.

Journal entry

for 2015

Balance, Dec. 31, 2015

Answer:

Marlin Corporation

Pension Work Sheet2015

General Journal Entries Memo Entries

OCI

AnnualPriorGain /PensionProjected

PensionServiceLossAsset / BenefitPlan

ExpenseCashCostLiabilityObligationAssets

Bal., Dec. 31, 20141,250,000 Cr. 4,000,000 Cr. 2,750,000 Dr.

Service Cost500,000 Dr.500,000 Cr.

Interest Cost (1)400,000 Dr.400,000 Cr.

Actual return250,000 Cr.250,000 Dr.

Unexpected

gain/loss (2)30,000 Dr.30,000 Cr.

Amortization

of PSC125,000 Dr.125,000 Cr.

Contributions920,000 Cr.920,000 Dr.

Benefits60,000 Dr.60,000 Cr.

Gain/loss Amort..

Journal entry

for 2015805,000Dr.920,000Cr 125,000 Cr.30,000 Cr. 270,000 Dr.

AOCI, 12/31/14 625,000 Dr. -0-

Bal., Dec. 31, 2015500,000 Dr.30,000 Cr. 980,000 Cr. 4,840,000 Cr. 3,860,000 Dr.

(1)$4,000,000 x 10% = $400,000

(2)$250,000 – ($2,750,000 x 8%) = $30,000

(b)Pension Expense805,000

Pension Asset / Liability270,000

Cash920,000

Other Comprehensive Income (PSC) 125,000

27) Which of the following is true?

a.Rents occur at the beginning of each period of an ordinary annuity

b.Rents occur at the end of each period of an annuity due

c.Rents occur at the beginning of each period of an annuity due

d.None of these answer choices are correct

28) Martin Industries maintains its accounting records using IFRS. The company

purchases equipment with a price of $400,000. The manufacturer has offered a payment

plan that would allow Martin to make 10 equal annual payments of $49,316, with the

first payment due one year after the purchase.

How much total interest will Martin pay on this payment plan?

a.$93,160

b.$49,316

c.$160,000

d.$40,000

29) On September 10, 2014, Jenks Co. incurred the following costs for one of its

printing presses:

Purchase of attachment$45,000

Installation of attachment5,000

Replacement parts for renovation of press18,000

Labor and overhead in connection with renovation of press7,000

Neither the attachment nor the renovation increased the estimated useful life of the

press. However, the renovation resulted in significantly increased productivity. What

amount of the costs should be capitalized?

a.$0

b.$57,000

c.$68,000

d.$75,000

30) Molina Companys reported net incomes for 2015 and the previous two years are

presented

below.

2015 2014 2013

$105,000$95,000$70,000

2015s net income was properly determined after giving effect to the following

accounting changes, error corrections, etc. which took place during the year. The

incomes for 2013 and 2014 do not take these items into account and are stated at the

amounts determined in those years. Ignore income taxes.

Instructions

(a)For each of the six accounting changes, errors, or prior period adjustment situations

described below, prepare the journal entry or entries Molina Company should record

during 2015 . If no entry is required, write none.

(b)After recording the situation in part (a) above, prepare the year-end adjusting entry

for December 31, 2015 . If no entry, write none.

1>Early in 2015, Molina determined that equipment purchased in January, 2013 at a

cost of $1,075,000, with an estimated life of 5 years and salvage value of $75,000 is

now estimated to continue in use until December 31, 2019 and will have a $25,000

salvage value. Molina recorded its 2015 depreciation at the end of 2015 .

2>Molina determined that it had understated its depreciation by $20,000 in 2014 owing

to the fact that an adjusting entry did not get recorded.

3>Molina bought a truck January 1, 2012 for $60,000 with a $6,000 estimated salvage

value and a six-year life. The company debited an expense account and credited cash on

the purchase date. The truck is expected to be traded at the end of 2017 . Molina uses

straight-line depreciation for its trucks.

4>During 2015, Molina changed from the straight-line method of depreciating its

cement plant to the double-declining-balance method. The following calculations

present depreciation on both bases. (Ignore income taxes.) The 2015 amount applies

double-declining balance to the 1/1/15 carrying amount after straight-line was used.

2015 2014 2013

Straight-line$100,000$100,000$100,000

Double-declining$200,000$160,000$200,000

5>Molina, in reviewing its provision for uncollectibles during 2015, has determined

that 1/2 of 1% is the appropriate amount of bad debt expense to be charged to

operations. The company had used 1% as its rate in 2014 and 2013 when the expense

had been $20,000 and $14,000, respectively. The company would have recorded

$60,000 of bad debt expense on December 31, 2015 under the old rate.

