1) Which is usually included in the engagement letter?

A)

B)

C)

D)

2) Research indicates that the most effective way to prevent and deter fraud is to:

A) implement programs and controls that are based on core values embraced by the

company

B) hire highly ethical employees

C) communicate expectations to all employees on an annual basis

D) terminate employees who are suspected of committing fraud

3) Auditors seldom expect to find misstatements when testing payroll transactions.

A) True

B) False

4) Which of the following is a factor that relates to attitudes or rationalization to

commit fraudulent financial reporting?

A) Significant accounting estimates involving subjective judgments

B) Excessive pressure for management to meet debt repayment requirements

C) Management’s practice of making overly aggressive forecasts

D) High turnover of accounting, internal audit and information technology staff

5) When making decisions about evidence for a given audit, the auditor’s goal is to

obtain a sufficient amount of timely, reliable evidence that is relevant to the information

being verified. In addition, the goal of audit efficiency is to gather and evaluate the

information:

A) no matter the cost involved in obtaining such evidence

B) even if cost is irrelevant to the auditor, because they bill the client for costs incurred

C) at the lowest possible total cost

D) at the cost suggested in the engagement letter

6) Tests of the presentation and disclosure-related objectives are generally done as part

of the completion phase of the audit.

A) True

B) False

7) In a financial statement audit, inherent risk is evaluated to help an auditor asses

which of the following?

A) The internal audit department’s objectivity in reporting a material misstatement of a

financial statement assertion it detects to the audit committee

B) The risk the internal control system will not detect a material misstatement of a

financial statement assertion

C) The risk that the audit procedures implemented will not detect a material

misstatement of a financial statement assertion

D) The susceptibility of a financial statement assertion to a material misstatement

assuming there are no related controls

8) In which situation would the auditor be choosing between “except for” qualified

opinion and an adverse opinion?

A) The auditor lacks independence

B) A client-imposed scope limitation

C) A circumstance imposed scope limitation

D) Lack of full disclosure within the footnotes

9) Which of the following would indicate a deficiency in internal controls in the

acquisition and payment cycle?

A) Repairs and maintenance accounts are reviewed for unusual entries each quarter

B) Acquisitions are made and approved by the department that will use the equipment

C) Acquisitions of equipment greater than $1,000 are to be capitalized

D) Acquisitions of equipment less than $1,000 are to be expensed as incurred

10) Match eight of the terms (a-k) with the definitions provided below (1-8):

a.Haphazard selection

b.Attributes sampling

c.Block sample selection

d.Judgmental sampling

e.Non-probabilistic sample selection

f.Probabilistic sample selection

g.Random sample

h.Representative sample

i.Statistical sampling

j.Systematic sample selection

k.Sampling distribution

________ 1> The use of mathematical measurement techniques to calculate formal

statistical results and quantify sampling risk.

________ 2> A non-probabilistic method of sample selection in which items are

selected in measured sequences.

________ 3> A sample whose characteristics are the same as those of the population.

________ 4> A statistical, probabilistic method of sample evaluation that results in an

estimate of the proportion of items in a population containing a characteristic of

interest.

________ 5> A non-probabilistic method of sample selection in which items are chosen

without regard to their size, source, or other distinguishing characteristics.

________ 6> An auditor selects items such that each population item has a known

probability of being included in the sample.

________ 7> A frequency distribution of the results of all possible samples of a

specified size that could be obtained from a population containing some specific

parameters.

________ 8> A sample in which every possible combination of elements in the

population has an equal chance of constituting the sample.

11) For proper internal control, the person(s) responsible for signing the payroll checks

should not have access to timekeeping or be otherwise involved in the preparation of

payroll.

A) True

B) False

12) Difference estimation frequently results in smaller sample sizes than any other

variables sampling method.

A) True

B) False

13) SSARS are issued by the SEC.

A) True

B) False

14) In determining the reasonableness of the client’s amount for depreciation expense

the auditor is primarily concerned that the client has followed a consistent policy and

the calculations are correct. Which of the following audit objectives best addresses the

above concerns?

A) Existence

B) Accuracy

C) Valuation

D) Allocation

15) In auditing the current year acquisitions of property, plant, and equipment, all

balance-related audit objectives except realizable value and disclosure are used as a

framework for subsequent audit testing.

