Which of the following creates a deferred tax liability? A. An unrealized loss from

recording inventory at lower of cost or market.

B. Accelerated depreciation in the tax return.

C. Estimated warranty expense.

D. Subscriptions collected in advance.

Answer:

M Corp. has an employee benefit plan for compensated absences that gives each

employee 15 paid vacation days. Vacation days can be carried over indefinitely.

Employees can elect to receive payment in lieu of vacation days. At December 31,

2013, M’s unadjusted balance of liability for compensated absences was $30,000. M

estimated that there were 200 total vacation days available at December 31, 2013. M’s

employees earn an average of $150 per day. In its December 31, 2013, balance sheet,

what amount of liability for compensated absences is M required to report? A. $0.

B. $30,000.

C. $225,000.

D. $450,000.

Answer:

Under the gross method, purchase discounts taken are: A. Deducted from interest

expense.

B. Added to net purchases.

C. Added to interest income.

D. Deducted from purchases.

Answer:

B Corp. has an employee benefit plan for compensated absences that gives each

employee 10 paid vacation days and 10 paid sick days. Both vacation and sick days can

be carried over indefinitely. Employees can elect to receive payment in lieu of vacation

days; however, no payment is given for sick days not taken. At December 31, 2013, B’s

unadjusted balance of liability for compensated absences was $42,000. B estimated that

there were 300 total vacation days and 150 sick days available at December 31, 2013.

B’s employees earn an average of $200 per day. In its December 31, 2013, balance

sheet, what amount of liability for compensated absences is B required to report? A.

$60,000.

B. $84,000.

C. $90,000.

D. $144,000.

Answer:

Listed below are ten terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1)Related-party transactions

2)Unearned revenues

3)Subsequent events

4)Accounts receivable

5)Oil well

6)MDA

7)Franchise

8)Retained earnings

9)Inventories

10)Prepaid expense

A. Transactions with owners, managers, and affiliated companies.

B. Cash received from a customer in advance of providing a good or service.

C. Amounts due from customers.

D. Goods to be sold in the ordinary course of business.

E. A natural resource.

F. Asset recorded when an expense is paid for in advance.

G. Net income less dividends since inception of the corporation.

H. Material event that occurs after the end of the fiscal year and before the statements

are issued.

I. Management’s views on significant events.

J. An intangible asset.

Answer:

