The exclusive right to benefit from a creative work, such as a film, is a:

a. Patent.

b. Copyright.

c. Trademark.

d. Franchise.

Which of the following is never a current liability account?

a. Accrued payroll.

b. Dividends payable.

c. Prepaid rent.

d. Subscriptions collected in advance from customers.

The net pension liability (PBO minus plan assets) is decreased by:

a. Service cost.

b. Expected return on plan assets.

c. Amortization of net gain-AOCI.

d. Prior service cost.

The Management Discussion and Analysis section of the annual report can best be

described as:

a. Frank but objective.

b. Independent but precise.

c. Legalistic and lengthy.

d. Biased but informative.

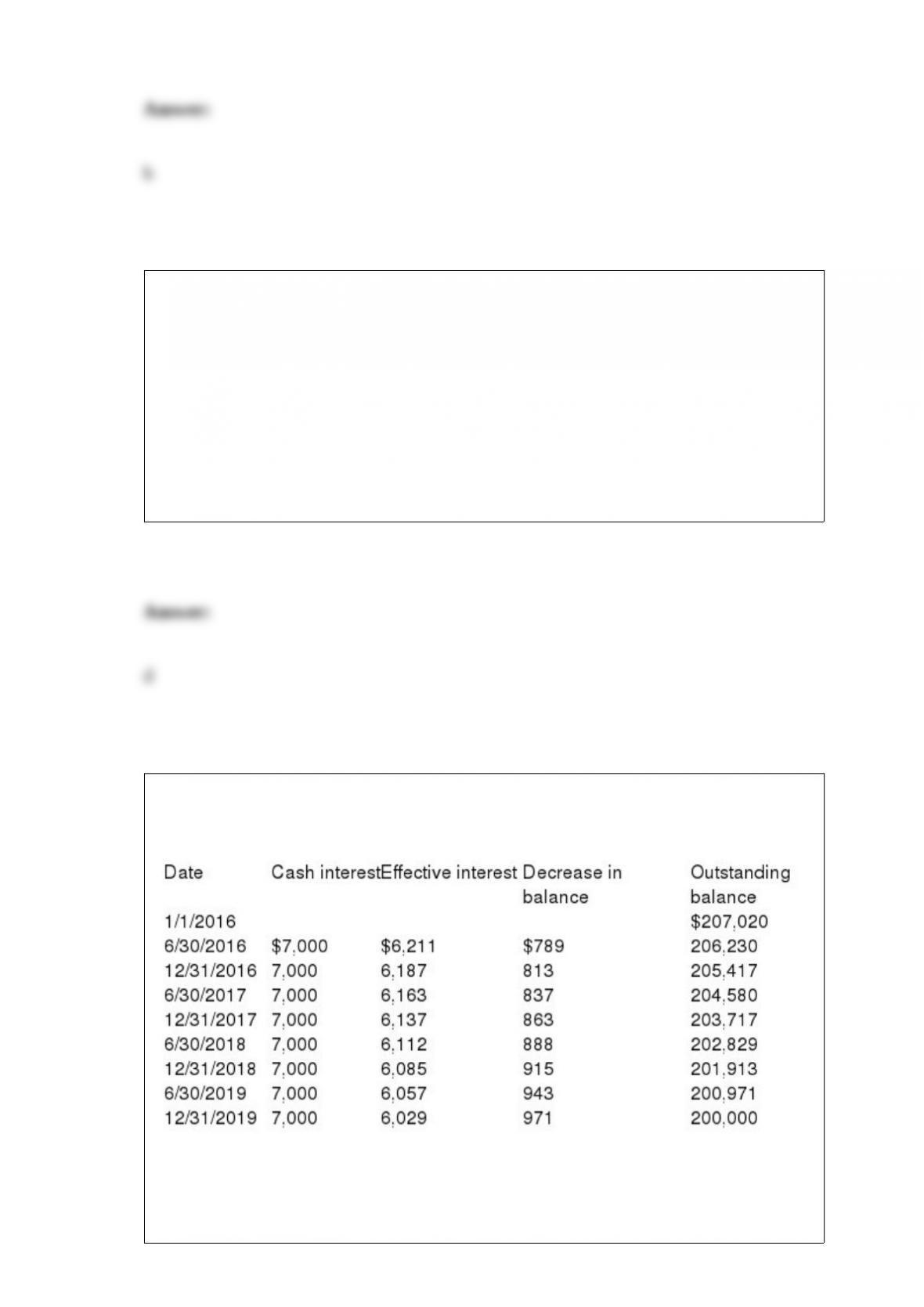

Lopez Plastics Co. (LPC) issued callable bonds on January 1, 2016. LPC’s accountant

has projected the following amortization schedule from issuance until maturity:

LPC issued the bonds:

a. At par.

b. At a premium.

c. At a discount.

d. Cannot be determined from the given information.

Indiana Co. began a construction project in 2016 with a contract price of $150 million

to be received when the project is completed in 2018. During 2016, Indiana incurred

$36 million of costs and estimates an additional $84 million of costs to complete the

project. Indiana recognizes revenue over time and for this project recognizes revenue

over time according to the percentage of the project that has been completed. In 2017,

Indiana incurred additional costs of $58.5 million and estimated an additional $40.5

million in costs to complete the project. Indiana:

a. Recognized $15 million gross profit on the project in 2017.

b. Recognized $13.5 million gross profit on the project in 2017.

c. Recognized $6 million gross profit on the project in 2017.

d. Recognized $1.5 million gross profit on the project in 2017.

Which of the following is not a change in accounting principle that usually is accounted

for by retrospectively revising prior financial statements?

a. Change from FIFO to the average method of inventory costing.

b. Change from SYD to DDB depreciation.

c. Change from the average method of inventory costing to FIFO.

d. Change from the LIFO to the FIFO method of inventory costing.

An overfunded pension plan means that the:

a. PBO is less than plan assets.

b. PBO exceeds plan assets.

c. ABO is less than plan assets.