A) True

B) False

16) If tests of controls reveal that controls are sufficiently effective to justify reducing

control risk, the auditor is justified in reducing substantive audit tests.

A) True

B) False

17) The transfer of money from one bank account to another and improperly recording

the transfer so that the amount is recorded as an asset in both banks is referred to as

kiting.

A) True

B) False

18) The audit firm issues an audit report for its client. The auditor’s have NO obligation

to make further inquiries with respect to the client’s audited financial statements unless:

A) a development occurs that may affect the company’s long term viability as a

company

B) final resolution was made on disclosed contingency for which no liability needed to

be accrued

C) new information comes to the auditor’s attention concerning an event that occurred

prior to the date of the audit report that, if known, would have impacted the audit

opinion

D) a lawsuit, in which the risk of loss was considered remote, was resolved in the

company’s favor

19) Acceptable risk of incorrect rejection affects auditors’ action only when they

conclude that a population is:

A) fairly stated

B) acceptable

C) materially misstated

D) acceptable after certain adjustments

20) “An attitude, character, or set of ethical values exist that allow management or

employees to commit a dishonest act .” describes the opportunities condition included

in the fraud triangle.

A) True

B) False

21) When using statistical sampling, the auditor would most likely require a smaller

sample if the:

A) population increases

B) desired reliability decreases

C) desired precision interval narrows

D) expected exception rate increases

22) Which of the following is a significant audit concern related to the transfer of

inventory from one location to another?

A) recorded transfers occurred

B) transfers were properly transported

C) transfers were properly planned

D) transfers represent efficient movement of assets

23) Tests of controls and tests of details of balances are the auditor’s most important

means of verifying account balances in the payroll and personnel cycle.

A) True

B) False

24) Inherent risk for payroll-related liabilities is normally higher than for accounts

receivable.

