1) An inverted yield curve predicts that short-term interest rates

A) are expected to rise in the future

B) will rise and then fall in the future

C) will remain unchanged in the future

D) will fall in the future

2) At the beginning of 2011, Parling Food Services acquired a 90% interest in Simmons’

Orchards when Simmons’ book values of identifiable net assets equaled their fair

values. On December 26, 2011, Simmons declared dividends of $50,000, and the

dividends were unpaid at year-end. Parling had not recorded the dividend receivable at

December 31 . A consolidated working paper entry is necessary to

A) enter $50,000 dividends receivable in the consolidated balance sheet

B) enter $45,000 dividends receivable in the consolidated balance sheet

C) reduce the dividends payable account by $45,000 in the consolidated balance sheet

D) eliminate the dividend payable account from the consolidated balance sheet

3) If the probability of a bond default increases because corporations begin to suffer

large losses, then the default risk on corporate bonds will ________ and the expected

return on these bonds will ________, everything else held constant

A) decrease; increase

B) decrease; decrease

C) increase; increase

D) increase; decrease

4) What is the threshold for reporting a major customer?

A) 5 percent of revenues

B) 5 percent of profits

C) 10 percent of revenues

D) 10 percent of profits

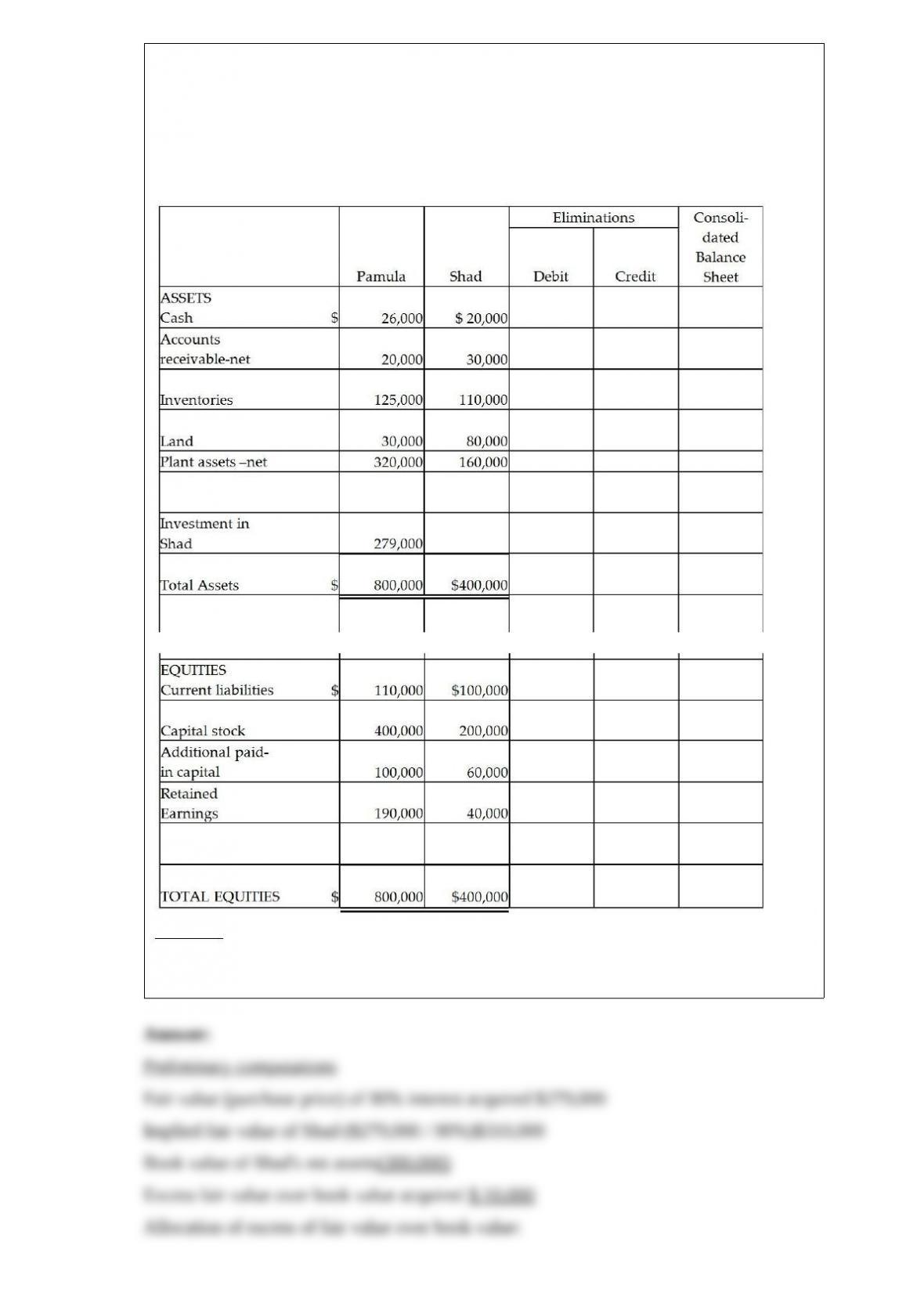

5) Pamula Corporation paid $279,000 for 90% of Shad Corporation’s $10 par common

stock on December 31, 2011, when Shad Corporation’s stockholders’ equity was made

up of $200,000 of Common Stock, $60,000 Additional Paid-in Capital and $40,000 of

Retained Earnings. Shad’s identifiable assets and liabilities reflected their fair values on

December 31, 2011, except for Shad’s inventory which was undervalued by $5,000 and

their land which was undervalued by $2,000. Balance sheets for Pamula and Shad

immediately after the business combination are presented in the partially completed

working papers.

Required:

Complete the consolidated balance sheet working papers for Pamula Corporation and

Subsidiary.

6) Drawings

A) are advances to a partnership

B) are loans to a partnership

C) are a function of interest on partnership average capital

D) are the same nature as withdrawals

7) When short-term interest rates are expected to fall sharply in the future, the yield

curve will

A) slope up

B) be flat

C) be inverted

D) be an inverted U shape

8) In reference to the determination of goodwill impairment, which of the following

statements is correct?

A) The goodwill impairment test under FASB 142 is a three-step process

B) If the reporting unit’s fair value exceeds its carrying value, goodwill is unimpaired

C) Under FASB 142, firms must first compare carrying values (book values) at the firm

level

D) All of the above are correct

9) A summary balance sheet for the Lemon, Mango, and Nobb partnership appears

below. Lemon, Mango, and Nobb share profits and losses in a ratio of 2:3:5,

respectively.

Assets

Cash$ 100,000

Marketable securities200,000

Inventory125,000

Land100,000

Building-net500,000

Total assets$1,025,000

Equities

Lemon, capital$ 425,000

Mango, capital400,000

Nobb, capital200,000

Total equities$1,025,000

The partners agree to admit Oran for a one-fifth interest. The fair market value of

partnership land is appraised at $200,000 and the fair market value of inventory is

$175,000. The assets are to be revalued prior to the admission of Oran and there is

$30,000 of goodwill that attaches to the old partnership.

How much cash must Oran invest to acquire a one-fifth interest?

A) $235,000

B) $141,000

C) $293,750

D) $301,250

10) The following are transactions for the city of Springfield.

a.Borrowed $20,000 by issuing a three-month, 5% note.

b.Paid $4,000 for equipment.

c.Services for $1,000 were billed and collected.

d.Year-end accrual of 3 months interest on note in (a).

Required:

Analyze the above transactions by using the accounting equation for a proprietary fund.