6>During 2015, Molina decided to change from the LIFO method of valuing

inventories to average cost. The net incomes involved under each method were as

follows:

2015 2014 2013

LIFO$51,000$59,000$42,000

Average cost$63,000$67,000$48,000

Assume no difference between LIFO and average cost inventory values in years prior to

2013 .

31) External events do not include

a.interaction between an entity and its environment

b.a change in the price of a good or service that an entity buys or sells

c.improvement in technology by a competitor

d.using buildings and machinery in operations

32) Noncumulative preferred dividends in arrears

a.are not paid or disclosed

b.must be paid before any other cash dividends can be distributed

c.are disclosed as a liability until paid

d.are paid to preferred stockholders if sufficient funds remain after payment of the

current preferred dividend

33) The following information is taken from French Corporation’s financial statements:

December 31

2015 2014

Cash$73,000$ 27,000

Accounts receivable102,00080,000

Allowance for doubtful accounts(4,500)(3,100)

Inventory155,000175,000

Prepaid expenses7,5006,800

Land100,00060,000

Buildings289,000244,000

Accumulated depreciation(32,000)(13,000)

Patents 20,000 35,000

$710,000$611,700

Accounts payable$ 90,000$ 84,000

Accrued liabilities54,00063,000

Bonds payable125,00060,000

Common stock100,000100,000

Retained earningsappropriated80,00010,000

Retained earningsunappropriated276,000302,700

Treasury stock, at cost (15,000) (8,000)

$710,000$611,700

For 2015 Year

Net income$73,300

Depreciation expense19,000

Amortization of patents5,000

Cash dividends declared and paid30,000

Gain or loss on sale of patentsnone

Instructions

Prepare a statement of cash flows for French Corporation for the year 2015 . (Use the

indirect method.)

34) Gibbs Manufacturing Co. was incorporated on 1/2/14 but was unable to begin

manufacturing activities until 8/1/14 because new factory facilities were not completed

until that date. The Land and Buildings account at 12/31/14 per the books was as

follows:

Date Item Amount

1/31/14Land and dilapidated building$200,000

2/28/14Cost of removing building4,000

4/1/14Legal fees6,000

5/1/14Fire insurance premium payment5,400

5/1/14Special tax assessment for streets4,500

5/1/14Partial payment of new building construction190,000

8/1/14Final payment on building construction190,000

8/1/14General expenses30,000

12/31/14Asset write-up 75,000

$704,900

Additional information:

1>To acquire the land and building on 1/31/14, the company paid $100,000 cash and

1,000 shares of its common stock (par value = $100/share) which is very actively traded

and had a fair value per share of $160.

2>When the old building was removed, Gibbs paid Kwik Demolition Co. $4,000, but

also received $1,500 from the sale of salvaged material.

3>Legal fees covered the following:

Cost of organization$2,500

Examination of title covering purchase of land2,000

Legal work in connection with the building construction 1,500

$6,000

4>The fire insurance premium covered premiums for a three-year term beginning May

1, 2014 .

5>General expenses covered the following for the period 1/2/14 to 8/1/14.

President’s salary$20,000

Plant superintendent covering supervision of new building 10,000

$30,000

6>Because of the rising land costs, the president was sure that the land was worth at

least $75,000 more than what it cost the company.

Instructions

Determine the proper balances as of 12/31/14 for a separate land account and a separate

buildings account. Use separate T-accounts (one for land and one for buildings) labeling

all the relevant amounts and disclosing all computations.

35) Briefly describe some of the similarities and differences between U.S. GAAP and

IFRS with respect to balance sheet reporting.

36) Presented below is certain information pertaining to Edson Company.

Assets, January 1$250,000

Assets, December 31230,000

Liabilities, January 1150,000

Common stock, December 3180,000

Retained earnings, December 3141,000

Common stock sold during the year10,000

Dividends declared during the year13,000

Compute the net income for the year.

37) Under what circumstances is it appropriate to record goodwill in the accounts? How

should goodwill, properly recorded on the books, be written off in accordance with

generally accepted accounting principles?

38) Bell Company has stock outstanding as follows: Common, $10 par value per share,

140,000 shares; Preferred, 4%; $100 par value per share, 8,000 shares. The Preferred is

cumulative and participating up to an additional 3% of par; two years are in arrears (not

including the current year); and the total amount of cash dividends declared for both

classes of stock is $192,000.

Instructions

Prepare the entry for the dividend declaration, separating the dividend into the common

and preferred portions.

39) 1> What are intangible assets?

2> How are limited-life intangibles accounted for subsequent to acquisition?

40) Indicate the principal effects of a stock dividend versus a stock split on the issuing

corporation. Respond in the spaces as follows: “C” for change; “NC” for no change.

Stock DividendStock Split

Number of Shares Outstanding

Par Value per Share

Total Par Outstanding

Retained Earnings

Total Stockholders’ Equity

Composition of Stockholders’ Equity