1) The order in which the costs of service departments are allocated will affect the

amounts allocated to an operating department when the step-down method is used.

2) Joint products are products that are sold to customers as a set or as part of a group of

products.

3) If a company is considering accepting a number of jobs, but there is insufficient

production capacity to do all of them, then the jobs that require the greatest amount of

the production capacity should be rejected.

4) When the number of units in work in process and finished goods inventories

decrease, absorption costing net operating income will typically be greater than variable

costing net operating income.

5) For a capital intensive, automated company the break-even point will tend to be

higher and the margin of safety will be lower than for a less capital intensive company

with the same sales.

6) Under the simplifying assumptions made in the text, to calculate the amount of

income tax expense associated with an investment project, first calculate the

incremental net income earned during each year of the project and then multiply each

year’s incremental net income by the tax rate.

7) The profitability index for a volume trade-off decision involving products should be

computed by dividing the unit contribution margin of a product by the amount of the

constrained resource required by one unit of the product.

8) A cost that is traceable to a segment through activity-based costing may or may not

be an avoidable cost for decision making.

9) Absolute profitability refers to the process of deciding which products to drop when

a constraint forces trade-offs.

10) What would be the total appraisal cost appearing on the quality cost report?

A.$269,000

B.$170,000

C.$136,000

D.$78,000

11) Mendoza Corporation manufactures and sells one product. The following

information pertains to the company’s first year of operations:

The company does not have any variable manufacturing overhead costs or variable

selling and administrative costs. During its first year of operations, the company

produced 47,000 units and sold 45,000 units. The company’s only product is sold for

$275 per unit.

Required:

a. Assume the company uses super-variable costing. Compute the unit product cost for

the year and prepare an income statement for the year.

b. Assume that the company uses a variable costing system that assigns $24 of direct

labor cost to each unit that is produced. Compute the unit product cost for the year and

prepare an income statement for the year.

c. Prepare a reconciliation that explains the difference between the super-variable

costing and variable costing net incomes.

12) The total cash flow net of income taxes in year 2 is:

