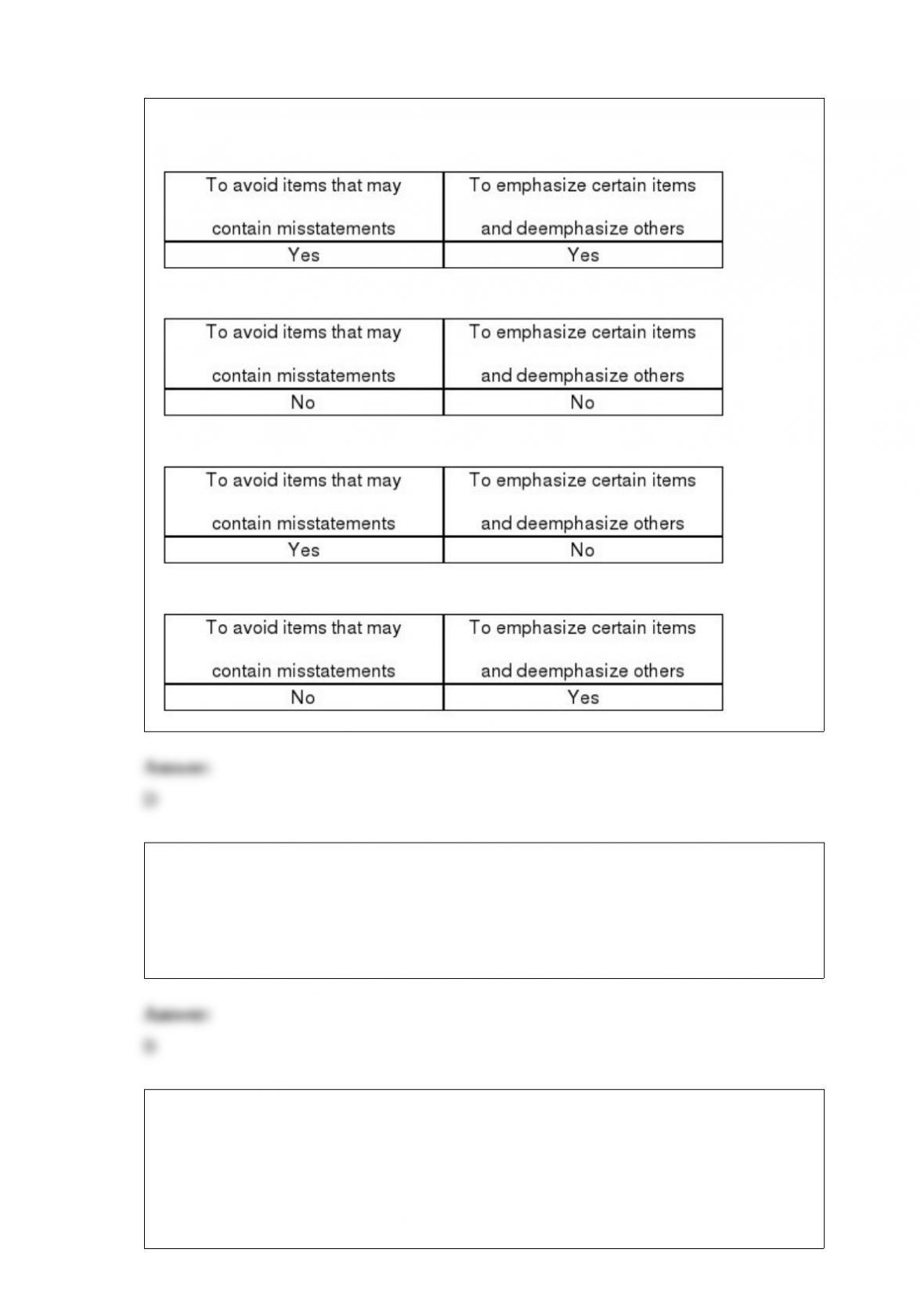

1) What is the purpose of applying stratified sampling to a population?

A)

B)

C)

D)

2) Which of the following is a factor that relates to incentives to misappropriate assets?

A) Significant accounting estimates involving subjective judgments

B) Significant personal financial obligations

C) Management’s practice of making overly aggressive forecasts

D) High turnover of accounting, internal audit and information technology staff

3) If the auditor believes that the financial statements are not fairly stated or is unable to

reach a conclusion because of insufficient evidence, the auditor:

A) should withdraw from the engagement

B) should request an increase in audit fees so that more resources can be used to

conduct the audit

C) has the responsibility of notifying financial statement users through the auditor’s

report

D) should notify regulators of the circumstances

4) Under Rule 101, Independence, independence is considered to be impaired if fees

remain unpaid for professional services provided more than six months before the date

of the current year’s report.

A) True

B) False

5) Which of the following statements are true with respect to audit committees?

I.One member has to be a financial expert.

II.Audit committees are required for all companies.

III.Outside member of the board of directors should comprise the audit committee.

A) I and II

B) I and III

C) II and III

D) I, II, and III

6) The exception rate that the auditor will permit in the population and still be willing to

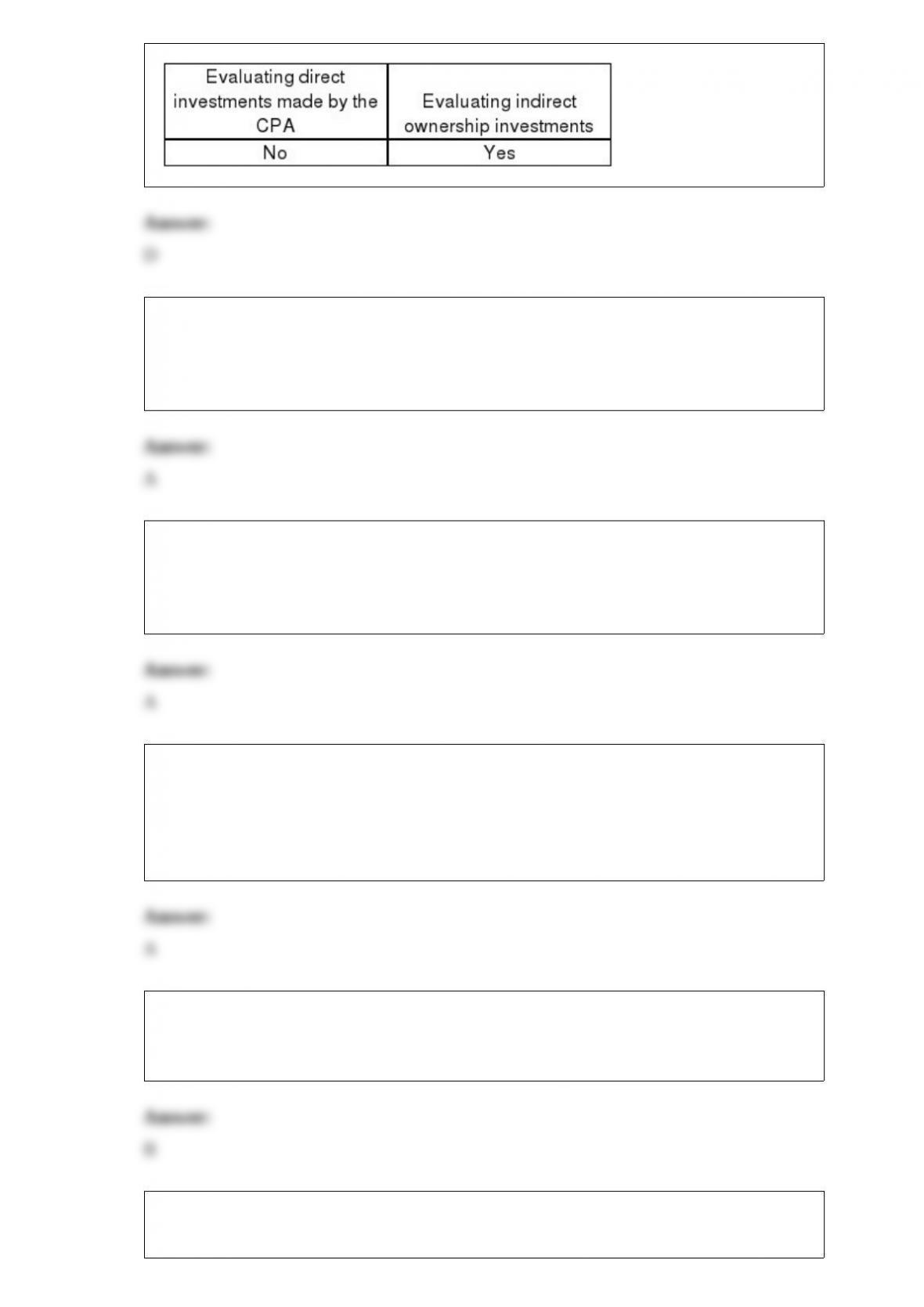

use the preliminary control risk assessment is called the:

A) acceptable exception rate

B) estimated population exception rate

C) sample exception rate

D) tolerable exception rate

7) The job time ticket indicates the starting and stopping times of work during the pay

period.

A) True

B) False

8) Which of the following is the best way for an auditor to determine that every name

on a company’s payroll for the Rodgers factory is that of a bona fide employee presently

on the job?

A) Examine personnel records for accuracy and completeness

B) Examine employees’ names listed on payroll tax returns for agreement with payroll

accounting records

C) Make a surprise observation of the company’s regular distribution of paychecks

D) Visit the working areas and confirm with employees their badge or identification

numbers

9) The emphasis in verifying petty cash is normally on which of the following?

