Adjusting entries are required to match revenues and expenses.

Because an inventory error causes an offsetting error in the next period, it is sometimes

said to be self-correcting.

A properly designed internal control system is a key part of systems design, analysis,

and performance.

Accrued expenses reflect transactions where cash is paid before a related expense is

recognized.

TechCom factored $35,000 of its accounts receivable and was charged a 2% factoring

fee. The journal entry to record this would include a debit to Cash of $35,000; a debit to

Factoring Fee Expense of $700; and a credit to Accounts Receivable of $35,700.

The balance sheet is also called the statement of financial position because it shows the

financial position of the business on a particular date.

The steps in the closing process are (1) close credit balances in revenue accounts to

Income Summary; (2) close credit balances in expense accounts to Income Summary;

(3) close Income Summary to Owner’s Capital; (4) close Withdrawals to Owner’s

Capital.

The common rule of thumb is that a company’s acid-test ratio should be at least 1.5 to 1.

Sales of $350,000 and net sales of $323,000 may reflect sales discounts of $27,000.

Internal users include creditors, shareholders, internal auditors and managers.

The advantage of FIFO is that it assigns the most recent costs to cost of goods sold, and

better matches current costs with revenues on the income statement.

A credit purchase of a business expense item should be recorded with a debit to an

expense account and a credit to Accounts Payable.

The inventory cost flow assumption that assigns the highest cost to ending inventory in

a period of rising prices is moving weighted average.

Hasbro had $750 million in accounts receivable and $2,900 million in net sales for the

period. Its days’ sales uncollected was 29.8.

A T-Account is a formal account frequently used in business.

A company can raise cash by borrowing money, and then factoring its accounts

receivable as security for the loan.

Chuck Taylor withdrew $6,000 in cash for his personal use from his business. This

amount should be included as an expense on the income statement.

Credit sales are recorded by crediting an account receivable for a specific customer.

An adjusting entry can only affect income statement accounts.

The book value of an asset is equivalent to the market value of that asset.

Sharp’s post-closing trial balance has debit totals of $40,350 and credit totals of

$40,650. The next step is to review for errors in the closing process.

Private enterprises are all required to report using International Financial Reporting

Standards (IFRS).

Maintaining accurate records is an important internal control principle.

Sales Discounts, Sales Returns and Allowances, and Cost of Goods Sold are closed to

Income Summary with debits.

After posting the entries to close all revenue accounts and all expense accounts, the

Income Summary account of Waif Services has a $4,000 debit balance. This shows that

Waif Services earned a net income of $4,000.

Assets tied up in inventory are not productive assets.

Chequing accounts are sometimes called savings accounts.

The General Journal is flexible and can be used for original, adjusting, closing, and

correcting entries.

Net income is the excess of expenses over revenues, whereas net loss is the excess of

revenues over expenses.

Asset, liability and revenue accounts are not closed as long as a company continues in

business.

Credit cards are seen as an advantage by businesses because the cash is normally

received quicker than with other forms of extended credit.

A perpetual inventory system gives a continuous record of the amount of inventory on

hand.

In a periodic inventory system, Purchases is a temporary account.

On a work sheet, adjusted balances of revenues and expenses are sorted to the Income

Statement columns.

The practice of placing dishonoured notes receivable into Accounts Receivable keeps

only current notes receivable in the Notes Receivable account.

Budgeting is the process of developing formal plans for an organization’s future

activities.

To include the personal assets and transactions of a business’s owner in the records and

reports of the business would be in conflict with the:

A. Monetary unit principle.

B. Cost principle.

C. Business entity principle.

D. Going concern principle.

E. Revenue recognition principle.

An account the balance of which is subtracted from the balance of a related account so

that more complete information than simply the net amount is provided is a(n):

A. Accrued expense.

B. Contra account.

C. Accrued revenue.

D. Prepaid expense.

E. Withdrawal.

Generally accepted accounting principles are:

A. Not used in the real world.

B. Are required to make financial statement information relevant and faithfully

represented.

C. Are only used for internal reporting.

D. Are only used by auditors.

E. Are only used for reporting to Canada Revenue Agency.

Exchanges between the entity and some other person or organization are:

A. Internal transactions.

B. External transactions.

C. Business papers.

D. Source documents.

E. Investments.

A business sold some inventory on credit for $5,000 before taxes. The sale is subject to

5% goods and services tax (GST) and 7% provincial sales tax (PST). The business uses

a perpetual inventory system. What is the amount that will be recorded in the GST

payable account as a result of this sale?

A. $250 debit

B. $250 credit

C. $350 debit

D. $350 credit

E. None of these answers is correct.

A cheque that was outstanding on last month’s bank reconciliation was not among the

cancelled cheques returned by the bank this month. As a result, in preparing this

month’s reconciliation, the amount of this cheque should be:

A. Added to the book balance of cash.

B. Deducted from the book balance of cash.

C. Added to the bank balance of cash.

D. Deducted from the bank balance of cash.

E. Noted as a memo.

Vanderet’s Computer Business owns computer equipment which cost $3,240 and has an

expected useful life of three years. No residual value is expected. At the company’s

yearend, December 31, the equipment’s book value is $2,520. In what month was the

computer purchased using the straight-line depreciation method?

A. January

B. March

C. May

D. June

E. August

Cash equivalents:

A. Are short-term, highly liquid investments.

B. Include 6-month certificates of deposit.

C. Include chequing accounts.

D. Are recorded in petty cash.

E. Are short-term, highly liquid investments and include chequing accounts.

Gross profit is derived from:

A. Sales.

B. Beginning inventory.

C. Ending inventory.

D. Cost of goods sold.

E. All of these answers are correct.

If a merchandising company ends a period with a larger inventory than it owned at the

beginning of the period, then:

A. The cost of goods sold was larger than net purchases.

B. Net income was larger than gross profit.

C. The cost of goods sold was smaller than net purchases.

D. The cost of goods available for sale was smaller than the cost of goods sold.

E. Gross profit was larger than the cost of goods sold.

The accounting principle that requires financial statement information to be based on

costs incurred in business transactions, and requires assets and services to be recorded

initially at the cash or cash-equivalent amount given in exchange, is the:

A. Accounting equation.

B. Cost principle.

C. Going concern principle.

D. Revenue recognition principle.

E. Business entity principle.

A company that has operated with a 30% average gross profit ratio for a number of

years had $110,000 in net sales during the first quarter of this year. If it began the

quarter with $28,000 in inventory at cost and purchased $75,000 of merchandise during

the quarter, its estimated ending inventory by the gross profit method is:

A. $20,000.

B. $21,000.

C. $24,000.

D. $25,000.

E. $26,000.

The approach to preparing financial statements based on recognizing revenues when the

cash is received and reporting expenses when the cash is paid is called:

A. Accrual basis accounting.

B. The operating cycle of a business.

C. Cash basis accounting.

D. The revenue recognition principle.

E. The matching principle.

Sales returns:

A. Refer to merchandise that customers return to the seller after the sale.

B. Refer to reductions in the selling price of merchandise sold to customers.

C. Represent cash discounts.

D. Represent trade discounts.

E. Are related to purchase discounts.

A credit is used to record:

A. A decrease in an expense account.

B. A decrease in an asset account.

C. An increase in an unearned revenue account.

D. An increase in a revenue account.

E. All of these answers are correct.

Which inventory cost flow assumption results in the highest tax expense in a period of

inflation?

A. Retail method.

B. FIFO.

C. Average cost.

D. Specific identification.

E. Moving weighted average.

An asset created by a payment for economic benefits that does not expire until some

later time is:

A. Recorded as a debit to an unearned revenue account.

B. Recorded as a debit to a prepaid expense account.

C. Recorded as a credit to an unearned revenue account.

D. Recorded as a credit to a prepaid expense account.

E. Not recorded in the accounting records.

On June 30, the Cash account of Lutness Company had a normal balance of $4,300.

During July the account was debited for a total of $3,400 and credited for a total of

$3,600. What was the balance in the Cash account on August 1?

A. $-0.

B. $4,100 debit.

C. $3,400 credit.

D. $3,400 debit.

E. $4,100 credit.

A statement of profit and loss is another name for:

A. The income statement.

B. The balance sheet.

C. The statement of cash flows.

D. The statement of changes in equity.

E. The accounting equation.

Costs incurred or the using up of assets as a result of the main operations of a business

are called:

A. Liabilities.

B. Equity.

C. Revenues.

D. Expenses.

E. Net losses

Goods on consignment:

A. Are goods shipped by the owner to the consignee who sells the goods for the owner.

B. Are reported in the consignee’s books as inventory.

C. Are reported on the consignor’s books as inventory.

D. Are goods shipped by the owner to the consignee who sells the goods for the owner

and are reported in the consignee’s books as inventory.

E. Are goods shipped by the owner to the consignee who sells the goods for the owner

and are reported on the consignor’s books as inventory.

If equity is $30,000 and liabilities are $73,000, then assets equal:

A. $30,000.

B. $40,000.

C. $60,000.

D. $73,000.

E. $103,000.

The operating cycle of a merchandising company:

A. Begins with the purchase of merchandise.

B. Ends with the collection of cash from the sale of merchandise.

C. Varies among types of businesses.

D. Applies to both cash and credit sales.

E. All of these answers are correct.

A post-closing trial balance shows:

A. All ledger accounts with a balance, none of which can be temporary accounts.

B. All ledger accounts with a balance, none of which can be real accounts.

C. All ledger accounts with a balance, which include some temporary and some real

accounts.

D. Only revenue and expense accounts.

E. Only asset accounts.

Merchandise inventory includes:

A. All goods owned by a company and held for sale.

B. Goods in transit.

C. Goods on consignment.

D. Damaged goods.

E. All of these answers are correct.

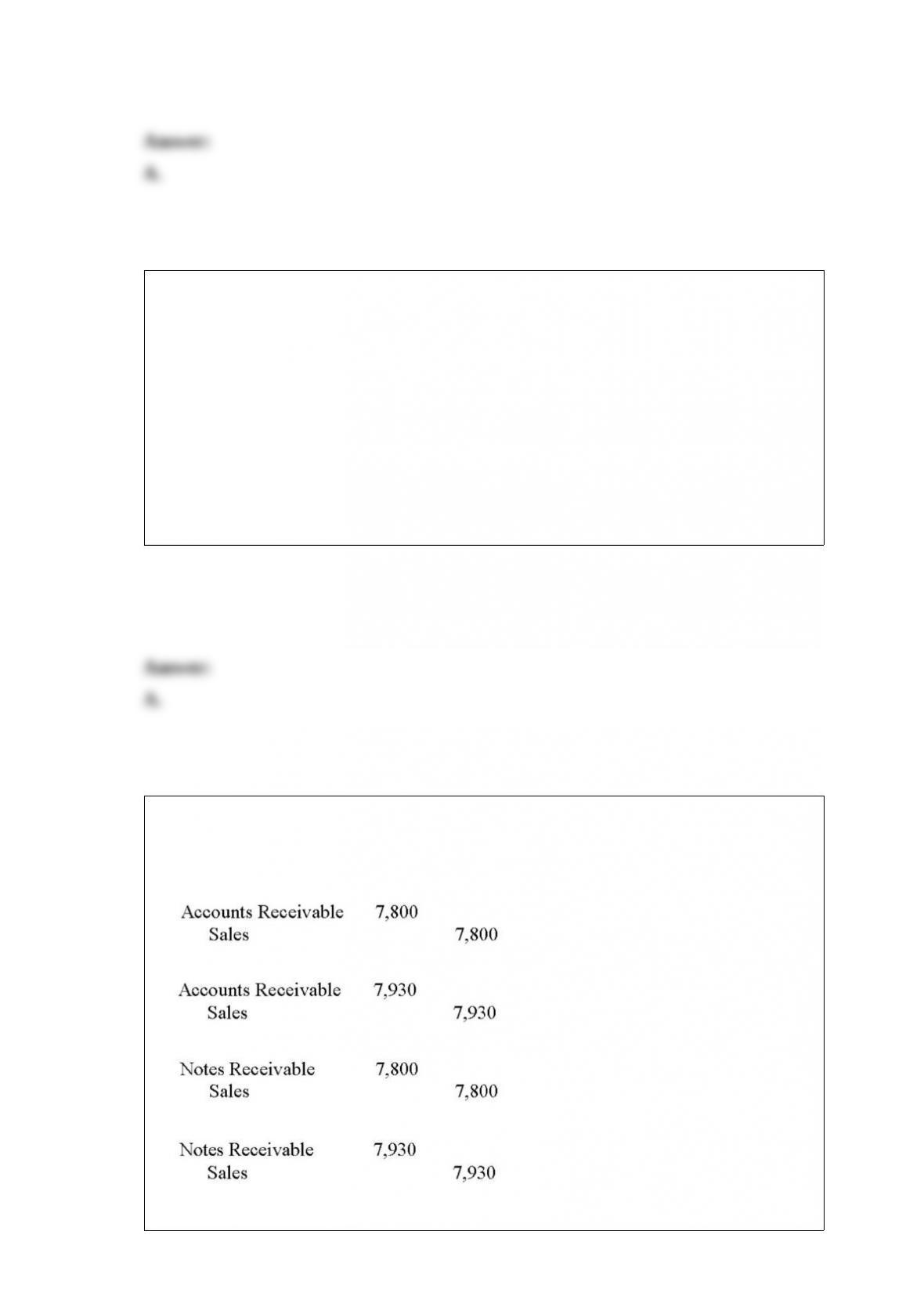

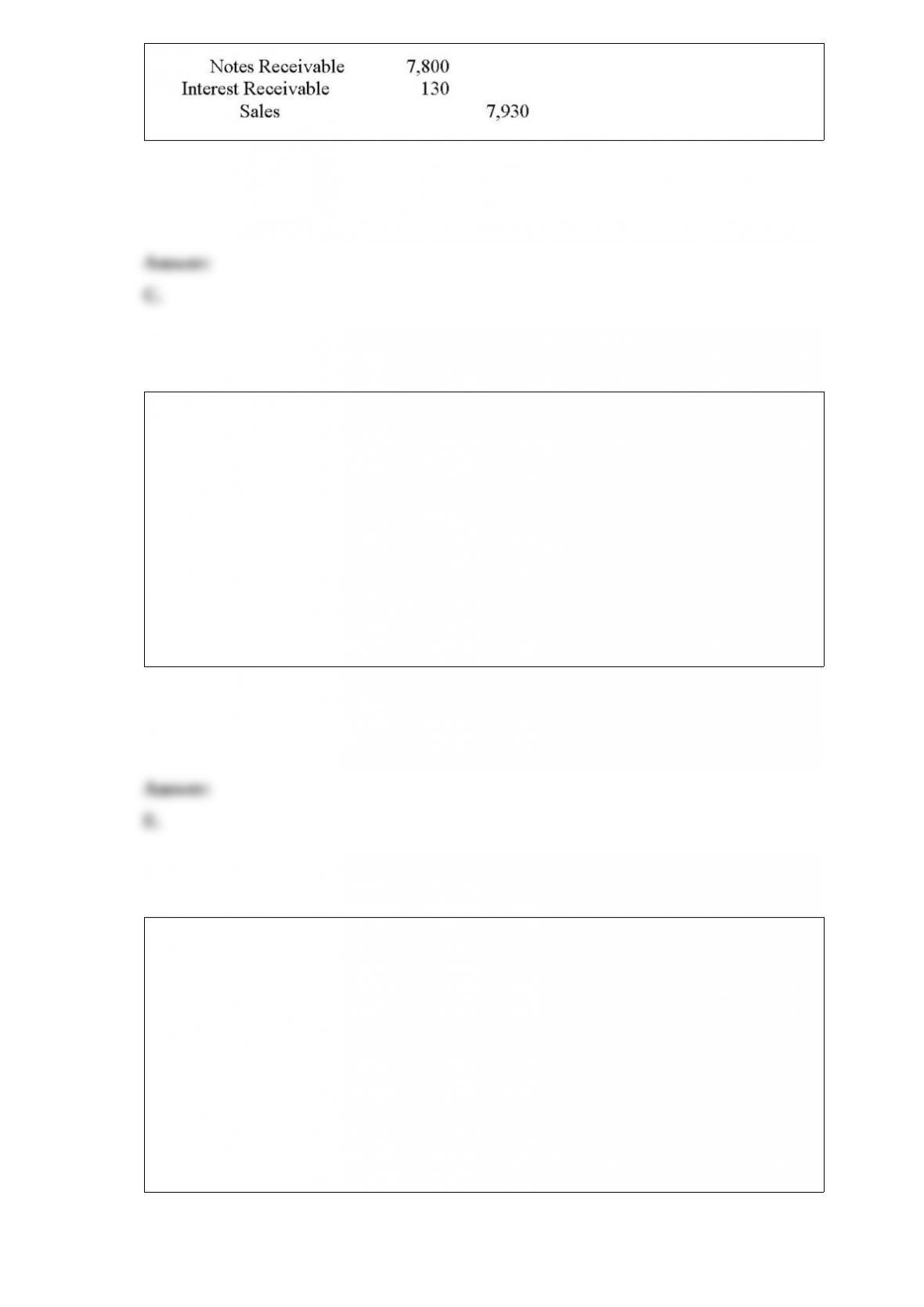

MixRecording Studios purchased $7,800 in electronic components from TechCom.

MixRecording Studios signed a 60-day, 10% promissory note for $7,800. TechCom’s

journal entry to record the transaction should be:

A.

B.

C.

D.

E.

Cash receipts are the result of:

A. Cash sales.

B. Cash disbursements.

C. Collection of accounts receivable.

D. Collection of accounts payable.

E. Cash sales and collection of accounts receivable.

Which of the following is not reported on the income statement?

A. Revenues earned by a business.

B. Expenses incurred by a business.

C. Withdrawals.

D. Net income.

E. All of these answers are correct.

The three primary components of accounting information systems are:

A. Relevance, compatibility, and flexibility.

B. Compatibility, flexibility, and cost-benefit.

C. Compatibility, flexibility, and safety.

D. Compatibility, timeliness, and cost-benefit.

E. Accounts payable, accounts receivable, and payroll.

At the end of its first year of operations, Lockerbie and Role Company has total assets

of $3,000,000 and total liabilities of $1,200,000. The owner originally invested

$200,000 in the business, but has not made any further investments or taken any

withdrawals. What is the first year’s net income for Lockerbie and Role Company?

A. $1,600,000.

B. $1,800,000.

C. $1,000,000.

D. $3,000,000.

E. $3,200,000.

Explain how accounting adjustments affect financial statements.

Outdoors Unlimited had net sales for YR 1 of $285,000 and $575,000 for YR 2. The

year-end balances of accounts receivable were $49,000 for YR 1 and $85,000 for YR 2.

Calculate the days’ sales uncollected at the end of each year (to the nearest day) and

describe any changes in the apparent liquidity of the company’s receivables.

The following are the steps in the accounting cycle. List them in the order in which they

are completed:

Completing the work sheet

Posting

Preparing an unadjusted trial balance

Journalizing

Preparing the statements

Closing the temporary accounts

Adjusting the ledger accounts

Preparing a post-closing trial balance

Put the steps of the accounting cycle in the correct order:

Adjust

Analyze transactions

Close

Journalize

Post

Prepare adjusted trial balance

Prepare post-closing trial balance

Prepare statements

Prepare unadjusted trial balance

A merchandising company’s _______________ begins with the purchase of

merchandise and ends with the collection of cash from sales.

What are the effects of inventory methods on financial and tax reporting?