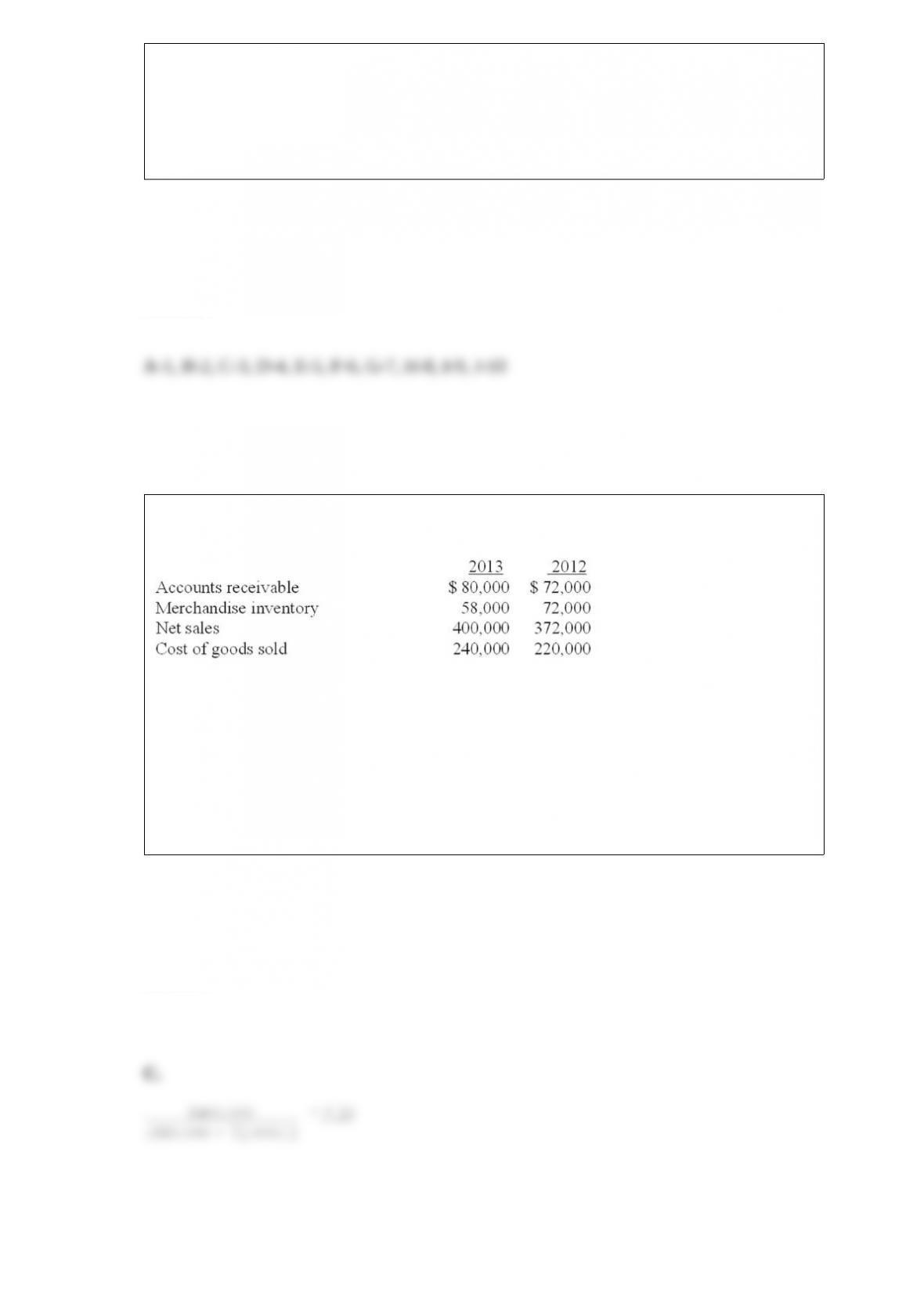

Excerpts from Huckabee Company’s December 31, 2013 and 2012, financial statements

are presented below:

Huckabee’s 2013 receivables turnover (rounded) is: A. 3.69.

B. 5.00.

C. 5.26.

D. 3.16.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1) Recognition

2) Consistency

3) Cost-effectiveness

4) Comparability

5) Neutrality

A. Accounting information should be unbiased.

B. Important in analysis between firms.

C. Applying the same accounting practices over time.

D. Considers the value of using information relative to cost of providing it.

E. The decision to include an amount in the financial statements.

Answer:

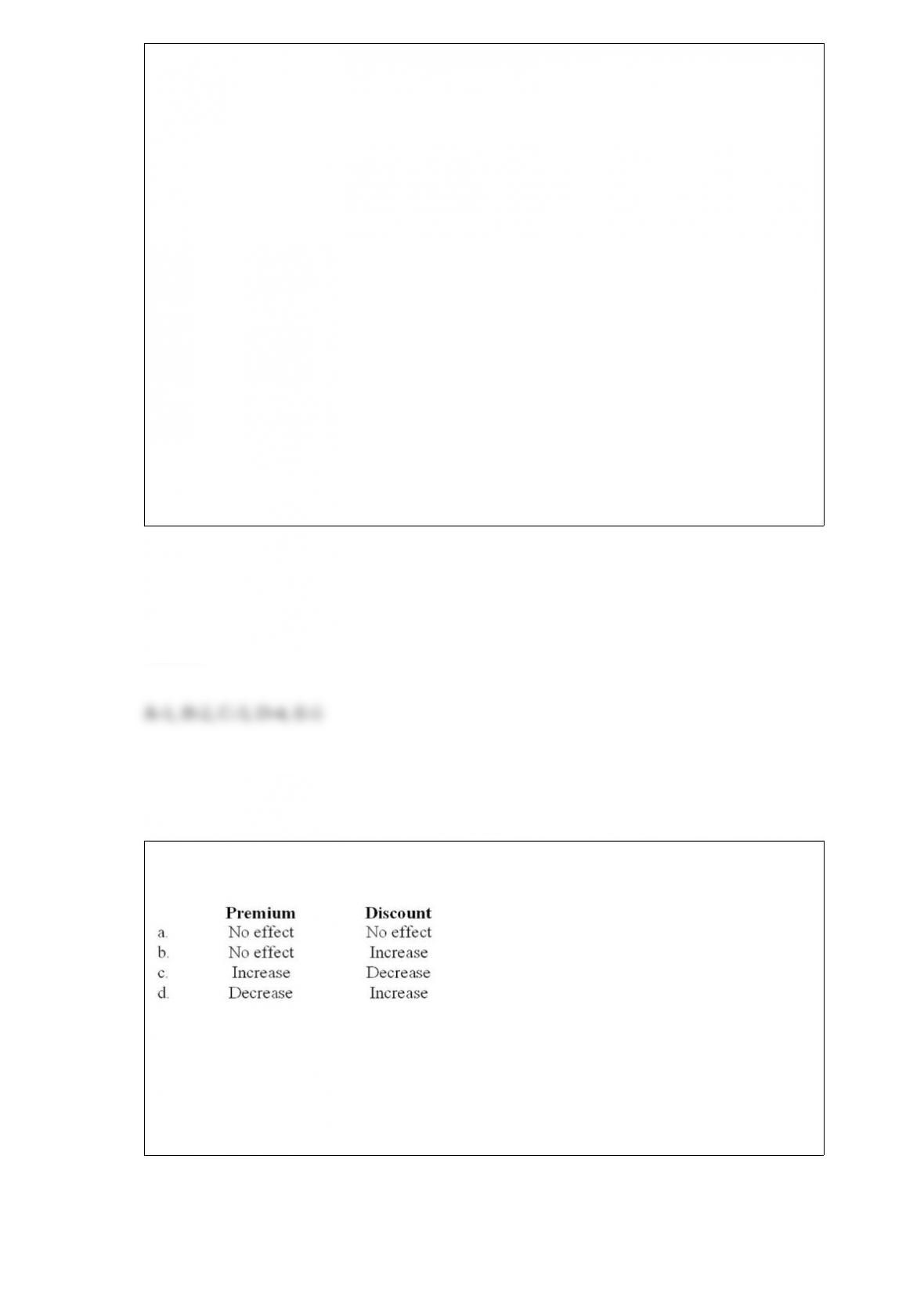

How would the carrying value of bonds payable be affected by the amortization of each

of the following?

