1) Which of the following statements is most correct about an auditor’s required

communication with management and those charged with corporate governance?

A) The auditor is required to inform those charged with governance about significant

errors discovered and subsequently corrected by management

B) Any significant matter reported to those charged with governance must also be

communicated to management

C) Communication is required before the audit report is issued

D) Auditor does not have any requirement to communicate with anyone other than the

company’s senior management

2) Which of the following is not a problem with monetary-unit selection?

A) Population items with a zero recorded balance

B) Population items that should have a zero balance but do not

C) Accounts with negative balances

D) Accounts with small recorded balances that are significantly understated

3) The audit procedure which requires the auditor to record the last check number used

on the last day of the year and subsequently trace to the outstanding checks and the cash

disbursements records is performed to satisfy the audit objective of:

A) detail tie-in

B) existence

C) completeness

D) cutoff

4) The internal control that requires that “checks are prenumbered and accounted for”

satisfies the objective of:

A) accuracy

B) existence

C) completeness

D) posting and summarization

5) An auditor has been asked to report on the balance sheet of Kane Company but not

on the other basic financial statements. The auditor will have access to all information

underlying the basic financial statements. Under these circumstances, the auditor:

A) may accept the engagement because such engagements merely involve limited

reporting objectives

B) may accept the engagement but should disclaim an opinion because of an inability to

apply the procedures considered necessary

C) should refuse the engagement because there is a client-imposed scope limitation

D) should refuse the engagement because of a departure from generally accepted

auditing standards

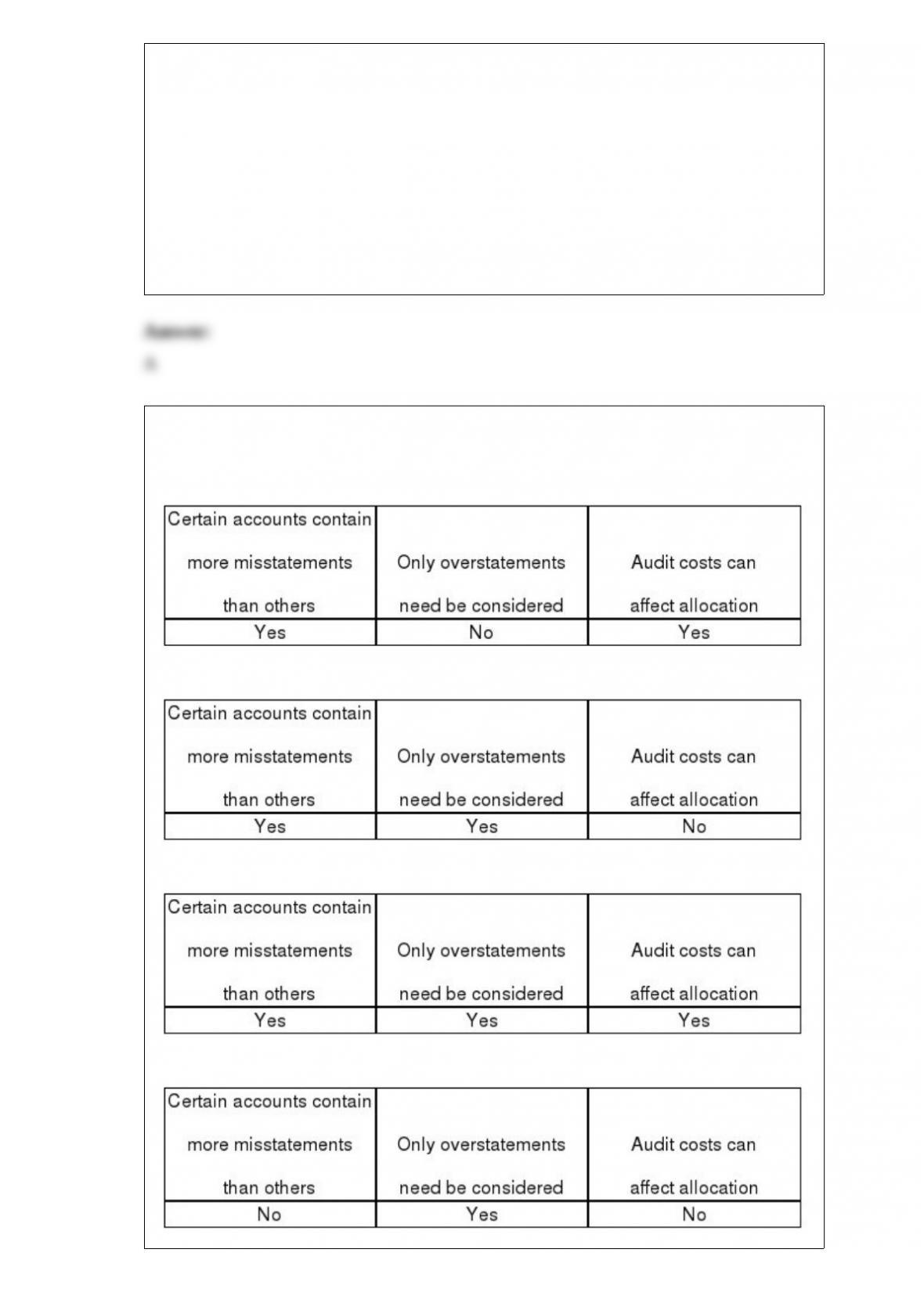

6) Which of the following are major difficulties auditors face when allocating

materiality to balance sheet accounts?

A)

B)

C)

D)

7) Which of the following audit procedures would be most useful in testing the cut-off

audit objective for payroll-related liabilities?

A) Review documentation for proper classification between long and short term

liabilities

B) Compare the clients accrual of payroll liabilities with the payroll tax return

C) Examine payment tax returns to determine that the expense was recorded in the

correct period

D) Examine subsequent cash disbursements to determine when the liabilities for payroll

were paid

8) Confirmations are among the most expensive type of evidence to obtain.

A) True

B) False

9) The preferred defense in third-party suits is:

A) lack of duty to perform

B) non-negligent performance

C) absence of causal connection

D) client fraud

10) Most tests of accounts receivable are based on what schedule, file, or listing?

A) Sales master file

B) Aged accounts receivable trial balance

C) Accounts receivable master file

D) Accounts receivable general ledger account

11) The three requirements for becoming a CPA include all but which of the following?

A) Uniform CPA examination requirement

B) Educational requirements

C) Character requirements

D) Experience requirement

12) A set of records for each piece of equipment that includes descriptive information,

date of acquisition, original cost, current year depreciation, and accumulated

depreciation is the:

A) acquisitions journal

B) depreciation schedule

C) fixed asset master file

D) file of purchase requisitions

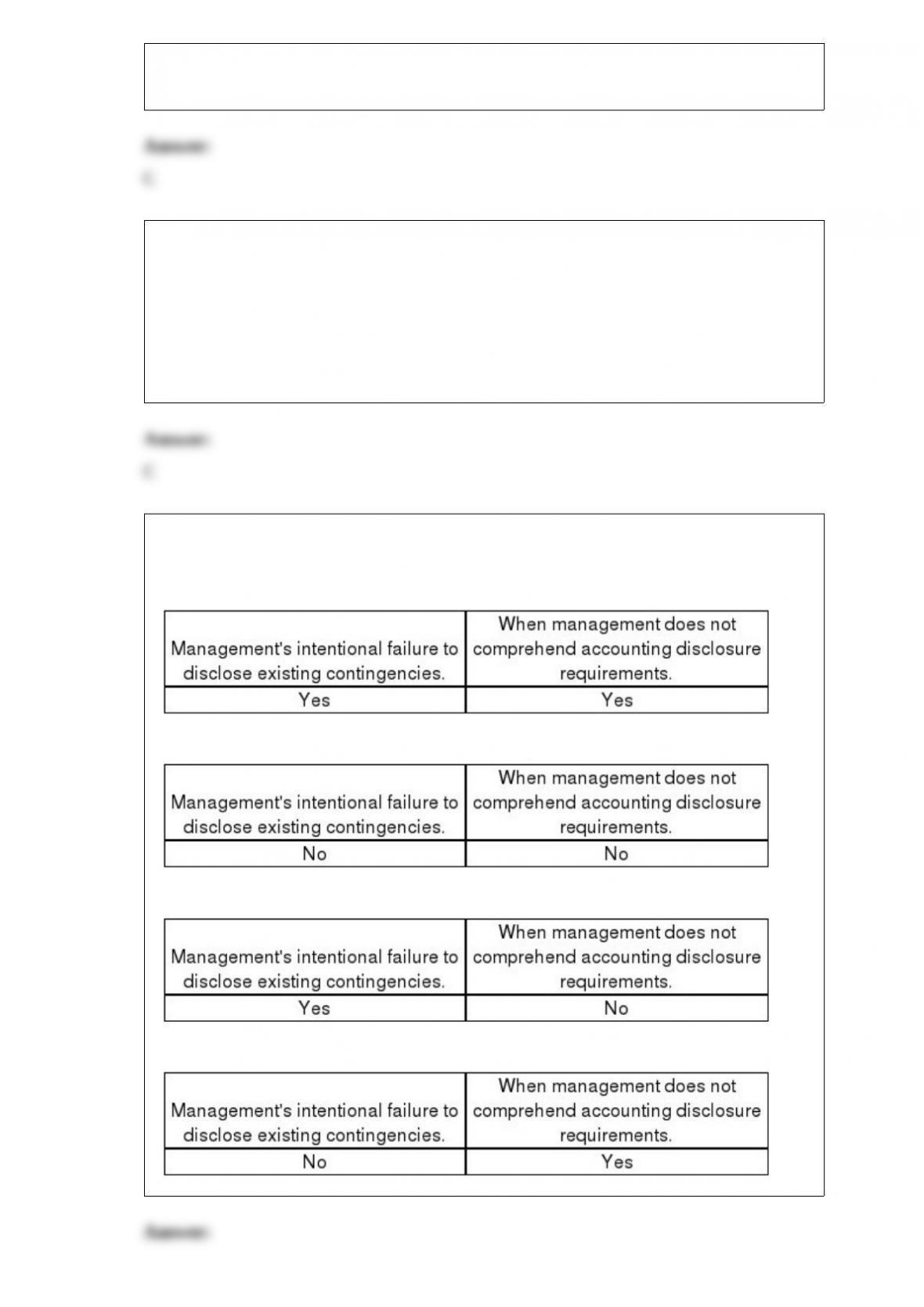

13) Inquiries of management regarding the possibility of unrecorded contingencies will

be useful in uncovering:

A)

B)

C)

D)

14) Which of the following is not a “cash equivalent”?

A) Time deposits

B) Certificates of deposit

C) Money market funds

D) Marketable securities

15) Which of the following would least concern an auditor regarding the lack of a

specific authorization to conduct the sales transaction?

A) granting of credit

B) shipment of goods

C) determination of discounts

D) selling of goods for cash

16) The tests of details of balances procedure which requires the auditor to trace the

totals of the notes payable list to the general ledger satisfies the audit objective of:

A) accuracy

B) existence

C) detail tie-in

D) completeness

17) “Physical examination” is the inspection or count by the auditor of items such as:

A) cash, inventory, and payroll timecards

B) cash, inventory, canceled checks, and sales documents

C) cash, inventory, canceled checks, and tangible fixed assets

D) cash, inventory, securities, notes receivable, and tangible fixed assets

18) Auditing standards (SAS No. 59) requires the auditor to evaluate whether there is a

substantial doubt about a client’s ability to continue as a going concern for at least:

A) one quarter beyond the balance sheet date

B) one quarter beyond the date of the auditor’s report

C) one year beyond the balance sheet date

D) one year beyond the date of the auditor’s report

19) General controls in smaller companies are usually less effective than in more

complex IT environments.

A) True

B) False

20) Which of the following balance-related audit objectives typically is assessed as

having high inherent risk for cash?

A) Existence

B) Cutoff

C) Detail tie-in

D) Presentation and disclosure

21) Auditors normally link controls and deficiencies in general controls to specific

transaction-related audit objectives.

A) True

B) False

22) An auditor who conducts an examination in accordance with generally accepted

auditing standards and concludes that the financial statements are fairly presented in

accordance with a comprehensive basis of accounting other than GAAP, should issue a:

A) review report

B) special kind of report

C) qualified opinion

D) disclaimer of opinion

23) Auditors accumulate evidence to:

A) defend themselves in the event of a lawsuit

B) justify the conclusions they have otherwise reached

C) satisfy the requirements of the Securities Acts of 1933 and 1934

D) enable them to reach conclusions about the fairness of the financial statements

24) Which of the following would generally not be a component of the audit of the

acquisition and payment cycle?

A) Adequacy of controls over acquisitions of long-lived assets

B) Tracing disposals of long-lived assets to the Fixed Asset Master File

C) Determining the adequacy of the funds available for capital expenditures

D) Reperformance of recorded depreciation expense

25) Which of the following audits can be regarded as generally being a compliance

audit?

A) IRS agents’ examinations of taxpayer returns

B) GAO auditor’s evaluation of the computer operations of governmental units

C) An internal auditor’s review of a company’s payroll authorization procedures

D) A CPA firm’s audit of a public company

26) Analytical procedures must be used in the planning and completion phases of the

audit.

A) True

B) False

27) Which of the following types of procedures will be performed in an audit of internal

control over financial reporting?

A)

B)

C)

D)

28) The approach to auditing patents and copyrights is similar to that used for property,

plant, and equipment accounts.

A) True

B) False

29) Match seven of the terms for documents and records (a-k) with the descriptions

provided below (1-7):

a.Customer order form

b.Sales order

c.Bill of lading

d.Sales invoice

e.Summary sales report

f.Accounts receivable master file

g.Monthly statement

h.Remittance advice

i.Prelisting of cash receipts

j.Credit memo

k.Uncollectible account authorization form

________ 1> A list prepared when cash is received by someone who has no

responsibility for recording sales, accounts receivable, or cash, and has no access to the

accounting records. It is used to verify whether cash received was recorded and

deposited at the correct amounts and on a timely basis.

________ 2> A document indicating a reduction in the amount due from a customer

because of returned goods or an allowance.

________ 3> A document prepared to initiate shipment of goods, indicating the

description of the merchandise, the quantity shipped, and other relevant data. It is a

written contract between the carrier and seller of the receipt and shipment of goods.

________ 4> A document for communicating the description, quantity, and related

information for goods ordered by a customer. This is frequently used to indicate credit

approval and authorization for shipment.

________ 5> A document mailed to the customer and typically returned to the seller

with the cash payment.

________ 6> A document used internally to indicate authority to write-off an account

receivable as uncollectible.

________ 7> A document or electronic record indicating the description and quantity of

goods sold, the price, freight charges, insurance, terms, and other relevant data.

30) Financial statement users are typically more concerned with an unqualified report

with explanatory paragraphs than they are with a disclaimer of opinion.

A) True

B) False

31) For effective internal control, employees maintaining the accounts receivable

subsidiary ledger should not also approve:

A) employee overtime wages

B) credit granted to customers

C) write-offs of customer accounts

D) cash disbursements

32) Which of the following statements is not correct with respect to analytical

procedures?

A) Auditing standards emphasize the need for auditors to develop and use expectations

B) Analytical procedures must be performed throughout the audit

C) Analytical procedures may be performed at any time during the audit

D) Analytical procedures use comparisons and relationships to assess whether account

balances appear reasonable

33) Which is not a purpose of an economy and efficiency audit?

A) Whether the entity is acquiring, protecting, and using resources economically and

efficiently

B) The causes of inefficiencies and uneconomical practices

C) Whether the entity has complied with laws and regulations concerning matters of

economy and efficiency

D) Each of the above is a purpose

34) A document used by organizations to establish a formal means of recording and

controlling acquisitions which usually contains a package of documents about the

acquisition is the:

A) voucher

B) purchase order

C) receiving report

D) purchase requisition

35) In making client acceptance decisions the audit firm will consider:

A) inherent and control risk of the client

B) audit risk to the CPA Firm

C) the client’s business risk and the CPA Firm’s engagement risk

D) CPA Firm’s potential ongoing revenue from the audit client

36) The independent auditor should acquire an understanding of the internal audit

function as it relates to the independent auditor’s study and evaluation of internal

control because the:

A) audit programs, working papers, and reports of internal auditors can often be used as

a substitute for the work of the independent auditor’s staff

B) procedures performed by the internal audit staff may eliminate the independent

auditor’s need for an extensive study and evaluation of internal control

C) work performed by internal auditors may be a factor in determining the nature,

timing, and extent of the independent auditor’s procedures

D) understanding of the internal audit function is an important substantive test to be

performed by the independent auditor

37) Attributes sampling would be an appropriate method to use on which one of the

following procedures in an audit program?

A) Review sales transactions for large and unreasonable amounts

B) Observe whether the duties of the accounts receivable clerk are separate from

handling cash

C) Examine a sample of duplicate sales invoices for credit approval by the credit

manager

D) Review the aged schedule of accounts receivable to determine if receivables from

officers are included

38) Explain the audit objective allocation and why it is important to have accurate

allocation within the financial statements, particularly for property, plant, and

equipment

39) Discuss the factors an auditor should consider before accepting a company as an

audit client.

40) Draft a report that would be appropriate when an independent accountant has

performed a compilation of financial statements which substantially omits all

disclosures and the statement of cash flows required by GAAP.