A.$96,000

B.$24,000

C.$80,000

D.$120,000

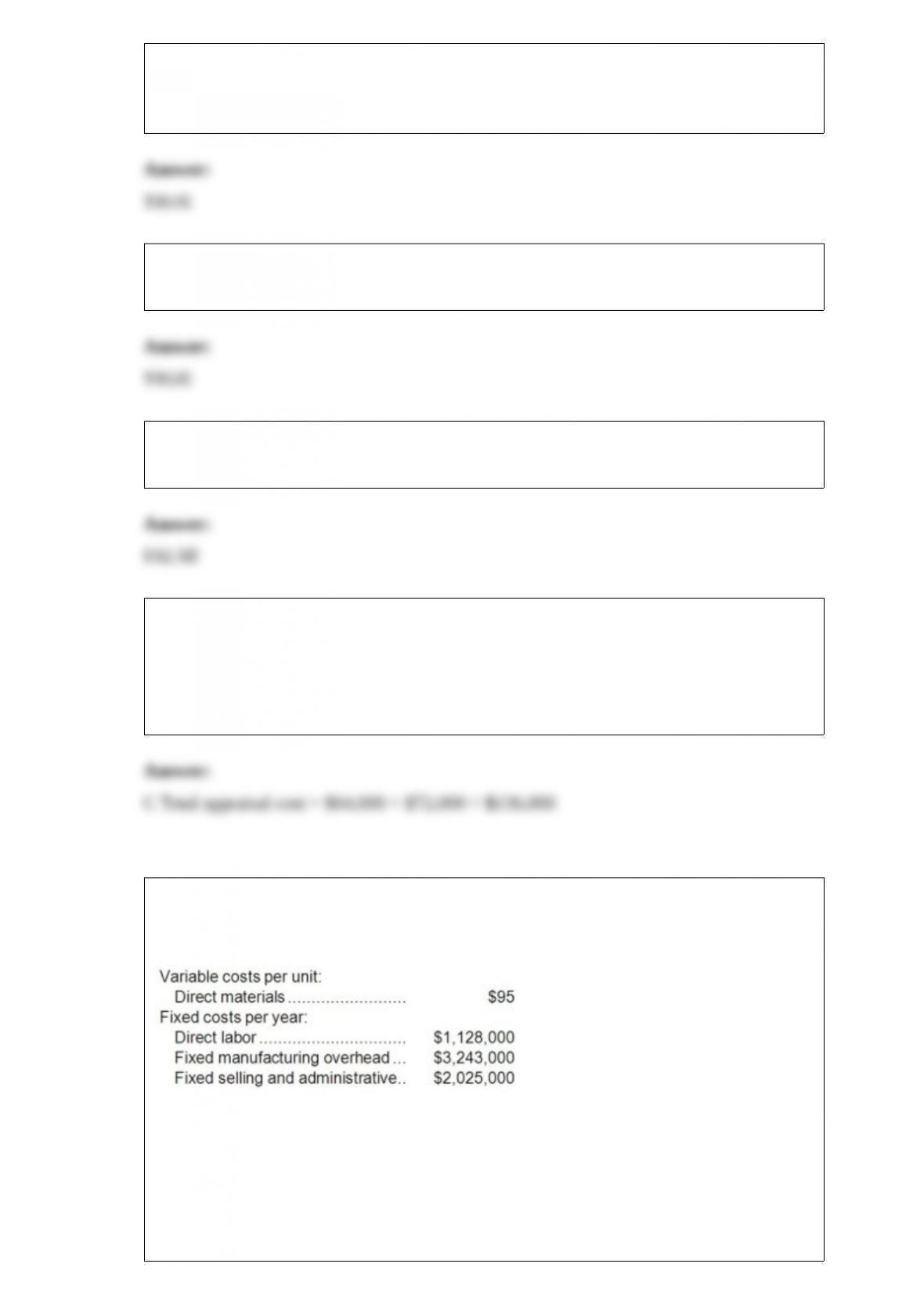

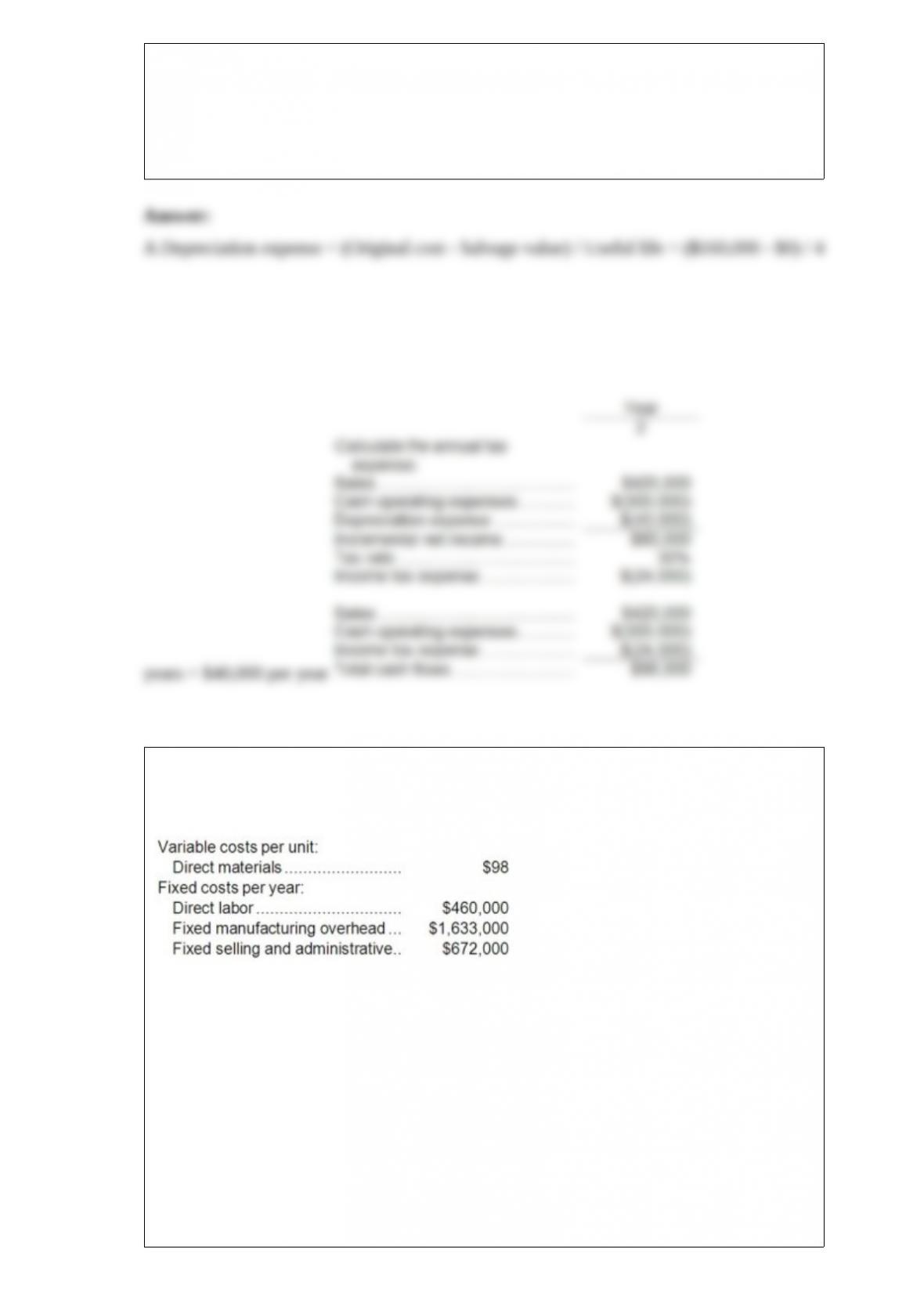

13) Grand Corporation manufactures and sells one product. The following information

pertains to the company’s first year of operations:

The company does not have any variable manufacturing overhead costs or variable

selling and administrative costs. During its first year of operations, the company

produced 23,000 units and sold 21,000 units. The company’s only product is sold for

$254 per unit.

Required:

a. Assume the company uses super-variable costing. Compute the unit product cost for

the year and prepare an income statement for the year.

b. Assume that the company uses a variable costing system that assigns $20 of direct

labor cost to each unit that is produced. Compute the unit product cost for the year and

prepare an income statement for the year.

c. Assume that the company uses an absorption costing system that assigns $20 of direct

labor cost and $71 of fixed manufacturing overhead to each unit that is produced.

Compute the unit product cost for the year and prepare an income statement for the

year.

d. Prepare a reconciliation that explains the difference between the super-variable

costing and variable costing net incomes.

e. Prepare a reconciliation that explains the difference between the super-variable

costing and absorption costing net incomes.

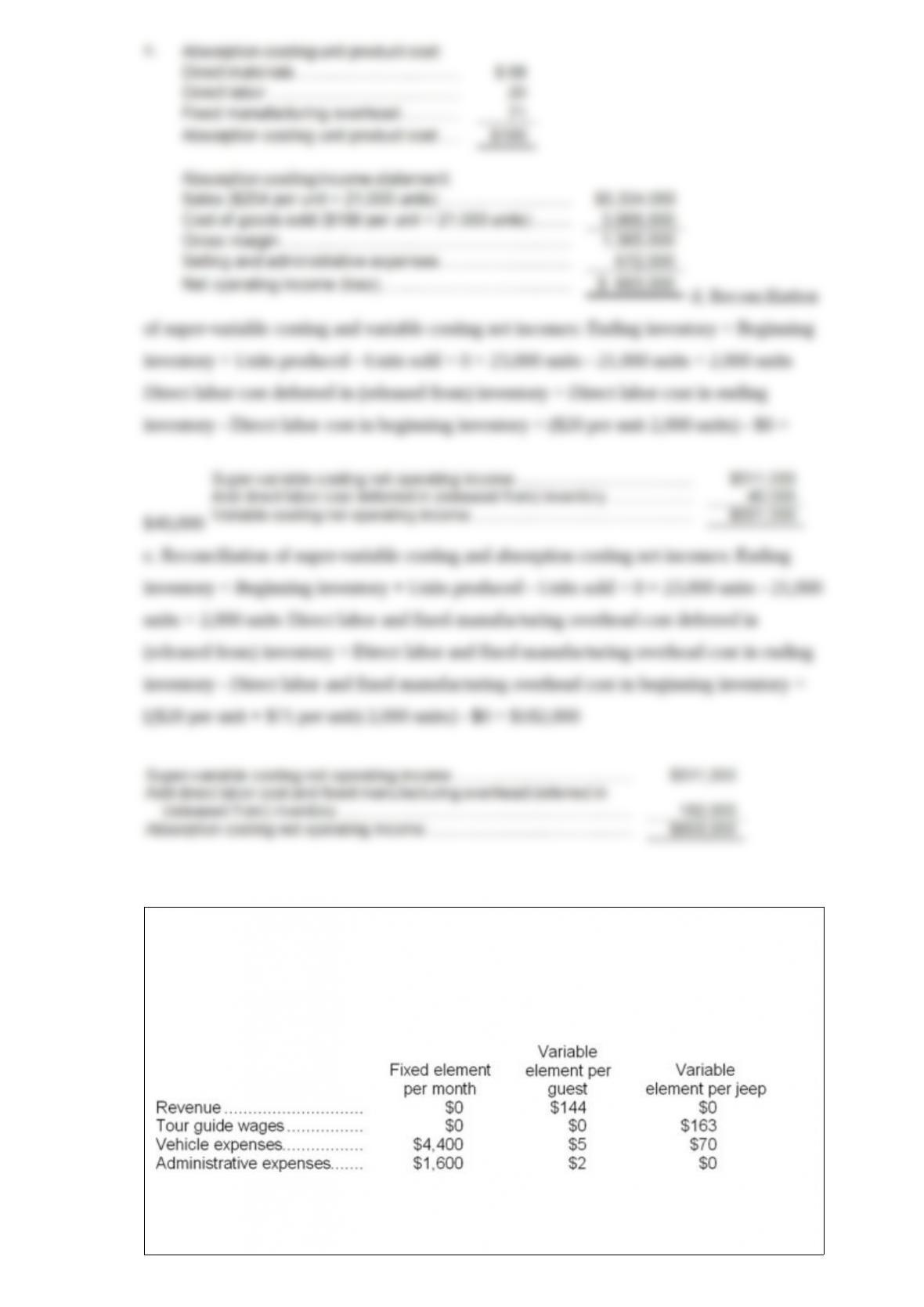

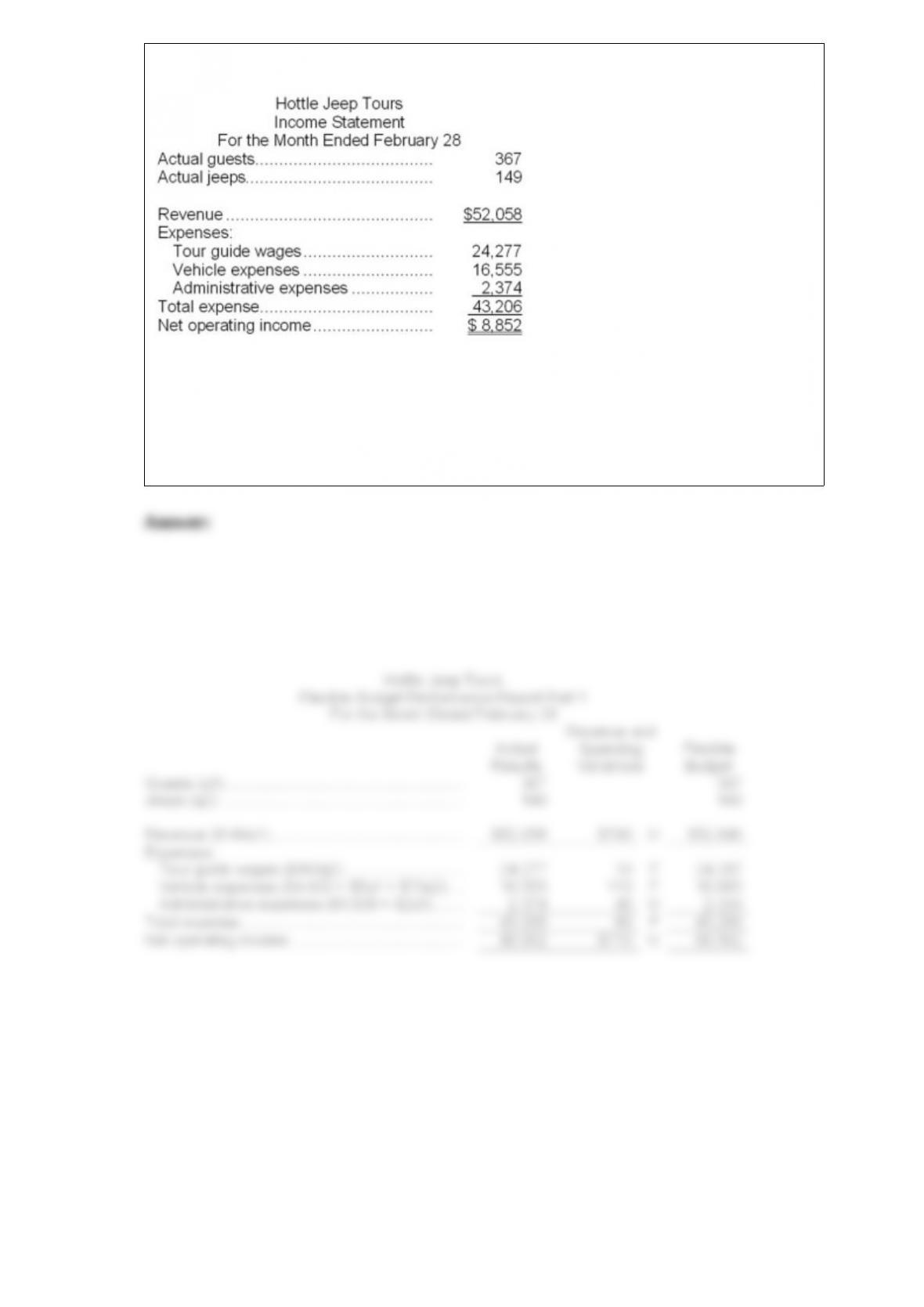

14) Hottle Jeep Tours operates jeep tours in the heart of the Colorado Rockies. The

company bases its budgets on two measures of activity (i.e., cost drivers), namely

guests and jeeps. One vehicle used in one tour on one day counts as a jeep. Each jeep

has one tour guide. The company uses the following data in its budgeting:

In February, the company budgeted for 342 guests and 146 jeeps. The company’s

income statement showing the actual results for the month appears below:

Required:

Prepare a flexible budget performance report showing both the company’s activity

variances and revenue and spending variances for February. Label each variance as

favorable (F) or unfavorable (U).

15) Bakos Corporation bases its predetermined overhead rate on variable manufacturing

overhead cost of $8.80 per machine-hour and fixed manufacturing overhead cost of

$100,688 per period. If the denominator level of activity is 2,800 machine-hours, the

variable component in the predetermined overhead rate would be:

A.$44.76

B.$35.96

C.$43.52

D.$8.80

16) The company’s price-earnings ratio is closest to:

A.19.79

B.0.51

C.8.36

D.12.53

17) Mciver Corporation uses activity-based costing to assign overhead costs to

products. Overhead costs have already been allocated to the company’s three activity

cost pools as follows: Machining, $10,900; Order Filling, $10,500; and Other, $75,600.

Machining costs are assigned to products using machine-hours (MHs) and Order Filling

costs are assigned to products using the number of orders. The costs in the Other

activity cost pool are not assigned to products. Activity data appear below:

The activity rate for the Machining activity cost pool under activity-based costing is

closest to:

A.$2.67 per MH

B.$1.09 per MH

C.$0.93 per MH

D.$9.70 per MH

18) Using the high-low method of analysis, the variable cost per meal served in the

cafeteria would be estimated to be:

A) $1.50

B) $2.00

C) $2.80

D) $1.00

19) Division T of Clocker Company makes a timer which it sells for $30 to outside

customers. The division has supplied the following data concerning the timer:

Division S of Clocker Company is currently buying 5,000 similar timers each month

from an overseas supplier at $27 each. Division S would like to acquire its timers from

Division T if the price is right.

Suppose Division T is operating at capacity and can sell all of the timers it produces to

outside customers at its usual selling price. According to the formula in the text, what is

the lowest acceptable transfer price from the viewpoint of the selling division?

A.$30 per timer

B.$27 per timer

C.$25 per timer

D.$15 per timer

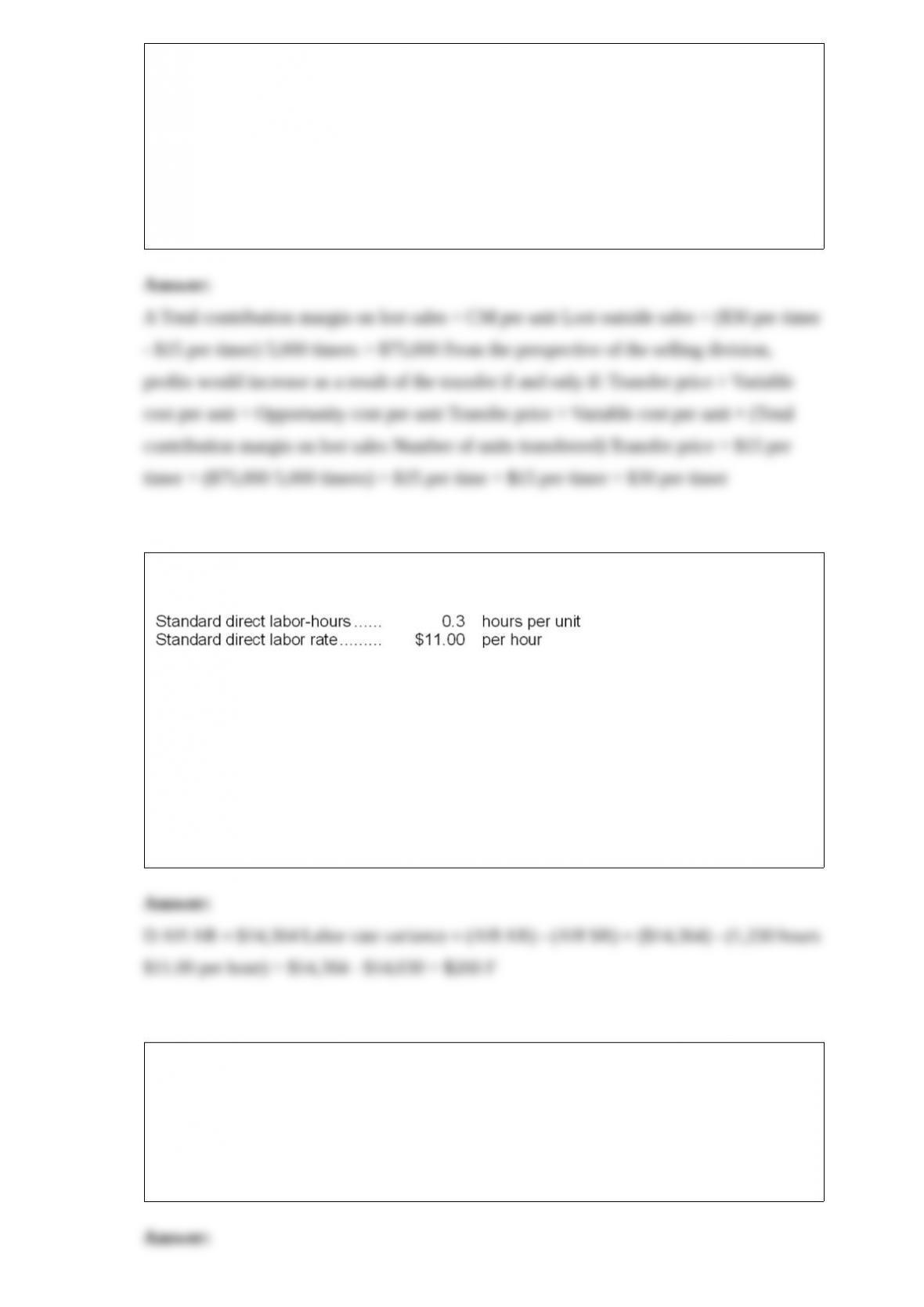

20) Jurczyk Corporation makes a product that has the following direct labor standards:

In December the company’s budgeted production was 4,600 units, but the actual

production was 4,400 units. The company used 1,330 direct labor-hours to produce this

output. The actual direct labor cost was $14,364.

The labor rate variance for December is:

A.$264 F

B.$266 U

C.$264 U

D.$266 F

21) What is the net total dollar advantage (disadvantage) of purchasing the part rather

than making it?

A) $264,000

B) $(328,000)

C) $548,000

D) $(64,000)

22) All other things being the same, which of the following would increase the residual

income?

A.Decrease in average operating assets.

B.Decrease in sales.

C.Increase in minimum required return.

D.Decrease in net operating income.

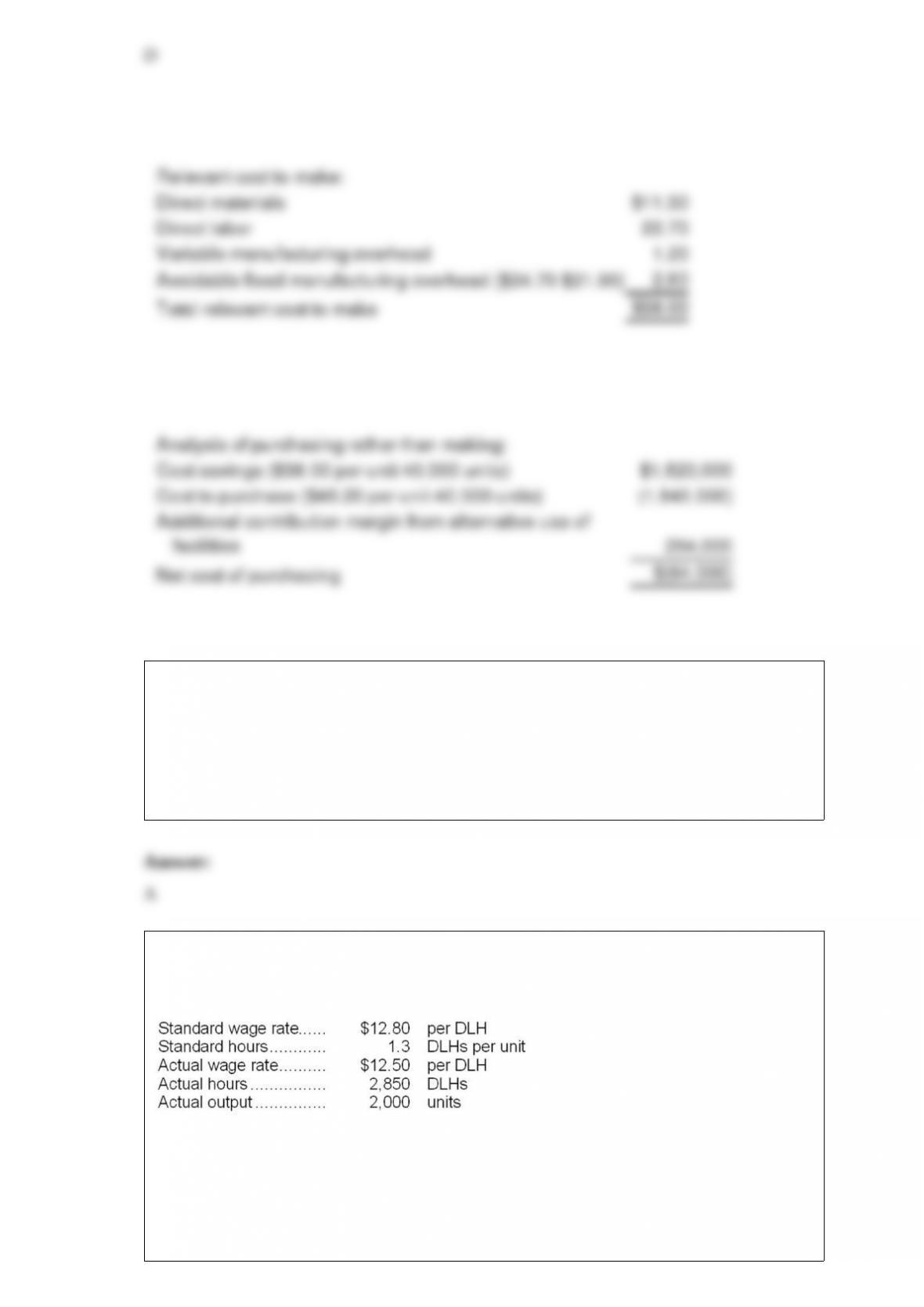

23) Cafferty Corporation has provided the following data concerning its direct labor

costs for March:

The journal entry to record the incurrence of direct labor costs in March would include

the following for Work in Process:

A.Credit of $33,280

B.Debit of $35,625

C.Debit of $33,280

D.Credit of $35,625

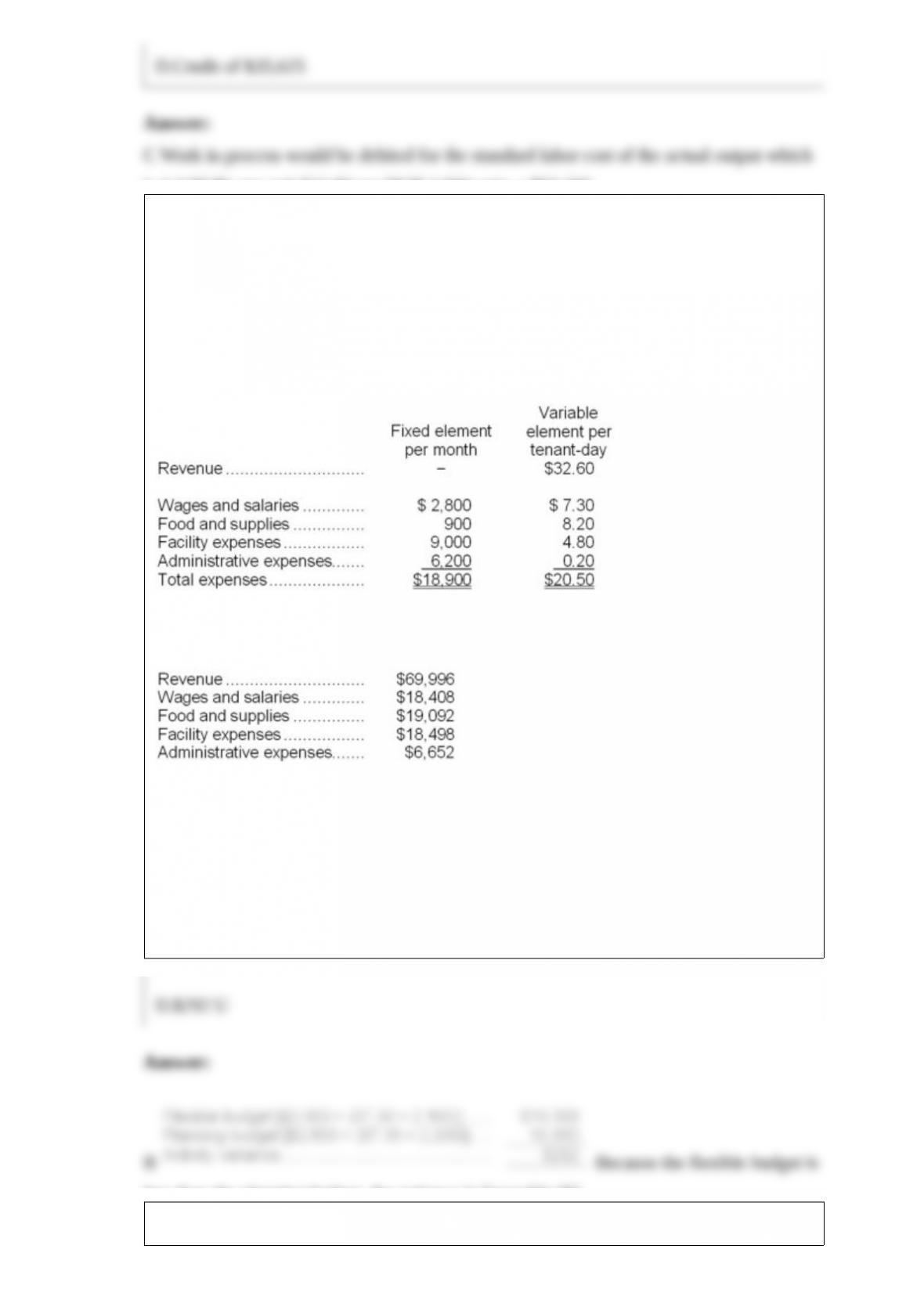

24) Perla Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During March, the kennel budgeted for

2,200 tenant-days, but its actual level of activity was 2,160 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for March:

Data used in budgeting:

Actual results for March:

The activity variance for wages and salaries in March would be closest to:

A.$452 F

B.$292 F

C.$452 U

D.$292 U

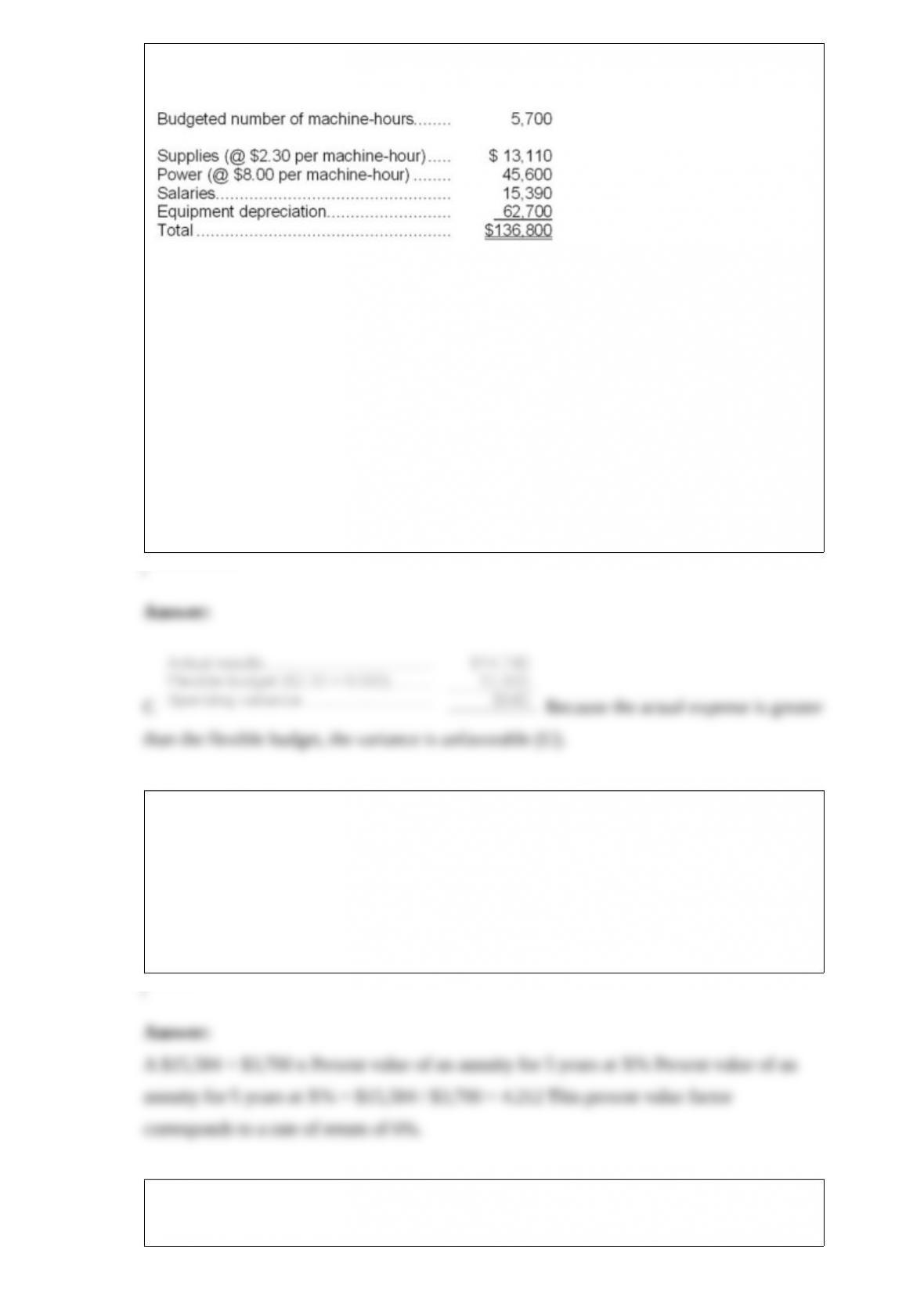

25) Zike Corporation’s static planning budget for October appears below. The company

bases its budgets on machine-hours.

In October, the actual number of machine-hours was 6,000, the actual supplies cost was

$14,740, the actual power cost was $49,170, the actual salaries cost was $15,390, and

the actual equipment depreciation was $63,670.

The spending variance for supplies cost in the flexible budget performance report for

the month should be:

A.$940 F

B.$1,630 U

C.$940 U

D.$1,630 F

26) You have deposited $15,584 in a special account that has a guaranteed rate of

return. If you withdraw $3,700 at the end of each year for 5 years, you will completely

exhaust the balance in the account. The guaranteed rate of return is closest to:

A.6%

B.19%

C.24%

D.4%

27) Clemmens Corporation has two major business segments: Consumer and

Commercial. Data for the segments and for the company for August appear below:

In addition, common fixed expenses totaled $265,000 and were allocated as follows:

$135,000 to the Consumer business segment and $130,000 to the Commercial business

segment.

The contribution margin of the Commercial business segment is:

A.$17,000

B.$152,000

C.$476,000

D.$265,000

28) Using the least-squares regression method, the estimate of the variable component

of inspection cost per unit produced is closest to:

A.$5.40

B.$5.33

C.$5.43

D.$16.07

29) The company is considering launching a new product that would have a variable

cost of $178.00 per unit and no avoidable fixed costs. It would require 3 minutes of the

constrained resource. The absolute minimum acceptable selling price for the new

product should be:

A.$184.80

B.$204.40

C.$178.00

D.$198.40