1) Because IFRS is very general in its provisions for lease accounting, the required

disclosures for leases under IFRS are more detailed and extensive than those required

under U.S. GAAP.

2) Under IFRS, both the investor and the investee should follow the same accounting

practices, requiring adjustments be made to the investors books in order to prepare

financial information.

3) Under IFRS an affirmative judgment approach is used for recognizing deferred tax

assets up to the amount that is probable to be realized.

4) When the conventional retail method includes both net markups and net markdowns

in the cost-to-retail ratio, it approximates a lower-of-cost-or-market valuation.

5) Under both U.S. GAAP and IFRS, the calculation of basic and diluted earnings per

share is identical.

6) A zero-interest-bearing note payable that is issued at a discount will not result in any

interest expense being recognized.

7) When an ordinary repair occurs, several periods will usually benefit.

8) In a period of rising prices, the inventory method which tends to give the highest

reported cost of goods sold is

a.FIFO

b.average cost

c.LIFO

d.None of these choices are correct

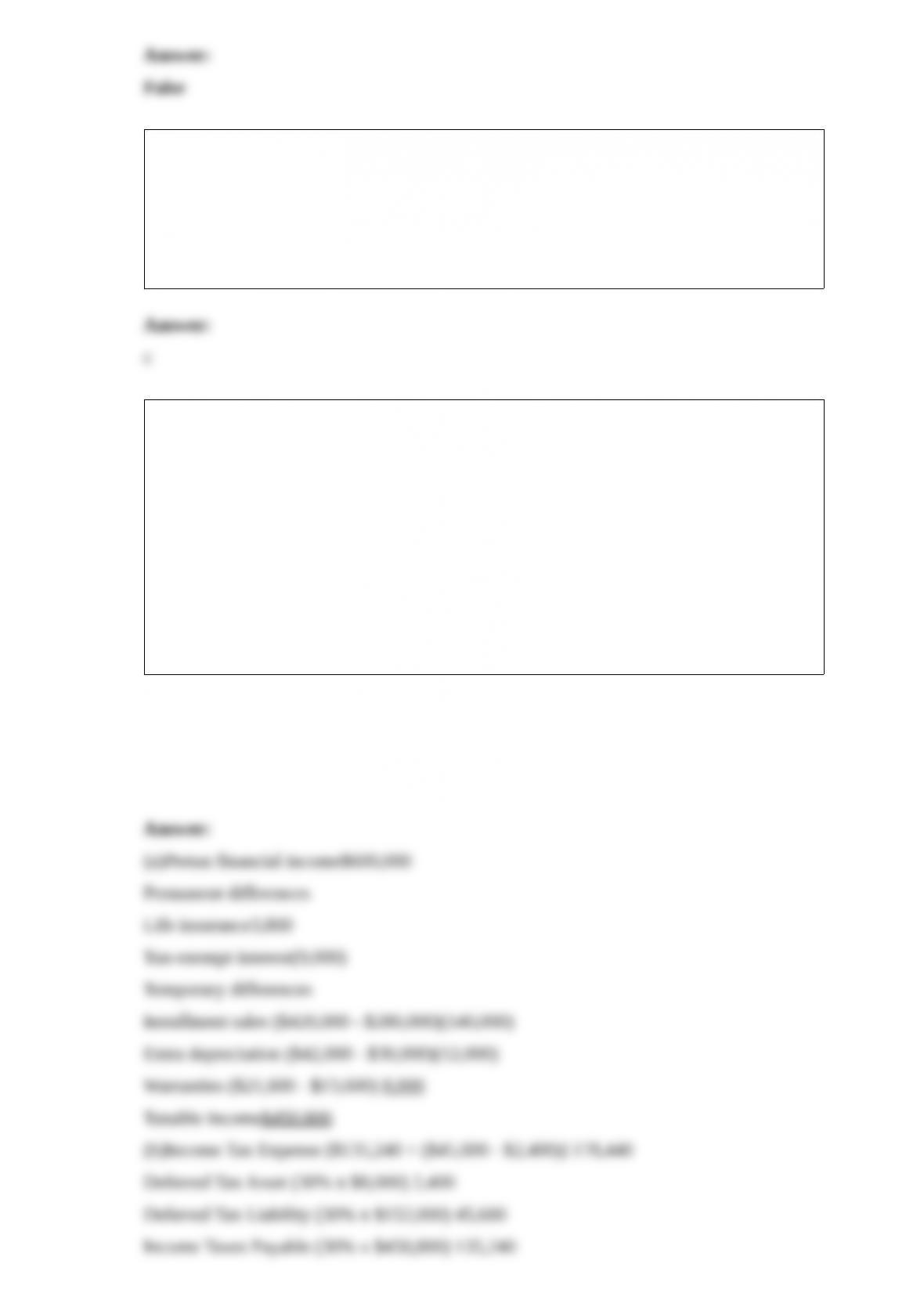

9) The records for Bosch Co. show this data for 2015:

Gross profit on installment sales recorded on the books was $420,000. Gross profit

from collections of installment receivables was $280,000.

