Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1) 1.Prior period adjustment

2) 2.Depreciation

3) 3.Accelerated methods

4) 4.Change in useful life

5) 5.Repairs and maintenance

A. Allocation of cost for plant and equipment.

B. Results from subsequent year correction of a material error

C. Generate declining amounts of depreciation over time

D. Is a change in accounting estimate

E. Expenditures made to maintain a given level of benefits from an asset

Answer:

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1)Current assets

2)Subsequent events

3)Property, plant, and equipment

4)Short-term investments

5)Cash equivalent

A. Liquid investments not classified as cash equivalents.

B. Includes buildings and machinery.

C. Items expected to be converted to cash or consumed within one year or the operating

cycle.

D. Occurs after the fiscal year-end, but before the statements are issued.

E. One-month U.S. Treasury bill.

Answer:

Prepayments made on an operating lease are considered to be: A. A lease expense.

B. A depreciable asset.

C. Executory costs.

D. A prepayment of rent.

Answer:

In a perpetual inventory system, the cost of inventory sold is: A. Debited to accounts

receivable.

B. Credited to cost of goods sold.

C. Debited to cost of goods sold.

Answer:

For a leased asset under a lease that qualifies as a capital lease because of a bargain

purchase option, the depreciation period used by the lessee must be: A. The same period

that was used by the lessor.

B. The useful life to the lessee.

C. The term of the lease regardless of the lease provisions.

D. The remaining life of the asset at the time the lease agreement took effect.

Answer:

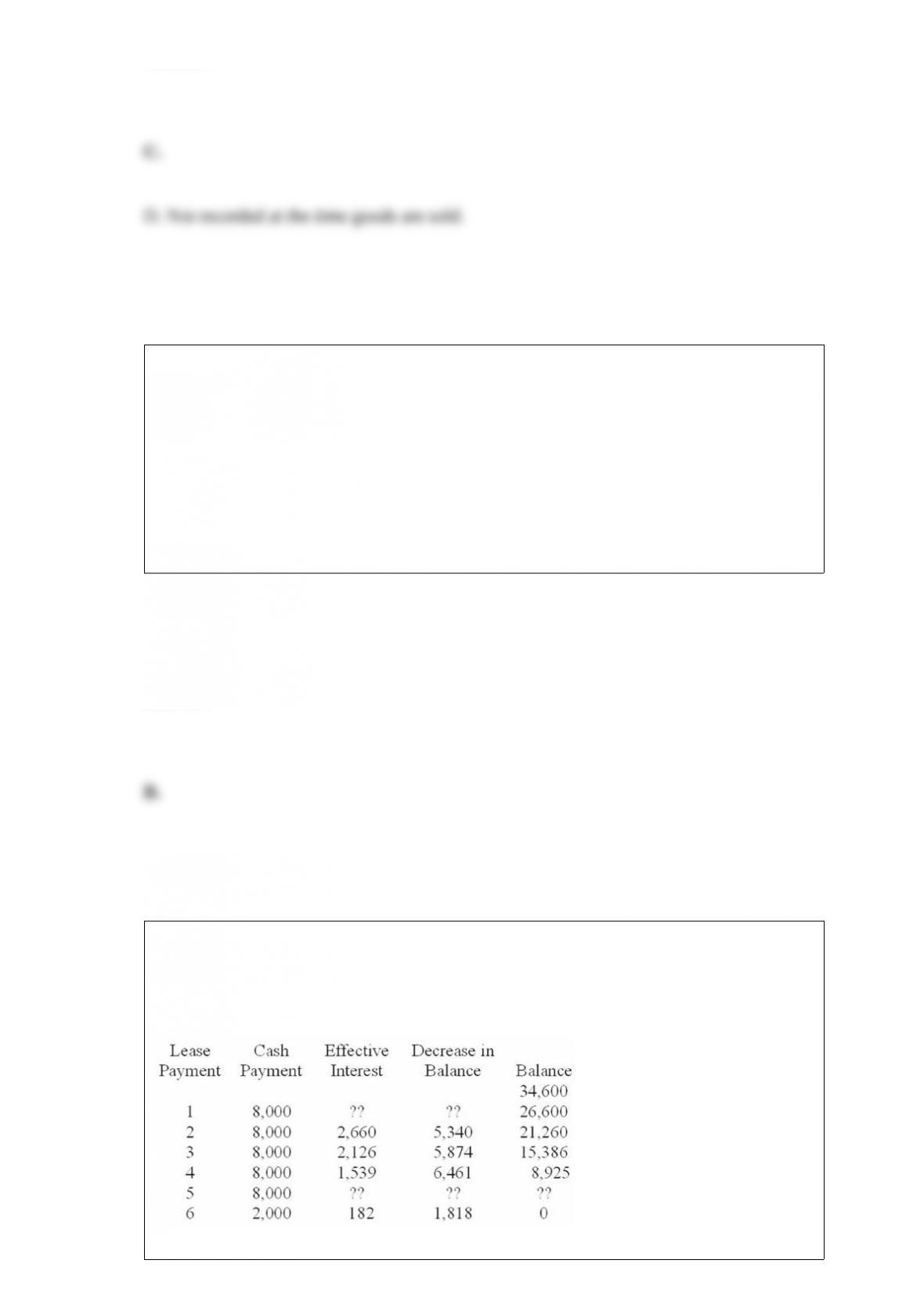

Refer to the following lease amortization schedule. The five payments are made

annually starting with the inception of the lease. A $2,000 bargain purchase option is

exercisable at the end of the five-year lease. The asset has an expected economic life of

eight years.

What is the total interest paid over the term of the lease? A. $42,000.

B. $8,200.

C. $7,400.

D. $3,460.

Answer:

In the statement of cash flows, inflows and outflows of cash from buying and selling

available for sale securities are considered: A. Operating activities.

B. Financing activities.

C. Investing activities.

D. Noncash financing activities.

Answer:

When an equity security is appropriately carried and reported as securities available for

sale, a gain should be reported in the income statement: A. When the fair value of the

security increases.

B. When the present value of the security increases.

C. Only when the Dow Jones Industrial Average increases at least 100 points.

D. Only when the security is sold.

Answer:

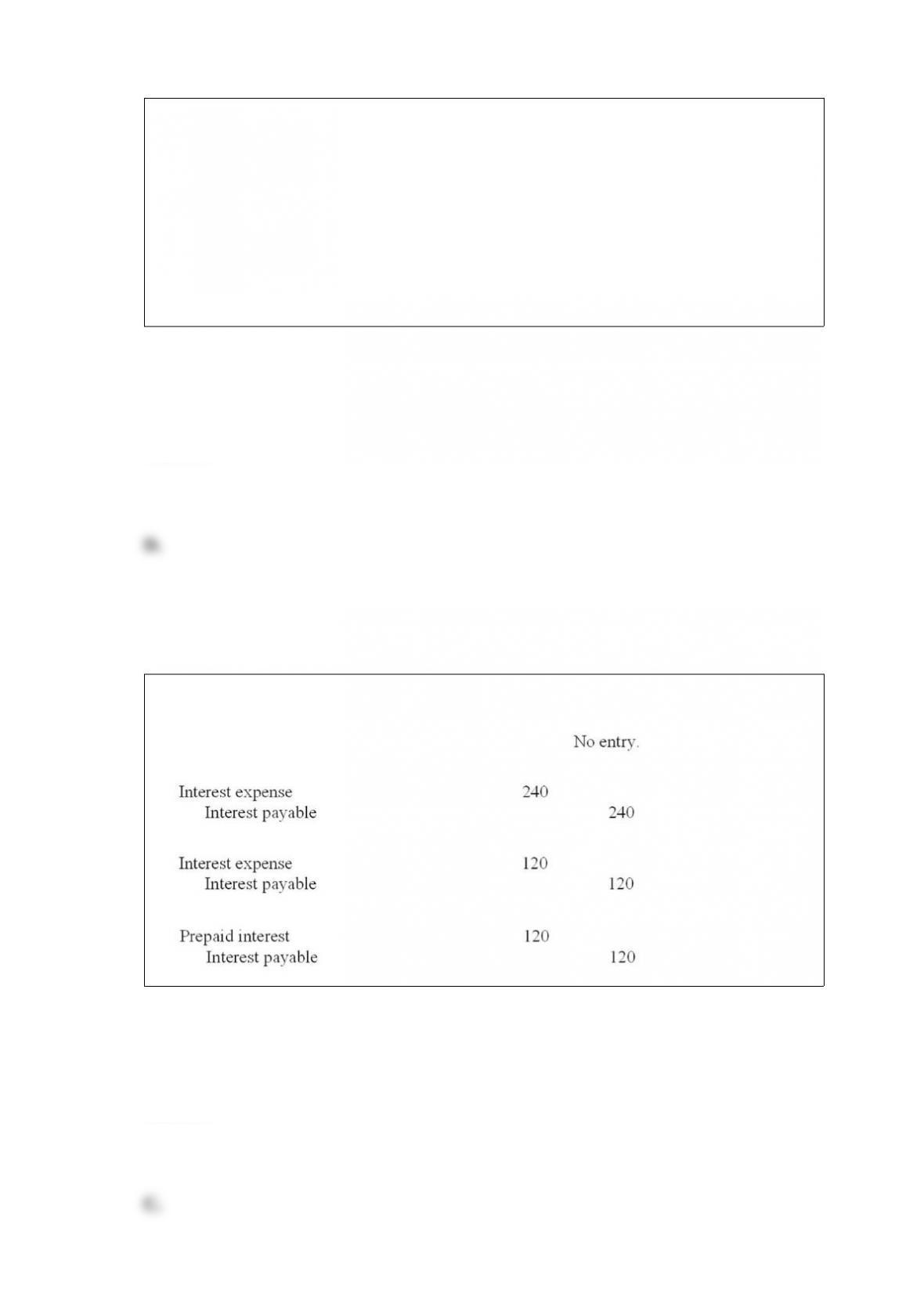

Mama’s Pizza Shoppe borrowed $8,000 at 9% interest on May 1, 2013, with principal

and interest due on October 31, 2014. The company’s fiscal year ends June 30, 2013.

What adjusting entry is necessary on June 30, 2013? A.

B.

C.

D.

Answer:

Melanie Corporation declared cash dividends of $13,500 during the current year. The

beginning and ending balances in dividends payable were $450 and $750, respectively.

What was the amount of cash paid for dividends? A. $12,750.

B. $13,800.

C. $12,900.

D. $13,200.

Answer:

Which of the following is not a reason to consider a decline in the fair value of a debt

investment to be “other than temporary”? A. The investor determines that a credit loss

exists on the investment.

B. The investor intends to sell the investment.

C. The investor believes it is “more likely than not” that the investor will be required to

sell the investment prior to recovering the amortized cost of the investment less any

credit losses arising in the current year.

D. The investor intends to hold the investment to maturity.

Answer:

Assuming an asset is used evenly over a four-year service life, which method of

depreciation will always result in the largest amount of depreciation in the first year? A.

Straight-line.

B. Units-of-production.

C. Double-declining balance.

D. Sum-of-the-year’s digits.

Answer:

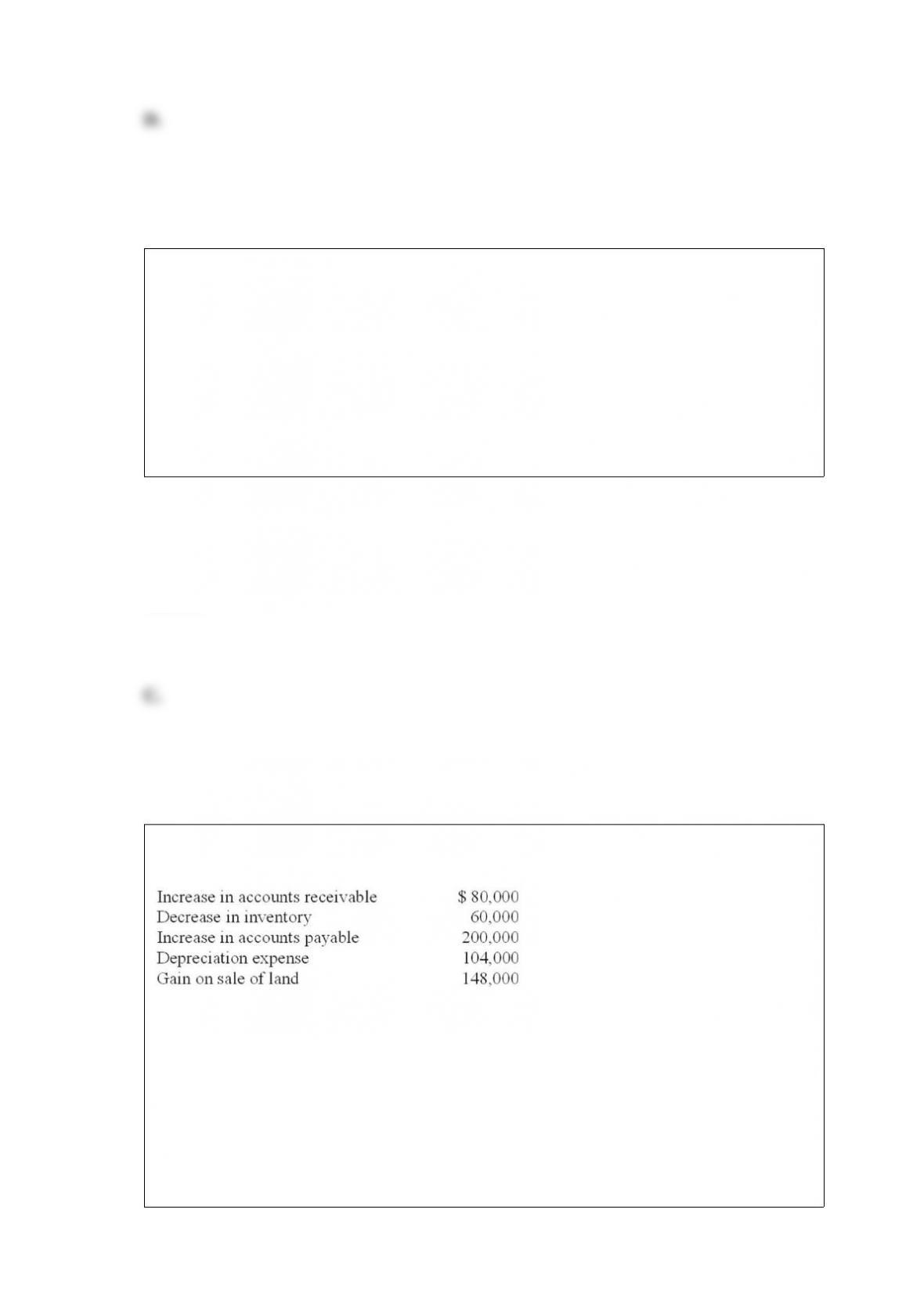

S Company reported net income for 2013 in the amount of $400,000. The company’s

financial statements also included the following:

What is net cash provided by operating activities under the indirect method? A.

$432,000.

B. $536,000.

C. $580,000.

D. $832,000.

Answer:

On March 31, 2013, M. Belotti purchased the right to remove gravel from an old rock

quarry. The gravel is to be sold as roadbed for highway construction. The cost of the

quarry rights was $164,000, with estimated salable rock of 20,000 tons. During 2013,

Belotti loaded and sold 4,000 tons of rock and estimated that 16,000 tons remained at

December 31, 2013. At January 1, 2014, Belotti estimated that 20,000 tons still

remained. During 2014, Belotti loaded and sold 8,000 tons.

Belotti would record depletion in 2014 of: A. $54,667.

B. $65,600.

C. $52,480.

D. $55,760.

Answer:

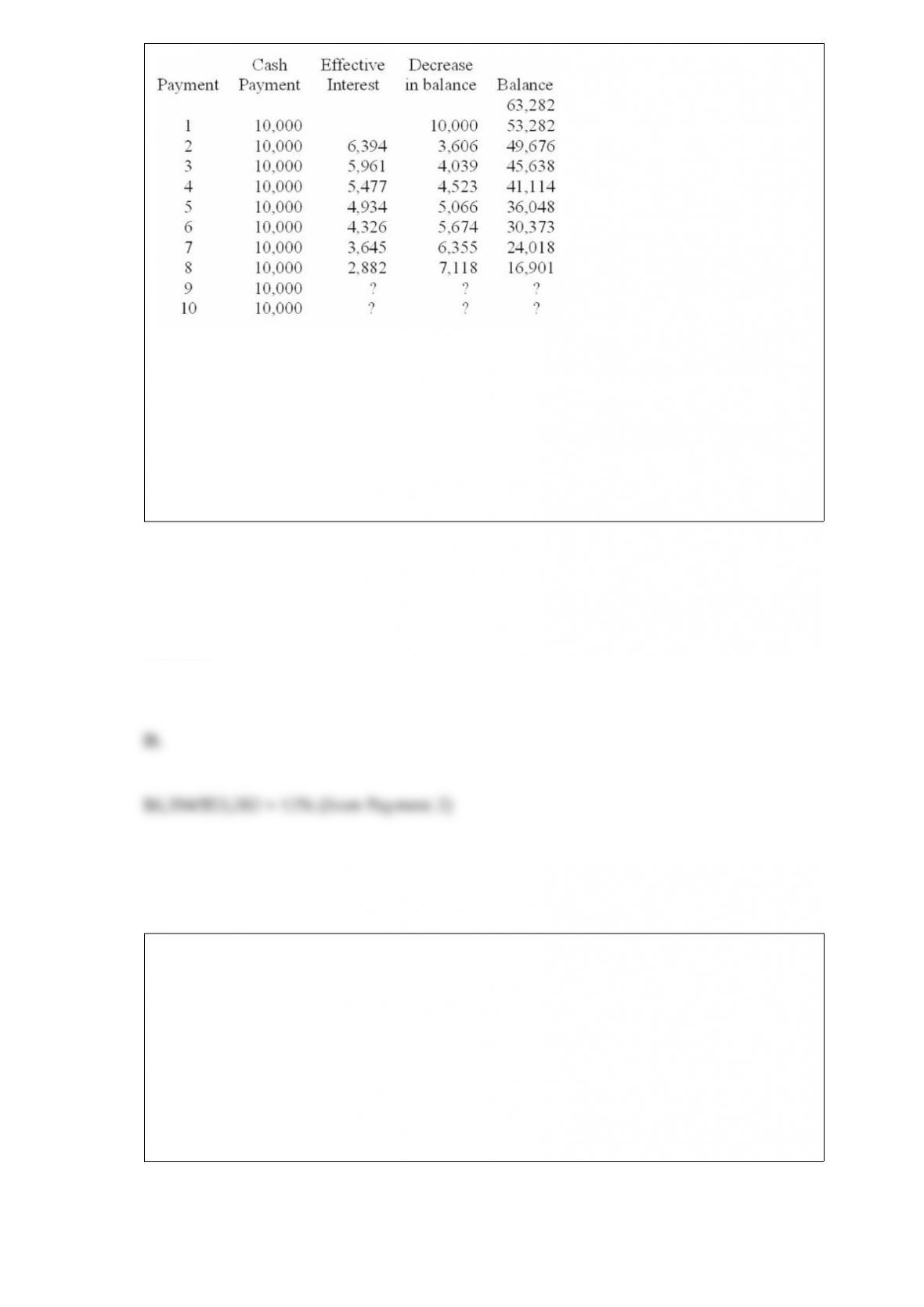

Refer to the following lease amortization schedule. The 10 payments are made annually

starting with the inception of the lease. Title does not transfer to the lessee and there is

no bargain purchase option or guaranteed residual value. The asset has an expected

economic life of 12 years. The lease is noncancelable.

What is the effective annual interest rate? A. 9%.

B. 10%.

C. 11%.

D. 12%.

Answer:

Which of the following is reported as a deduction from net income when using the

indirect method to determine net cash flows from operating activities? A. Depreciation

expense.

B. Amortization of a patent.

C. Amortization of premium on bonds payable.

D. Dividends declared.

Answer:

Bond X and bond Y both are issued by the same company. Each of the bonds has a

maturity value of $100,000 and each pays interest at 8%. The current market rate of

interest is 8% for each. Bond X matures in 7 years while bond Y matures in 10 years.

Which of the following is correct? A. Both bonds sell for the same amount.

B. Both bonds sell for more than $100,000.

C. Bond X sells for more than bond Y.

D. Bond Y sells for more than bond X.

Answer:

Cash equivalents do not include: A. Money market funds.

B. High grade marketable equity securities.

C. U.S. treasury bills.

D. Commercial paper.

Answer:

Accounting for impairment losses: A. Involves a two-step process for recoverability and

measurement.

B. Applies only to depreciable assets.

C. Applies only to assets with finite lives.

D. All of the above are correct.

Answer:

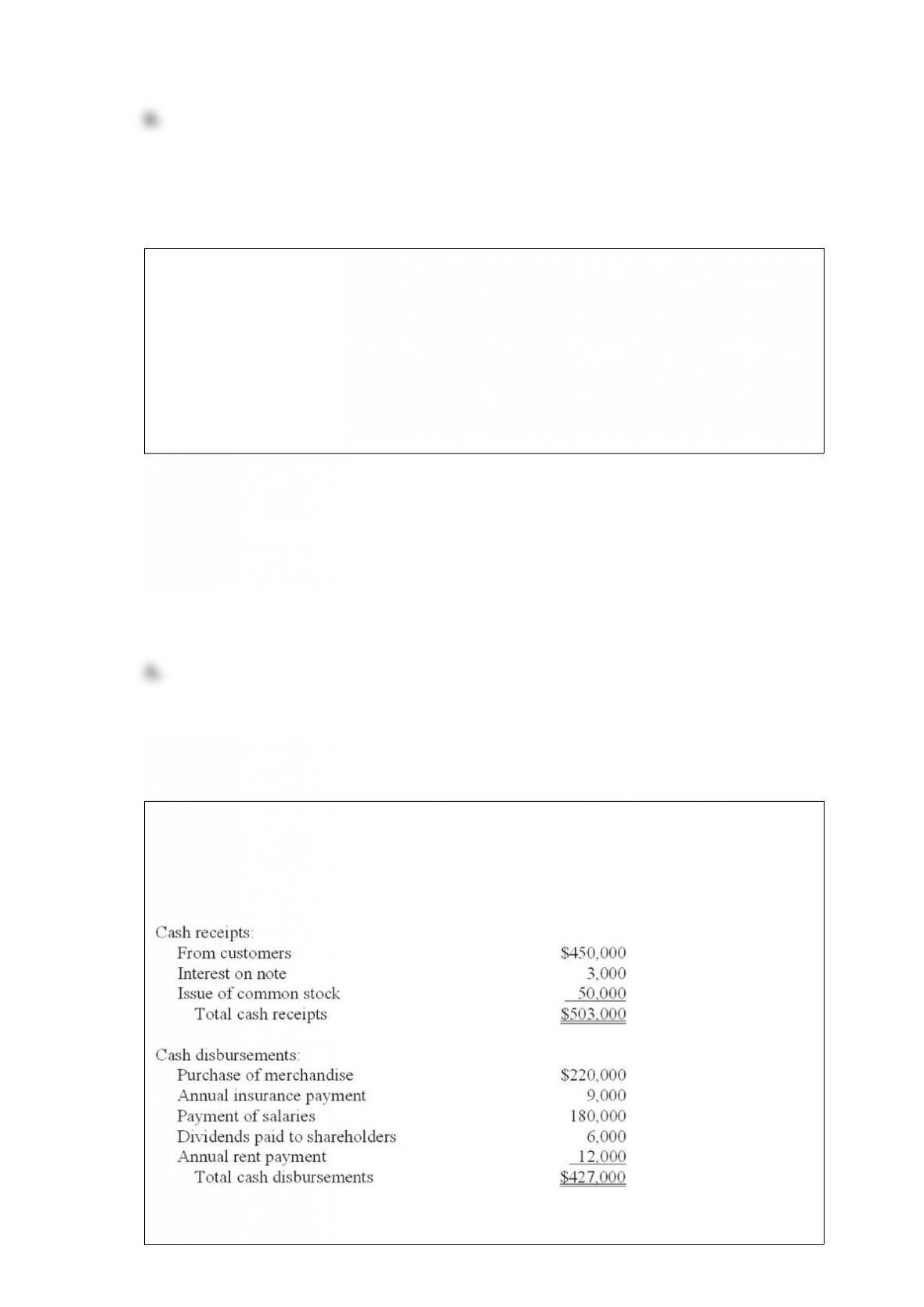

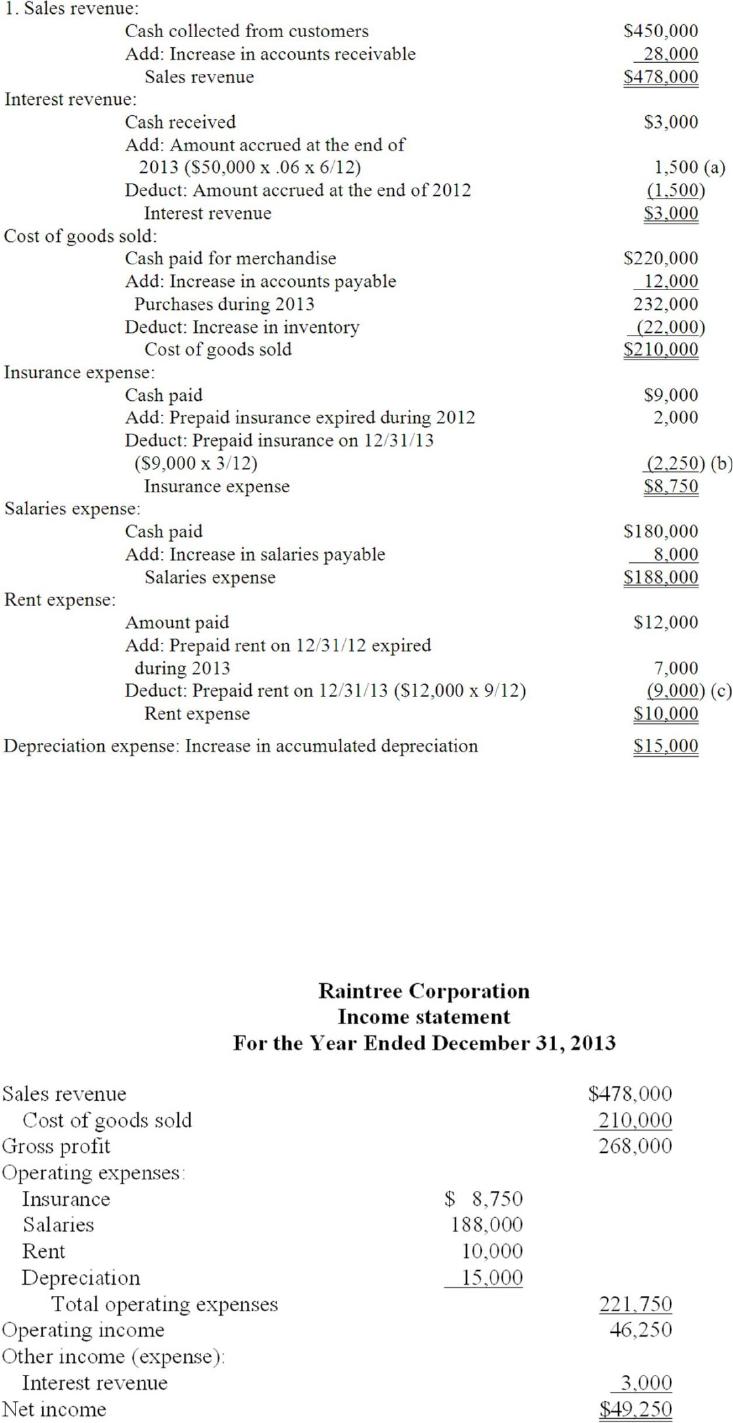

Raintree Corporation maintains its records on a cash basis. At the end of each year the

company’s accountant obtains the necessary information to prepare accrual basis

financial statements. The following cash flows occurred during the year ended

December 31, 2013:

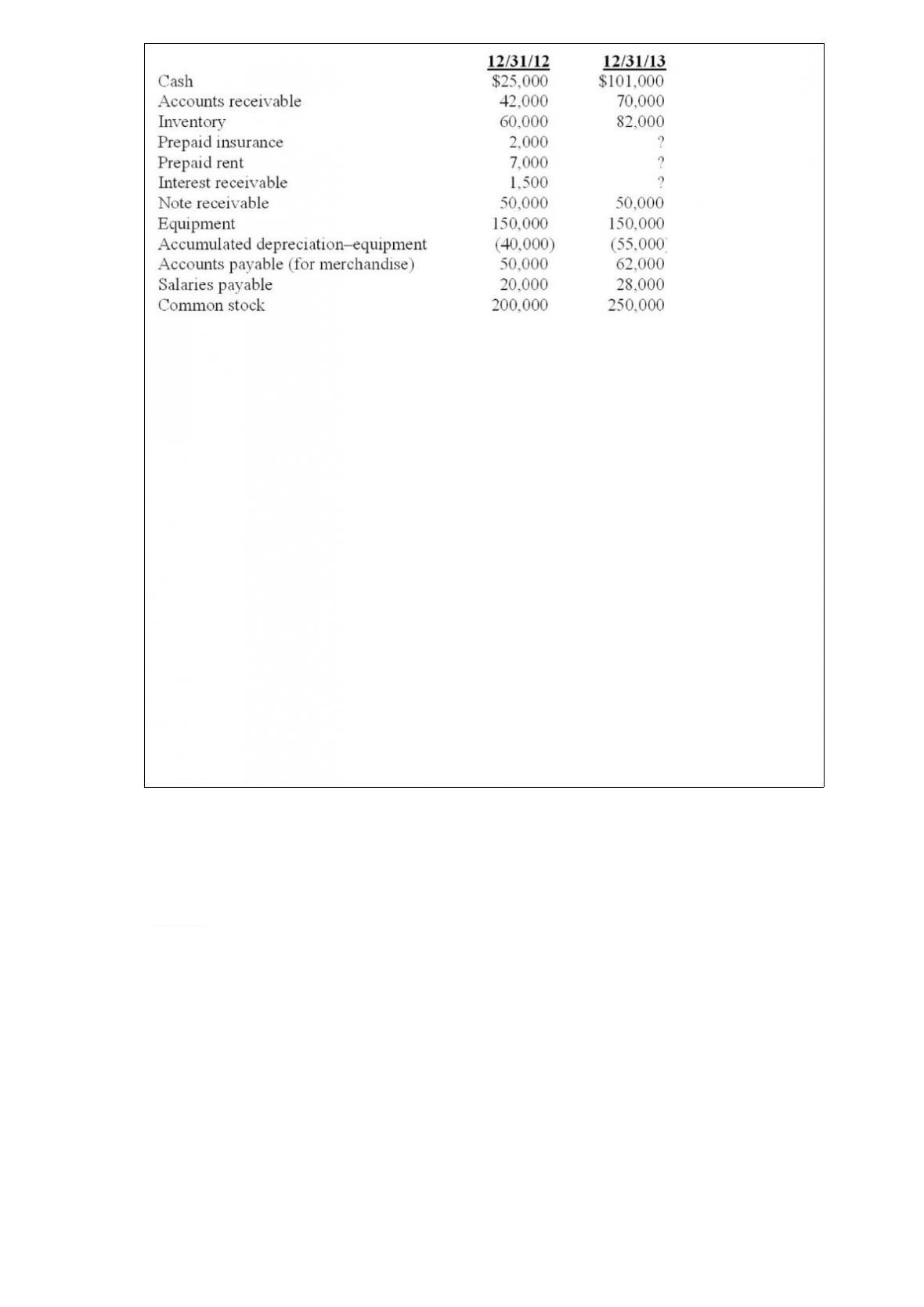

Selected balance sheet information:

Additional information:

1. On June 30, 2012, Raintree lent a customer $50,000. Interest at 6% is payable

annually on each June 30. Principal is due in 2016.

2. The annual insurance payment is made in advance on March 31.

3. Annual rent on the company’s facilities is paid in advance on September 30.

Required:

1. Prepare an accrual basis income statement for 2013 (ignore income taxes).

2. Determine the following balance sheet amounts on December 31, 2013:

a. Interest receivable

b. Prepaid insurance

c. Prepaid rent

Answer:

Accounting standard setting has been characterized as: A.A political process.

B.Using the scientific method.

C.Pure deductive reasoning.

D.Pure inductive reasoning.

Answer:

On January 1, 2013, an investor paid $291,000 for bonds with a face amount of

$300,000. The contract rate of interest is 8% while the current market rate of interest is

10%. Using the effective interest method, how much interest income is recognized by

the investor in 2014 (assume annual interest payments and amortization)? A. $23,280.

B. $25,140.

C. $29,100.

D. $29,610.

Answer:

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1)Deficit

2)Other assets

3)Investments

4)Acid-test ratio

5)Balance sheet

A. Also known as the quick ratio.

B. Assets not used directly in operations.

C. A discouraging retained earnings balance.

D. A catch-all classification.

E. An organized array of assets, liabilities and equity at a point in time.

Answer:

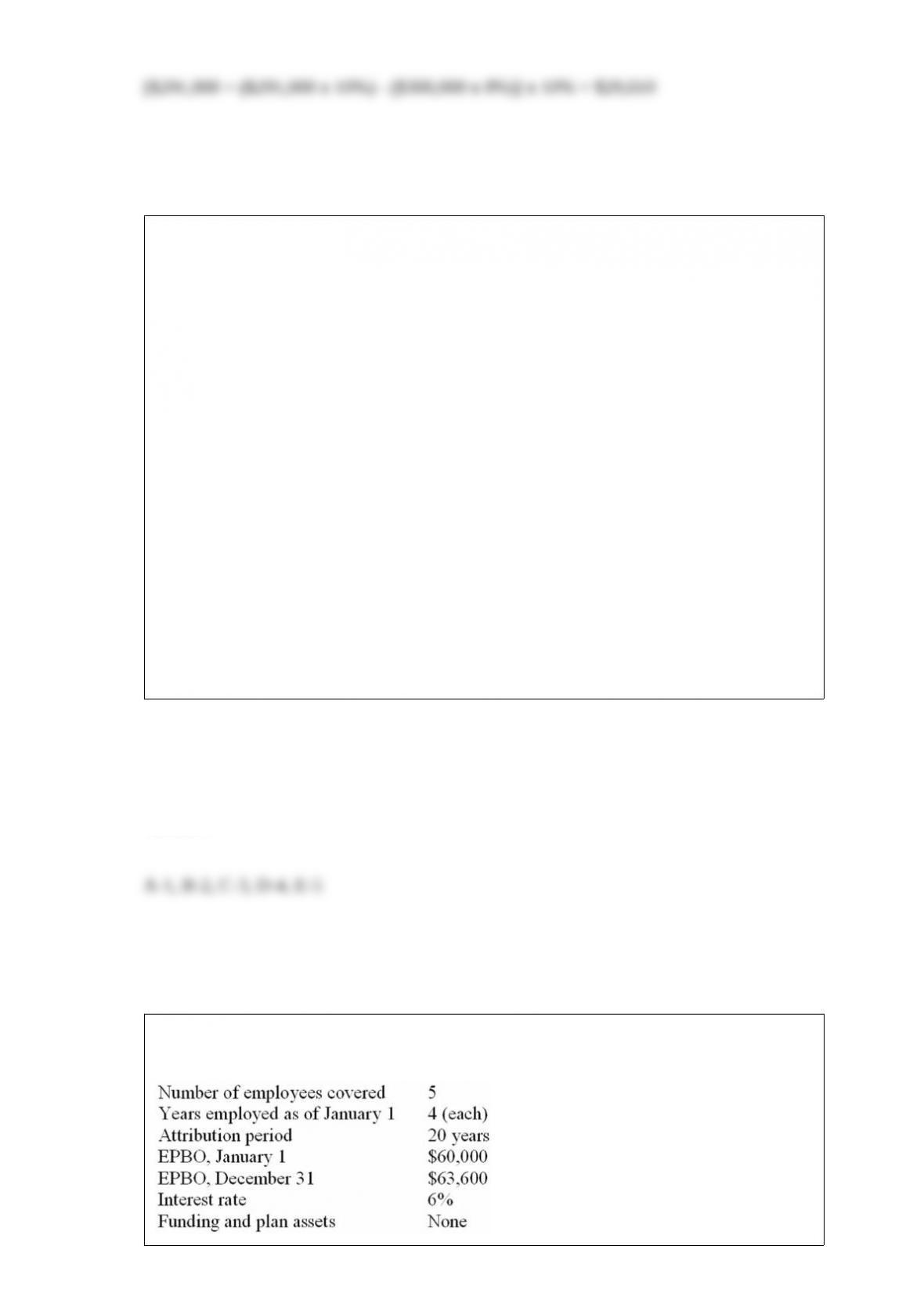

The following data are for Guava Company’s retiree health care plan for the current

calendar year.

What is the correct entry to record postretirement benefit expense for the current year?

A.

B.

C.

D.

Answer:

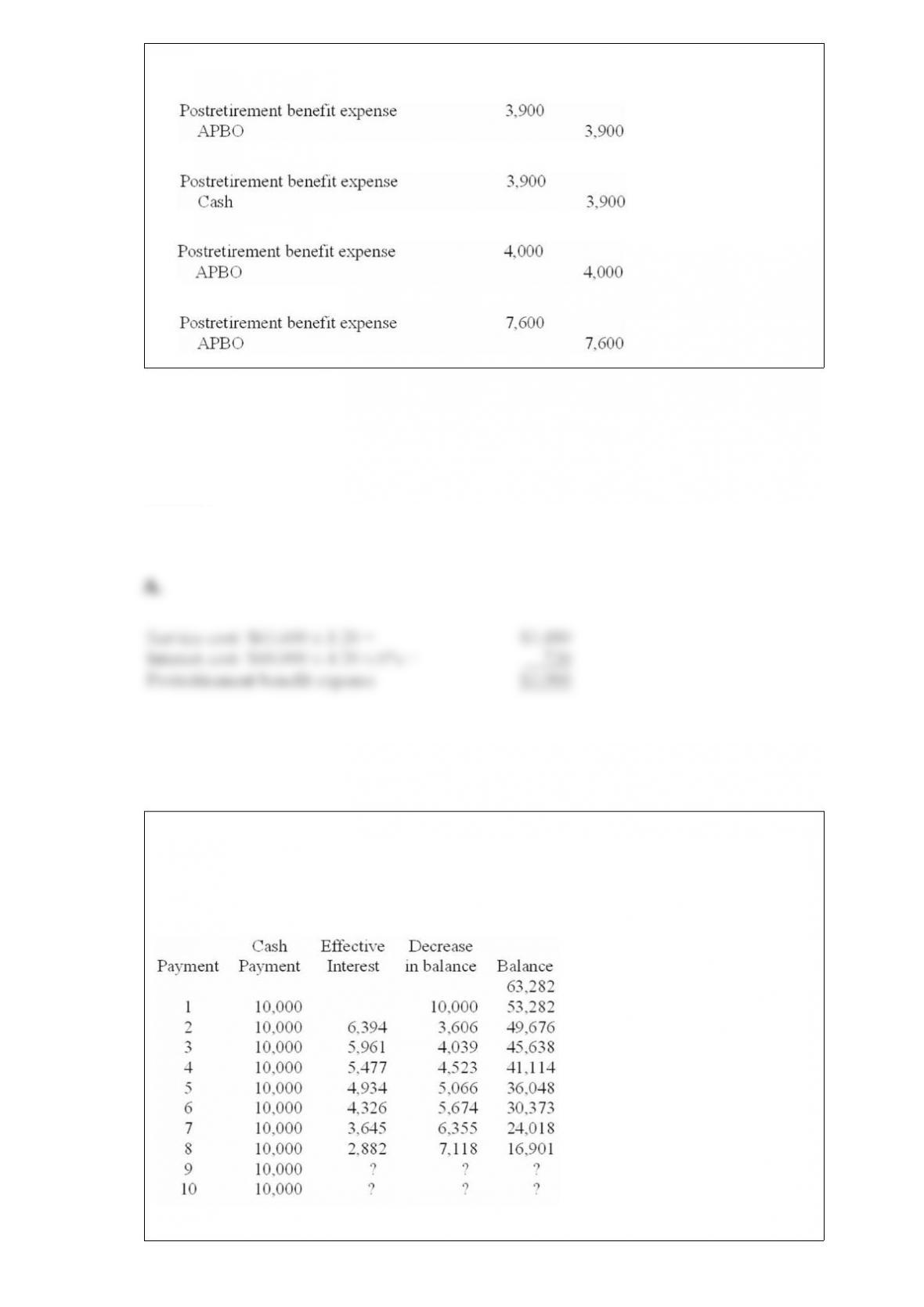

Refer to the following lease amortization schedule. The 10 payments are made annually

starting with the inception of the lease. Title does not transfer to the lessee and there is

no bargain purchase option or guaranteed residual value. The asset has an expected

economic life of 12 years. The lease is noncancelable.

What is the outstanding balance after payment 9? A. $8,929.

B. $13,463.

C. $5,000.

D. $5,537.

Answer:

Costs incurred by the lessor that are associated directly with originating a lease and are

essential to acquire that lease are called initial direct costs. Initial direct costs are

recorded as assets and amortized over the term of the lease in: A. An operating lease.

B. A capital lease.

C. A direct financing lease.

D. A sales-type lease.

Answer:

In deciding whether financing with receivables is a secured borrowing or a sale under

U.S. GAAP, the critical element is the extent to which:A. The transferee has received

substantially all the risks and rewards of ownership.

B. The age of the receivables transferred differs from the average age of the receivables.

C. The transferor of the receivable surrenders control over the assets transferred.

D. The transferee relies on funds from the transferor to maintain operations.

Answer:

Treasury shares are most often reported as: A. A reduction of total shareholders’ equity.

B. A reduction of total paid-in capital.

C. A reduction to retained earnings.

D. An expense on the income statement.

Answer:

The balance in retained earnings at the end of the year is determined by retained

earnings at the beginning of the year: A. Plus revenues, minus liabilities.

B. Plus accruals, minus deferrals.

C. Plus net income, minus dividends.

D. Plus assets, minus liabilities.

Answer:

Accounting for postretirement health care benefits is similar, in most respects, to

accounting for: A. Payroll taxes.

B. Health insurance costs for current employees.

C. Pension benefits.

D. Sick pay and vacation pay.

Answer:

In 2012, Antle Inc. had acquired Demski Co. and recorded goodwill of $245 million as

a result. The net assets (including goodwill) from Antle’s acquisition of Demski Co. had

a 2013 year-end book value of $580 million. Antle assessed the fair value of Demski at

this date to be $700 million, while the fair value of all of Demski’s identifiable tangible

and intangible assets (excluding goodwill) was $550 million. The amount of the

impairment loss that Antle would record for goodwill at the end of 2013 is: A. $150

million.

B. $95 million.

C. $0.

D. None of the above is correct.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term by placing the letter

designating the best term in the space provided by the phrase. 1) Discount rate

2) Interest expense

3) Deferred gain on sale-leaseback

4) Lessor’s gross investment

5) Depreciation on leased assets

A. Identified as the lower of implicit rate or lessee’s incremental borrowing rate.

B. Based on term of lease or useful life depending on lease contract

C. Classified as a contra asset account.

D. Calculated as effective rate times balance

E. Calculated as minimum lease payments plus unguaranteed residual value

Answer:

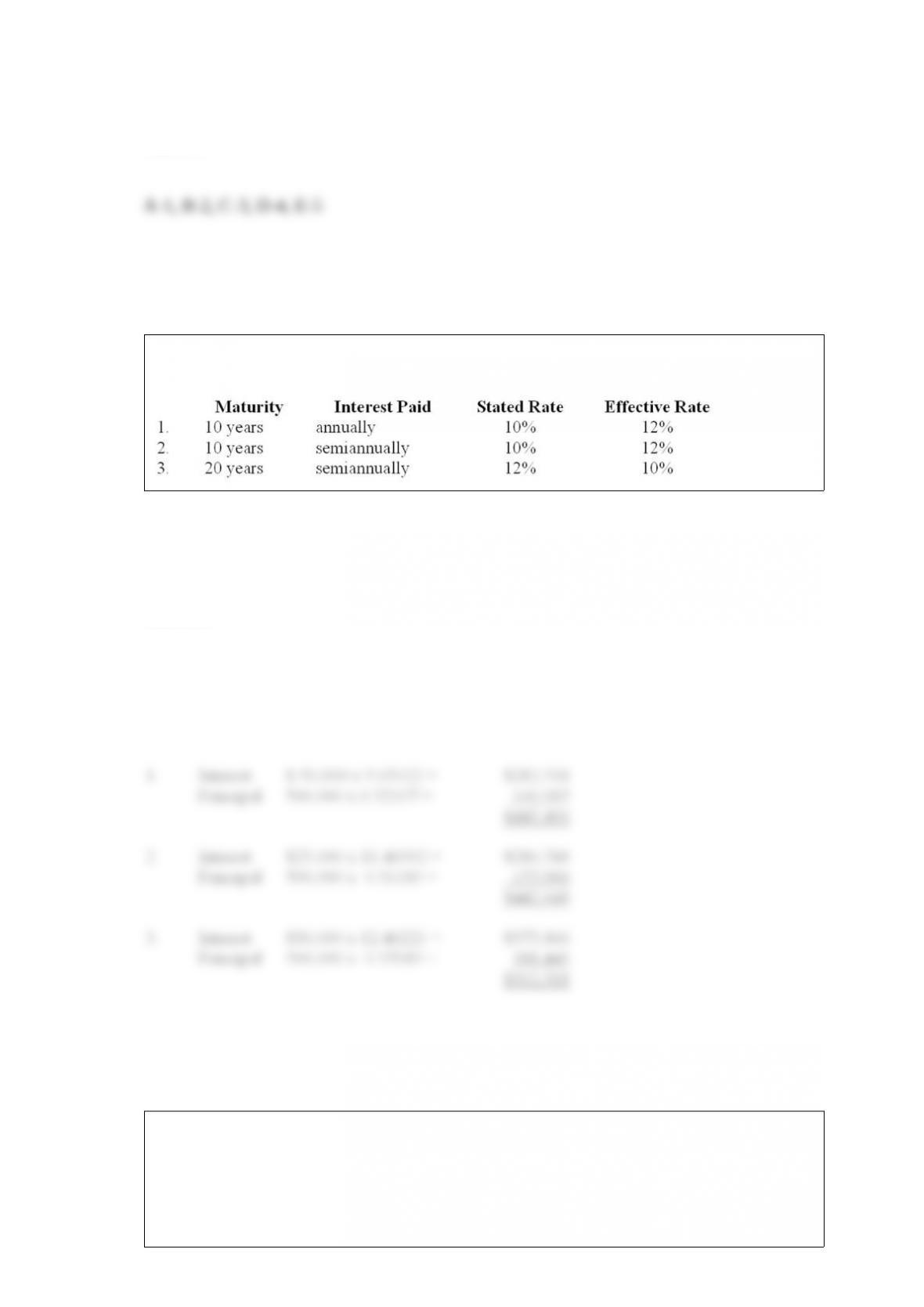

Determine the price of a $500,000 bond issue under each of the following independent

assumptions:

Answer:

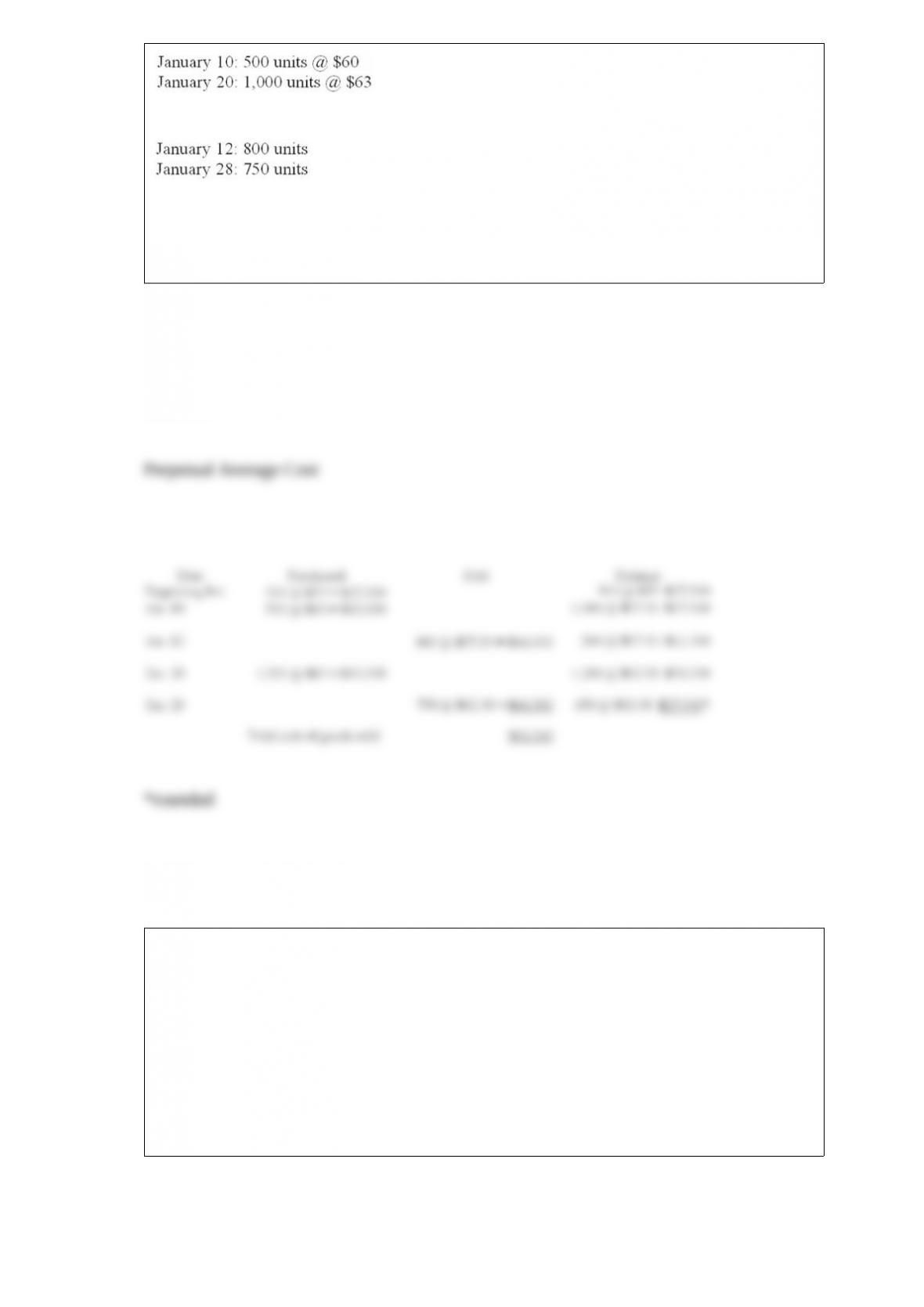

Shown below is activity for one of the products of Denver Office Equipment:

January 1 balance, 500 units @ $55 $27,500

Purchases:

Sales:

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming

Denver uses average cost and a perpetual inventory system.

Answer:

Stern Corporation borrowed $10 million cash on September 1, 2013, to provide

additional working capital for the year’s production. Stern issued a 6-month, 10%

promissory note to Second State Bank. Interest on the note is payable at maturity. Each

firm uses the calendar year as the fiscal year.

Required:

1) Prepare all journal entries from issuance to maturity for Stern Corporation.

2) Prepare all journal entries from issuance to maturity for Second State Bank.

Answer:

Describe what is meant by unearned revenues and give two examples.

Answer:

What activities are included in the statement of cash flows under the section titled

“Cash flows from investing activities”?

Answer:

Casper Chemical recently acquired a building located on two acres of land for a

lump-sum price of $3.2 million. In your job as assistant controller, you determined the

allocation of the price using the relative fair values to be $1 million and $2.2 million for

the land and building, respectively. When you reported these initial values to Jake

Reese, the company’s controller, he told you to change the allocation to $1.5 million for

the land and $1.7 million for the building. When you asked him why the change, he

explained that the company is having a difficult time meeting profitability goals and

that his proposed allocation will help the bottom line for future years.

Required:

1) How will the controller’s proposed allocation help the bottom line in future years?

2) Discuss the ethical dilemma faced by the assistant controller.

Answer:

Hamilton Security leased equipment to American Parcel Service for a 16-year period, at

which time possession of the leased asset will revert back to Hamilton. The equipment

cost Hamilton $16 million and has an expected useful life of 22 years. Its normal sales

price is $23 million. The present value of the minimum lease payments for both the

lessor and lessee is $20 million. The first payment was made at the inception of the

lease.

Required:

How would American Parcel Service classify this lease if it prepares its financial

statements using U.S. GAAP? IFRS? Why?

Answer:

KateCo leased a warehouse from Big Dave Industries on July 1, 2013. The present

value of the lease payments discounted at 10% was $160,000. Ten annual lease

payments of $24,000 are due at the beginning of each fiscal year beginning July 1,

2013. Big Dave had constructed the equipment recently for $132,000 and its retail fair

value was $200,000.

Required:

Following the guidance of the new ASU, prepare the two journal entries to record the

lease by Big Dave at its commencement.

Answer:

In early December of 2013, Blue Corp. purchased $40,000 of Yellow Company

common stock, which constitutes less than 3% of Yellow’s outstanding shares. Blue

accounts for the Yellow investment as available for sale. By December 31, 2013, the

value of the Yellow investment had fallen to $30,000, and Blue recorded an unrealized

loss. By December 31, 2014, the value of the Yellow investment had fallen to $15,000,

and Blue determined that it can no longer assert that it has both the intent and ability to

hold the shares long enough for their fair value to recover, so Blue recorded an OTT

impairment. By December 31, 2015, fair value had recovered to $20,000.

Prepare appropriate entry(s) at December 31, 2014, and indicate how the scenario will

affect net income, OCI, and comprehensive income.

Answer:

How does GAAP define fair value?

Answer:

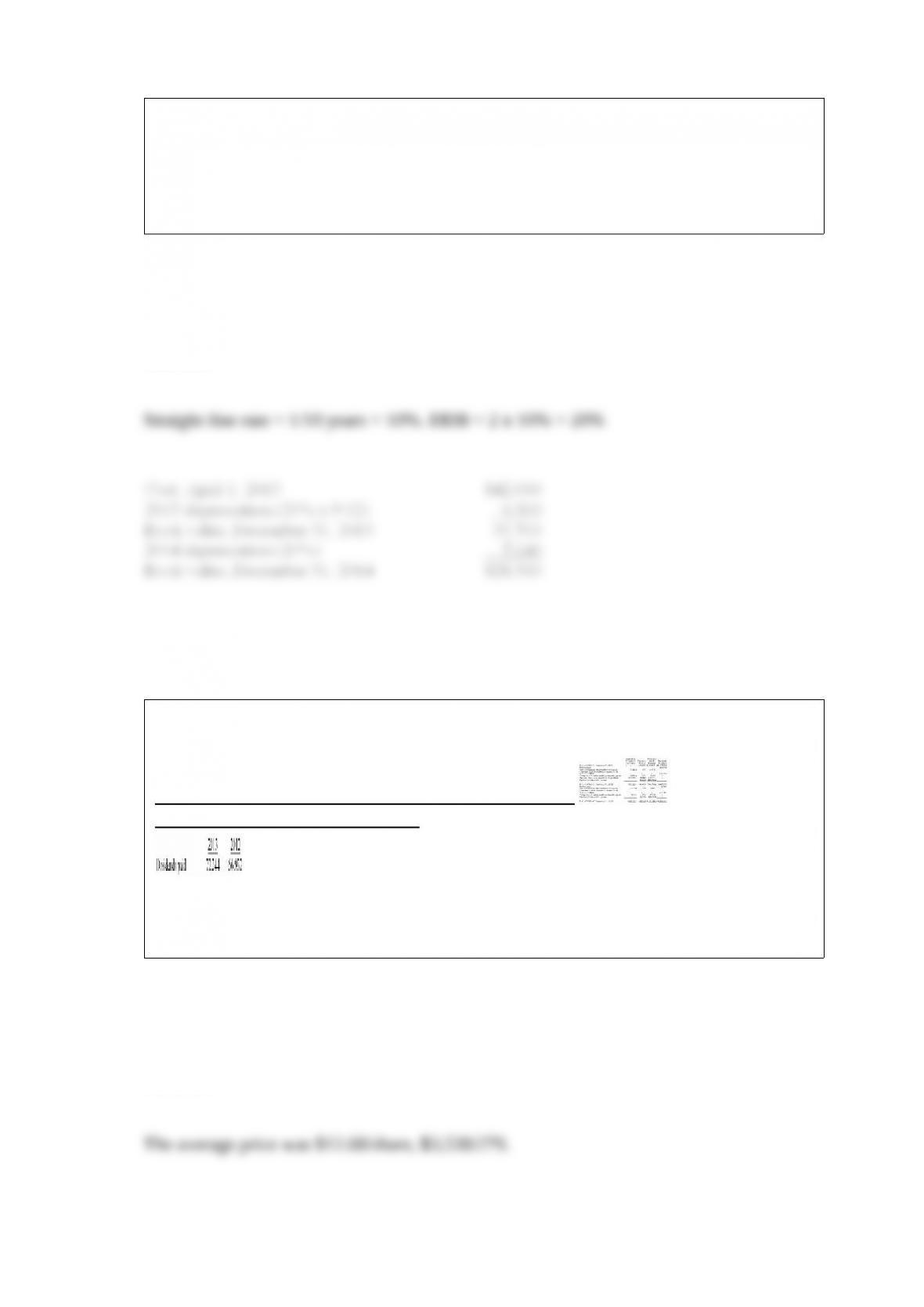

On April 1, 2013, Parks Co. purchased machinery at a cost of $42,000. The machinery

is expected to last 10 years and to have a residual value of $6,000.

Required: Compute depreciation for 2013 and 2014 and the book value of the

machinery at December 31, 2013 and 2014, assuming double-declining balance method

is used.

Answer:

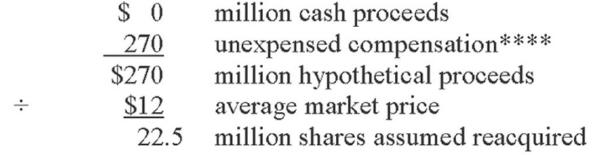

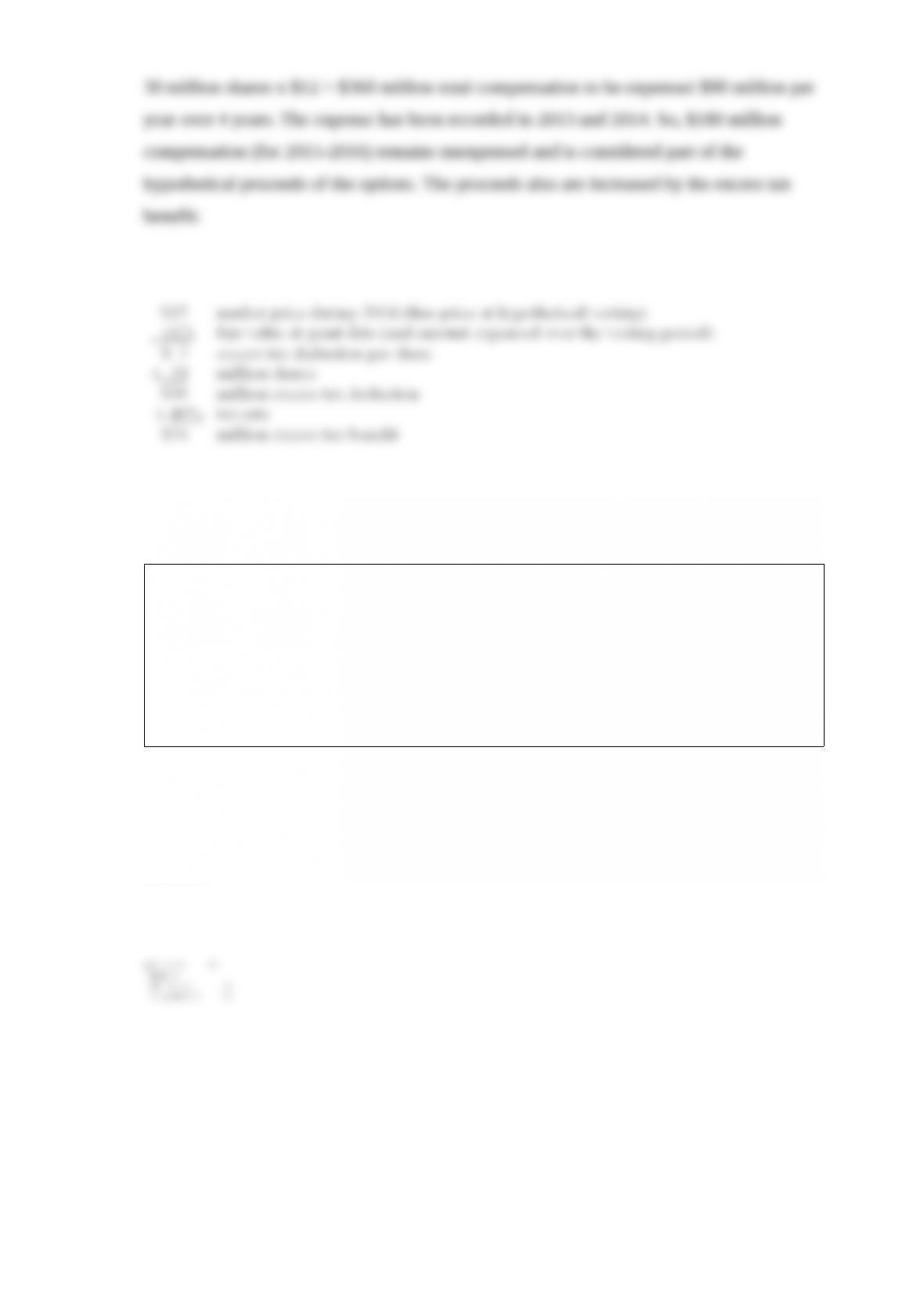

The following information comes from the 2013 Annual Report to stockholders of

Composition Inc. (in thousands):

From the Statement of Changes in Stockholders’ Equity:

From the Statement of Cash Flows: In Cash flows from financing activities:

What was the average exercise price per share of stock issued under option plans in

2013?

Answer:

On September 5, 2013, Howard Corporation signed a purchase commitment to purchase

inventory for $130,000 on or before March 31, 2014. The company’s fiscal year-end is

December 31. The contract was exercised on March 4, 2014, and the inventory was

purchased for cash at the contract price. On the purchase date of March 4, the market

price of the inventory was $116,000. The market price of the inventory on December

31, 2013, was $120,000. The company uses a perpetual inventory system.

Required:

1) Prepare the necessary adjusting journal entry (if any is required) on December 31,

2013.

2) Prepare the journal to record the purchase on March 4, 2014.

Answer:

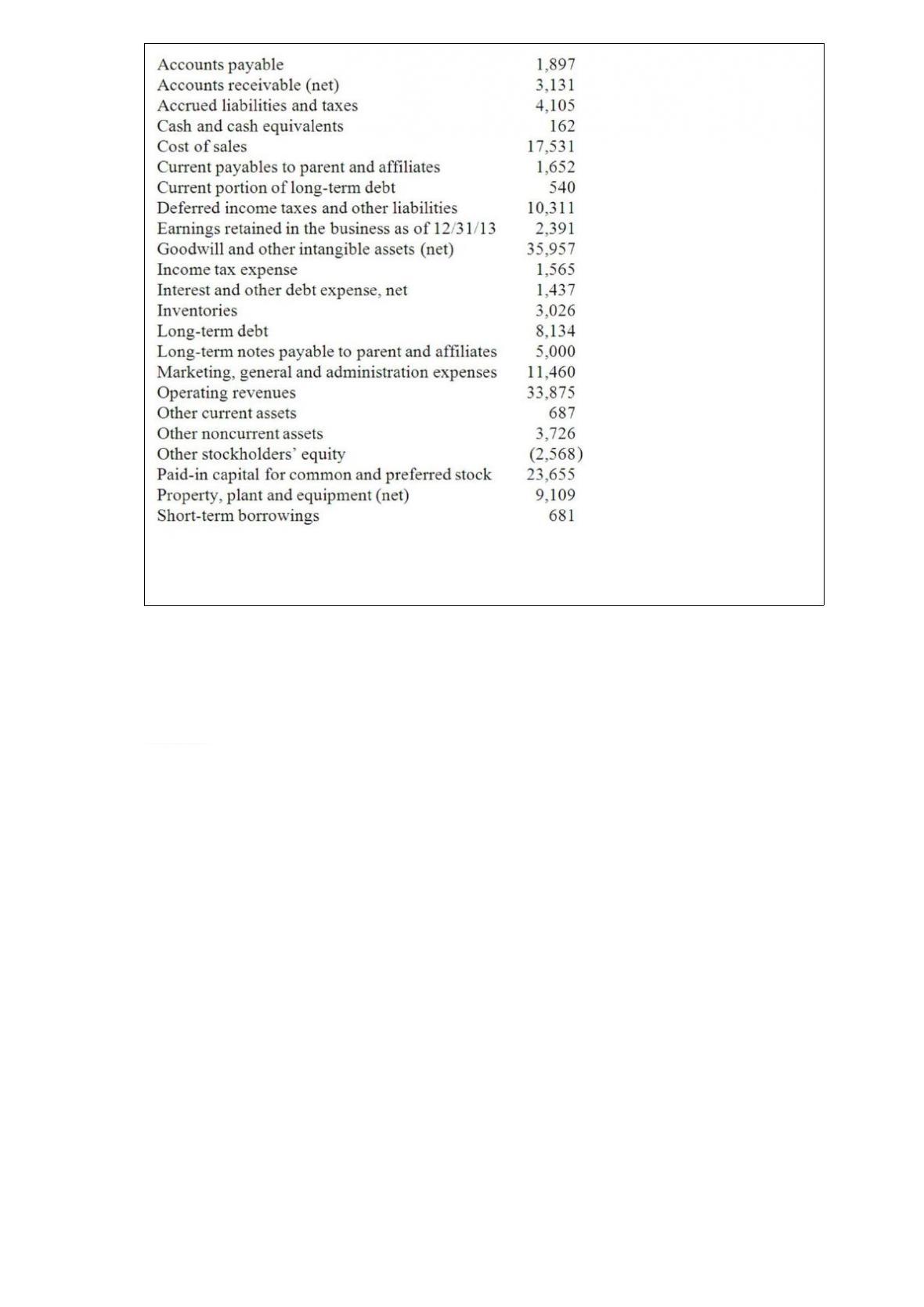

The following information, based on the 12/31/13 Annual Report to Shareholders of

Krafty Foods ($ in millions):

Based on the information presented above, prepare the 12/31/13 Balance Sheet for

Krafty Foods.

Answer:

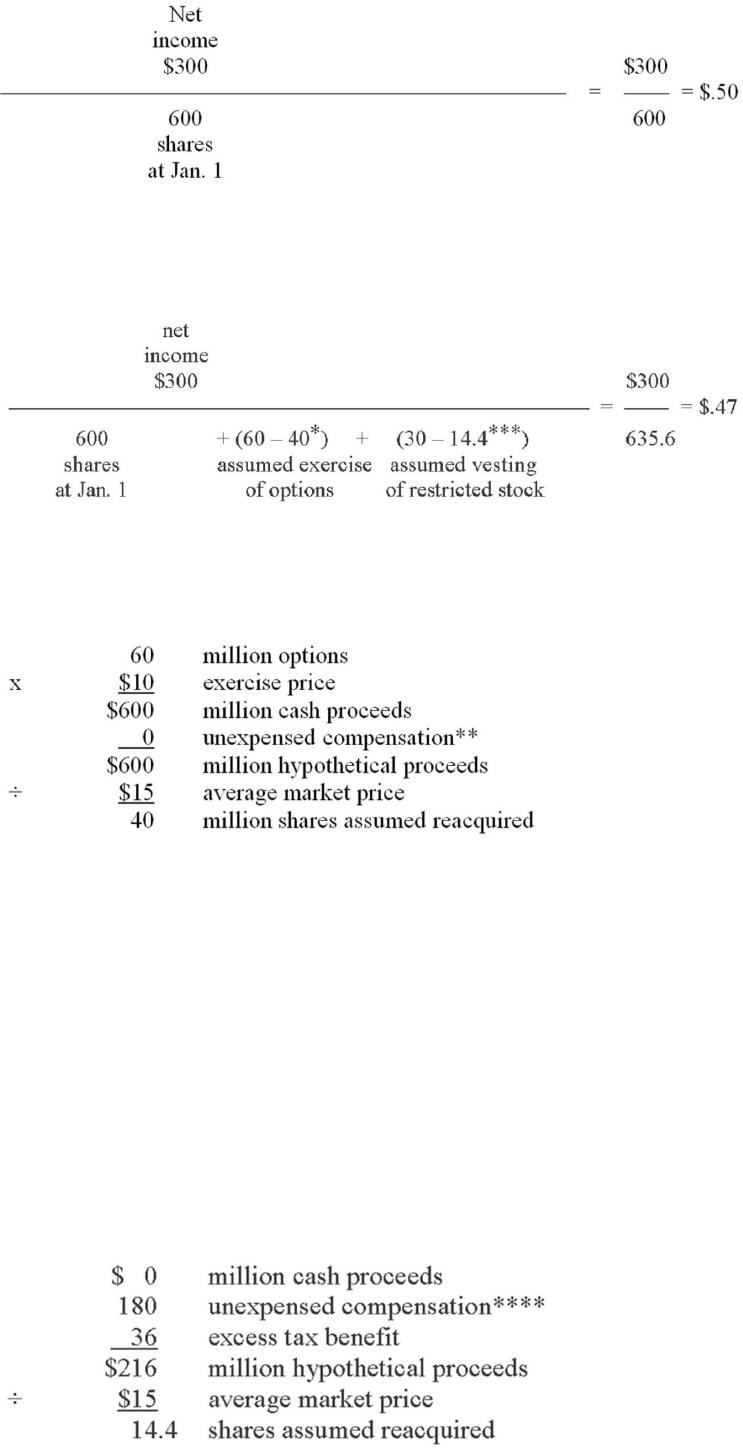

JD Co. is a calendar-year firm with 600 million common shares outstanding throughout

2013 and 2014. As part of its executive compensation plan, at January 1, 2012, the

company had issued 60 million executive stock options permitting executives to buy 60

million shares of stock for $10 per share within the next eight years, but not prior to

January 1, 2015. The fair value of the options was estimated on the grant date to be $3

per option.

In 2013, JD began granting employees stock awards rather than stock options as part of

its equity compensation plans and granted 30 million restricted common shares to

senior executives at January 1, The shares vest four years later. The fair value of the

stock was $12 per share on the grant date. The average market price of the common

shares was $12 and $15 during 2013 and 2014, respectively.

The stock options qualify for tax purposes as an incentive plan. The restricted stock

does not. The company’s net income was $240 million and $300 million in 2013 and

2014, respectively. Its income tax rate is 40%.

Required:

1) Determine basic and diluted earnings per share (rounded to 2 decimal places) for JD

in 2013.

2) Determine basic and diluted earnings per share for JD (rounded to 2 decimal places)

in 2014.

Answer:

Roberts Corp. reports pretax accounting income of $200,000, but due to a single

temporary difference, taxable income is only $150,000. At the beginning of the year, no

temporary differences existed. Roberts is subject to a tax rate of 40%.

Required:

Prepare the compound journal entry to record Roberts Corp.’s income taxes. Show

well-labeled computations.

Answer: