Carpenter Gems began the year with a net pension liability of $84 million (underfunded

pension plan). Pension expense for the year included the following ($ in millions):

service cost, $30; interest cost, $18; expected return on assets, $12; amortization of net

loss, $6.

Required:

Prepare the appropriate general journal entry to record Carpenter’s pension expense.

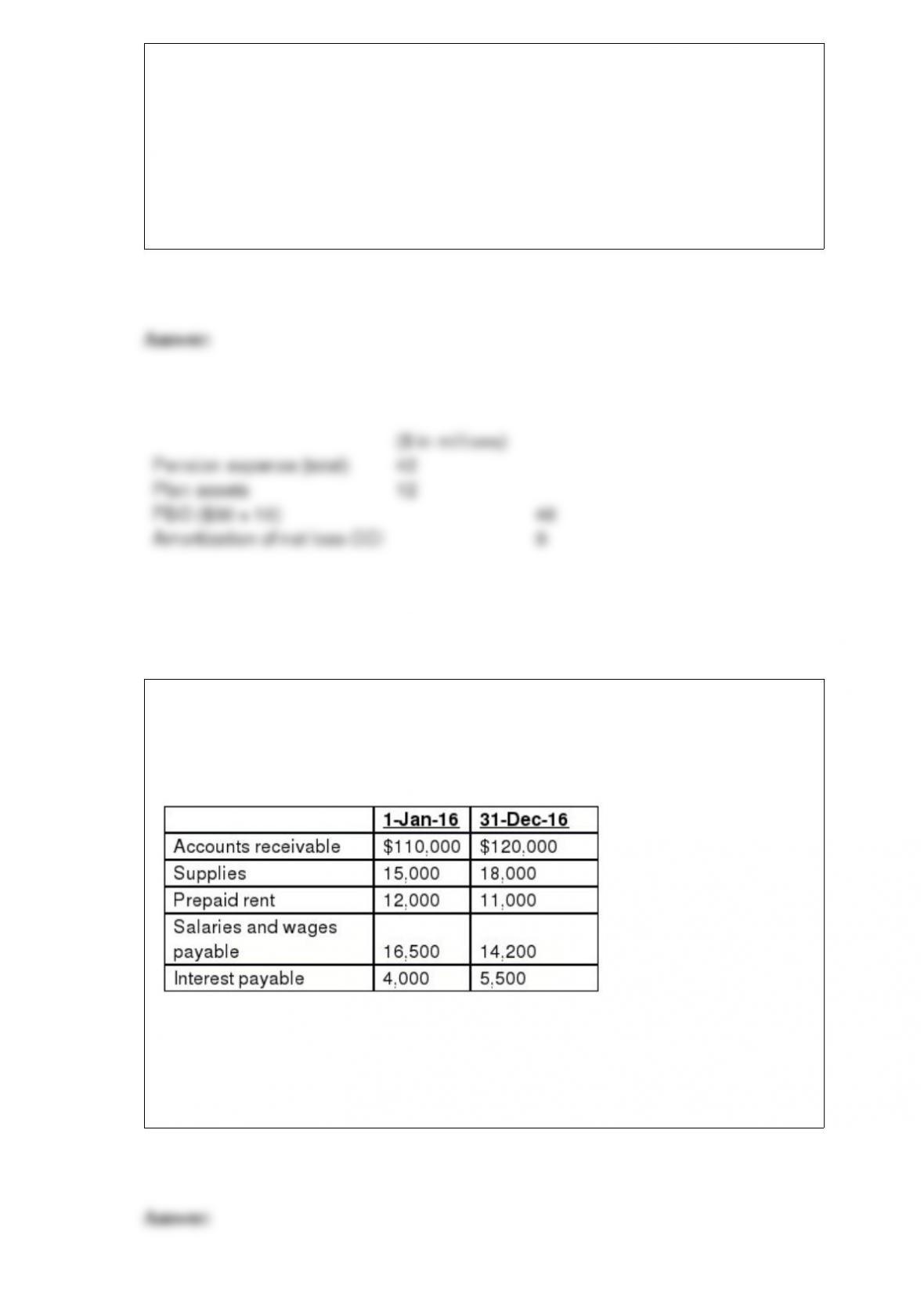

Claymore Corporation maintains its book on a cash basis. During 2016, the company

collected $825,000 in fees from its clients and paid $512,000 in expenses. You are able

to determine the following information about accounts receivable, supplies, prepaid

rent, salaries payable, and interest payable:

In addition, 2016 depreciation expense on office equipment and furniture is $55,000.

Required:

Determine accrual basis income for 2016.

Previously, marketable equity securities were reported using a technique referred to as

“lower of cost or market.” The current accounting standard requires fair value reporting

for trading securities and securities available for sale. Some accountants believe that the

FASB was inconsistent when GAAP was issued requiring changes in the value of

trading securities to be reported in the income statement and balance sheet, while

changes in the value of securities available for sale are reported only in the balance

sheet.

Required:

Evaluate the rationale for these two diverse reporting requirements for equity securities.

What arguments could be made to support each treatment?

In early December of 2016, Blue Corp. purchased $40,000 of Yellow Company

common stock, which constitutes less than 3% of Yellow’s outstanding shares. Blue

accounts for the Yellow investment as available for sale. By December 31, 2016, the

value of the Yellow investment had fallen to $30,000, and Blue recorded an unrealized

loss. By December 31, 2017, the value of the Yellow investment had fallen to $15,000,

and Blue determined that it can no longer assert that it has both the intent and ability to

hold the shares long enough for their fair value to recover, so Blue recorded an OTT

impairment. By December 31, 2018, fair value had recovered to $20,000. Prepare

appropriate entry(s) at December 31, 2018, and indicate how the scenario will affect net

income, OCI, and comprehensive income.

Are the following separate performance obligations: prepayments, quality-assurance

warranty, extended warranty, right of return? For each, indicate yes or no, and explain.