A) True

B) False

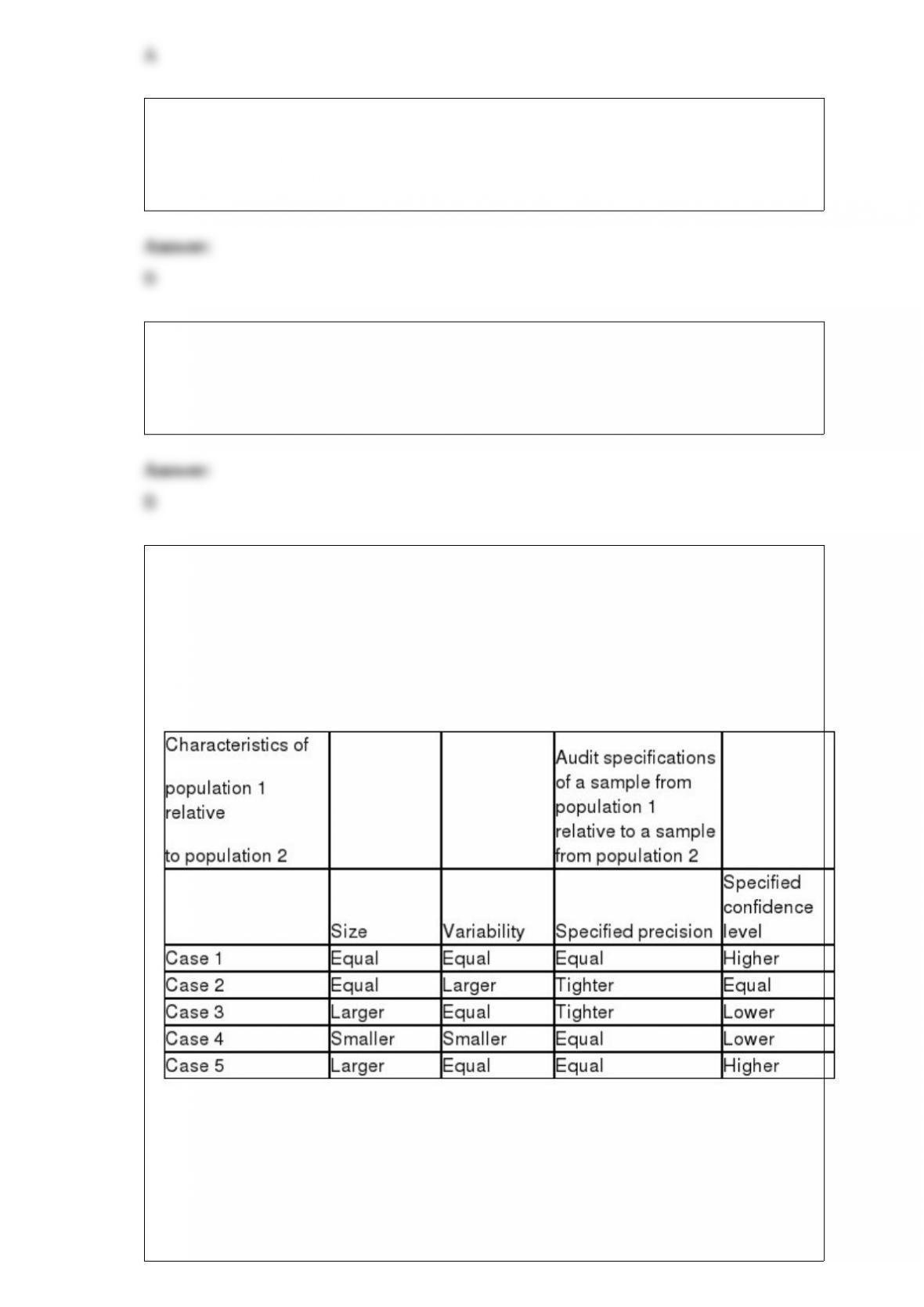

25) An audit partner is developing an office-training program to familiarize his

professional staff with statistical decision models applicable to the audit of dollar-value

balances. He wishes to demonstrate the relationship of sample sizes to population size

and variability and the auditor’s specifications as to precision and confidence level. The

partner prepared the following table to show comparative population characteristics and

audit specifications of two populations.

Based on the information presented above, you are to indicate for the specified case

from the table the required sample size to be selected from population 1 relative to the

sample from population 2 . In case 5, the required sample from population 1 is:

A) larger than the required sample size from population 2

B) equal to the required sample size from population 2

C) smaller than the required sample size from population 2

D) indeterminate relative to the required sample size from population 2

26) The reason for testing the client’s bank reconciliation is to verify whether the

client’s recorded bank balance is the same amount as the actual cash in bank, except for

deposits in transit, checks outstanding, and other reconciling items. The information

needed to complete the tests of the reconciliation are provided by the:

A) client’s records and ledgers for the year under audit

B) cutoff bank statement

C) client’s records and ledgers for the subsequent year

D) canceled checks for the year under audit

27) Which of the following errors would be least likely to be discovered during the tests

of the bank reconciliation?

A) Payment was made to an employee for more hours than he worked

B) Cash received by the client subsequent to the balance sheet date was recorded as

cash receipts in the current year

C) Payments on notes payable were debited directly to the bank balance by the bank

were not entered in the client’s records

D) Deposits were recorded in the cash receipts records near the end of the year,

deposited in the bank, and were included in the bank reconciliation as a deposit in

transit

28) Failure to record the acquisition of goods is a violation of which audit objective?

A) Accuracy

B) Occurrence

C) Authorization

D) Completeness

29) Describe the differences between positive and negative confirmations. Which type

is generally viewed as more reliable?

30) There are three primary reasons for obtaining a thorough understanding of the

client’s industry and external environment. What are these reasons?

31) You are part of the audit team that is auditing Hillsburg Hardware Co. and you have

been assigned to the sales and collection business process. You are testing whether the

cash received has been recorded in the cash receipts journal. (completeness objective

/assertion). List two tests of controls and at least one test of transactions that you would

do to satisfy yourself regarding the completeness assertion.

32) Management’s identification and analysis of risk is an ongoing process and is a

critical component of effective internal control. An important first step is for

management to identify factors that may increase risk. Identify at least five factors,

observable by management, which may lead to increased risk in a typical business

organization.

33) How do auditors determine the extent of testing of internal controls in the

acquisition and payment cycle?

34) Discuss the audit procedures performed when testing the detail tie-in objective for

accounts receivable, and explain why this objective is ordinarily tested before any other

objectives for accounts receivable.

35) What two steps must an auditor do if they have reservations about the audit client

continuing as a going concern?

36) In developing an understanding of the client’s accounting information system the

auditor follows a sequential process. Describe the process below:

37) Discuss three major differences between operational and financial auditing.