Which of the accounting changes listed below is more associated with financial

statements prepared in accordance with U.S. GAAP than with International Financial

Reporting Standards (IFRS)?

a. Change in reporting entity.

b. Change to the LIFO method from the FIFO method.

c. Change in accounting estimate.

d. Change in depreciation methods.

Which of the following is an example of an extended warranty?

a. Fancy Headphones, Inc. provides assurance that its headphones are defect-free after

purchase.

b. Azalea’s Flowers assures clients that its flowers will stay fresh for at least a week.

c. Mark Electronics offers a warranty at an affordable price that provides additional

protection after the customer takes possession of the product.

d. Erickson Electronics promises to make repairs or replace any product found to be

defective within a week of purchase.

Consider the following:

I. Present value of vested benefits at present pay levels.

II. Present value of nonvested benefits at present pay levels.

III. Present value of additional benefits related to projected pay increases.

Which of the above constitutes the projected benefit obligation?

a. III only.

b. I, II.

c. I, II, III.

d. II only.

Which of the following would be reported as a cash outflow from investing activities?

a. Issuance of bonds.

b. Purchase of land.

c. Payment of dividends.

d. Retirement of common stock.

Which of the following statements is true regarding correcting errors in previously

issued financial statements prepared in accordance with International Financial

Reporting Standards (IFRS)?

a. The error can be reported in the current period if it’s not considered practicable to

report it retrospectively.

b. The error can be reported in the current period if it’s not considered practicable to

report it prospectively.

c. The error can be reported prospectively if it’s not considered practicable to report it

retrospectively.

d. Retrospective application is required with no exception.

Each of the following would be reported as items of other comprehensive income

except:

a. Foreign currency translation gains.

b. Unrealized gains on investments accounted for as securities available for sale.

c. Deferred gains from derivatives.

d. Gains from the sale of equipment.

Current liabilities normally are recorded at their:

a. Present value.

b. Cost.

c. Maturity amount.

d. Expected value.

Lucia Ltd. reported net income of $135,000 for the year ended December 31, 2016.

January 1 balances in accounts receivable and accounts payable were $29,000 and

$26,000, respectively. Year-end balances in these accounts were $30,000 and $24,000,

respectively. Assuming that all relevant information has been presented, Lucia’s cash

flows from operating activities would be:a. $132,000.

b. $134,000.

c. $136,000.

d. $138,000.

Pension expense is decreased by:

a. Amortization of prior service cost.

b. Amortization of net gain.

c. Benefits paid to retired employees.

d. Prior service cost.

At the start of the current year, SBC Corp. purchased 30% of Sky Tech Inc. for $45

million. At the time of purchase, the carrying value of Sky Tech’s net assets was $75

million. The fair value of Sky Tech’s depreciable assets was $15 million in excess of

their book value. For this year, Sky Tech reported a net income of $75 million and

declared and paid $15 million in dividends.

The amount of purchased goodwill is:

a. $18 million.

b. $30 million.

c. $60 million.

d. None of the above is correct.

Wilson Links Products sells a product that involves two separate performance

obligations: the SwingRight golf club weight and the SwingCoach teaching software.

SwingRight has a stand-alone selling price of $150. Wilson sells both the SwingRight

and the SwingCoach as a package deal for $200. The SwingCoach software is not sold

separately. Wilson is aware that other vendors charge $100 for similar software, and

Wilson’s prices are generally 10% lower than what is charged by those vendors. Wilson

estimates that it incurs approximately $65 of cost per copy of the software, and usually

charges 50% above cost on similar products.

Estimate the stand-alone selling price of the software using the adjusted market

assessment approach.

a. $50

b. $80

c. $90

d. $97.50

The component of pension expense that results from amending a pension plan to give

recognition to previous service of currently enrolled employees is the amortization of:

a. Prior service costs.

b. Amendment costs.

c. Retiree service costs.

d. Transition costs.

The amortization of bond discount is included in the statement of cash flows (indirect

method) as:

a. A financing cash inflow.

b. An investing activity.

c. An addition to net income.

d. A deduction from net income.

Explain the appropriate accounting method used to account for lump-sum purchases of

a group of long-term assets.

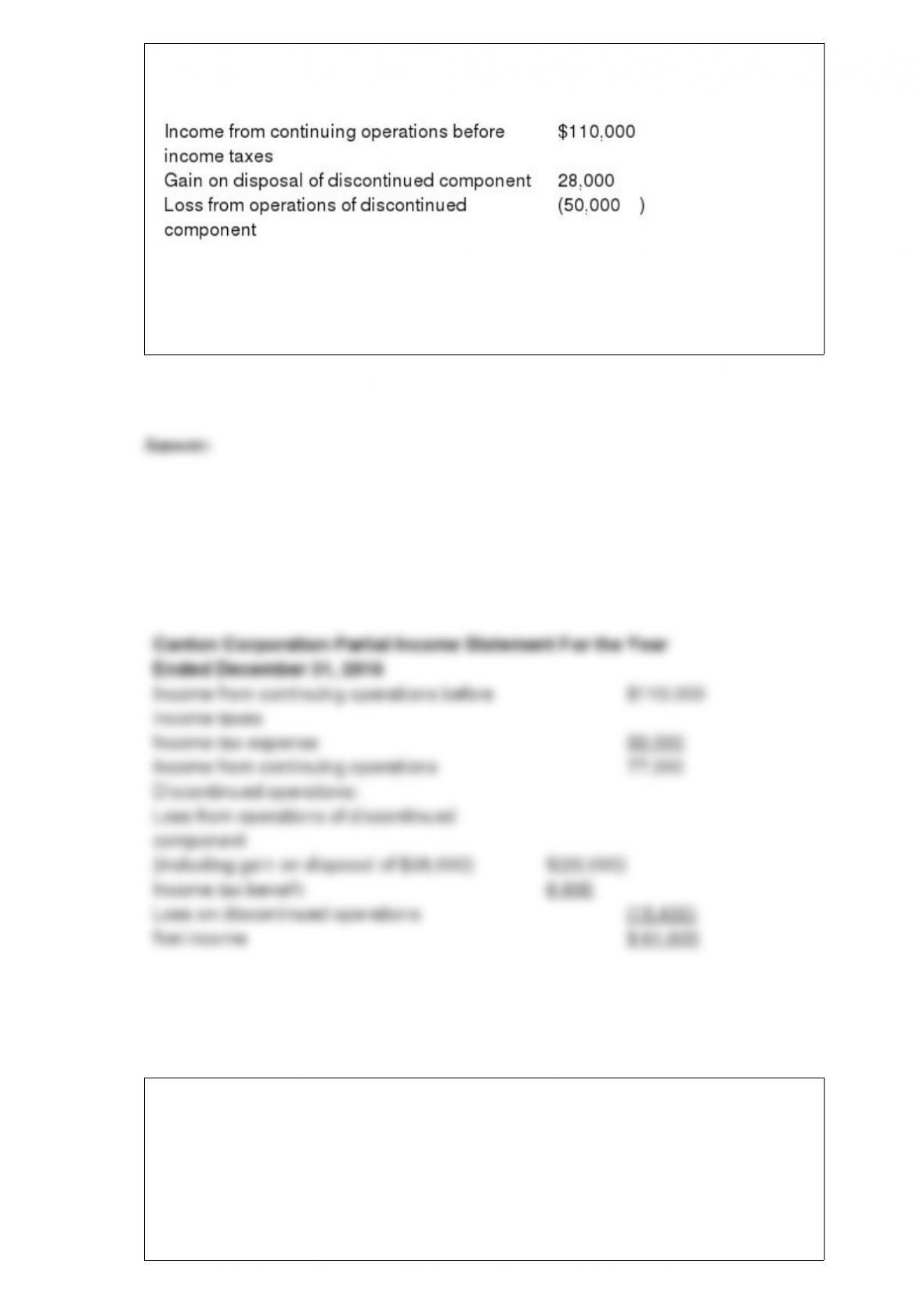

Canton Corporation reported the following items in its adjusted trial balance for the

year ended December 31, 2016:

Canton is subject to a 30% tax rate.

Required: Prepare the December 31, 2016, income statement for Canton Corporation,

starting with income from continuing operations before income taxes.

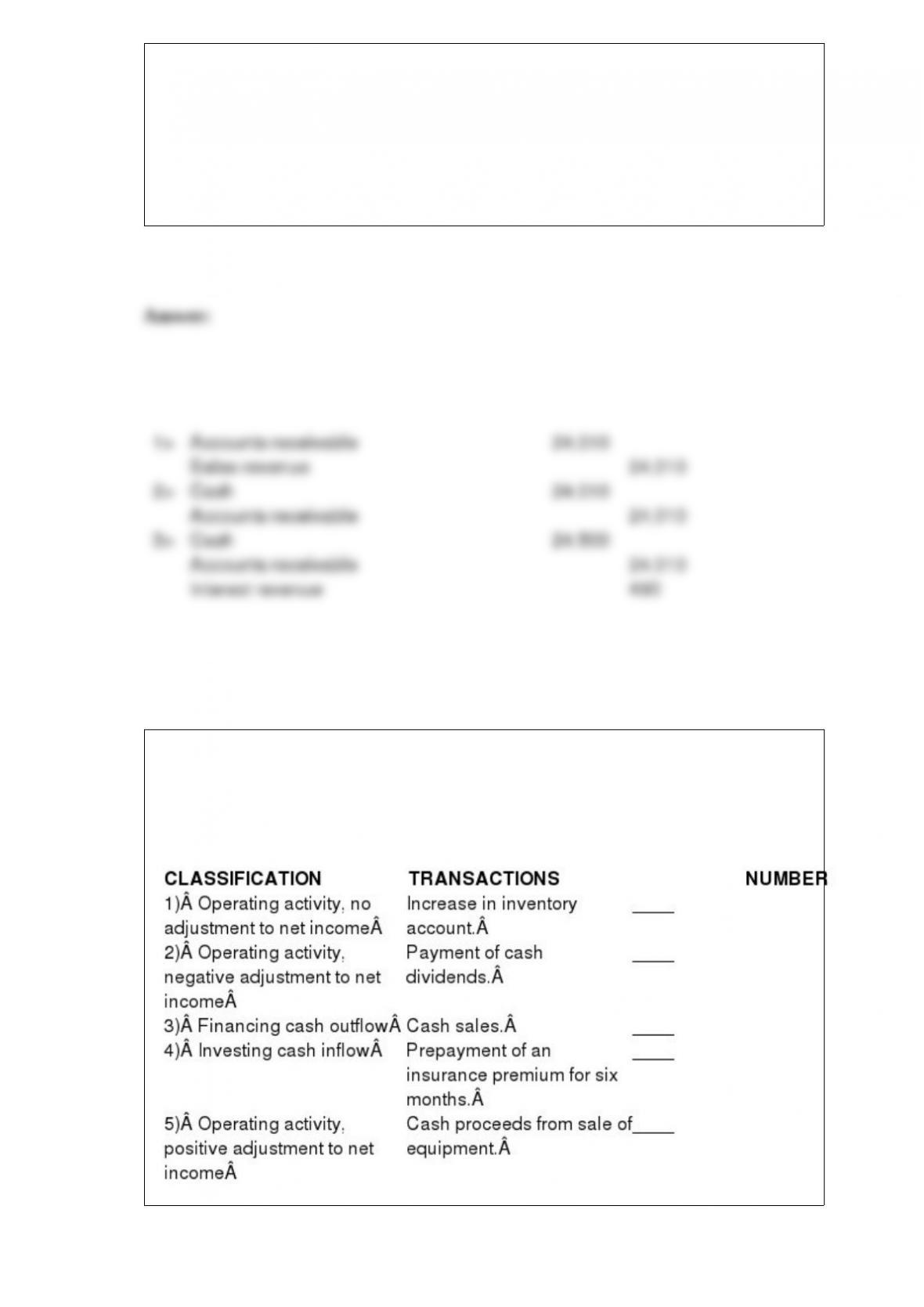

On February 14, 2016, Prime Company sold 50 air-conditioning units to L&P Heating

and Cooling. The units list for $700 each, but L&P was granted a 30% trade discount.

All of Prime’s sales are subject to terms 2/10, n/30. Prime uses the net method of

accounting for sales discounts.

Required:

1> Prepare the journal entry to record the sale.

2> Prepare the journal entry to record receipt of the payment, assuming the correct

amount was received on February 22, 2016.

3> Prepare the journal entry to record receipt of the payment, assuming the correct

amount was received on March 10, 2016.

Listed below are reporting classifications for a statement of cash flows using the

indirect method for reporting operating cash flows. Indicate the reporting classification

that would apply to each of the five transactions described below by placing the number

of the reporting classification in the space provided by each transaction.

Many high-tech companies sell products with the opportunity for retailers to return the

merchandise if it is unsold after a certain period. This reduces the retailer’s risk of

inventory obsolescence. Explain the implications on revenue recognition under this

kind of policy. Include a specific example.

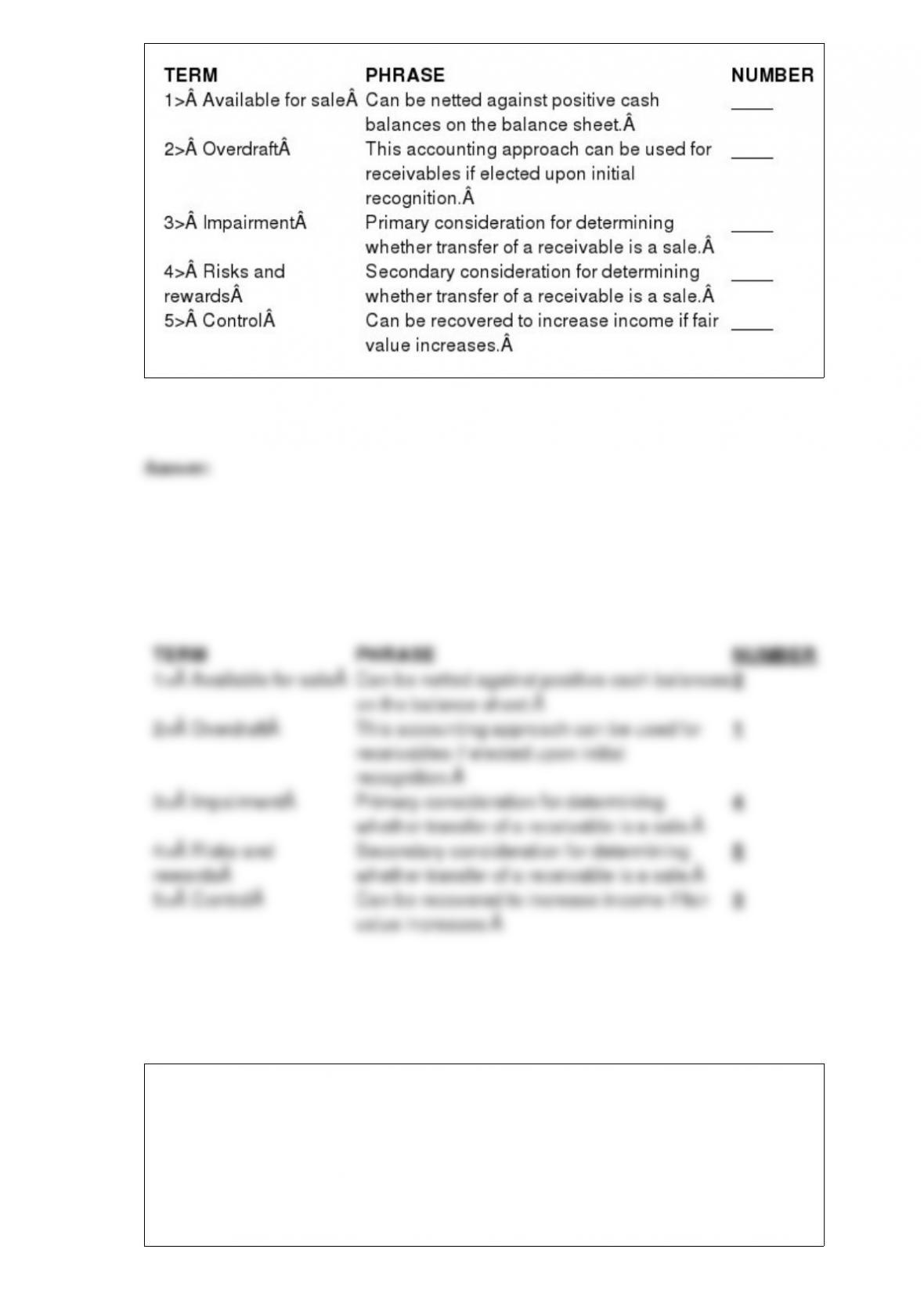

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms with respect to accounting under IFRS. Match each phrase with the

number for the correct term.

Nagy Industries reported a net income of $619,369 on December 31, 2016. At the

beginning of the year, the company had 500,000 common shares outstanding. On April

1, the company sold 27,000 shares for cash. On August 31, the company issued 48,000

additional shares as part of a merger. On December 1, 2016, the company declared and

issued a 10% stock dividend.

Required:

Compute Nagy’s net income that would produce a basic EPS of $2.00 per share for

2016.