1) The prime cost for September was:

A) $114,000

B) $100,000

C) $103,000

D) $47,000

2) Shelby Boat Wash’s cost formula for its cleaning equipment and supplies is $2,200

per month plus $34 per boat. For the month of September, the company planned for

activity of 82 boats, but the actual level of activity was 32 boats. The actual cleaning

equipment and supplies for the month was $3,340.

The spending variance for cleaning equipment and supplies in September would be

closest to:

A.$1,648 F

B.$1,648 U

C.$52 F

D.$52 U

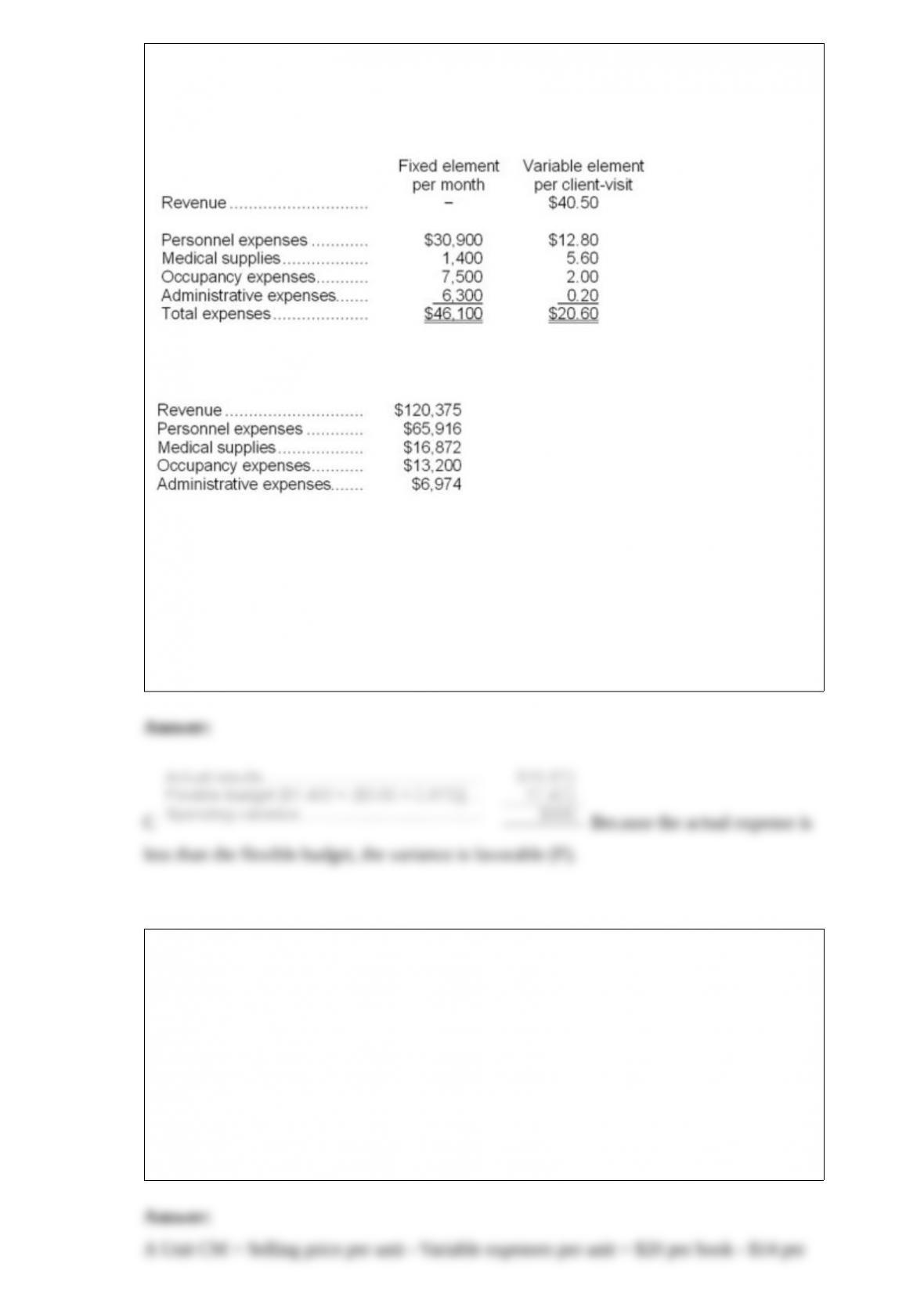

3) Wesolick Clinic uses client-visits as its measure of activity. During August, the clinic

budgeted for 2,900 client-visits, but its actual level of activity was 2,870 client-visits.

The clinic has provided the following data concerning the formulas used in its

budgeting and its actual results for August:

Data used in budgeting:

Actual results for August:

The spending variance for medical supplies in August would be closest to:

A.$768 U

B.$768 F

C.$600 F

D.$600 U

4) Darwin Inc. sells a particular textbook for $20. Variable expenses are $14 per book.

At the current volume of 50,000 books sold per year the company is just breaking even.

Given these data, the annual fixed expenses associated with the textbook total:

A.$300,000

B.$1,000,000

C.$1,300,000

D.$700,000

5) The debits to the Work in Process account as a consequence of the raw materials

transactions in August total:

A.$56,000

B.$0

C.$63,000

D.$69,000

6) Which product makes the MOST profitable use of the grinding machines?

A.Product A

B.Product B

C.Product C

D.Product D

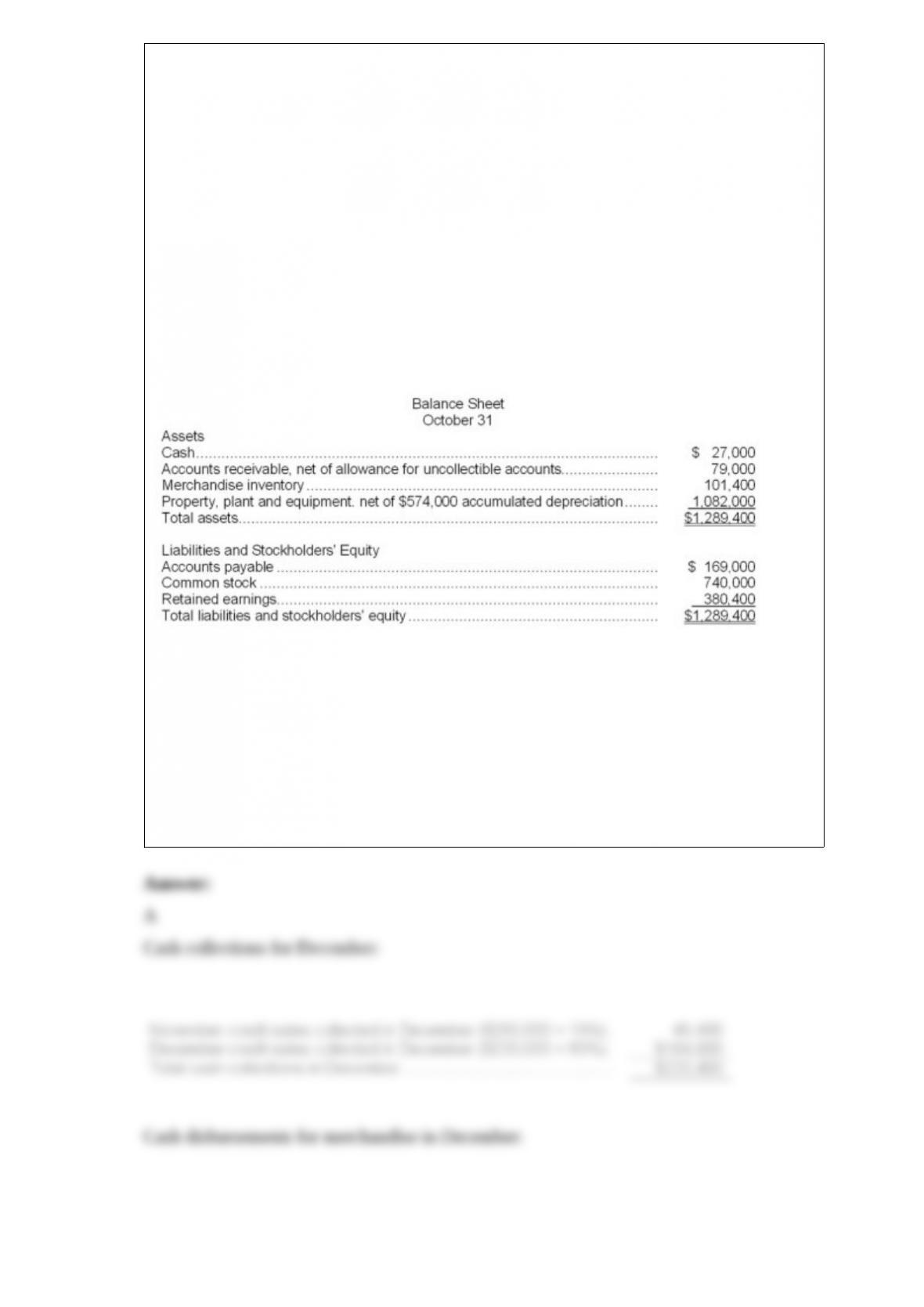

7) Dilbert Farm Supply is located in a small town in the rural west. Data regarding the

store’s operations follow:

Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000

for January.

Collections are expected to be 80% in the month of sale, 19% in the month following

the sale, and 1% uncollectible.

The cost of goods sold is 65% of sales.

The company desires to have an ending merchandise inventory at the end of each

month equal to 60% of the next month’s cost of goods sold. Payment for merchandise is

made in the month following the purchase.

Other monthly expenses to be paid in cash are $20,300.

Monthly depreciation is $20,000.

Ignore taxes.

The difference between cash receipts and cash disbursements for December would be:

A.$55,800

B.$37,900

C.$93,700

D.$17,900

8) During the most recent month at Luinstra Corporation, queue time was 4.5 days,

inspection time was 0.8 day, process time was 1.9 days, wait time was 5.1 days, and

move time was 0.7 day.

Required:

a. Compute the throughput time.

b. Compute the manufacturing cycle efficiency (MCE).

c. What percentage of the production time is spent in non-value-added activities?

d. Compute the delivery cycle time.

9) The total cash flow net of income taxes in year 2 is:

A.$60,000

B.$69,000

C.$43,000

D.$90,000

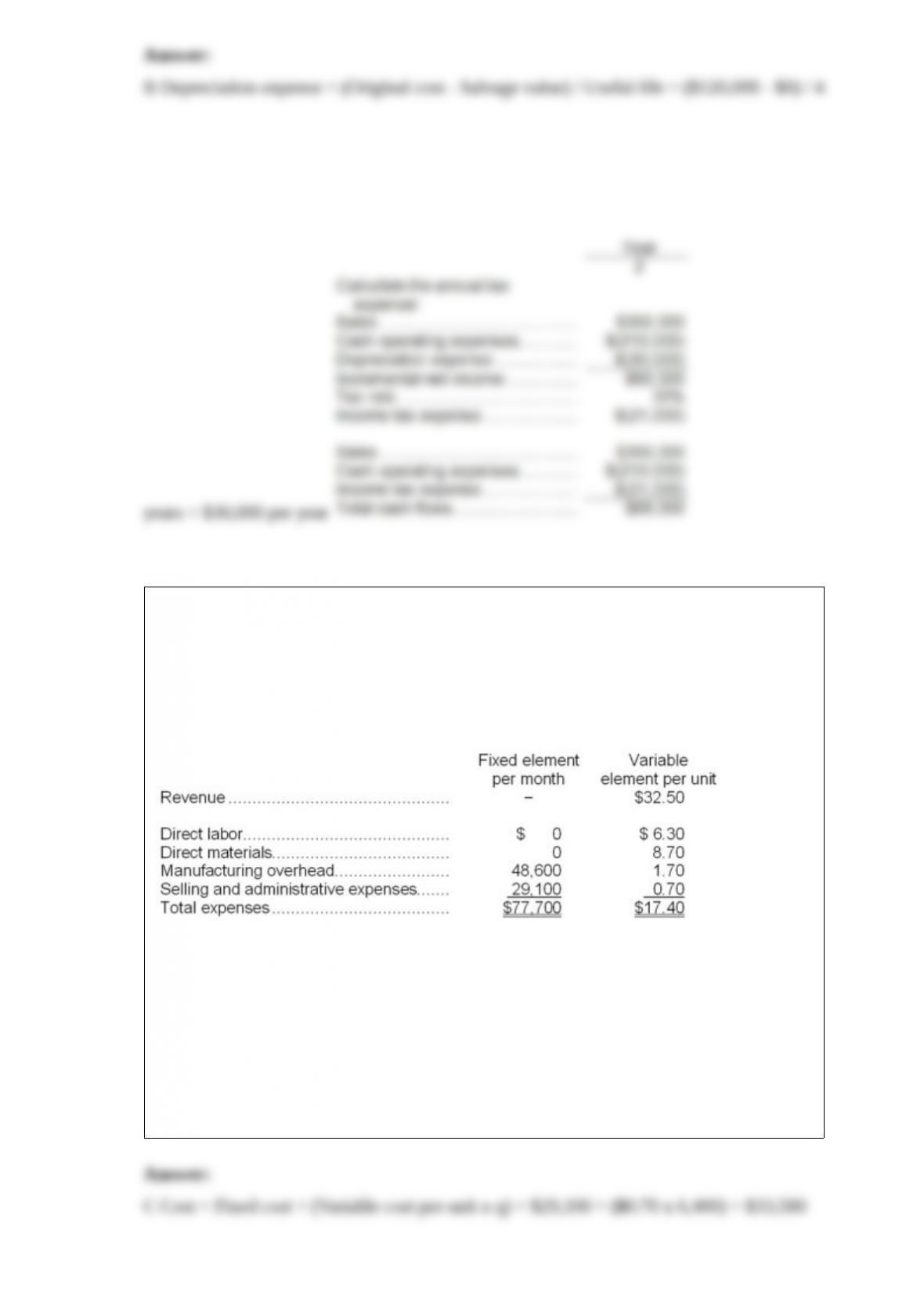

10) Illescas Corporation manufactures and sells a single product. The company uses

units as the measure of activity in its budgets and performance reports. During

December, the company budgeted for 6,400 units, but its actual level of activity was

6,440 units. The company has provided the following data concerning the formulas to

be used in its budgeting:

The selling and administrative expenses in the planning budget for December would be

closest to:

A.$32,396

B.$33,608

C.$33,580

D.$32,598

11) The inventory turnover for Year 2 is closest to:

A.1.06

B.0.94

C.4.36

D.4.24

12) During May at Shatswell Corporation, $57,000 of raw materials were requisitioned

from the storeroom for use in production. These raw materials included both direct and

indirect materials. The indirect materials totaled $7,000. The journal entry to record this

requisition would include a debit to Manufacturing Overhead of:

A.$57,000

B.$7,000

C.$0

D.$50,000

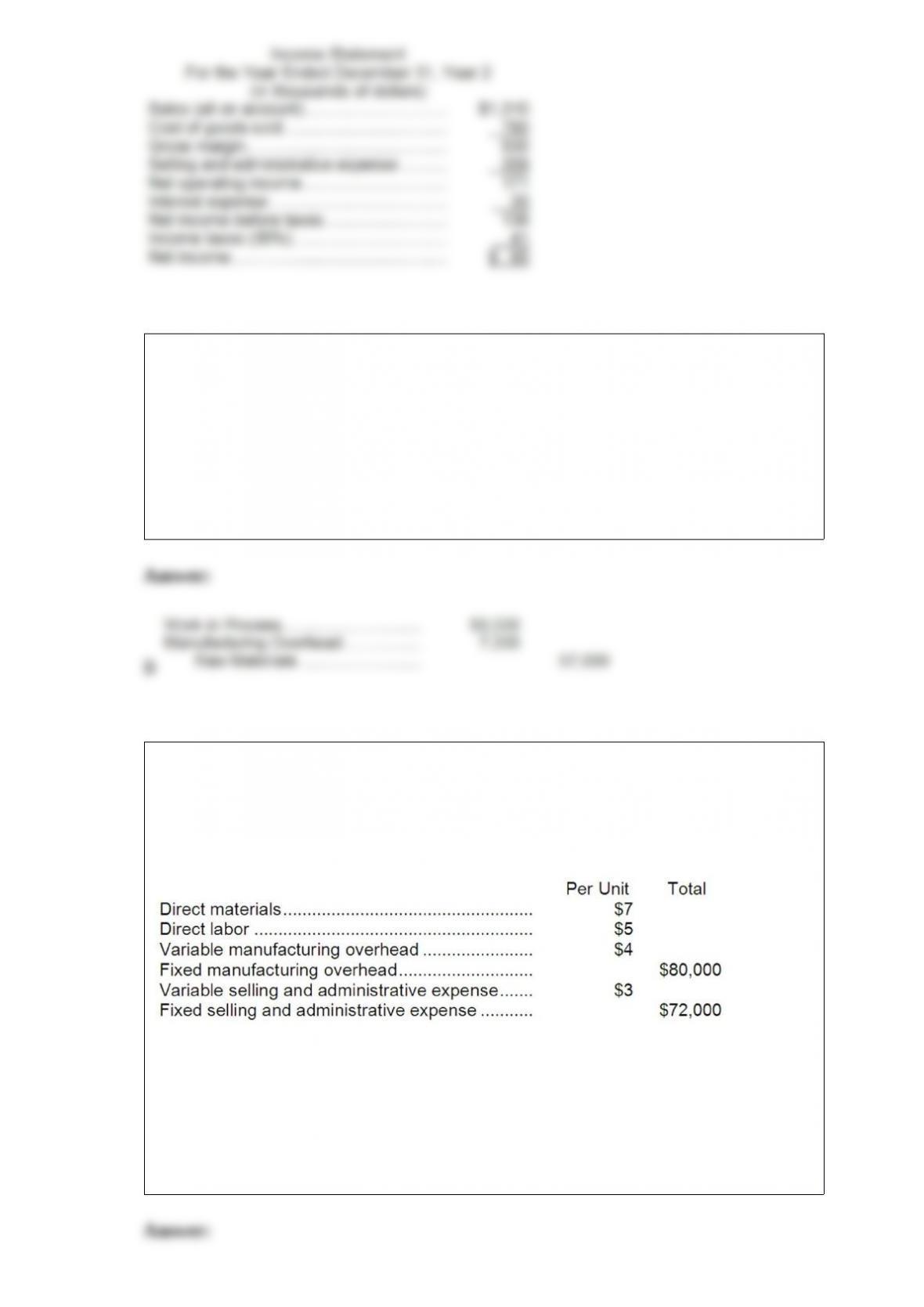

13) The Sloan Corporation must invest $120,000 to produce and market 16,000 units of

Product X each year. The company uses the absorption costing approach to cost-plus

pricing described in the text to set prices for its products. Other cost information

regarding Product X is as follows:

If Sloan Corporation requires a 15% return on investment, then the markup percentage

on absorption cost for Product X (rounded to the nearest percent) would be:

A.41%

B.16%

C.29%

D.22%

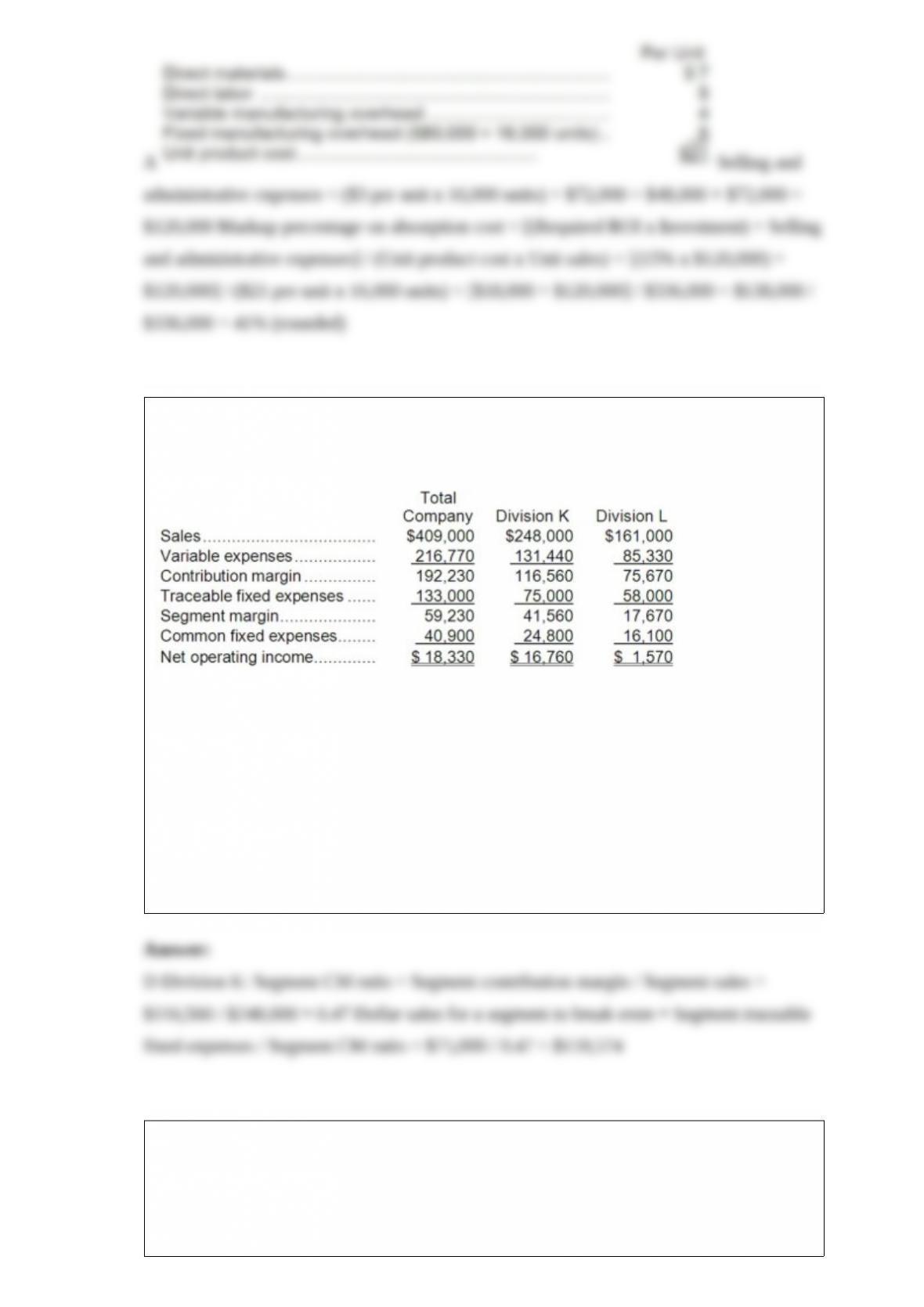

14) Muhn Corporation has two divisions: Division K and Division L. Data from the

most recent month appear below:

Management has allocated common fixed expenses to the Divisions based on their

sales. The break-even in sales dollars for Division K is closest to:

A.$212,340

B.$246,596

C.$370,000

D.$159,574

15) The term gross margin is used in reports prepared using:

A.both absorption costing and variable costing.

B.absorption costing but not variable costing.

C.variable costing but not absorption costing.

D.neither variable costing nor absorption costing.