A) Year-end balance

B) Controls over petty cash

C) Transactions for the period

D) Balance sheet classifications

10) The Code of Conduct rule on independence indicates that materiality must be

considered when:

A)

B)

C)

D)

11) Section 404 of the Sarbanes-Oxley Act requires public companies to have an

external auditor attest to their internal control over financial reporting.

A) True

B) False

12) Favorable results from analytical procedures may reduce the extent to which the

auditor needs to test details of balances.

A) True

B) False

13) The major concern when using nonfinancial data in analytical procedures is the:

A) accuracy of the nonfinancial data

B) source of the nonfinancial data

C) type of nonfinancial data

D) presence of multiple sources of nonfinancial data

14) The most important audit objective for depreciation expense is detail tie-in.

A) True

B) False

15) To assure proper segregation of duties, who should maintain the perpetual inventory

master files?

A) production personnel

B) inventory storeroom personnel

C) inventory receiving personnel

D) accounting department personnel

16) Which of the following is generally not included in the “evidence mix”?

A) Tests of Controls

B) Substantive Tests of Transactions

C) Risk Assessment Procedures

D) Tests of details of balances

17) Which of the following types of receivables would not deserve the special attention

of the auditor?

A) Accounts receivables with credit balances

B) Accounts that have been outstanding for a long time

C) Receivables from related parties

D) Each of the above would receive special attention

18) In designing audit procedures for the sales returns and allowances account, the

auditor would primarily rely on the following accounts, except for:

A) sales returns and allowances transaction file

B) accounts receivable master file

C) cash receipts journal

D) sales returns and allowances will be recorded in all of the above

19) Absent disputed amounts and minor timing differences, the vendor’s statements

should reconcile to the:

A) acquisition journal

B) accounts payable master file

C) cash disbursements amount for purchases

D) vouchers payable amount for vendors

20) Which type of audit procedure would normally be sufficient for purposes of

auditing prepaid expenses and deferred charges?