Life insurance on officers was $3,800.

Machinery was acquired in January for $300,000. Straight-line depreciation over a

ten-year life (no salvage value) is used. For tax purposes, MACRS depreciation is used

and Bosch may deduct 14% for 2015 .

Interest received on tax exempt Iowa State bonds was $9,000.

The estimated warranty liability related to 2015 sales was $21,600. Repair costs under

warranties during 2015 were $13,600. The remainder will be incurred in 2016 .

Pretax financial income is $600,000. The tax rate is 30%.

Instructions

(a)Prepare a schedule starting with pretax financial income and compute taxable income.

(b)Prepare the journal entry to record income taxes for 2015 .

10) Riley Co. incurred the following costs during 2015:

Significant modification to the formulation of a chemical product$160,000

Trouble-shooting in connection with breakdowns during commercial

production150,000

Cost of exploration of new formulas200,000

Seasonal or other periodic design changes to existing products185,000

Laboratory research aimed at discovery of new technology325,000

In its income statement for the year ended December 31, 2015, Riley should report

research and development expense of

a.$685,000

b.$835,000

c.$870,000

d.$1,020,000

11) June Corp. sells one product and uses a perpetual inventory system. The beginning

inventory consisted of 40 units that cost $20 per unit. During the current month, the

company purchased 240 units at $20 each. Sales during the month totaled 180 units for

$43 each. What is the cost of goods sold using the LIFO method?

a.$ 800

b.$3,600

c.$4,800

d.$7,740

12) The accounting equation must remain in balance

a.throughout each step in the accounting cycle

b.only when journal entries are recorded

c.only at the time the trial balance is prepared

d.only when formal financial statements are prepared

13) Which of the following is not a major characteristic of a plant asset?

a.Possesses physical substance

b.Acquired for resale

c.Acquired for use

d.Yields services over a number of years

14) Which of the following is included in inventory costs?

a.Product costs

b.Period costs

c.Product and period costs

d.Neither product or period costs

15) Fina Corp. had the following transactions during the quarter ended March 31, 2015:

Loss from hurricane damage$420,000

Payment of fire insurance premium for calendar year 2015700,000

What amount should be included in Fina’s income statement for the quarter ended

March 31, 2015?

Extraordinary LossInsurance Expense

a.$420,000$700,000

b.$420,000$175,000

c.$105,000$175,000

d.$0$700,000

16) A reclassification adjustment is reported in the

a.income statement as an Other revenue or expense

b.stockholders equity section of the balance sheet

c.statement of comprehensive income as other comprehensive income

d.statement of stockholders equity

17) On June 30, 2015, Cey, Inc. exchanged 6,000 shares of Seely Corp. $30 par value

common stock for a patent owned by Gore Co. The Seely stock was acquired in 2015 at

a cost of $165,000. At the exchange date, Seely common stock had a fair value of $46

per share, and the patent had a net carrying value of $330,000 on Gore’s books. Cey

should record the patent at

a.$165,000

b.$180,000

c.$276,000

d.$330,000

18) When calculating the cost ratio for the retail inventory method,

a.if it is the conventional method, the beginning inventory is included and markdowns

are deducted

b.if it is the LIFO method, the beginning inventory is excluded and markdowns are

deducted

c.if it is the LIFO method, the beginning inventory is included and markdowns are not

deducted

d.if it is the conventional method, the beginning inventory is excluded and markdowns

are not deducted

19) Which of the following is false?

a.The future value of a deferred annuity is the same as the future value of an annuity not

deferred

b.A deferred annuity is an annuity in which the rents begin after a specified number of

periods

c.To compute the present value of a deferred annuity, we compute the present value of

an ordinary annuity of 1 for the entire period and subtract the present value of the rents

which were not received during the deferral period

d.If the first rent is received at the end of the sixth period, it means the ordinary annuity

is deferred for six periods

20) Which of the following features of preferred stock makes it more like a debt than an

equity instrument?

a.Participating

b.Voting

c.Redeemable

d.Noncumulative

21) The original sale of the $50 par value common shares of Gray Company was

recorded as follows:

Cash290,000

Common Stock250,000

Paid-in Capital in Excess of Par40,000

Instructions

Record the treasury stock transactions (given below) under the cost method:

Transactions:

(a)Bought 400 shares of common stock as treasury shares at $62.

(b)Sold 120 shares of treasury stock at $60.

(c)Sold 60 treasury shares at $68.

22) The accounting for cash discounts and trade discounts are

a.the same

b.always recorded net

c.not the same

d.tied to the timing of cash collections on the account

23) Which group of items listed below should be included in the cash account?

a.Silver coins, postage stamps, demand deposits, personal checks

b.Promissory notes, demand deposits, money orders, silver coins

c.Money orders, postdated checks, personal checks, time deposits

d.Silver coins, money orders, demand deposits, personal checks

24) Potter Variety Store uses the LIFO retail inventory method. Information relating to

the computation of the inventory at December 31, 2014, follows:

Cost Retail

Inventory, January 1, 2014$146,000$220,000

Purchases480,000700,000

Freight-in80,000

Sales770,000

Net markups160,000

Net markdowns60,000

Instructions

Assuming that there was no change in the price index during the year, compute the

inventory at December 31, 2014, using the LIFO retail inventory method.

25) Indicate which of the following securities would be included in the computation of

“basic earnings per share,” and which would be included in the computation of “diluted

earnings per share.” Place a “B” before those which affect only basic EPS, a “D” before

those which affect only diluted EPS, a “BD” before those which affect both basic and

diluted EPS, and an “N” before those securities which do not affect EPS computations.

Assume that, where applicable, the appropriate securities are dilutive.

1> Warrants to purchase additional common shares.

2> Common stock.

3> Nonconvertible debenture bonds.

4> Convertible, noncumulative preferred stock.

5> Cumulative, nonconvertible preferred stock.

6> Convertible bonds.

7> Executive stock options.

8> Notes payable.

26) Early in 2014, Dobbs Corporation engaged Kiner, Inc. to design and construct a

complete modernization of Dobbs’s manufacturing facility. Construction was begun on

June 1, 2014 and was completed on December 31, 2014 . Dobbs made the following

payments to Kiner, Inc. during 2014:

Date Payment

June 1, 2014$6,000,000

August 31, 20149,000,000

December 31, 20147,500,000

In order to help finance the construction, Dobbs issued the following during 2014:

1>$5,000,000 of 10-year, 9% bonds payable, issued at par on May 31, 2014, with

interest payable annually on May 31 .

2>1,000,000 shares of no-par common stock, issued at $10 per share on October 1,

2014 .

In addition to the 9% bonds payable, the only debt outstanding during 2014 was a

$1,250,000, 12% note payable dated January 1, 2010 and due January 1, 2020, with

interest payable annually on January 1 .

Instructions

Compute the amounts of each of the following (show computations):

1>Weighted-average accumulated expenditures qualifying for capitalization of interest

cost.

2>Avoidable interest incurred during 2014 .

3>Total amount of interest cost to be capitalized during 2014 .

27) Snow Co. began operations on January 2, 2014 . It employs 15 people who work

8-hour days. Each employee earns 10 paid vacation days annually. Vacation days may

be taken after January 10 of the year following the year in which they are earned. The

average hourly wage rate was $20.00 in 2014 and $21.25 in 2015 . The average

vacation days used by each employee in 2015 was 9 . Snow Co. accrues the cost of

compensated absences at rates of pay in effect when earned.

Instructions

Prepare journal entries to record the transactions related to paid vacation days during

2014 and 2015 .

28) LF Corporation, a manufacturer of Mexican foods, contracted in 2014 to purchase

1,500 pounds of a spice mixture at $5.00 per pound, delivery to be made in spring of

2015 . By 12/31/14, the price per pound of the spice mixture had dropped to $4.70 per

pound. In 2014, LF should recognize

aa loss of $7,500

b.a loss of $450

c.no gain or loss

d.a gain of $450

29) Briefly describe some of the differences between U.S. GAAP and IFRS with respect

to the accounting for long-term liabilities.

30) Explain the procedures used to account for a direct-financing lease.

31) The records for Todd Inc. showed the following for 2014:

Jan. 1 Dec. 31

Accrued expenses$1,300$2,150

Prepaid expenses720870

Cash paid during the year for expenses, $42,500

Show the computation of the amount of expense that should be reported on the income

statement.