d. ABO exceeds plan assets.

On June 1st, Joseph & Company received a $500 deposit for 80 cases of wine. On June

10th the customer identified specific vintages that are included in Joseph’s inventory,

and asked that Joseph not ship the wine until June 20 so the customer could ready space

to store the wine, so Joseph set those wines aside for the customer, boxed and ready for

shipment to the customer. On June 20th the wine was shipped and delivered to the

customer. Joseph likely would recognize revenue on

a. June 20th

b. June 10th

c. June 1st

d. Upon consumption of the wine by the customer

In December 2016, Kojak Insurance Co. received $500,000 in premiums for a two-year

property insurance policy. The company recorded the transaction by debiting cash and

crediting insurance premium revenue for the full amount. An internal audit conducted in

early 2017 flagged this transaction. The appropriate accounting treatment is that:

a. Kojak needs to correct an accounting error.

b. Kojak has made a change in accounting principle, requiring retrospective adjustment.

c. Kojak is required to adjust a change in accounting estimate prospectively.

d. Kojak is not required to make any accounting adjustments.

Present and future value tables of $1 at 3% are presented below:

Shane wants to invest money in a 6% CD account that compounds semiannually. Shane

would like the account to have a balance of $100,000 four years from now. How much

must Shane deposit to accomplish his goal?

a. $88,849.

b. $78,941.

c. $25,336.

d. $22,510.

Due to an error in computing depreciation expense, Crote Corporation understated

accumulated depreciation by $60 million as of December 31, 2016. Crote has a tax rate

of 40%. Crote’s retained earnings as of December 31, 2016, would be:

a. Overstated by $36 million.

b. Understated by $36 million.

c. Overstated by $24 million.

d. Understated by $24 million.

Other things being equal, most managers would prefer to report liabilities as noncurrent

rather than current. The logic behind this preference is that the long-term classification

permits the company to report:

a. Higher working capital and a higher inventory turnover.

b. Lower working capital and a higher current ratio.

c. Higher working capital and a higher current ratio.

d. Higher working capital and a lower debt to equity ratio.