A) Tests of controls

B) Tests of transactions

C) Tests of details of balances

D) Analytical procedures

21) “Independence” in auditing means:

A) maintaining an indirect financial interest

B) not being financially dependent on a client

C) taking an unbiased and objective viewpoint

D) being an advocate for a client

22) Authorization for accepting goods in the receiving department should be based on:

A) Vendor Invoice

B) Requisition Request

C) Purchase order from the purchasing department

D) Vendor Statement

23) Which of the following statements regarding the relevance of evidence is correct?

A) To be relevant, evidence must pertain to the audit objective of the evidence

B) To be relevant, evidence must be persuasive

C) To be relevant, evidence must relate to multiple audit objectives

D) To be relevant, evidence must be derived from a system including effective internal

controls

24) The audit procedure “observe the client taking a physical inventory count and test

the count” is sufficient to determine all of the following except:

A) whether recorded inventory actually exists

B) whether recorded inventory was properly valued by the client

C) whether recorded inventory was properly counted by the client

D) whether client inventory instruction had properly been followed

25) The acquisition and payment cycle consists of one class of transactions.

A) True

B) False

26) An audit designed to provide reasonable assurance of detecting material

misstatements resulting from noncompliance with provisions of contracts or grant

agreements that have a material and direct effect on the financial statements would be

called a(n):

A) performance audit

B) management audit

C) operational audit

D) compliance audit

27) The purpose of establishing quality control policies and procedures to accept or

continue a client relationship is to:

A) provide reasonable assurance that personnel are adequately trained to fulfill their

responsibilities

B) monitor the risk factors concerning misstatements that arise from the

misappropriation of assets

C) document objective criteria for the CPA firm’s peer review

D) minimize the likelihood of associating with client’s whose management may lack

integrity

28) When the auditor decides to “audit around the computer” to obtain an understanding

of the client’s internal controls related to the IT system.

A) True

B) False

29) You are auditing Raji and Company. You discover an item of inventory with an

audited value of $5,000 with a recorded amount of $3,000. If this is the only error you

discover the projected misstatement for the sample would be:

A) $5,000

B) $2,000

C) $3,000

D) $4,000

30) The only modified unqualified opinion that does not include an explanatory

paragraph is when other auditors are involved. In this case only the introductory

paragraph is modified.

A) True

B) False

31) Firing personnel terminates the payroll and personnel cycle.

A) True

B) False

32) In which of the following instances would impair a CPA’s independence when they

have been retained as the auditor?

I.A charitable organization where the CPA serves as treasurer.

II.A municipality where the CPA owns $250,000 of the $25 million outstanding bonds

of the municipality.

III.A company that the CPA’s investment club has a one-tenth investment interest.

A) I and II

B) I and III

C) II and III

D) I, II, and III

33) A signed payroll check that has not been cashed is considered an asset to the

company that issued the check.

A) True

B) False

34) In the fraud triangle, fraudulent financial reporting and misappropriation of assets:

A) share little in common

B) share most of the same risk factors

C) share the same three conditions

D) share most of the same conditions

35) Which one of the following is not one of the primary purposes of audit

documentation prepared by the audit team?

A) A basis for planning the audit

B) A record of the evidence accumulated and the results of the tests

C) A basis for review by supervisors and partners

D) A basis for determining work deficiencies by peer review teams

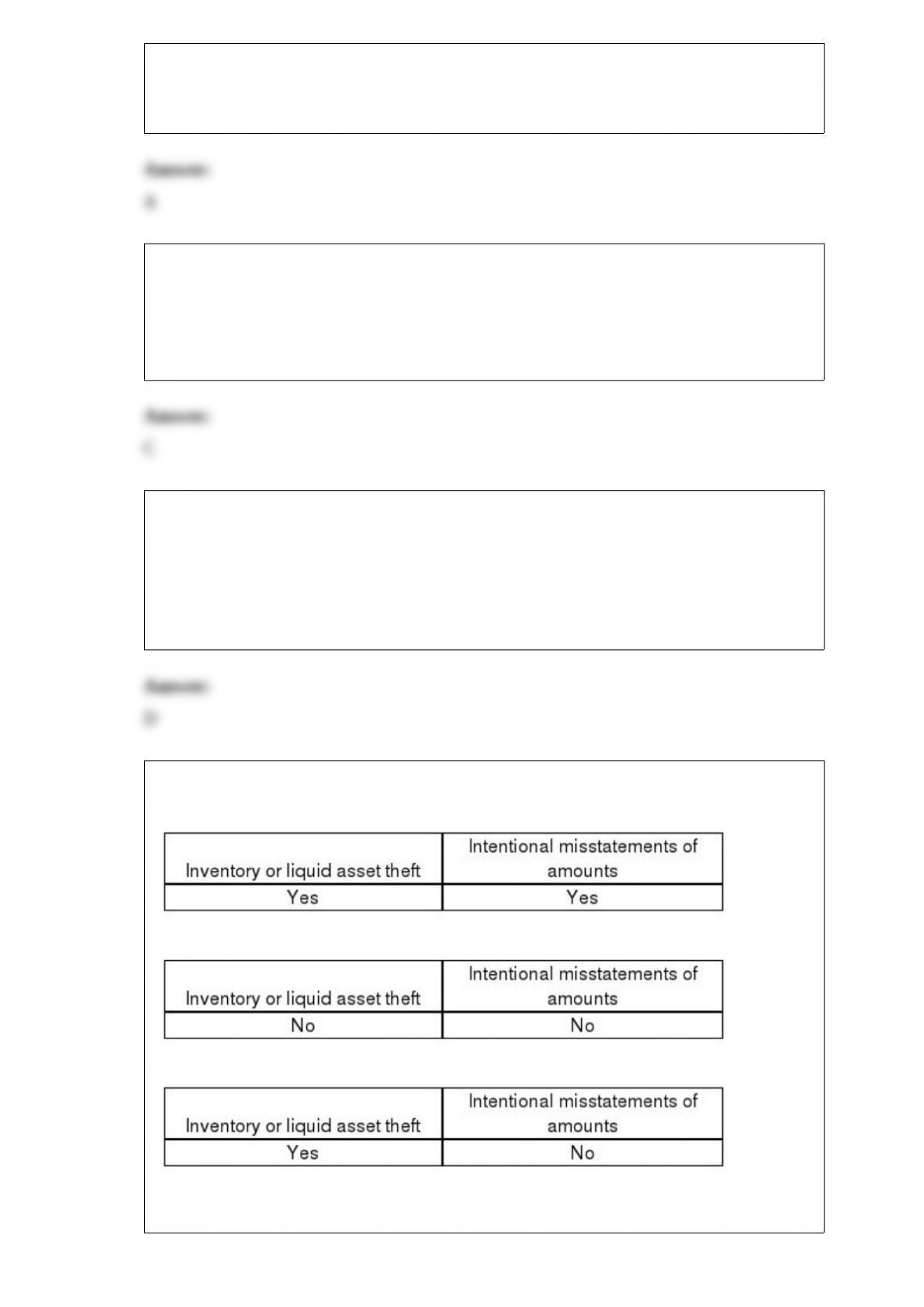

36) With respect to misappropriation of assets, most frauds involve:

A)

B)

C)

Yes No

D)

37) The primary emphasis by auditors is on controls over:

A) classes of transactions

B) account balances

C) both A and B, because they are equally important

D) both A and B, because they vary from client to client

38) In monetary-unit sampling, the likelihood of high dollar items from the population

being included in the sample is lower than the likelihood for small dollar items.

A) True

B) False

39) When a client fails to follow GAAP, the audit can be unqualified, qualified, or

adverse depending on the materiality. What factors affect materiality that an auditor

should consider?

A) The dollar amount in comparison to a base

B) If the misstatement can be measured

C) The nature of the item

D) All the above are factors an auditor should consider regarding materiality