1) The accounting equation for an agency fund is

A) Current assets – Current liabilities = Fund Balance

B) Assets – Liabilities = Equity

C) Assets = Equity + Liabilities

D) Assets = Liabilities

2) Paris Corporation purchased 80% of the outstanding voting common stock of

Sanders Corporation on January 1, 2011, at a cost of $400,000. The stockholders’ equity

of Sanders Corporation on this date consisted of $200,000 of Capital Stock and

$100,000 of Retained Earnings. Book values were equal to fair values except for land

and inventory. The book value of Sanders’ land was $10,000, and fair value was

$22,000. The book value of Sanders’ inventory was $30,000, and fair value was

$25,000.

Assume Paris’s inventory account had a book value of $40,000 and a fair value of

$44,000 on January 1, 2011 . Using the parent company theory, what was the amount

reported on the consolidated balance sheet for inventories on January 1, 2011?

A) $65,000

B) $66,000

C) $69,000

D) $70,000

3) In a not-for-profit, private university, the federal grant funds given directly to

students for financial aid are an example of

A) a bequest

B) an agency transaction

C) unrestricted revenue

D) a restricted contribution

4) Which statement is correct in describing the rank order of payments as specified by

the Uniform Partnership Act?

A) Payments to partners are ranked equally, regardless of underlying basis

B) Payment to partners with excess capital balances may be placed ahead of payments

to creditors

C) Payments to creditors other than partners are ranked ahead of payments to partners

D) After payments are made to other creditors and partners with loans to the

partnership, payment up to the same amount can be made to partners with capital

interests

5) The fixed assets and long-term liabilities associated with Proprietary Funds are

reported on the

A) financial statements of governmental funds

B) financial statements of fiduciary funds

C) financial statements of proprietary funds

D) financial statements of trust funds

6) If a parent company and outside investors purchase shares of a subsidiary in relation

to existing stock ownership (ratably), then

A) there will be an adjustment to additional paid-in capital if the stock is sold above

book value

B) there will be no adjustment to additional paid-in capital regardless whether the stock

is sold above or below book value

C) there will be an adjustment to additional paid-in capital if the stock is sold below

book value

D) there will be the elimination of a gain

7) An entity which qualified for fresh-start accounting is not required to disclose which

of the following items in their initial financial statements?

A) Adjustments from historical cost of assets and liabilities

B) Amount of debt of the prior entity forgiven

C) Amount of ending retained earnings/deficit of the prior entity

D) Changes to the management team from the prior entity

8) On January 1, 2012 Saffron Co. recorded a $40,000 profit on the upstream sale of

some equipment that had a remaining four-year life under the straight-line depreciation

method. The equipment has no salvage value. Saffron had separate income of $100,000

in 2012 . The parent company, Pommel Incorporated, owns 90% of Saffron. Pommel

would report investment income from Saffron in 2012 of

A) $54,000

B) $63,000

C) $90,000

D) $126,000

9) The collapse of the subprime mortgage market increased the spread between Baa and

default-free US Treasury bonds This is due to

A) a reduction in risk

B) a reduction in maturity

C) a flight to quality

D) a flight to liquidity

10) According to the liquidity premium theory of the term structure, a slightly upward

sloping yield curve indicates that short-term interest rates are expected to

A) rise in the future

B) remain unchanged in the future

C) decline moderately in the future

D) decline sharply in the future

11) A summary balance sheet for the Lemon, Mango, and Nobb partnership appears

below. Lemon, Mango, and Nobb share profits and losses in a ratio of 2:3:5,

respectively.

Assets

Cash$ 100,000

Marketable securities200,000

Inventory125,000

Land100,000

Building-net500,000

Total assets$1,025,000

Equities

Lemon, capital$ 425,000

Mango, capital400,000

Nobb, capital200,000

Total equities$1,025,000

The partners agree to admit Oran for a one-fifth interest. The fair market value of

partnership land is appraised at $200,000 and the fair market value of inventory is

$175,000. The assets are to be revalued prior to the admission of Oran and there is

$30,000 of goodwill that attaches to the old partnership.

By how much will the capital accounts of Lemon, Mango, and Nobb increase,

respectively, due to the revaluation of the assets and the recognition of goodwill?

A) The capital accounts will increase by $50,000 each

B) The capital accounts will increase by $60,000 each

C) $36,000, $54,000, and $90,000

D) $40,000, $50,000, and $60,000

12) A(n) ________ in the liquidity of corporate bonds will ________ the price of

corporate bonds and ________ the yield on corporate bonds, all else equal

A) increase; increase; decrease

B) increase; decrease; decrease

C) decrease; increase; increase

D) decrease; decrease; decrease

13) What basis of accounting is used to prepare Government-wide financial statements?

A) Modified accrual basis

B) Accrual basis

C) Cash basis

D) Fiduciary basis

14) On January 1, 2010, Shrimp Corporation purchased a delivery truck with an

expected useful life of five years, and a salvage value of $8,000. On January 1, 2012,

Shrimp sold the truck to Pacet Corporation. Pacet assumed the same salvage value and

remaining life of three years used by Shrimp. Straight-line depreciation is used by both

companies. On January 1, 2012, Shrimp recorded the following journal entry:

Debit Credit

Cash50,000

Accumulated depreciation18,000

Truck53,000

Gain on Sale of Truck15,000

Pacet holds 60% of Shrimp. Shrimp reported net income of $55,000 in 2012 and Pacet’s

separate net income (excludes interest in Shrimp) for 2012 was $98,000.

In preparing the consolidated financial statements for 2012, the elimination entry for

depreciation expense was a

A) debit for $5,000

B) credit for $5,000

C) debit for $15,000

D) credit for $15,000

15) Pull Incorporated and Shove Company reported summarized balance sheets as

shown below, on December 31, 2011 .

Pull Shove

Current assets$420,000 $210,000

Noncurrent assets670,000 430,000

Total assets $1,090,000$640,000

Current liabilities$230,000$50,000

Long-term debt 350,000 150 000

Stockholders’ equity 510,000 440,000

Total liabilities and equities$1,090,000$640,000

On January 1, 2012, Pull purchased 70% of the outstanding capital stock of Shove for

$392,000, of which $92,000 was paid in cash, and $300,000 was borrowed from their

bank. The debt is to be repaid in 10 annual installments beginning on December 31,

2012, with each payment consisting of $30,000 principal, plus accrued interest.

The excess fair value of Shove Company over the underlying book value is allocated to

inventory (60 percent) and to goodwill (40 percent).

Required: Calculate the balance in each of the following accounts, on the consolidated

balance sheet, immediately following the acquisition.

a.Current assets

b.Noncurrent assets

c.Current liabilities

d.Long-term debt

e.Stockholders’ equity

16) On November 1, 2010, Athom Corporation purchased 5,000 television sets for its

merchandise inventory from Sockk, a South Korean firm, at a total quoted cost of

600,000,000 won (W). On this date, the spot rate for the won was $1 = 1,080W. On the

same day, Athom invested $500,000 cash in a non-interest bearing account with a

Japanese bank, to hedge its exposed liability position. The account payable to Sockk is

due on January 30, 2011 . The exchange rates on December 31, 2010 and January 30,

2011 were $1 = 1,060W, and $1 = 1,030W, respectively. Athom agreed to pay Sockk in

won. The bank deposit made by Athom will be held in won, but will be withdrawn in

dollars by Athom on January 30th. Assume that Athom has a December 31 year-end.

Assume this is a fair value hedge.

Required:

Prepare all the journal entries for Athom Corporation’s General Journal on November 1,

2010, December 31, 2010, and January 30, 2011 . Round entries to the nearest whole

dollar. If no entry is required on a particular date, indicate “No entry” in the General

Journal.

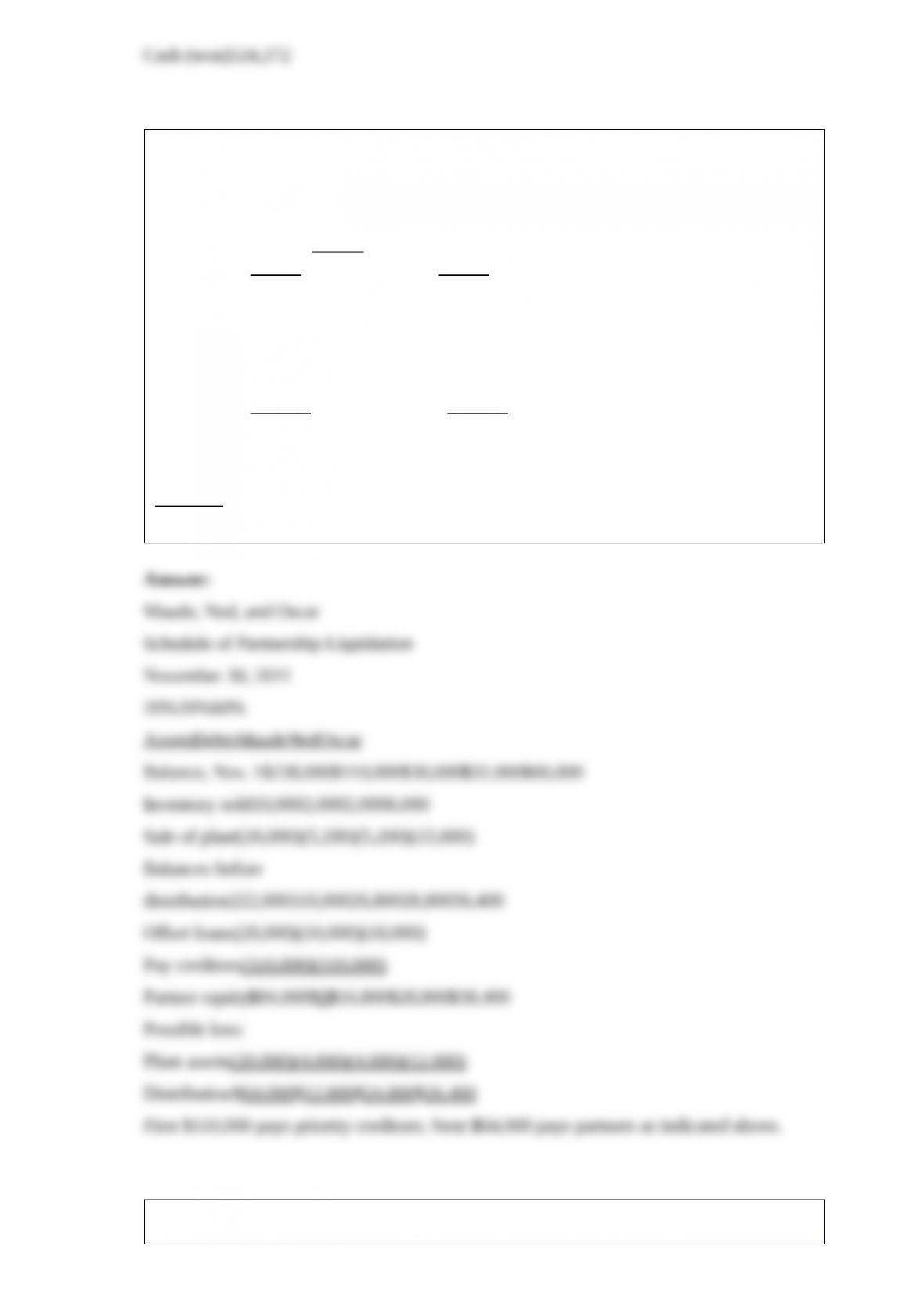

17) The balance sheet of the Maude, Ned, and Oscar partnership on November 1, 2011

(before commencement of partnership liquidation) was as follows:

Cash$12,000Georgia, capital (40%)$36,000

Holly, capital (30%)6,000

Festus, capital (50%)31,000

Total assets$90,000Total liab./equity$90,000

Cash$70,000Accounts payable$42,000

Inventory60,000Notes payable68,000

Loan to Maude10,000Maude, capital(20%)30,000

Loan to Oscar18,000Ned, capital(20%)32,000

Plant assets-net80,000Oscar, capital(60%)66,000

Total assets$238,000Total liab./equity$238,000

Liquidation events in November were as follows:

– All the inventory was sold for $10,000 above book value;

– Plant assets with a book value of $60,000 were sold for $34,000.

Required:

Determine how the available cash on November 31, 2011 should be distributed.

18) Pfeifer Corporation acquired an 80% interest in Stern Corporation several years ago

when the book values and fair values of Stern’s assets and liabilities were equal. At the

time of acquisition, the cost of the 80% interest was equal to 80% of the book value of

Stern’s net assets. Separate company income statements for Pfeifer and Stern for the

year ended December 31, 2011 are summarized as follows:

PfeiferStern

Sales Revenue$1,000,000 $600,000

Investment income from Stern85,000

Cost of Goods Sold(600,000)(300,000)

Expenses(200,000)(200,000)

Net Income$285,000 $100,000

During 2010, Pfeifer sold merchandise that cost $120,000 to Stern for $180,000. Half of

this merchandise remained in Stern’s inventory at December 31, 2010 . During 2011,

Pfeifer sold merchandise that cost $150,000 to Stern for $225,000. One-third of this

merchandise remained in Stern’s December 31, 2011 inventory.

Required:

Prepare a consolidated income statement for Pfeifer Corporation and Subsidiary for

2011 .

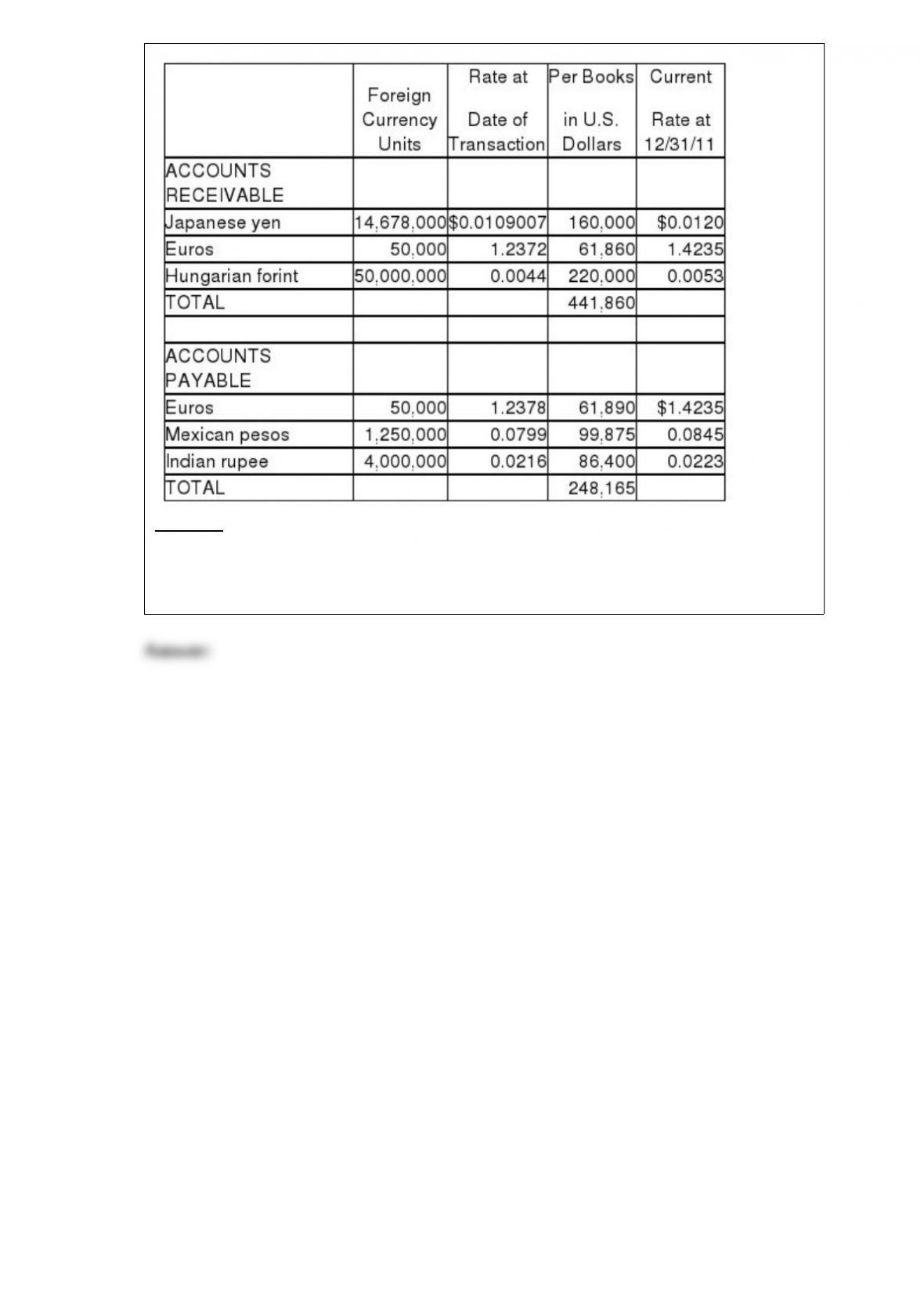

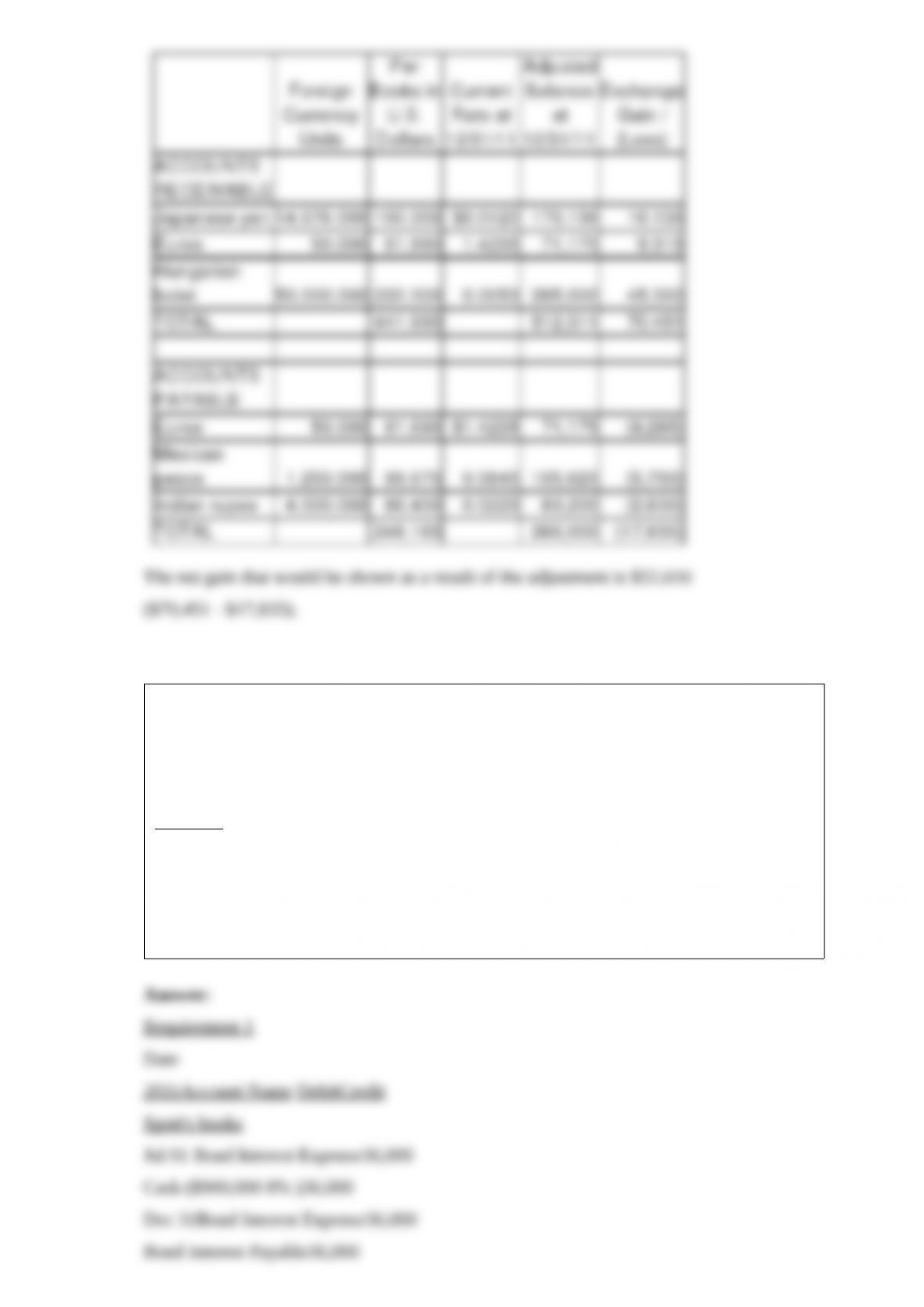

19) Lincoln Corporation, a U.S. manufacturer, both imports needed materials and

exports finished products. Their receivables and payables are listed below, prior to

year-end adjustments or preparation of the closing entries.

Required:

Determine the amount at which receivables and payables should be reported on

December 31, 2011, and the net exchange gain or loss that would be reported as a result

of year-end adjustments.

20) Spott is a 75%-owned subsidiary of Penthal. On January 1, 2010, Spott issued

$900,000 of $1,000 face amount 8% bonds at par. The bonds have interest payments on

January 1 and July 1 of each year and mature on January 1, 2014 . On July 2, 2011,

Penthal purchased all 900 bonds on the open market for $1,020 per bond. Both

companies use straight-line amortization.

Required:

With respect to the bonds, use General Journal format to:

1>Record the 2011 journal entries from July 1 to December 31 on Spott’s books.

2>Record the 2011 journal entries from July 1 to December 31 on Penthal’s books.

3>Record the elimination entries for the consolidation working papers for the year

ending December 31, 2011 .