Which of the following would not be a component of cash flows from investing

activities?

a. Sale of land.

b. Purchase of securities.

c. Purchase of equipment.

d. Dividends paid.

The tax effect of a net operating loss (NOL) carryback usually:

a. Results in a current receivable at the end of the NOL year.

b. Is subject to a valuation allowance.

c. Is reflected as deferred tax asset at the end of the NOL year.

d. Is reflected as a deferred tax liability at the end of the NOL year.

On April 1, 2016, BigBen Company acquired 30% of the shares of LittleTick, Inc.

BigBen paid $100,000 for the investment, which is $40,000 more than 30% of the book

value of LittleTick’s identifiable net assets. BigBen attributed $15,000 of the $40,000

difference to inventory that will be sold in the remainder of 2016, and the rest to

goodwill. LittleTick recognized a total of $20,000 of net income for 2016, and paid total

dividends for the year $10,000; these dividends were issued quarterly. BigBen’s

investment in LittleTick will affect BigBen’s 2016 net income by:

a. A loss of $10,500.

b. Earnings of $4,500.

c. Earnings of $1,125.

d. Earnings of $3,450.

Enhancing qualitative characteristics of accounting information include each of the

following except:

a. Timeliness.

b. Materiality.

c. Comparability.

d. Verifiability.

Which of the following is not true about accounting for revenue from franchise

arrangements?

a. Franchise arrangements often include a performance obligation for a license as well

as for delivery of goods and services.

b. Franchise arrangements typically include one or more performance obligations for

which revenue is recognized at a point in time.

c. Franchise arrangements typically include one or more performance obligations for

which revenue is recognized over a period of time.

d. Franchise arrangements typically include one performance obligation because the

goods and services included in the arrangement are not separately identifiable.

Cromartie Ltd. prepares its financial statements according to International Financial

Reporting Standards. During 2016 the company incurred $1,245,000 in research

expenditures to develop a new product. An additional $756,000 in development

expenditures were incurred after technological and commercial feasibility was

established and after the future economic benefits were deemed probable. The project

was successfully completed and the new product was patented before the end of the

2016 fiscal year. Sale of the product began in 2015. What amount of the above

expenditures would Cromartie expense in its 2016 income statement?

a. $2,001,000.

b. $ 756,000.

c. $1,245,000.

d. $0.

The calculation of diluted earnings per share assumes that stock options were exercised

and that the proceeds were used to buy treasury stock at:

a. The average market price for the reporting period.

b. The market price at the end of the period.

c. The purchase price stated on the options.

d. The stock’s par value.

Identify the major components included in the official definition of a liability as set

forth by Statement of Financial Accounting Concepts No. 6, “Elements of Financial

Statements.”

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

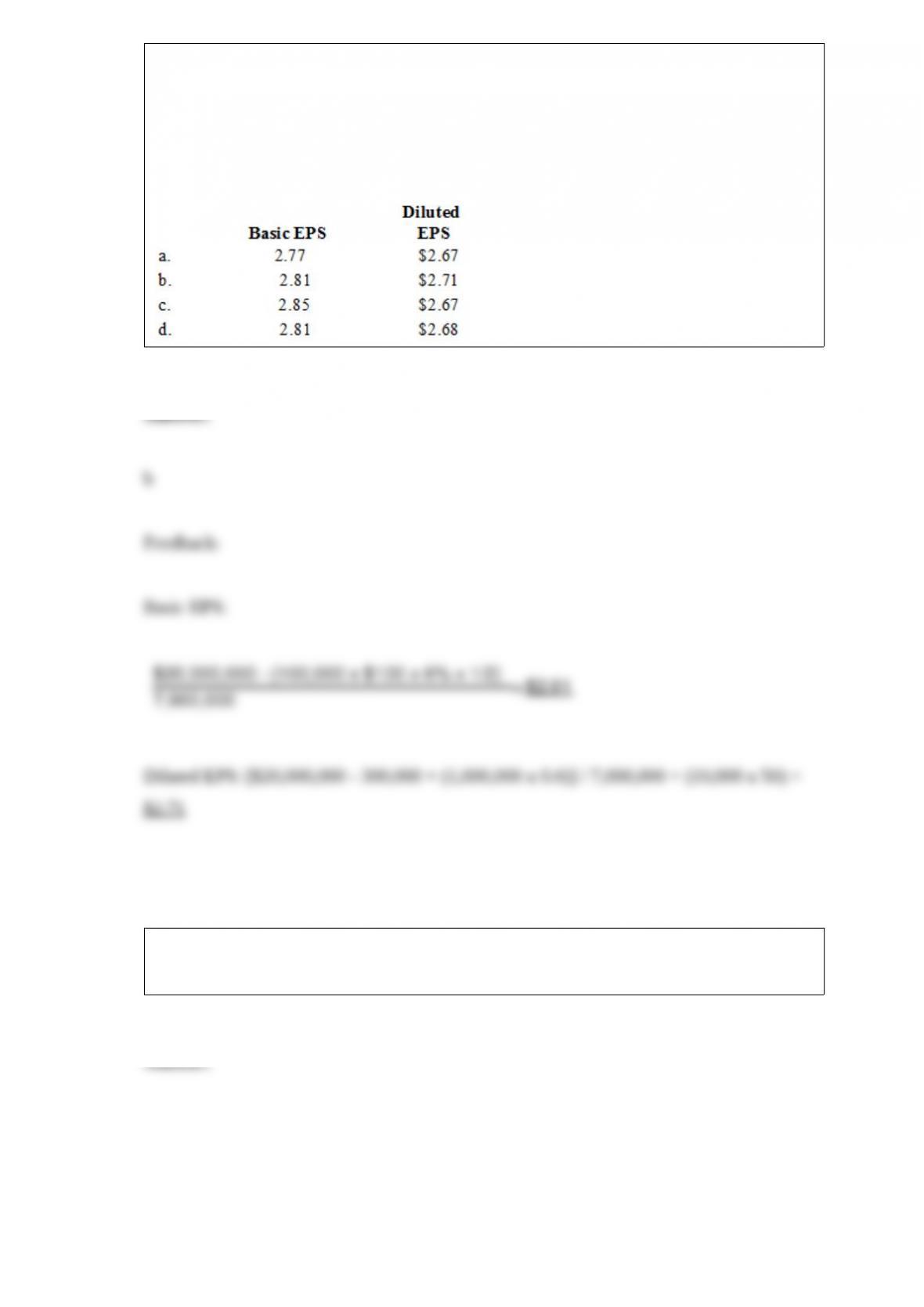

Ignatius Corporation had 7 million shares of common stock outstanding during the

current calendar year. It issued ten thousand $1,000, convertible bonds on January 1.

Each bond is convertible into 50 shares of common stock. The bonds were issued at

face amount and pay interest quarterly at an annual rate of 10%. On June 30, Ignatius

issued 100,000 shares of $100 par 6% cumulative preferred stock. Dividends are

declared and paid semiannually. Ignatius has an effective tax rate of 40%. Ignatius

would report the following EPS data (rounded) on its net income of $20 million:

() Prepare all appropriate journal entries, assuming a cash dividend in the amount of

$5.00 per share.

On January 1, 2016, for $18 million, Marker Company issued 10% bonds, dated

January 1, 2016, with a face amount of $20 million. For bonds of similar risk and

maturity, the market yield is 12%. Interest is paid semiannually on June 30 and

December 31.

Required:

1> Prepare the journal entry to record interest on June 30, 2016, using the effective

interest method.

2> Prepare the journal entry to record interest on December 31, 2016, using the

effective interest method.

Why are software development costs treated differently than other types of R&D?

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

What is the theoretical and practical trade-off when measuring the pension liability

using the projected benefit obligation compared to the accumulated benefit obligation?