11) The duties of a debtor in possession in a Chapter 11 bankruptcy case do not include

A) filing a list of creditors and schedules of assets and liabilities with the bankruptcy

court

B) operating the business during the reorganization period

C) filing a reorganization plan

D) issuing an order of relief

12) Creditor committees are elected

A) in all bankruptcy cases

B) in Chapter 7 cases

C) only in bankruptcy cases arising from involuntary petitions

D) in Chapter 11 cases

13) Entities other than the primary beneficiary account for their investment in a variable

interest entity using the

A) cost method

B) equity method

C) cost or equity methods

D) consolidated method

14) Pretax operating incomes of Pang Corporation and its 70%-owned subsidiary, Sala

Corporation, for the year 2011, are shown below. Sala pays total dividends of $60,000

for the year. There are no unamortized book value/fair value differentials relating to

Pang’s investment in Sala. During the year, Pang sold land to Sala for a gain of $35,000

and Sala holds this land at the end of the year. The marginal corporate tax rate for both

corporations is 34%.

PangSala

Sales revenue$900,000$600,000

Gain on sale of land35,000

Cost of sales(480,000)(325,000)

Other expenses(192,000)(78,000)

Pretax operating income (does not include investment income)$263,000$197,000

Required:

1> Determine the separate amounts of income tax expense for Pang and Sala as if they

had filed separate tax returns.

2> Determine Pang’s net income from Sala.

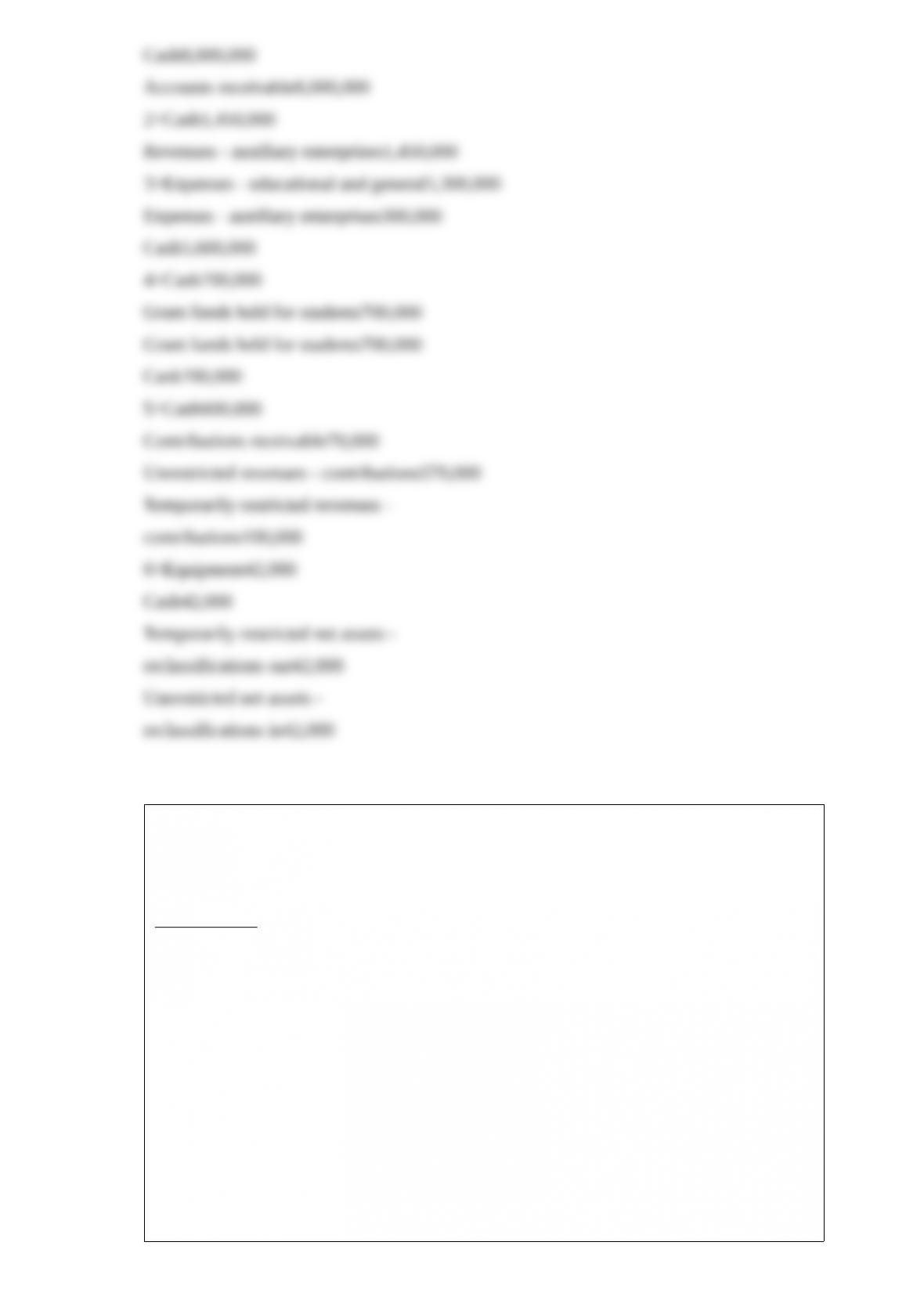

15) Prepare journal entries to record the following transactions for a private,

not-for-profit university.

1>Tuition and fees assessed total $10,000,000, 80% of which was collected by

year-end; tuition scholarships were granted for $1,300,000, and $650,000 was expected

to be uncollectible.

2>Revenues collected from sales and services by the university bookstore were

$1,450,000.

3>Salaries and wages paid were $5,600,000, $300,000 of which was for employees of

the university bookstore.

4>Financial aid funds of $700,000 were received from the Pell Grant program; the

funds were then disbursed to the appropriate students.

5>Contributions of $600,000 were received; $30,000 was restricted for the athletic

department and the balance was unrestricted. An additional $70,000 was pledged to the

athletic department by the alumni.

6>Athletic equipment was purchased with $42,000 previously set aside for that

purpose.

16) Eve, Fig, Gus, and Hal are partners who share profits and losses 50%, 25%, 15%,

and 10%, respectively. The partnership will be liquidated gradually over several months

beginning January 1, 2011 . The partnership trial balance at December 31, 2010 is as

follows:

DebitsCredits

Cash$9,000

Accounts receivable26,000

Inventory78,000

Loan to Eve16,000

Furniture27,000

Equipment59,000

Goodwill10,000

Accounts payable$23,000

Note payable70,000

Loan from Hal7,000

Eve, capital (50%)46,000

Fig, capital (25%)38,000

Gus, capital (15%)15,000

Hal, capital (10%)26,000

Totals$225,000$225,000

Required:

Prepare a cash distribution plan for January 1, 2011, showing how cash installments

will be distributed among the partners as it becomes available. Prepare vulnerability

rankings for the partners and a schedule of assumed loss absorption.

17) Pandy Corporation owns a 90% interest in Sakaj Corporation’s common stock.

Throughout 2010, Sakaj had 20,000 shares of common stock outstanding and Pandy

had 50,000 shares of common stock outstanding. Sakaj’s only dilutive security consists

of 10,000 stock options, with an exercise price of $20 per share. The average price of

Sakaj’s stock is $50 per share in 2010 . The options are exercisable for one share of

Sakaj’s common stock. Pandy’s and Sakaj’s separate net incomes for the year are

$200,000 and $180,000, respectively.

Required:

Compute the amount of basic and diluted earnings per share for Pandy (Consolidated)

and Sakaj Corporations.

18) The Trasque Hospital is a nongovernmental, not-for-profit hospital. During 2011,

they had the following transactions.

1>Trasque’s standard charges for services rendered amounted to $550,000. Contractual

adjustments on those amounts with third-party payors amounted to $230,000. Bad debts

on the remaining balance are estimated to be 10%.

2>The hospital received a cash donation of $20,000 to be used for medical equipment.

3>The hospital also received rent from a local shelter that uses the basement of their

facility for overflow housing, amounting to $6,000 per year.

4>The hospital paid the following costs: Professional fees (doctors and physician

assistants), $80,000; Nursing services, $70,000; and administrative services, $40,000.

5>The hospital paid for pharmaceuticals and medical supplies amounting to $110,000.

The hospital had an agreement with the pharmaceutical and medical supply vendors to

carry all inventory on consignment, due to their not-for-profit status. As a result, items

are only paid for as consumed, and all inventory belongs to the vendors.

Required:

Prepare the journal entries for Trasque for 2011 .

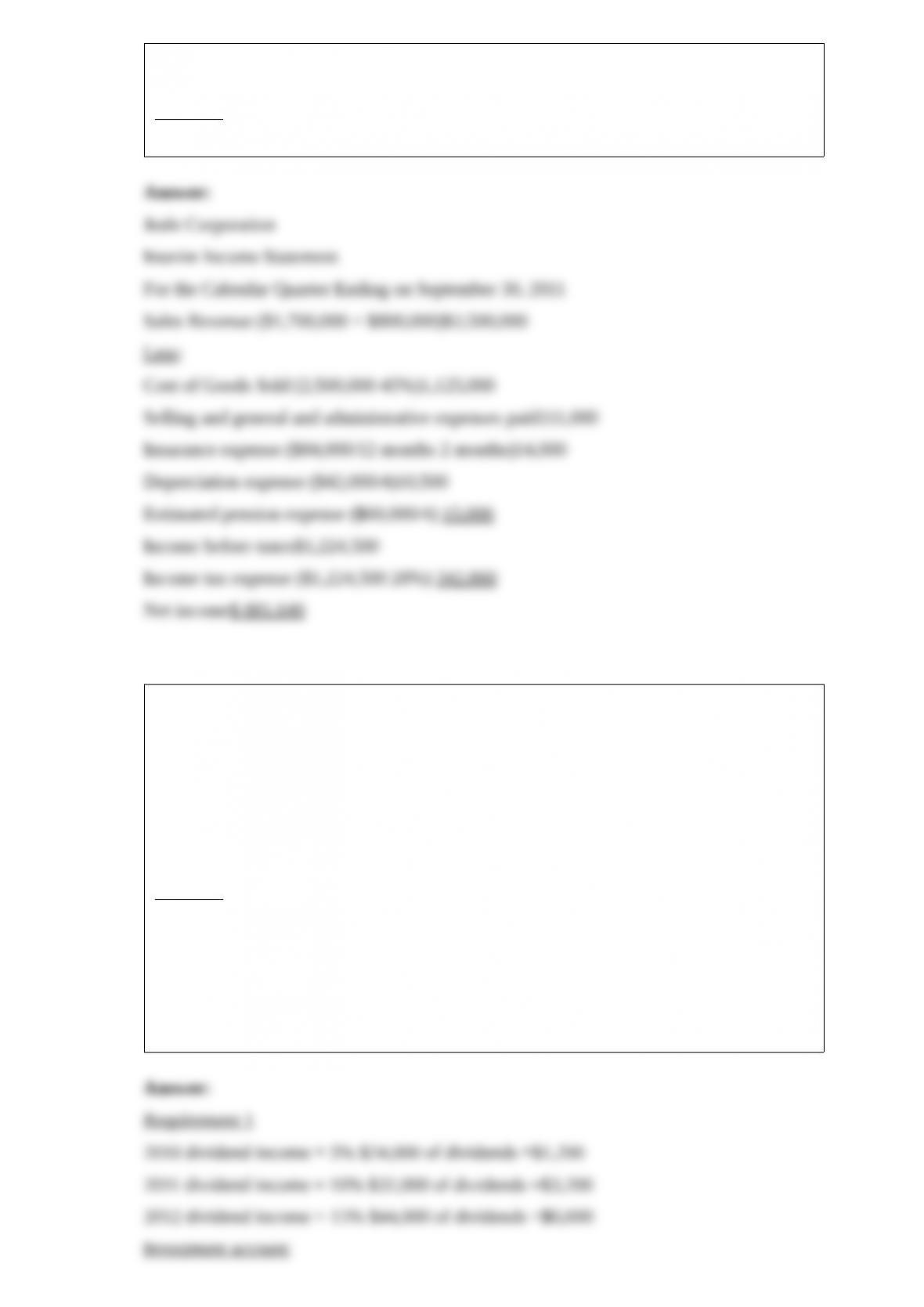

19) Jeale Corporation is preparing its interim financial statements for the third quarter

of calendar 2011 . The following information was provided for the preparation of the

statements:

1>Credit sales for the quarter$1,700,000

2>Cash sales for the quarter800,000

3>Inventories, July 1 (FIFO cost method)250,000

4>Cash purchases of inventory during the quarter400,000

5>Inventory purchases made on account for the quarter650,000

6>Estimated cost of goods sold ratio45%

7>Selling and general administrative expenses paid111,000

8>Effective corporate tax rate28%

9>Loss on sale of securities sold on June 30, 201175,000

10>Annual insurance premiums paid on August 1(the84,000

anniversary date of the policy) (Last year’s insurance expense is

included in general administrative expenses.)

Additional information:

At the end of the year, Jeale accrues its annual pension and depreciation expenses which

amount to $60,000 and $42,000, respectively.

Required:

Prepare Jeale’s interim income statement for the third quarter of calendar 2011 .

20) For 2010, 2011, and 2012, Squid Corporation earned net incomes of $40,000,

$70,000, and $100,000, respectively, and paid dividends of $24,000, $32,000, and

$44,000, respectively. On January 1, 2010, Squid had $500,000 of $10 par value

common stock outstanding and $100,000 of retained earnings.

On January 1 of each of these years, Albatross Corporation bought 5% of the

outstanding common stock of Squid paying $37,000 per 5% block on January 1, 2010,

2011, and 2012 . All payments made by Albatross in excess of book value were

attributable to equipment, which is depreciated over five years on a straight-line basis.

Required:

1>Assuming that Albatross uses the cost method of accounting for its investment in

Squid, how much dividend income will Albatross recognize for each of the three years

and what will be the balance in the investment account at the end of each year?

2>Assuming that Albatross has significant influence and uses the equity method of

accounting (even though its ownership percentage is less than 20%), how much net

investee income will Albatross recognize for each of the three years?

21) Prey Corporation created a wholly owned subsidiary, Sage Corporation, on January

1, 2010, at which time Prey sold land with a book value of $90,000 to Sage at its fair

market value of $140,000. Also, on January 1, 2010, Prey sold to Sage equipment with

a book value of $130,000 and a selling price of $165,000. The equipment had a

remaining useful life of 4 years and is being depreciated under the straight-line method.

The equipment has no salvage value. On January 1, 2012, Sage resold the land to an

outside entity for $150,000. Sage continues to use the equipment purchased from Prey.

Income statements for Prey and Sage for the year ended December 31, 2012 are

summarized below:

Prey Sage

Sales$450,000 $100,000

Gain on sale of land10,000

Cost of sales(220,000)(50,000)

Depreciation expense(95,000)(32,000)

Other expenses(37,000)(8,000)

Net income$98,000 $20,000

Required:

At what amounts did the following items appear on the consolidated income statement

for Prey and Subsidiary for the year ended December 31, 2012?

1>Gain on Sale of Land

2>Depreciation Expense

3>Consolidated net income

4>Controlling interest share of consolidated net income