IBM and AT&T decide to swap $1 million loans. IBM currently pays 9.0% fixed and

AT&T pays 8.5% on a LIBOR + 0.5% loan. What is the net cash flow for IBM if they

swap their fixed loan for a LIBOR + 0.5% loan and LIBOR rises to 8.5%?

A) -$50,000

B) $50,000

C) -$90,000

D) 0

A stock is selling for $41.60. The strike price on a call, maturing in 6 months, is $45.

The possible stock prices at the end of 6 months are $35.00 and $49.00. Interest rates

are 5.0%. Given an under-priced option, what are the short sale proceeds in an arbitrage

strategy?

A) $6.36

B) $8.22

C) $10.43

D) $11.89

If next year’s bond prices for 3-year zero coupon bonds may be either 0.8923 or 0.8644,

what is the yield volatility?

A) 12.7%

B) 13.7%

C) 14.7%

D) 15.7%

The underlying stock for a European exchange option has S = $27.15, div = 2.0%, and

σ = 0.18. The strike stock has S = $30.00, div = 0.0%, and σ = 0.22. The two stocks

have a correlation coefficient of 0.73. If the exchange option expires in 2 years, what is

the price of the call using a Black-Scholes approach?

A) $0.88

B) $0.98

C) $1.09

D) $1.19

Which of the following situations does NOT describe someone who should implement a

hedge strategy?

A) Mary is very nervous about losing profits if selling prices drop

B) Melanie’s creditors will not lend her money if her crops might lose money

C) Katherine’s board of directors will not tolerate losses, even if it means profits are

smaller

D) Dawn wants to reduce price fluctuations, but will need to conduct many transactions

to achieve her goals

Your $2 million portfolio consists of 25% Evans stock with = 0.16, σ = 0.22 and 75%

Indy stock with = 0.09, σ = 0.12. The correlation coefficient is 0.65. What is the

value at risk over 1 day at a 99% confidence level? Assume 252 days per year.

A) $27,976

B) $37,976

C) $47,976

D) $57,976

Use VaR techniques to determine the cost of insurance on a risky investment. The

investment asset has a value of $150 and pays no dividend. The historical standard

deviation of the asset is 20% and the expected return on the asset is 15%. At the 95%

confidence level, what is the price of a put option that insures the asset over the next 6

months?

A) $0.33

B) $1.25

C) $2.65

D) $6.56

In what option does it benefit to simulate the path of potential asset prices?

A) Barrier

B) European

C) Asian

D) A and C

Mead, Inc. may invest $20 million in a new fiber optic project. Due to market

conditions, annual production costs and revenues are forecasted at $10 million and $8

million, respectively, starting next year. Revenues are expected to grow at 4.0% and

interest rates are 6.0%. What is the change in value if the project is commenced in 5

years instead of today? (Use static analysis.)

A) $8.84 million

B) $10.84 million

C) $12.84 million

D) $14.84 million

A stock is valued at $28.00. The annual expected return is 9.0% and the standard

deviation of annualized returns is 19.0%. If the stock is lognormally distributed, what is

the expected median stock price after 4 years?

A) $28.00

B) $32.33

C) $40.13

D) $54.60

Assume S = $43, K = 45, div = 0.0, r = 0.09, σ = 0.36, and 90 days until expiration.

What is the premium on an Asian average strike put where N = 3?

A) $0.26

B) $0.36

C) $0.46

D) $0.56

A call option has an exercise price of $30. The stock price at a point on the binomial

tree is $36.24. The calculated present value of the option at that same point is $5.86.

What figure should be used to calculate option prices at points moving toward the final

price?

A) $5.86

B) $6.24

C) $6.62

D) $7.01

A modification to the Brownian process that permits mean reversion is called:

A) Ornstein-Uhlenbeck

B) Diffusion

C) Ito

D) Geometric

A stock is selling for $53.20. Interest rates are 6.0% and the returns on the stock have a

standard deviation of 24.0%. What is the forecasted up movement in the stock over a

6-month interval?

A) $64.96

B) $69.69

C) $73.48

D) $76.96

The primary link between Brownian motion and Girsanov’s theorem relates to which

variable?

A) Drift

B) Numeraire

C) Returns

D) Standard deviation

Assume S = $56.00, σ = 0.45, r = 0.05, div = 0.0, on a $55 strike call and 45 days until

expiration. Given delta = 0.6253, gamma = 0.0735, and theta = -0.0253, what is the

approximate change in call price over 1 day, all else being the same?