A. Option a

B. Option b

C. Option c

D. Option d

Answer:

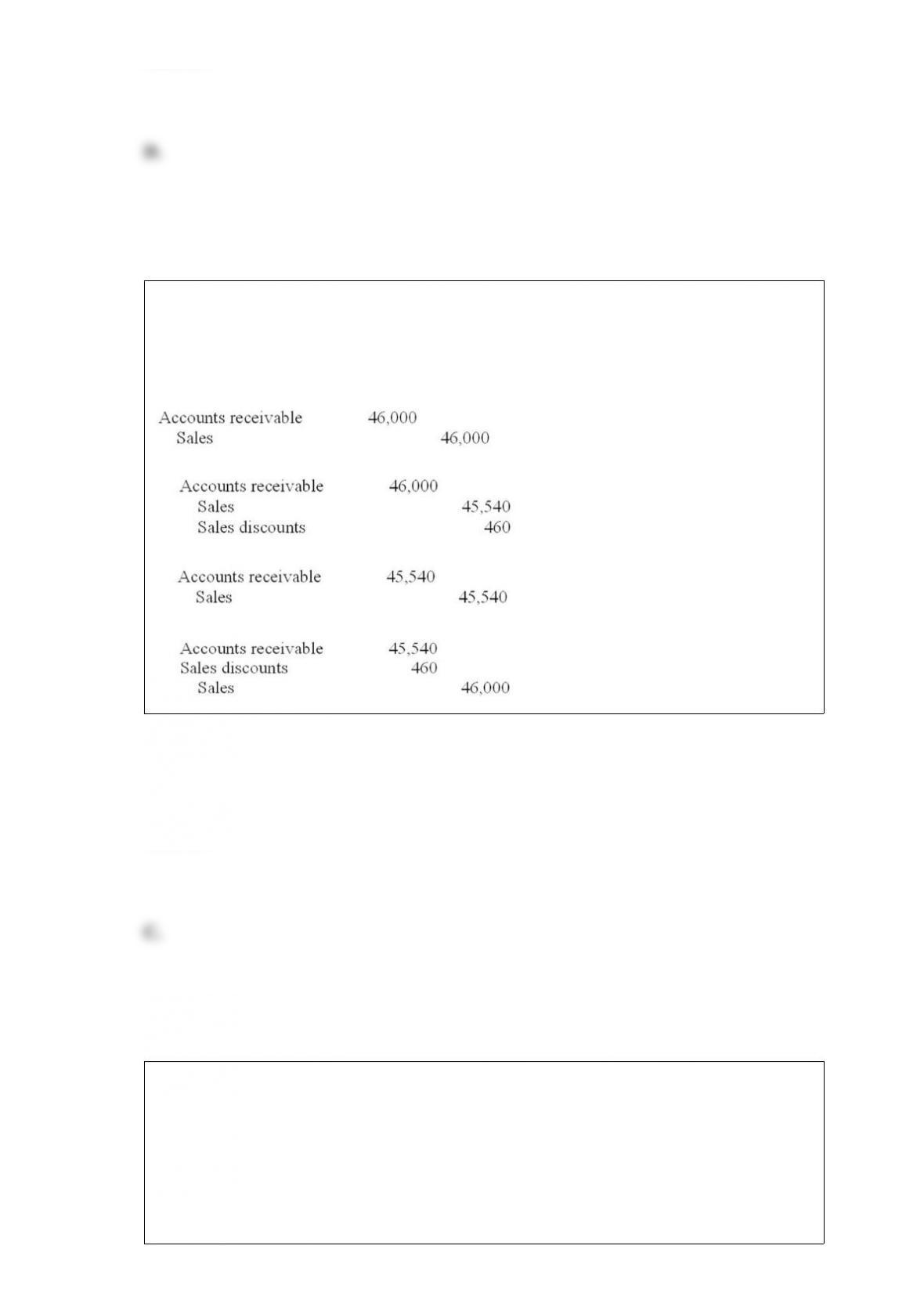

Harvey’s Wholesale Company sold supplies of $46,000 to Northeast Company on April

12 of the current year, with terms 1/15, n/60. Harvey uses the net method of accounting

for cash discounts.

What entry would Harvey’s make on April 12? A.

B.

C.

D.

Answer:

Pension benefits and postretirement health benefits typically are similar in their: A.

Application of present value concepts.

B. Vesting policies.

C. Coverage for eligible dependents.

D. Relationship between cost of coverage and length of service.

Answer:

“Condorsement”: A.Is a term used by the IASB to refer to the conditional endorsement

process used by the EU with respect to IFRS.

B.Describes a combination of convergence and endorsement that the SEC suggested the

United States might use in the future to incorporate IFRS into U.S. GAAP.

C.Was coined by a representative of the AICPA to describe the lengthy convergence

process.

D.Has nothing to do with the convergence process.

Answer:

B Corp. has a debt/equity ratio of 2 to 1. Not including any indirect effects on earnings,

the debt/equity ratio is increased when B records:

A. Option a

B. Option b

C. Option c

D. Option d

Answer:

A company reported interest expense of $540,000 for the year. Interest payable was

$35,000 and $75,000 at the beginning and the end of the year, respectively. What was

the amount of interest paid? A. $580,000.

B. $615,000.

C. $500,000.

D. $575,000.

Answer:

In a period when costs are rising and inventory quantities are stable, the inventory

method that would result in the highest ending inventory is: A. Weighted average.

B. Moving average.

C. FIFO.

D. LIFO.

Answer:

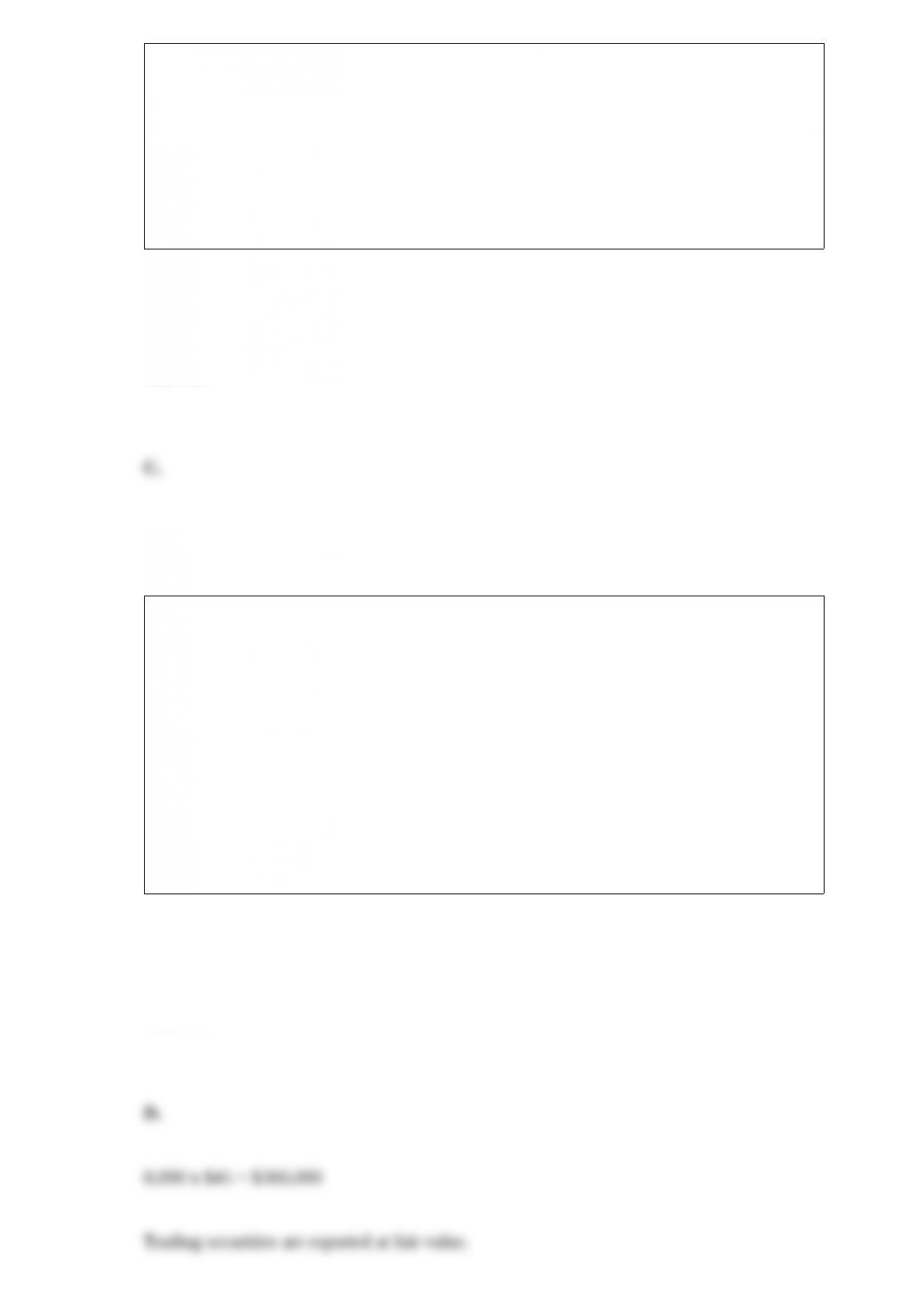

On January 1, 2013, Nana Company paid $100,000 for 8,000 shares of Papa Company

common stock. These securities were classified as trading securities. The ownership in

Papa Company is 10%. Papa reported net income of $52,000 for the year ended

December 31, 2013. The fair value of the Papa stock on that date was $45 per share.

What amount will be reported in the balance sheet of Nana Company for the investment

in Papa at December 31, 2013? A. $284,400.

B. $300,000.

C. $315,600.

D. $360,000.

Answer:

A major expenditure increased a truck’s life beyond the original estimate of life. GAAP

permits the expenditure to be debited to: A. Repairs.

B. Accumulated depreciation.

C. Major repairs.

D. None of the above.

Answer:

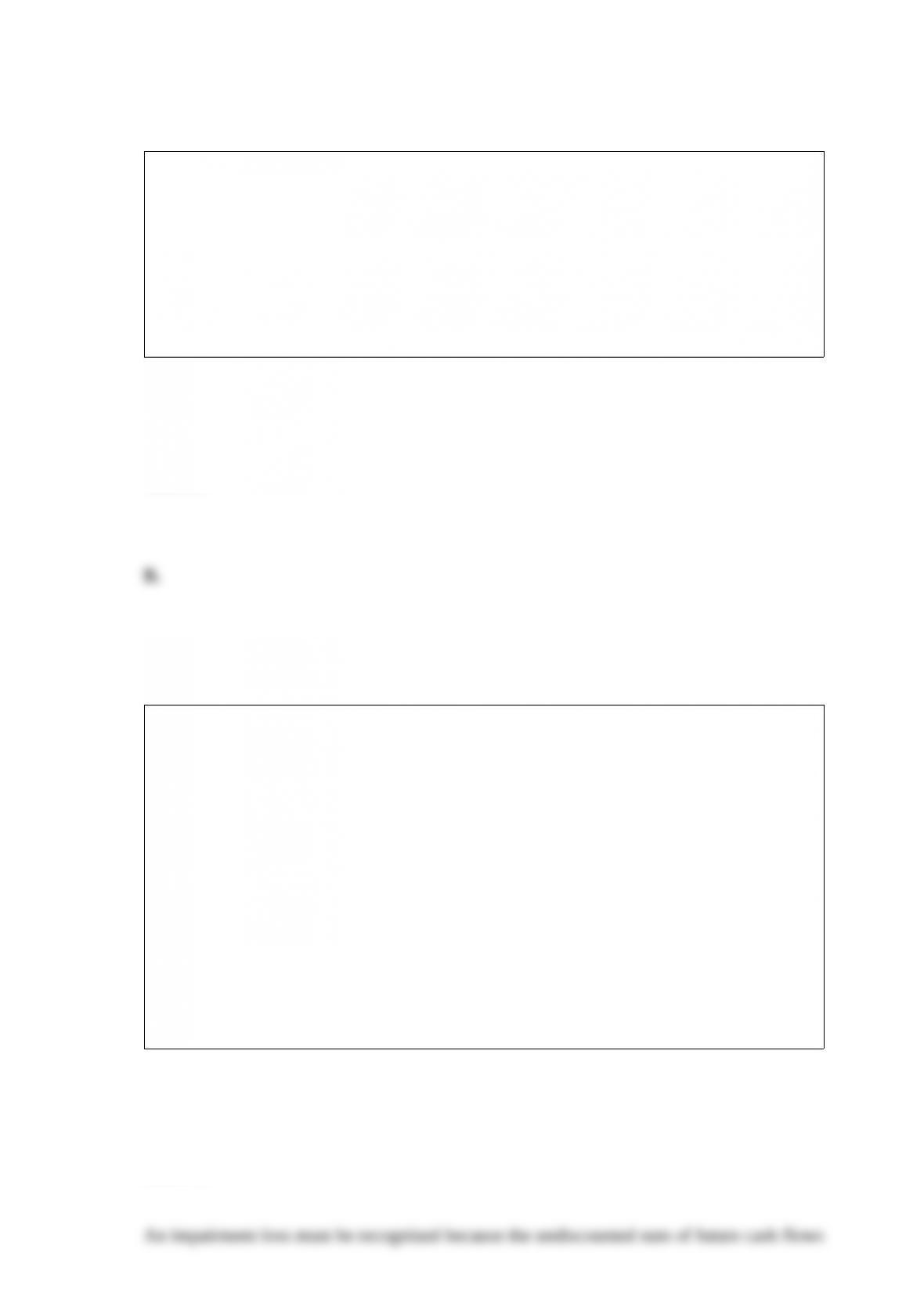

El Dorado Foods Inc. owns a chain of specialty stores in the Pacific Northwest.

Recently, four of the stores have experienced declining profits due to market saturation

in the area. As a result, management gathered data about possible impairment of the

assets of the stores. The information gathered was as follows:

Book value: $17.5 million

Fair value: $14.9 million

Undiscounted sum of future cash flows: $16.5 million

Required:

Determine the amount, if any, of the impairment loss that El Dorado must recognize on

these assets.

Answer:

If the fair value of a trading security declines for a reason that is viewed as “other than

temporary”: A. The investment is not written down to fair value.

B. The investment is written down to fair value, and an “impairment loss” is recognized

in net income.

C. The investment is written down to fair value, and the impairment loss is recognized

in accumulated other comprehensive income.

D. The investment is treated the same way it would be treated if the decline in fair value

was viewed as temporary.

Answer:

Which of the following does not pertain to accounting for asset retirement obligations?

A. They accrete (increase over time) at the company’s credit-adjusted risk-free rate.

B. They must be recognized according to GAAP.

C. Statement of Financial Accounting Concepts No. 7 is applied when adjusting cash

flow obligations for uncertainty.

D. All of the above pertain to accounting for asset retirement obligations.

Answer:

Gains on the cash sales of fixed assets: A. Are the excess of the book value over the

cash proceeds.

B. Are part of cash flows from operations.

C. Are reported on a net-of-tax basis if material.

D. Are the excess of the cash proceeds over the book value of the assets sold.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Accruals

2)Adjusted trial balance

3)Prepayments

4)Post-closing trial balance

5)Unadjusted trial balance

A. Assets or liabilities created when cash flows precede recognition.

B. A list of only permanent accounts and their balances prepared to show that the

accounting equation is in balance.

C. Assets or liabilities created when recognition precedes cash flows.

D. A list of accounts and their balances prepared before the effects of internal

transactions are recorded.

E. A list of accounts and balances containing the source data for preparation of financial

statements.

Answer:

The cumulative effect of most changes in accounting principle is reported: A. In the

income statement between extraordinary items and net income.

B. In the income statement after income and before income tax.

C. In the income statement between discontinued operations and extraordinary items.

D. In the balance sheet accounts affected.

Answer:

An amortization schedule for bonds issued at a premium: A. Summarizes the

amortization of the premium, a contra-asset account with a credit balance.

B. Is reported in the balance sheet.

C. Is a schedule that reflects the changes in the debt over its term to maturity.

D. All of the above are correct.

Answer:

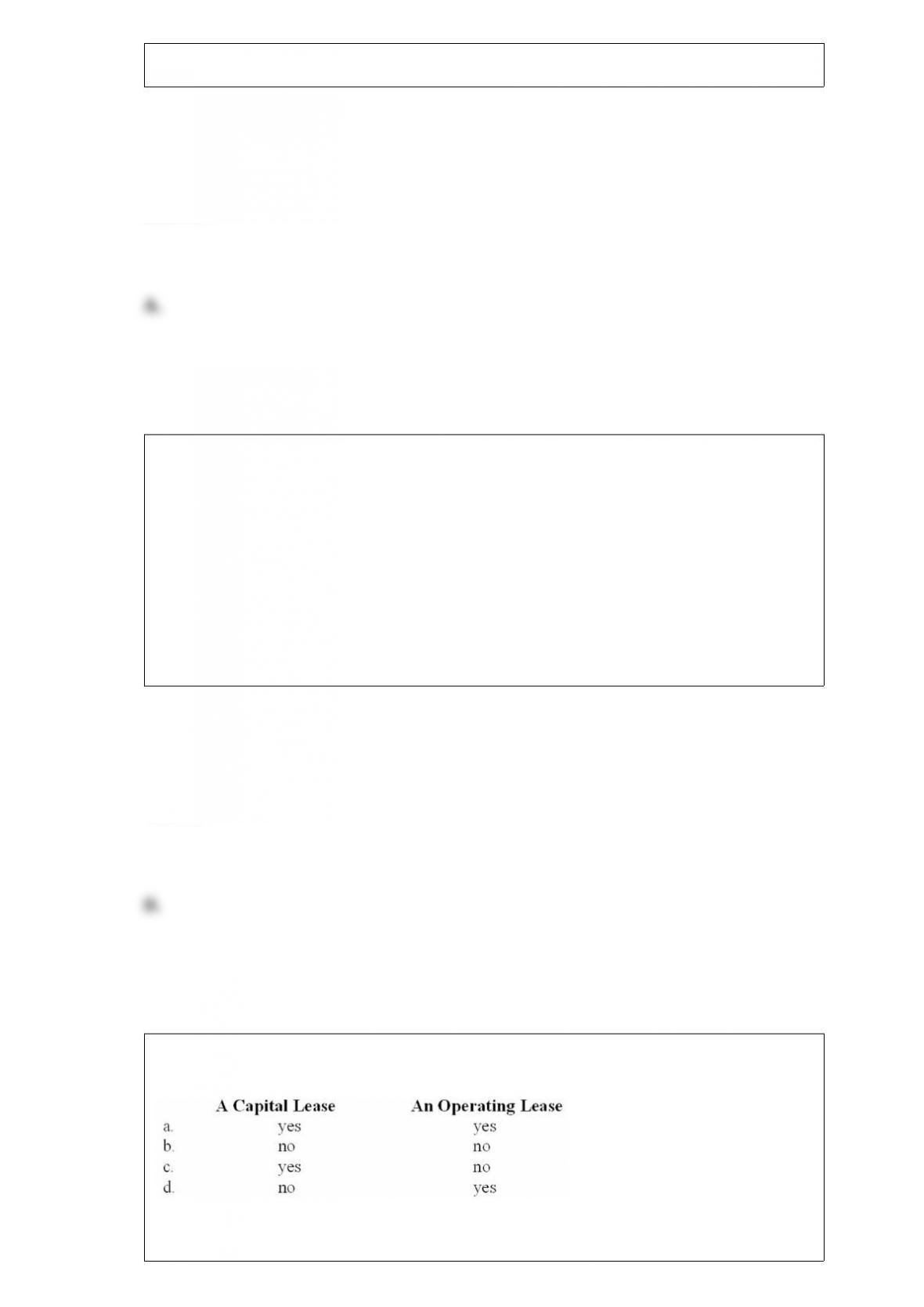

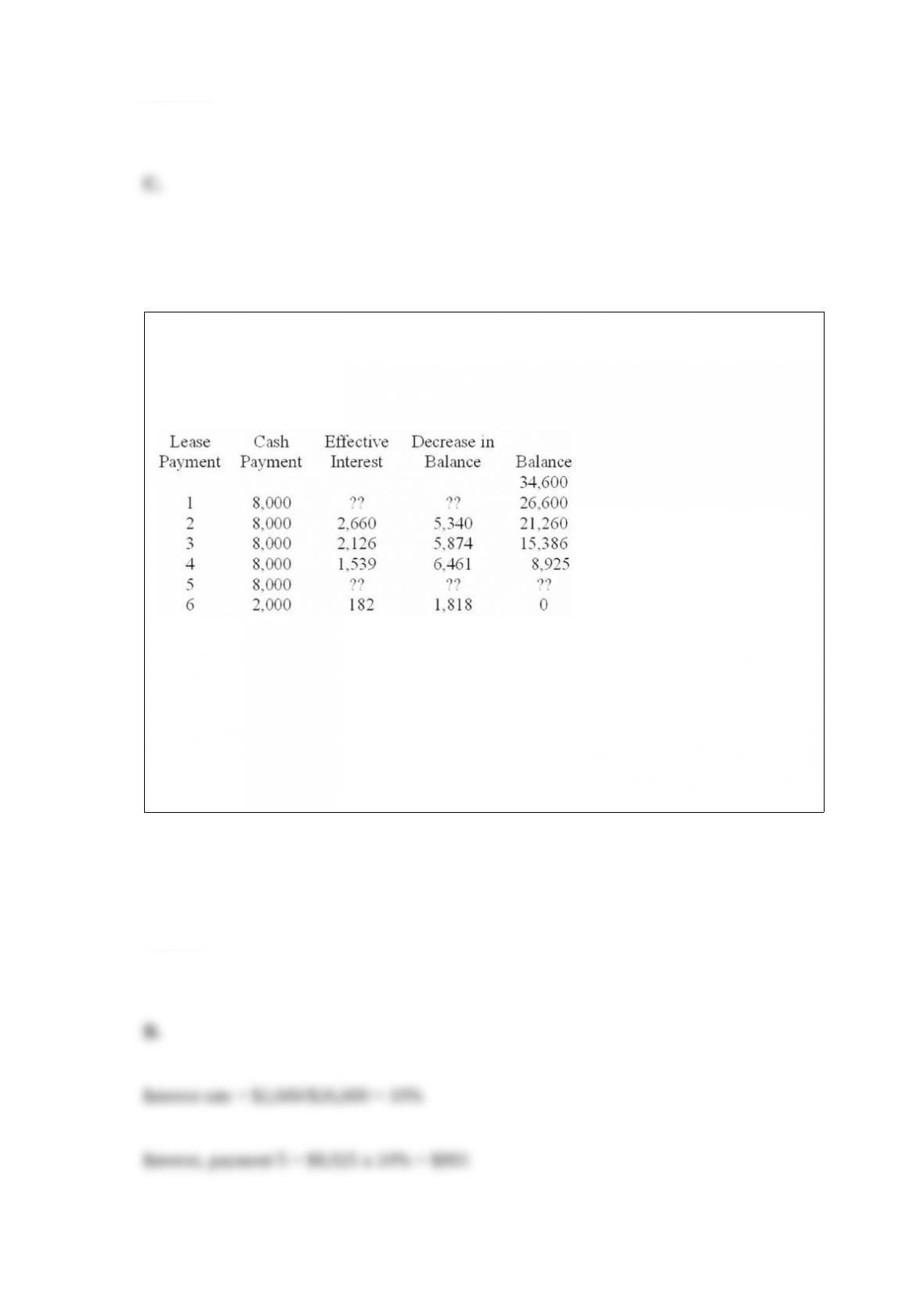

Refer to the following lease amortization schedule. The five payments are made

annually starting with the inception of the lease. A $2,000 bargain purchase option is

exercisable at the end of the five-year lease. The asset has an expected economic life of

eight years.

What would be the amount of interest expense recorded with payment 5? A. $2,000.

B. $893.

C. $7,107.

D. $1,107.

Answer:

Temporary accounts would not include: A. Salaries payable.

B. Depreciation expense.

C. Supplies expense.

D. Cost of goods sold.

Answer:

An extraordinary event for financial reporting purposes is both: A. Unusual and

material.

B. Infrequent and significant.

C. Material and infrequent.

D. Unusual and infrequent.

Answer:

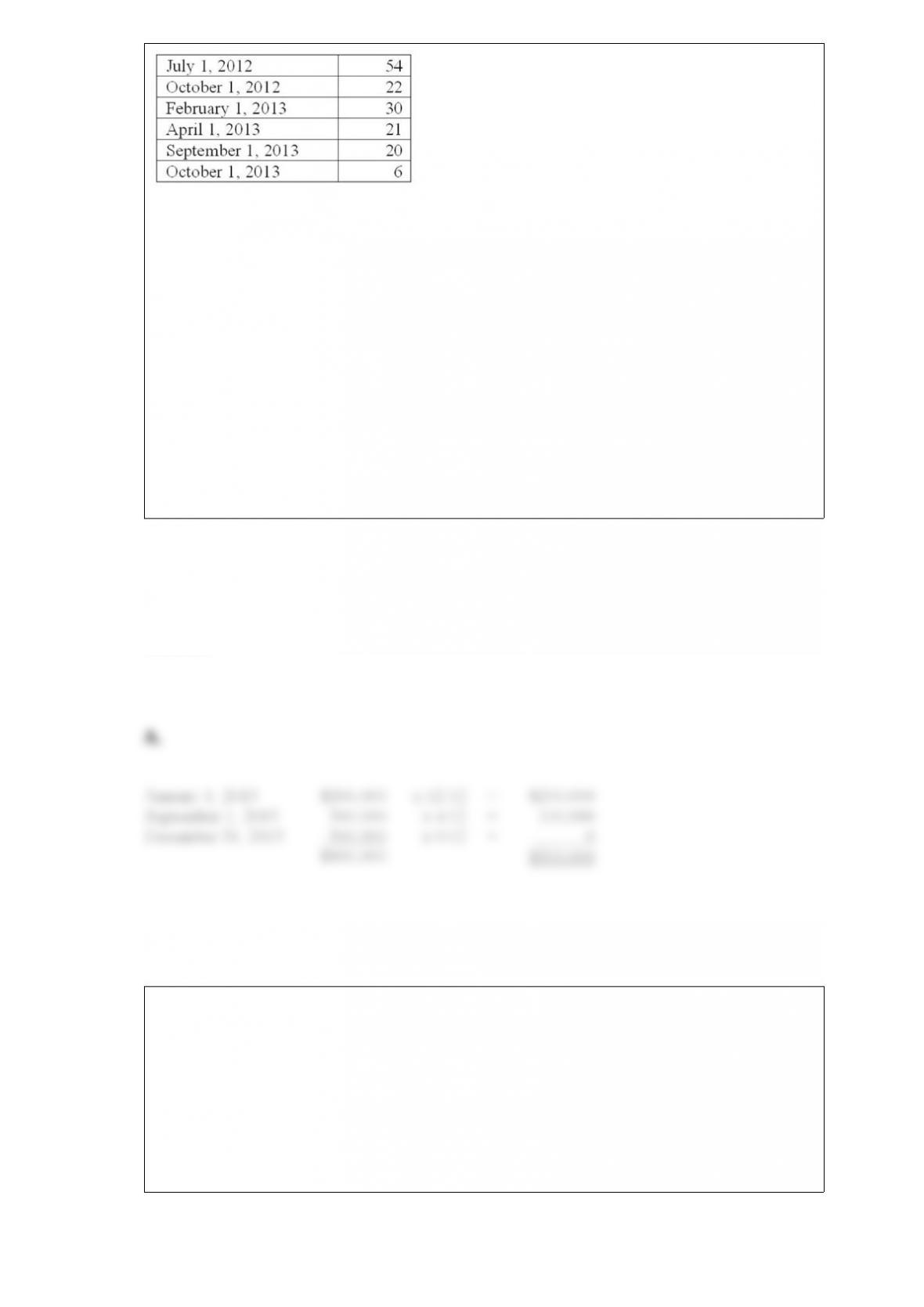

On June 1, 2012, the Crocus Company began construction of a new manufacturing

plant. The plant was completed on October 31, 2013. Expenditures on the project were

as follows ($ in millions):

On July 1, 2012, Crocus obtained a $70 million construction loan with a 6% interest

rate. The loan was outstanding through the end of October, 2013. The company’s only

other interest-bearing debt was a long-term note for $100 million with an interest rate of

8%. This note was outstanding during all of 2012 and 2013. The company’s fiscal

year-end is December 31.

Average accumulated expenditures for 2013 was: A. $300,000.

B. $350,000.

C. $500,000.

D. $400,000.

Answer:

Disclosure notes to a company’s financial statements: A.Are relatively unimportant facts

that don’t belong in the basic financial statements.

B.Document the source of financial statement facts, like literary footnotes.

C.Are an integral part of a company’s financial statements.

D.Are irrelevant facts that are immaterial in amount.

Answer:

A company’s investment in receivables is influenced by several variables, including: A.

The level of sales.

B. The nature of the product or service sold.

C. The credit and collection policies.

D. All of the above are correct.

Answer:

El Dorado Foods Inc. owns a chain of specialty stores in the Pacific Northwest.

Recently, four of the stores have experienced declining profits due to market saturation

in the area. As a result, management gathered data about possible impairment of the

assets of the stores. The information gathered was as follows:

Book value: $17.5 million

Fair value: $14.9 million

Undiscounted sum of future cash flows: $16.5 million

Required:

Assume that the undiscounted sum of future cash flows is $18.2 million, instead of

$16.5 million. Determine the amount, if any, of the impairment loss that El Dorado

must recognize on these assets.

Answer:

Suppose that the Footwear Division’s assets had not been sold by December 31, 2013,

but were considered held for sale. Assume that the fair value of these assets at

December 31 was $40 million. In the 2013 income statement for Foxtrot Co., it would

report a loss from discontinued operations of:A. $3 million loss.

B. $10 million loss.

C. $10.8 million loss.

D. $18 million loss.

Answer:

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the correct term. 1) Book value method

2) Warrants

3) Induced conversion

4) Straight-line method

5) Zero-coupon bonds

A. Additional consideration is recorded as an expense

B. No gain or loss recorded when convertible bond option is exercised

C. Often traded separately from associated bonds

D. Requires(s) no cash outflow before maturity.

E. A practical expediency when not misleading

Answer:

The purpose of closing entries is to transfer:A. Accounts receivable to retained earnings

when an account is fully paid.

B. Balances in temporary accounts to a permanent account.

C. Inventory to cost of goods sold when merchandise is sold.

D. Assets and liabilities when operations are discontinued.

Answer:

S Corp. has a rate of return on assets of 10% and a debt/equity ratio of 2 to 1. Not

including any indirect effects on earnings, the immediate impact of recording a capital

lease on these ratios is a(an):

A. Option a

B. Option b

C. Option c

D. Option d

Answer: