The purchase of treasury stock creates an asset for the corporation and is recorded at the

cost of the shares purchased.

The future amount of an annuity is calculated by multiplying the present value of the

annuity by its applicable factor from a table.

The future value will always be less than the present value.

Activity-based management is a subset of activity-based costing.

The gross profit method can be used for both interim and year-end financial reporting.

Return on equity is a commonly used measure of a company’s profitability.

Liability accounts should only be debited and never credited.

The first step in a bank reconciliation is to update the depositor’s accounting records for

any deposits in transit.

When a company makes a sale by accepting a bank-issued credit card from the

customer, the sale is recorded as a cash sale.

Debiting Work in Process in Department Two and crediting Work in Process in

Department One represents costs transferred from Department Two to Department One.

The Foreign Corrupt Practices Act distinguishes between influence peddling and

facilitating payments. Facilitating payments are prohibited, while influence peddling is

allowed.

The break-even point is the level of activity at which operating income is equal to cost

of goods sold.

The most important factor affecting the market price of common stock is the stated

dividend rate.

Management accounting encompasses the design and use of accounting information

systems inside the company to achieve the company’s objectives.

Depreciation is a non-cash expense.

The balance sheet is prepared first because if it balances, all the accounting information

is correct and can be used to prepare the other financial statements.

In the bank reconciliation, every adjustment to the balance per depositor’s records

requires a journal entry.

Increases in owners’ equity are recorded by credits; increases in assets and in liabilities

are recorded by debits.

The materials price variance is calculated by multiplying the difference between actual

unit price and standard unit price, by the standard units purchased.

Product costs become part of inventory and are placed on the balance sheet until the

products are sold.

Purchase Discounts Lost is shown as a reduction of cost of goods sold in the income

statement.

If a transaction takes place with terms 2/10, n/30, the “10” refers to the percent discount

a purchaser can take if payment is made within 2 days.

One of the purposes of adjusting entries is to convert assets to expenses.

Capital budgeting estimates often involve a considerable degree of uncertainty.

The relationship between book value and market price of capital stock is a measure of

investors’ confidence in a company’s management.

The Financial Accounting Standards Board (FASB) maintains and periodically updates

a well-defined list of disclosure items that companies must include in their annual

reports.

Canada has adopted IFRS, but Mexico and the European Union have chosen not to

adopt International Financial Reporting Standards.

The margin of safety sales volume times the contribution margin ratio equals operating

income.

Costs which increase in total amount in direct proportion to an increase in output are

called variable costs.

Return on investment is the same as return of investment.

As volume increases, per unit fixed costs stay the same.

Hedging refers to the strategy of taking offsetting positions so that gains in one

currency offset losses in another currency.

As volume increases, total fixed costs remain the same.

Closely held corporations have the same ability to qualify for credit sources as publicly

traded corporations.

Book value represents the cost of an asset that has already been allocated to expense.

The term “financial asset” is synonymous with the term “cash equivalent.”

In activity-based costing, only one cost driver should be used in applying overhead.

When a business borrows money from a bank, the immediate effect is an increase in

total assets and a decrease in liabilities or owners’ equity.

On April 30, 2014, Tilton Products purchased machinery for $88,000. The useful life of

this machinery is estimated at 8 years, with an $8,000 residual value.

Refer to the information above. In the year 2020, Tilton Products sells this machinery

for $4,500. At the date of sale, the machinery had been depreciated by Tilton Products

to its estimated residual value of $8,000. This sale results in:

A. A $3,500 loss in both the company’s financial statements and income tax return.

B. No gain or loss in either the financial statements or income tax return.

C. A $3,500 loss in the financial statements; a $3,500 gain in the income tax return.

D. A $3,500 loss in the financial statements, but no gain or loss in the income tax return.

At the end of last year, Games-2-Use had merchandise costing $140,000 in inventory.

During January of the current year, the company purchased merchandise costing

$102,000, and sold merchandise that it had purchased at a total cost of $84,000.

Games-2-Use uses a perpetual inventory system.

Refer to the information above. The total amount debited to the Inventory account

during January was:

A. $0.

B. $84,000.

C. $102,000.

D. $140,000.

At year-end, the perpetual inventory records of Anderson Co. indicate 60 units of a

particular product in inventory, acquired at the following dates and unit costs:

Purchased in August: 30 units at $750 per unit.

Purchased in November: 30 units at $700 per unit.

A complete physical inventory taken at year-end indicates only 50 units of this product

actually are on hand.

Refer to the information above. Assuming that Anderson uses the FIFO cost flow

assumption, it should record this inventory shrinkage by:

A. Crediting Cost of Goods Sold $7,500.

B. Debiting Cost of Goods Sold $7,000.

C. Crediting Cost of Goods Sold $7,000.

D. Debiting Cost of Goods Sold $7,500.

The set of activities necessary to create and distribute a desirable product or service to a

customer is known as:

A. A customer perspective.

B. Business process perspective.

C. Balanced scorecard.

D. Value chain.

The manufacturing efficiency ratio equals:

A. Value-added time divided by cycle time.

B. Value-added time multiplied by cycle time.

C. Cycle time divided by value-added time.

D. (Cycle time divided by value-added time) divided by 2.

Effective internal control over accounts receivable ensures all of the following except:

A. All shipments of goods during the period are recorded.

B. The sale transaction is recorded for the correct dollar amount.

C. That cash collections from customers are promptly deposited.

D. The availability of adequate cash for conducting business operations.

Which of the following is not a characteristic of managerial accounting?

A. Reports are used primarily by insiders rather than by persons outside of the business

entity.

B. Its purpose is to assist managers in planning and controlling business operations.

C. Information must be developed in conformity with generally accepted accounting

principles or with income tax regulations.

D. Information may be tailored to assist in specific managerial decisions.

During the current year, Carl Equipment Stores had net sales of $600 million, a cost of

goods sold of $500 million, average accounts receivable of $75 million, and average

inventory of $50 million.

Refer to the information above. Carl Equipment’s inventory turnover rate is:

A. 6.7 times.

B. 10 times.

C. 12 times.

D. 1.2 times.

Which statement is true about a stock split?

A. Total shareholders’ equity increases.

B. Total shareholders’ equity decreases.

C. Total shareholders’ equity remains the same.

D. A change in total stockholders’ equity depends upon whether it is a 2-for-1 split or a

3-for-1 split.

At the beginning of 2015, Wilson Stores has an inventory of $300,000. Because sales

growth was strong during 2015, the owner wants to increase inventory on hand to

$450,000 at December 31, 2015. If net sales for 2015 are expected to be $2,600,000,

and the gross profit rate is expected to be 35%, compute the cost of the merchandise the

owner should expect to purchase during 2015.

A. $750,000.

B. $1,240,000.

C. $1,690,000.

D. $1,840,000.

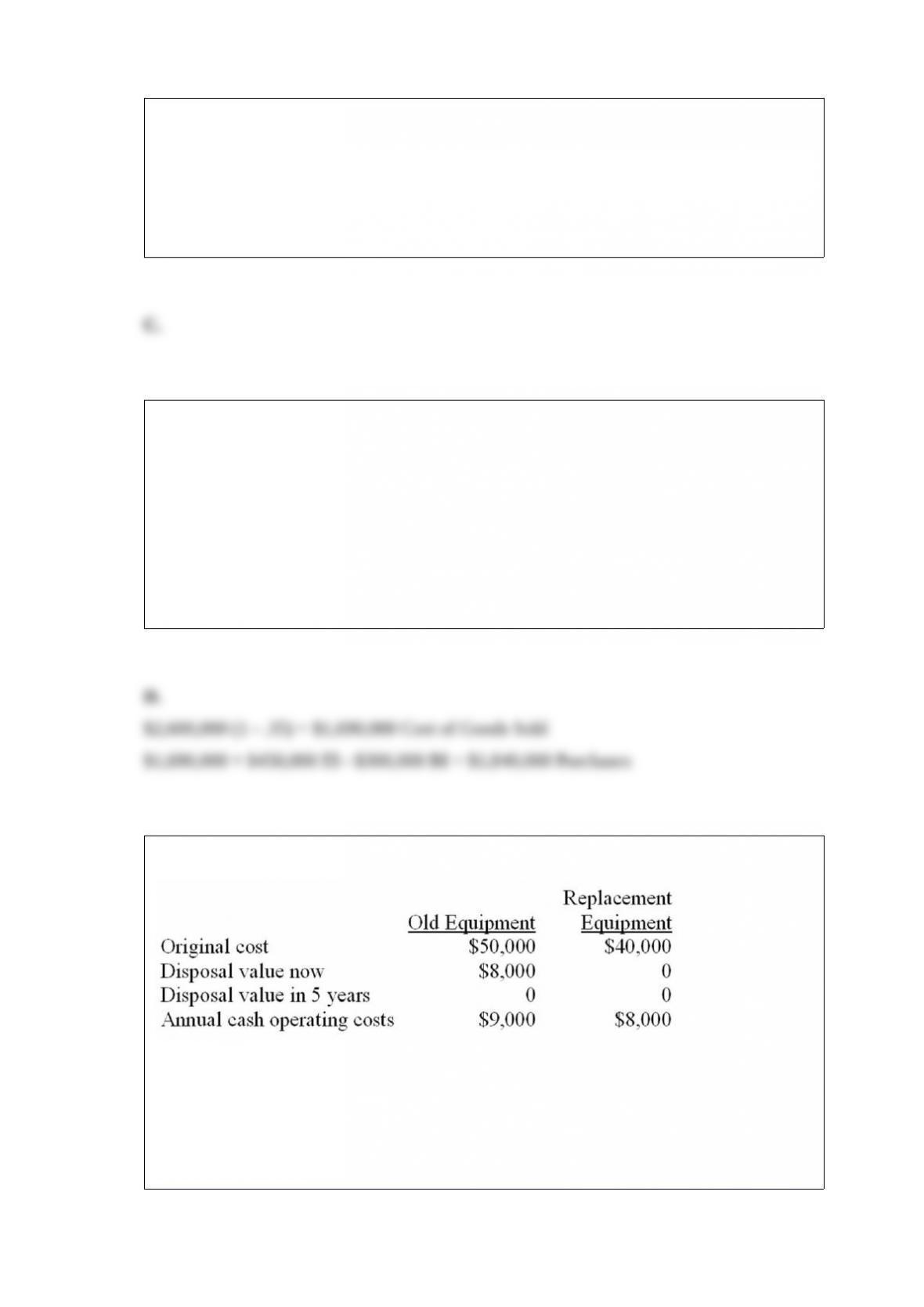

Express, Inc., is considering replacing equipment. The following data are available:

Refer to the information above. What are the total relevant costs of keeping the old

equipment?

A. $8,000.

B. $50,000.

C. $10,000.

D. $45,000.

An asset which costs $14,400 and has accumulated depreciation of $8,000 is sold for

$5,600. What amount of gain or loss will be recognized when the asset is sold?

A. A gain of $800.

B. A loss of $800.

C. A loss of $2,400.

D. A gain of $2,400.

Regal Artworks Co. records purchases net of all available purchase discounts. If the

company makes payment after the discount has expired, the entry to record the payment

should include a:

A. Debit to Purchase Discounts Lost.

B. Credit to Purchase Discounts Lost.

C. Debit to Sales Discounts.

D. Credit to Sales Discounts.

Busch, Inc. is a successful company, but has a lower inventory turnover rate than the

industry average. Of the following, the most likely explanation is that Busch:

A. Has a just-in-time inventory system.

B. Uses LIFO (assume rising purchase costs).

C. Offers its customers an unusually large selection of merchandise.

D. Sells unusually popular items.

If costs of goods sold is $560,000 and its gross profit rate is 20%, what is the gross

profit?

A. $140,000.

B. $70,000.

C. $120,000.

D. $112,000.

The Cost of Goods Sold account is closed by:

A. Debiting Cost of Goods Sold and crediting Income Summary.

B. Debiting Cost of Goods Sold and crediting Retained Earnings.

C. Debiting Income Summary and crediting Cost of Goods Sold.

D. Debiting Retained Earnings and crediting Cost of Goods Sold.

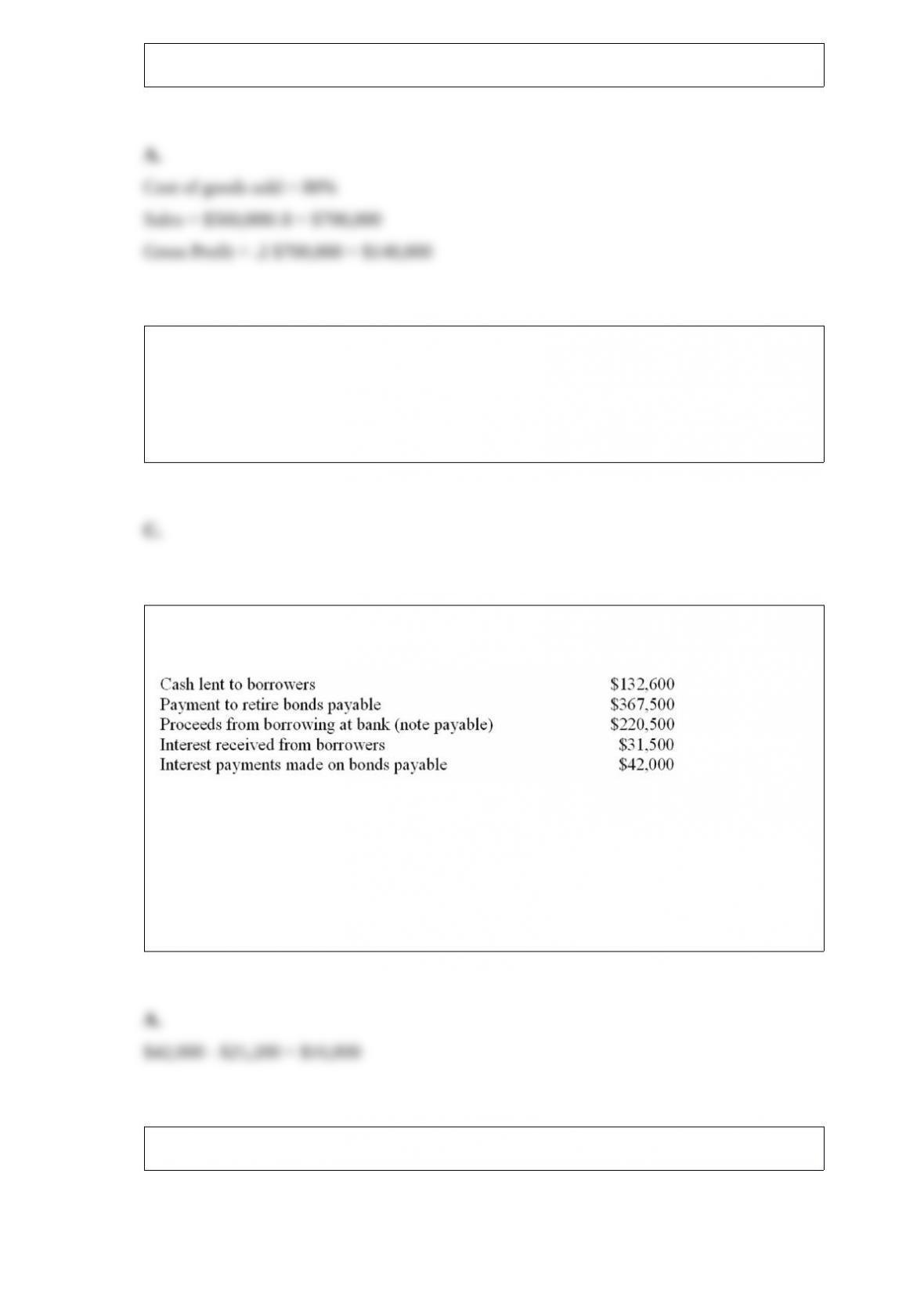

During 2015, the cash flows related to Global Data, Inc.’s lending and borrowing

activities are summarized as follows:

Refer to the information above. If Global Data’s income statement for 2015 reports

interest expense of $25,200, then:

A. Interest payable decreased by $16,800 in 2015.

B. Interest payable increased by $16,800 in 2015.

C. Interest payable at the end of 2015 amounts to $16,800.

D. Either the amount reported in the income statement or the interest payment shown

above must be incorrect.

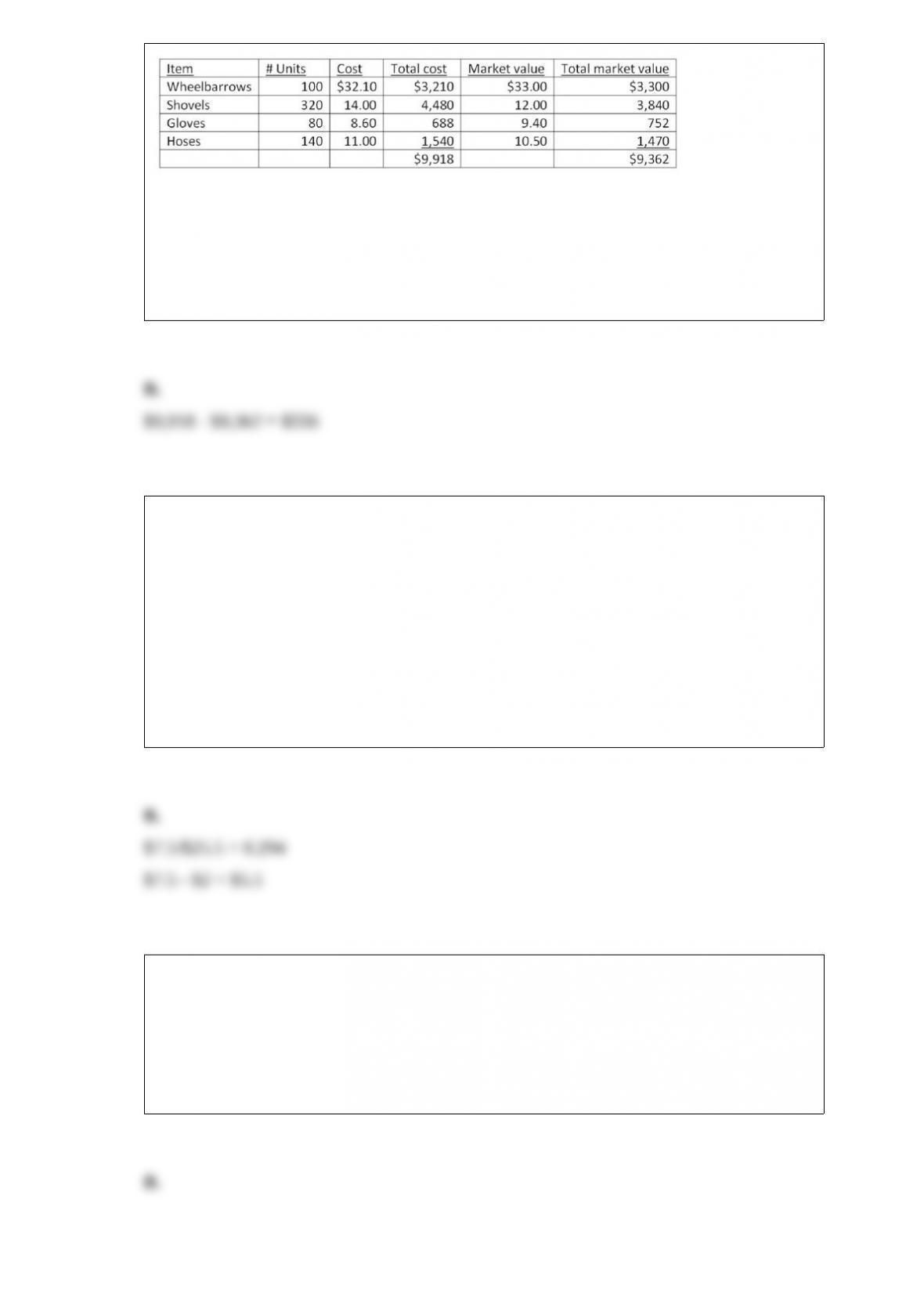

Green Leaf Company had the following information available on December 31:

Management applies the LCM rule on the basis of the total inventory. What is the

write-down required?

A. $864.

B. $556.

C. $576.

D. $710.

The current balance sheet of Apex reports total assets of $20 million, total liabilities of

$2 million, and owners’ equity of $18 million. Apex is considering several financing

possibilities in order to expand operations. Each question based on this data is

independent of any others.

Refer to the information above. What is the approximate maximum amount Apex can

borrow and not exceed a debt ratio of .3?

A. $4,000,000.

B. $5,500,000.

C. $5,000,000.

D. $600,000.

When reading a bank statement, which reference indicates an increase in the cash

balance?

A. Debit Memorandum.

B. Credit Memorandum.

C. NSF Check.

D. Service Charge.

If the beginning inventory of the current year and the ending inventory of the past year

were overstated by the same amount:

A. Retained earnings at the end of the current year would be correct.

B. Retained earnings at the end of the current year would be overstated.

C. Retained earnings at the end of the current year would be understated.

D. Net income for the current year would be correct.

Refer to the information above. The total debits in the After Closing-Trial Balance will

equal:

A. $23,360.

B. $28,640.

C. $22,400.

D. $6,720.

A master budget usually includes all of the following except:

A. A sales forecast.

B. A cash budget.

C. A projected tax return.

D. Projected financial statements.

The Music House issues a contract to a new recording artist to produce a number of

albums over the next five years at $1 million per album. This situation is an example of:

A. A contingent liability which should be recorded in the accounting records.

B. A contingent liability requiring footnote disclosure.

C. An estimated liability, since the number of albums to be produced is not yet

determined.

D. A commitment which, if material, may be disclosed in a footnote.

When a depreciable asset is sold at a price equal to its book value, a journal entry would

include:

A. A credit to the asset account for its book value.

B. A debit to accumulated depreciation.

C. A credit to accumulated depreciation.

D. A credit to cash.

The return on investment is calculated by:

A. Multiplying the capital turnover by the return on sales.

B. Dividing the capital turnover by the return on sales.

C. Dividing average invested capital by sales.

D. Multiplying operating income by capital turnover.

Carrier Corporation produces heating and air conditioning equipment at a number of

plants throughout the United States including one in Syracuse, New York. Carrier

should evaluate its Syracuse plant as:

A. A cost center.

B. An investment center.

C. A profit center (other than an investment center).

D. A committed center.

Partner A earns $68,000 from a partnership. Partner B earns $57,000 but withdraws

only $49,000. How much must Partner B report in his income tax return as income?

A. $49,000.

B. $57,000.

C. $125,000.

D. $117,000.

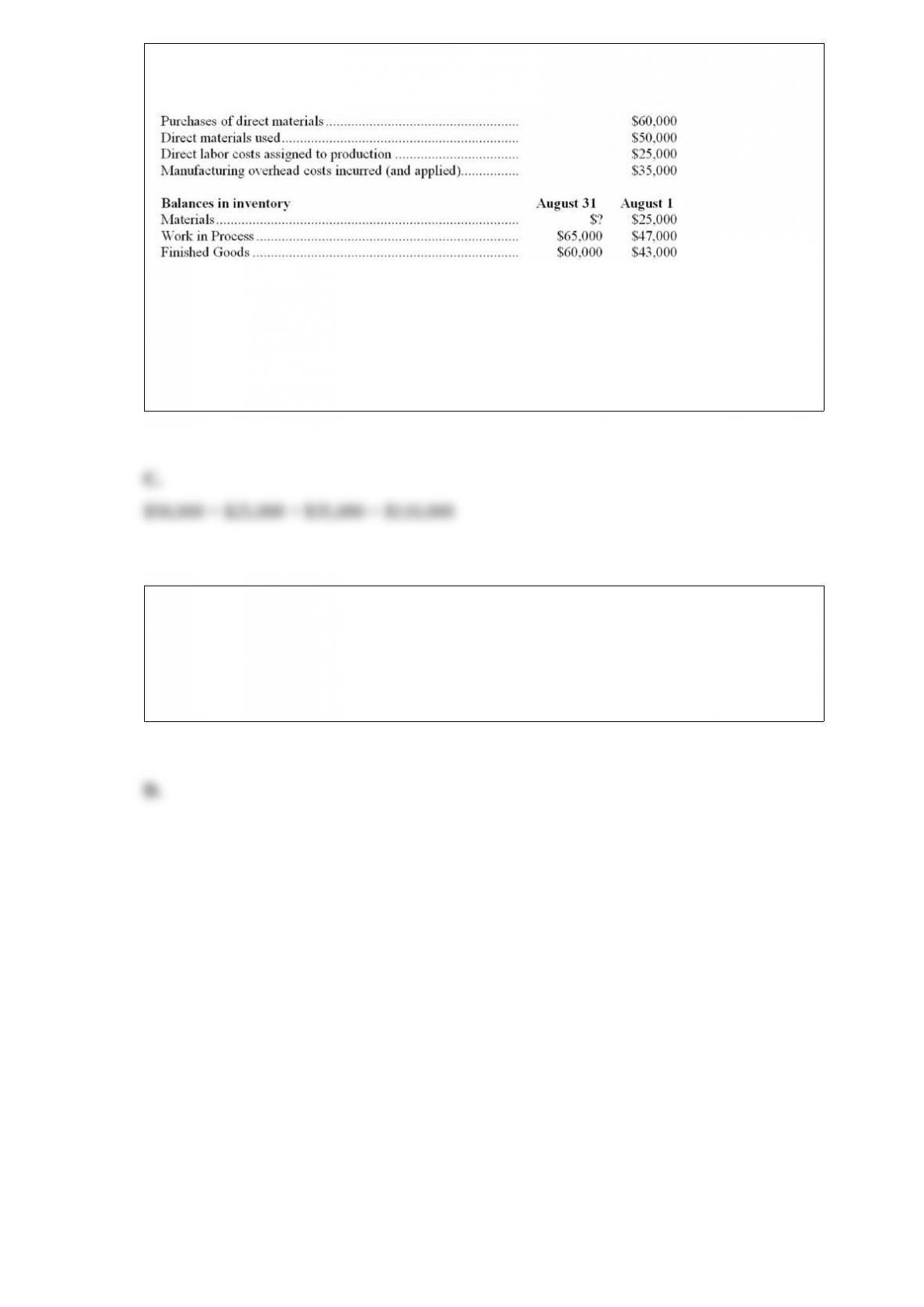

The following information has been taken from the perpetual inventory system of Elite

Mfg. Co. for the month ended August 31:

Refer to the above data. Total manufacturing costs charged (debited) to Work in Process

during August amount to:

A. $60,000.

B. $125,000.

C. $110,000.

D. Some other amount.

A typical production cost report will contain all of the following except:

A. The number of equivalent units.

B. The total cost of production.

C. The costs per equivalent units.

D. The costs assigned to each job.