A) $0.00

B) $0.01

C) $0.02

D) $0.03

Assume oil prices rise dramatically and the spot price of oil is $230 per barrel and the

3-year forward price is $245. Annualized 1-year, 2-year, and 3 year interest rates are

4.2%, 4.4%, and 4.6%, respectively. For a commodity-linked note to sell at par, what is

the annual coupon?

A) $6.00

B) $16.00

C) $26.00

D) $36.00

Assume that you open a 100-share short position in Jiffy, Inc. common stock at the

bid-ask price of $32.00 – $32.50. When you close your position, the bid-ask prices are

$32.50 – $33.00. If you pay a commission rate of 0.5%, what is your profit or loss on

the short investment?

A) $32.50 gain

B) $16.25 loss

C) $132.50 loss

D) $100.00 gain

Select the family member who is offering the most diversification to the rest of the

family.

A) Dad works for General Motors

B) Mom works for Goodyear

C) Daughter works for Jiffy Lube

D) Son works for Eli Lilly & Company

Given a mean of 45 and a standard deviation of 32 from a normally distributed sample,

what is the probability of an observation being between 35 and 75?

A) 0.35

B) 0.45

C) 0.55

D) 0.65

The annual coupon rate on a 1-year treasury bond is 5.5%. The coupon on a 2-year

treasury bond is 5.8%. What is the implied YTM on a hypothetical 2-year zero coupon

treasury bond?

A) 5.45%

B) 5.50%

C) 5.75%

D) 5.81%

All of the following are financially engineered products, except:

A) Mortgage

B) Mortgage backed security

C) Interest only

D) Principal only

Using base 100 pricing, the price of bonds that mature in years 1, 2, and 3 is 101.92,

100.87, and 99.34, respectively. Given this data, what is the 2-year forward price for a

1-year bond?

A) 98.48

B) 99.34

C) 100.22

D) 100.87

Assume that a $50 strike call pays a 2.0% continuous dividend, r = 0.07, σ = 0.25, and

the stock price is $48.00. What is the profit or loss, per share, for a short call position if

the option expires in 60 days and the price rises to $50.00 after 5 days?

A) $0.84 gain

B) $0.84 loss

C) $0.95 gain

D) $0.95 loss

Assume that you purchase 100 shares of Jiffy, Inc. common stock at the bid-ask prices

of $32.00 – $32.50. When you sell, the bid-ask prices are $32.50 – $33.00. If you pay a

commission rate of 0.5%, what is your profit or loss?

A) $0

B) $16.25 loss

C) $32.50 gain

D) $32.50 loss

What is the boundary condition for a European call option?

A) Max [0,S(T)-K]

B) Max [0,K-S(T)]

C) Min [0,S(T)-K]

D) Min [0,K-S(T)]

James, Inc. has zero-coupon outstanding debt maturing in 8 years. In rank of seniority,

each pays at maturity $20 million, $15 million, and $40 million. Assume asset value =

$60 million,

r = 0.05, σ = 0.28, and no dividend is paid. What is the yield on the $15 million

subordinate debt?

A) 5.72%

B) 6.72%

C) 7.72%

D) 8.72%

At the 6-month point, what is the breakeven index price for a strategy of longing the

market index at a price of 830? Interest rates are 0.5% per month.

A) $802.12

B) $830.00

C) $855.21

D) $866.32

Bonds maturing in 1, 2, and 3 years have prices of 0.9600, 0.9153 and 0.8620,

respectively. A 0.9300 strike call on a 1-year bond matures in 1 year with σ = 0.20.

What is the price of an 8.0% interest rate caplet that expires in 1 year?

A) $0.66

B) $0.76

C) $0.86

D) $0.96

What statistic is used to determine the accuracy of a Monte Carlo simulation?

A) Mean

B) Standard deviation

C) Covariance

D) Correlation coefficient

Suppose S = $52.50, K = $50, σ = 0.25, r = 0.04 and div = 0.01. What is the price of a

gap option with 156 days until expiration and K1 = $32.00?

A) $14.00

B) $15.00

C) $16.00

D) $17.00

An investor wants to hold 200 euro two years from today. The spot exchange rate is

$1.31 per euro. If the euro denominated annual interest rate is 3.0% what is the price of

a currency prepaid forward?

A) $200

B) $206

C) $231

D) $247

How does a reload option provide additional compensation compared to regular

compensation options?

Why should or should not a company expense compensation options?

What is the primary difference between ARCH models and GARCH models?

How is duration calculated? What is the nature and use of duration? How does duration

compare to the linear concept of the bond price and interest rate relationship? Is

duration better than convexity or worse?

Explain the impact transaction costs have on the ability to make arbitrage profits in

forward and futures markets.

What are the similarities and differences between bear and bull spreads?

As with Chrysler Corp. many years ago, the government occasionally guarantees loans.

What option is the government granting and to whom in a loan guarantee?

What assumption is made in the Black-Scholes model concerning volatility?

What are the two ways that the payoff conditional on default can be expressed?

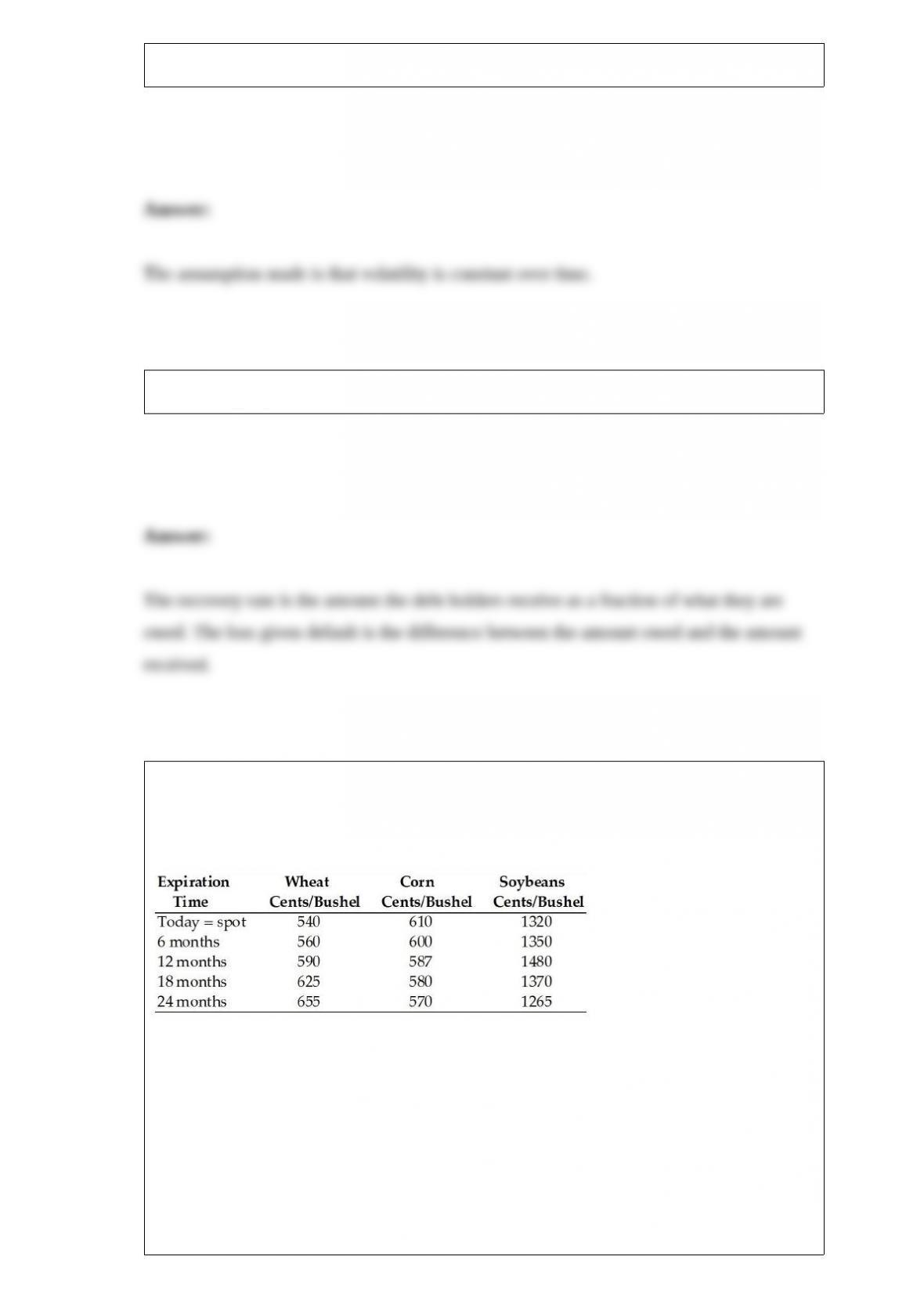

When answering the questions below, refer to the following table of commodity

forward and spot prices. The annual risk free interest rate is 4.0%.

Table 6.1

Refer to the table 6.1. What is the approximate annualized lease rate on the 12-month

corn forward contract?

A) 0.00%

B) 2.25%

C) 3.92%

D) 7.84%

How does a coupon bond differ from an equity-linked bond?

What is the relationship between dividends and the forecasted stock price in a binomial

model?