Version 1 1

Student name:__________

1) Suppose the U.S. dollar substantially depreciates against the Japanese yen. The change in

exchange rate

A) can have significant economic consequences for U.S. firmsonly.

B) can have significant economic consequences for Japanese firmsonly.

C) can have significant economic consequences for both U.S. and Japanese firms.

D) none of the options

2) Suppose the U.S. dollar substantially depreciates against the Japanese yen. The change in

exchange rate

A) will tend to weaken the competitive position of import-competing U.S. car makers.

B) will tend to strengthen the competitive position of import-competing U.S. car

makers.

C) will tend to strengthen the competitive position of Japanese car makers at the

expense of U.S. makers.

D) none of the options

3) The link between a firm’s future operating cash flows and exchange rate fluctuations is

A) asset exposure.

B) operating exposure.

C) asset exposure and operating exposure.

D) none of the options

4) When the Mexican peso collapsed in 1994, declining by 37 percent,

Version 1 2

A) U.S. firms that exported to Mexico and priced in pesos, but not dollars, were

adversely affected.

B) U.S. firms that exported to Mexico and priced in dollars, but not pesos were

adversely affected.

C) U.S. firms were unaffected by the peso collapse, since Mexico is such a small

market.

D) U.S. firms that exported to Mexico and priced in peso were adversely affected, and

U.S. firms that exported to Mexico and priced in dollars were adversely affected.

5) When exchange rates change,

A) U.S. firms that produce domestically and sell only to domestic customers will be

unaffected.

B) U.S. firms that produce domestically and sell only to domestic customers can be

affected if they compete against imports.

C) U.S. firms that produce domestically and sell only to domestic customers will be

affected, but only if they borrow in foreign currency to finance their domestic operations.

D) U.S. firms that produce domestically and sell only to domestic customers will be

unaffected, and U.S. firms that produce domestically and sell only to domestic customers can be

affected if they compete against imports.

6) When exchange rates change,

A) this can alter the operating cash flow of a domestic firm.

B) this can alter the competitive position of a domestic firm.

C) this can alter the home currency values of a multinational firm’s assets and liabilities.

D) all of the options

7) Two studies found a link between exchange rates and the stock prices of U.S. firms;

Version 1 3

A) this suggests that exchange rate changes can systematically affect the value of the

firm by influencing its operating cash flows.

B) this suggests that exchange rate changes can systematically affect the value of the

firm by influencing the domestic currency values of its assets and liabilities.

C) this suggests that exchange rate changes can systematically affect the value of the

firm by influencing its operating cash flows, as well influencing the domestic currency values of

its assets and liabilities.

D) none of the options

8) It is conventional to classify foreign currency exposures into the following types:

A) economic exposure, transaction exposure, and translation exposure.

B) economic exposure, noneconomic exposure, and political exposure.

C) national exposure, international exposure, and trade exposure.

D) conversion exposure, and exchange exposure.

9) Exposure to currency risk can be measured by the sensitivities of

A) the future home currency values of the firm’s assets and liabilitiesonly.

B) the firm’s operating cash flows to random changes in exchange ratesonly.

C) the future home currency values of the firm’s assets and liabilities, as well as the

firm’s operating cash flows to random changes in exchange rates.

D) none of the options

10) Operating exposure measures

Version 1 4

A) the extent to which the foreign currency value of the firm’s assets is affected by

unanticipated changes in exchange rates.

B) the extent to which the firm’s operating cash flows will be affected by unexpected

changes in exchange rates.

C) the effect of changes in exchange rates will have on the consolidated financial reports

of a MNC.

D) the effect of unanticipated changes in exchange rates on the dollar value of

contractual obligations denominated in a foreign currency.

11) Economic exposure refers to

A) the sensitivity of realized domestic currency values of the firm’s contractual cash

flows denominated in foreign currencies to unexpected exchange rate changes.

B) the extent to which the value of the firm would be affected by unanticipated changes

in exchange rate.

C) the potential that the firm’s consolidated financial statement can be affected by

changes in exchange rates.

D) ex post and ex ante currency exposures.

12) Currency risk

A) is the same as currency exposure.

B) represents random changes in exchange rates.

C) measure “what the firm has at risk.”

D) is the same as currency exposure and represents random changes in exchange rates.

13) Suppose a U.S.-based MNC maintains a vacation home for employees in the British

countryside and the local price of this property is always moving together with the pound price

of the U.S. dollar. As a result,

Version 1 5

A) whenever the pound depreciates against the dollar, the local currency price of this

property goes up by the same proportion.

B) the firm is not exposed to currency risk even if the pound–dollar exchange rate

fluctuates randomly.

C) whenever the pound depreciates against the dollar, the local currency price of this

property goes up by the same proportion. Additionally, the firm is not exposed to currency risk

even if the pound–dollar exchange rate fluctuates randomly.

D) none of the options

14) The exposure coefficient in the regression P = a + b × S + e is given by

A)

B) P = a + b × S + e

C)

D) none of the options

15) <p>The exposure coefficient in the regression P = a + b × S + e is

A) a measure of how a change in the exchange rate affects the dollar value of a firm’s

assets.

B) a value of zero if the value of the firm’s assets is perfectly correlated with changes in

the exchange rate.

C) a measure of how a change in the exchange rate affects the dollar value of a firm’s

assets, and has a value of zero if the value of the firm’s assets is perfectly correlated with changes

in the exchange rate.

D) none of the options

16) <p>The exposure coefficient in the regression P = a + b × S + e informs

Version 1 6

A) how much of a foreign currency to sell forward.

B) the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate.

C) captures the residual part of the dollar value variability that is independent of

exchange rate movements.

D) how many call options to write.

17) Before you can use the hedging strategies such as a forward market hedge, options

market hedge, and so on, you should consider running a regression of the form P = a + b × S + e .

When reviewing the output, you should initially focus on

A) the intercept a.

B) the slope coefficient b.

C) mean square error, MSE.

D) R2.

18) The link between the home currency value of a firm’s assets and liabilities and exchange

rate fluctuations is

A) asset exposure.

B) operating exposure.

C) asset exposure and operating exposure.

D) none of the options

19) A purely domestic firm that sources and sells only domestically,

Version 1 7

A) faces exchange rate risk to the extent that it has international competitors in the

domestic market.

B) faces no exchange rate risk.

C) should never hedge since this could actually increase its currency exposure.

D) faces no exchange rate risk and should never hedge since this could actually increase

its currency exposure.

20) In recent years, the U.S. dollar has depreciated substantially against most major

currencies of the world, especially against the euro.

A) The stronger euro has made many European products more expensive in dollar

terms, hurting sales of these products in the United States.

B) The stronger euro has made many American products less expensive in euro terms,

boosting sales of U.S. products in Europe.

C) The stronger euro has made many European products more expensive in dollar terms,

hurting sales of these products in the United States. Additionally, the stronger euro has made

many American products less expensive in euro terms, boosting sales of U.S. products in Europe.

D) none of the options

21) In recent years,

A) the U.S. dollar has appreciated substantially against most major currencies of the

world, especially against the euro.

B) the U.S. dollar has depreciated substantially against most major currencies of the

world, especially against the euro.

C) the U.S. dollar has maintained its value against most major currencies of the world,

especially against the euro.

D) none of the options

Version 1 8

22) From the perspective of the U.S. firm that owns an asset in Britain, the exposure that can

be measured by the coefficient b in regressing the dollar value P of the British asset on the

dollar–pound exchange rate S using regression equation P = a + b × S + e is

A) asset exposure.

B) operating exposure.

C) accounting exposure.

D) none of the options

23) On the basis of regression equation P = a + b × S + e, we can decompose the variability

of the dollar value of the asset, Var(P), into two separate components:

A) Cov(P,S) = b2 × VAR(P) + VAR(S)

B) VAR(P) = b2 × VAR(S) + VAR(e)

C) Cov(P,S) = b2 × Cov(S,P) + Cov(S,e)

D) VAR(P) = b2 × VAR(S)

24) On the basis of regression equation P = a + b × S + e, we can decompose the variability

of the dollar value of the asset, Var(P), into two separate components: Var(P) = b2 × Var(S) +

Var(e). The first term in the right-hand side of the equation, b2 × Var(S) represents

A) the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate.

B) the residual part of the dollar value variability that is independent of exchange rate

movements.

C) the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate, as well as the residual part of the dollar value variability that is

independent of exchange rate movements.

D) none of the options

Version 1 9

25) On the basis of regression equation P = a + b × S + e, we can decompose the variability

of the dollar value of the asset, VAR(P), into two separate components: VAR(P) = b2 × VAR(S)

+ VAR(e). The second term in the right-hand side of the equation, VAR(e) represents

A) the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate.

B) the residual part of the dollar value variability that is independent of exchange rate

movements.

C) the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate, as well as the residual part of the dollar value variability that is

independent of exchange rate movements.

D) none of the options

26) What does it mean to have redenominated an asset in terms of the dollar?

A) You have undertaken a hedging strategy that gives the asset a constant dollar value.

B) Multiply the foreign currency value of the asset by the spot exchange rate.

C) You have undertaken accounting changes to eliminate translation exposure.

D) none of the options

27) A firm with a highly elastic demand for its products

A) will be unable to pass increased costs following unfavorable changes in the exchange

rate without significantly lowering the quantity sold.

B) will be able to raise prices following unfavorable changes in the exchange rate

without significantly lowering the quantity sold.

C) can easily pass increased costs on to consumers.

D) will sell about the same amount of product regardless of price.

28) Operating exposure can be defined as

Version 1 10

A) the link between the future home currency values of the firm’s assets and liabilities

and exchange rate fluctuations.

B) the extent to which the firm’s operating cash flows would be affected by random

changes in exchange rates.

C) the sensitivity of realized domestic currency values of the firm’s contractual cash

flows denominated in foreign currencies to unexpected exchange rate changes.

D) the potential that the firm’s consolidated financial statement can be affected by

changes in exchange rates.

29) The extent to which the firm’s operating cash flows would be affected by random changes

in exchange rates is called

A) asset exposure.

B) operating exposure.

C) asset exposure or operating exposure.

D) none of the options

30) The variability of the dollar value of an asset (invested overseas) depends on

A) the variability of the dollar value of the asset that is related to random changes in the

exchange rate.

B) the dollar value variability that is independent of exchange rate movements.

C) Both A and B are correct.

D) none of the options

31) Consider a U.S. MNC who owns a foreign asset. If the foreign currency value of the asset

is inversely related to changes in the dollar–foreign currency exchange rate,

Version 1 11

A) the company has no built-in hedge.

B) the dollar value variability that is dependent on exchange rate movements.

C) the company has a built-in hedge and the dollar value variability that is independent

of exchange rate movements.

D) none of the options

32) With regard to operational hedging versus financial hedging,

A) operational hedging provides a more stable long-term approach than does financial

hedging.

B) financial hedging, when instituted on a rollover basis, is a superior long-term

approach to operational hedging.

C) since they both have the same goal, stabilizing the firm’s cash flows in domestic

currency, they are fungible in use.

D) none of the options

33) Which of the following are identified by your text as a strategy for managing operating

exposure?

1. (i) Selecting low-cost production sites

2. (ii) Flexible sourcing policy

3. (iii) Diversification of the market

4. (iv) Product differentiation and R&D efforts

5. (v) Financial Hedging

Version 1 12

A) (i), (iii), and (v) only

B) (ii) and (iv) only

C) (i), (iv), and (v) only

D) all of the options

34) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

2,000

£

2,500

£

3,000

P

$

4,400

$

5,000

$

5,400

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The expected value of the investment in U.S. dollars is

A) $4,950.

B) $3,700.

C) $2,112.50.

D) none of the options

35) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

2,000

£

2,500

£

3,000

Version 1 13

P

$

4,400

$

5,000

$

5,400

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The variance of the exchange rate is:

A) 0.0200

B) 0.10

C) 0.002

D) none of the options

36) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

2,000

£

2,500

£

3,000

P

$

4,400

$

5,000

$

5,400

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The “exposure” (i.e. the regression coefficient beta) is

Hint: Calculate the expression

A) −25,000

B) 2,500

C) −2,500

D) none of the options

Version 1 14

37) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

2,000

£

2,500

£

3,000

P

$

4,400

$

5,000

$

5,400

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following conclusions are correct?

A) Most of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 236,717 ($)2 and 493,751 ($)2

respectively.

B) Most of the volatility of the dollar value of the British asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 236,717 ($)2 and 493,751($)2

respectively.

C) Most of the volatility of the dollar value of the British asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 125,000 ($)2 and −127,500 ($)2

respectively.

D) Most of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 125,000 ($)2 and −127,500 ($)2

respectively.

38) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

Version 1 15

P*

£

2,000

£

2,500

£

3,000

P

$

4,400

$

5,000

$

5,400

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following would be an effective hedge?

A) Sell £2,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

B) Buy £2,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

C) Sell £25,000 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

D) none of the options

39) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The expected value of the investment in U.S. dollars is

A) $5,050

B) $3,700

C) $2,112.50

D) none of the options

Version 1 16

40) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The variance of the exchange rate is

A) 0.0200

B) 0.10

C) 0.002

D) none of the options

41) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

Version 1 17

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The “exposure” (i.e. the regression coefficient beta) is

Hint: Calculate the expression

A) 7,500

B) 2,500

C) −2,500

D) none of the options

42) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following conclusions are correct?

Version 1 18

A) Most of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 1,125,000 ($)2 and 2,500 ($)2

respectively.

B) Most of the volatility of the dollar value of the British asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 236,717 ($)2 and 493,751 ($)2

respectively.

C) Most of the volatility of the dollar value of the British asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 125,000 ($)2 and −127,500 ($)2

respectively.

D) Most of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 125,000 ($)2 and −127,500 ($)2

respectively.

43) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following would be an effective hedge?

A) Sell £7,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

B) Buy £2,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

C) Sell £25,000 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

D) none of the options

Version 1 19

44) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.50

/£

$

2.00

/£

$

1.60

/£

P*

£

1,800

£

2,250

£

2,812.50

P

$

4,500

$

4,500

$

4,500

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The expected value of the investment in U.S. dollars is:

A) $5,050

B) $4,500

C) $2,112.50

D) none of the options

45) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.50

/£

$

2.00

/£

$

1.60

/£

P*

£

1,800

£

2,250

£

2,812.50

P

$

4,500

$

4,500

$

4,500

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The variance of the exchange rate is

Version 1 20

A) 0.0200

B) 0.1019

C) 0.0020

D) none of the options

46) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.50

/£

$

2.00

/£

$

1.60

/£

P*

£

1,800

£

2,250

£

2,812.50

P

$

4,500

$

4,500

$

4,500

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The “exposure” (i.e., the regression coefficient beta) is

Hint: Calculate the expression

A) 7,500

B) 2,500

C) −2,500

D) none of the options

47) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.50

/£

$

2.00

/£

$

1.60

/£

Version 1 21

P*

£

1,800

£

2,250

£

2,812.50

P

$

4,500

$

4,500

$

4,500

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following conclusions are correct?

A) Most of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 0 ($)2 and 0 ($)2 respectively.

B) None of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 0 ($)2and 0 ($)2 respectively.

C) Most of the volatility of the dollar value of the British asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 125,000 ($)2 and −127,500 ($)2

respectively.

D) Most of the volatility of the dollar value of the British asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 125,000 ($)2 and −127,500 ($)2

respectively.

48) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.50

/£

$

2.00

/£

$

1.60

/£

P*

£

1,800

£

2,250

£

2,812.50

P

$

4,500

$

4,500

$

4,500

where,

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following would be an effective hedge?

Version 1 22

A) Sell £2,278.13 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

B) Buy £2,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

C) Sell £25,000 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

D) none of the options

49) A U.S. firm holds an asset in Israel and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

0.30

/IS

$

0.20

/IS

$

0.15

/IS

P*

IS

2,000

IS

5,000

IS

3,000

P

$

600

$

1,000

$

450

where,

P* = Israeli shekel (IS) price of the asset held by the U.S. firm

P = Dollar price of the same asset

The expected value of the investment in U.S. dollars is:

A) $2,083.33

B) $762.50

C) $6,250.00

D) $6,562.50

50) A U.S. firm holds an asset in Israel and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

0.30

/IS

$

0.20

/IS

$

0.15

/IS

P*

IS

2,000

IS

5,000

IS

3,000

Version 1 23

P

$

600

$

1,000

$

4,50

where,

P* = Israeli shekel (IS) price of the asset held by the U.S. firm

P = Dollar price of the same asset

The variance of the exchange rate is:

A) 0.001901

B) 0.002969

C) 0.0039

D) 0.0049

51) A U.S. firm holds an asset in Israel and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

0.30

/IS

$

0.20

/IS

$

0.15

/IS

P*

IS

2,000

IS

5,000

IS

3,000

P

$

600

$

1,000

$

4,50

where,

P* = Israeli shekel (IS) price of the asset held by the U.S. firm

P = Dollar price of the same asset

The “exposure” (i.e., the regression coefficient beta) is:

Hint: Calculate the expression

A) −52.6316

B) 1,289.80

C) 12,898.00

D) none of the options

Version 1 24

52) A U.S. firm holds an asset in Israel and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

0.30

/IS

$

0.20

/IS

$

0.15

/IS

P*

IS

2,000

IS

5,000

IS

3,000

P

$

600

$

1,000

$

4,50

where,

P* = Israeli shekel (IS) price of the asset held by the U.S. firm

P = Dollar price of the same asset

Based on the information provided in Mc. Qu 48, which of the following conclusions are

correct?

A) Most of the volatility of the dollar value of the Israeli asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 236,717 ($)2 and 493,751 ($)2

respectively.

B) Most of the volatility of the dollar value of the Israeli asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 236,717 ($)2 and 493,751 ($)2

respectively.

C) Most of the volatility of the dollar value of the Israeli asset cannot be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 8.22 ($)2 and 59,211 ($)2, respectively.

D) Most of the volatility of the dollar value of the Israeli asset can be removed by

hedging exchange risk because b2[Var(S)] and Var(e) are 8.22 ($)2 and 59,211 ($)2 respectively.

53) A U.S. firm holds an asset in Israel and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

0.30

/IS

$

0.20

/IS

$

0.15

/IS

P*

IS

2,000

IS

5,000

IS

3,000

Version 1 25

P

$

600

$

1,000

$

4,50

where,

P* = Israeli shekel (IS) price of the asset held by the U.S. firm

P = Dollar price of the same asset

Which of the following would be an effective hedge?

A) Sell 53 Israeli shekels forward at the 1-year forward rate, F1($/IS), that prevails at

time zero.

B) Buy 53 Israeli shekels forward at the 1-year forward rate, F1($/IS), that prevails at

time zero.

C) Sell 12,898 Israeli shekels forward at the 1-year forward rate, F1($/IS), that prevails

at time zero.

D) none of the options

54) Find an effective hedge financial hedge if a U.S. firm holds an asset in Great Britain and

faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

Version 1 26

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The CFO runs a regression of the form P = a + b × S + e

The regression coefficient beta is calculated as b =

Where

Cov(P,S) = 0.25 × ($6,600 − $5,050) × ($2.20 − $2.00)

+ 0.50 × ($5,000 − $5,050) × ($2.00 − $2.00)

+ 0.25 × ($3,600 − $5,050) × ($1.80 − $2.00)

Cov(P,S) = 77.50 + 0 + 72.50

Cov(P,S) = 150

b = = 7,500

The variance of the exchange rate is calculated as

E(S) = 0.25 × $2.20 + 0.50 × $2.00 + 0.25 × $1.80

= $.55 + $1 + $.45

= $2.00

VAR(S) = 0.25($2.20 − $2.00)2 + 0.50($2.00 − $2.00)2 + 0.25($1.80 − $2.00)2

= 0.01 + 0 + 0.01

= 0.02

The expected value of the investment in U.S. dollars is:

E[P] = 0.25 × $6,600 + 0.50 × $5,000 + 0.25 × $3,600 = $5,050

Which of the following is the most effective hedge financial hedge?

A) Sell £7,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

B) Buy £7,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

C) Sell £2,500 forward at the 1-year forward rate, F1($/£), that prevails at time zero.

D) 0.25 × £3,000 + 0.50 × £2,500 + 0.25 × £2,000 = £2,500

55) Find an effective hedge financial hedge if a U.S. firm holds an asset in Great Britain and

faces the following scenario:

State 1

State 2

State 3

Version 1 27

Probability

25%

50%

25%

Spot rate

$

2.20

/£

$

2.00

/£

$

1.80

/£

P*

£

3,000

£

2,500

£

2,000

P

$

6,600

$

5,000

$

3,600

P* = Pound sterling price of the asset held by the U.S. firm

P = Dollar price of the same asset

The CFO runs a regression of the form P = a + b × S + e

The regression coefficient beta is calculated as b =

Where

Cov(P,S) = 0.25 × ($6,600 − $5,050) × ($2.20 − $2.00)

+ 0.50 × ($5,000 − $5,050) × ($2.00 − $2.00)

+ 0.25 × ($3,600 − $5,050) × ($1.80 − $2.00)

Cov(P,S) = 77.50 + 0 + 72.50

Cov(P,S) = 150

b = = 7,500

The variance of the exchange rate is calculated as

E(S) = 0.25 × $2.20 + 0.50 × $2.00 + 0.25 × $1.80

= $.55 + $1 + $.45

= $2.00

VAR(S) = 0.25($2.20 − $2.00)2 + 0.50($2.00 − $2.00)2 + 0.25($1.80 − $2.00)2

= 0.01 + 0 + 0.01

= 0.02

The expected value of the investment in U.S. dollars is:

E[P] = 0.25 × $6,600 + 0.50 × $5,000 + 0.25 × $3,600 = $5,050

Suppose that you implement your hedge at F1($/£) = $2/£. Your cash flows in state 1, 2, and 3

respectively will be

Version 1 28

A) $5,100, $5,000, $5,100.

B) $5,100, $5,100, $5,100.

C) $5,000, $5,000, $5,000.

D) none of the options

56) A U.S. firm holds an asset in Great Britain and faces the following scenario:

State 1

State 2

State 3

Probability

25%

50%

25%

Spot rate

$

2.50

/£

$

2.00

/£

$

1.60

/£

P*

£

1,800

£

2,250

£

2,812.50

Where

P* = Pound sterling price of the asset held by the U.S. firm

The CFO decides to hedge his exposure by selling forward the expected value of the pound

denominated cash flow at F1($/£) = $2/£. As a result,

A) the firm’s exposure to the exchange rate is made worse.

B) he has a nearly perfect hedge.

C) he has a perfect hedge.

D) none of the options

57) A U.S. firm holds an asset in Italy and faces the following scenario:

State 1

State 2

State 3

Probability

30%

40%

30%

Spot rate

$

2.50

$

1.50

$

0.90

P*

€

1,350.00

€

2,250.00

€

3,750.00

Version 1 29

Where

P* = Euro price of the asset held by the U.S. firm

The CFO decides to hedge his exposure by selling forward the expected value of the euro

denominated cash flow at F1($/£) = $1.50/€. As a result,

A) the firm’s exposure to the exchange rate is made worse.

B) he has a nearly perfect hedge.

C) he has a perfect hedge.

D) none of the options

58) Suppose a U.S. firm has an asset in Britain whose local currency price is random. For

simplicity, suppose there are only three states of the world and each state is equally likely to

occur. The future local currency price of this British asset (P*) as well as the future exchange

rate (S) will be determined, depending on the realized state of the world.

State

Probability

P*

S

S× P*

1

1/3

£

980

$

1.40

/£

$

1,372

2

1/3

£

1,000

$

1.50

/£

$

1,500

3

1/3

£

1,070

$

1.60

/£

$

1,712

Which of the following statements is most correct?

A) The firm faces no exchange rate risk since the local currency price of the asset and

the exchange rate are negatively correlated.

B) The firm faces substantial exchange rate risk since the local currency price of the

asset and the exchange rate are positively correlated.

C) The firm’s exchange rate exposure can be completely hedged with derivatives written

on the British pound.

D) Since randomness is involved, no hedging is possible.

Version 1 30

59) Suppose a U.S. firm has an asset in Britain whose local currency price is random. For

simplicity, suppose there are only three states of the world and each state is equally likely to

occur. The future local currency price of this British asset (P*) as well as the future exchange

rate (S) will be determined, depending on the realized state of the world.

State

Probability

P*

S

S× P*

1

1/3

£

1,000

$

1.40

/£

$

1,400

2

1/3

£

1,000

$

1.50

/£

$

1,500

3

1/3

£

1,000

$

1.60

/£

$

1,600

Which of the following statements is most correct?

A) The firm faces no exchange rate risk since the local currency price of the asset and

the exchange rate are negatively correlated.

B) The firm faces substantial exchange rate risk since the local currency price of the

asset and the exchange rate are positively correlated.

C) The firm’s exchange rate exposure can be completely hedged with derivatives written

on the British pound.

D) Since randomness is involved, no hedging is possible.

60) Suppose a U.S. firm has an asset in Britain whose local currency price is random. For

simplicity, suppose there are only three states of the world and each state is equally likely to

occur. The future local currency price of this British asset (P*) as well as the future exchange

rate (S) will be determined, depending on the realized state of the world.

State

Probability

P*

S

S× P*

1

1/3

£

1,000

$

1.40

/£

$

1,400

2

1/3

£

933

$

1.50

/£

$

1,400

3

1/3

£

875

$

1.60

/£

$

1,400

Which of the following statements is most correct?

Version 1 31

A) The firm faces no exchange rate risk since the local currency price of the asset and

the exchange rate are negatively correlated.

B) The firm faces substantial exchange rate risk since the local currency price of the

asset and the exchange rate are positively correlated.

C) The firm’s exchange rate exposure can be completely hedged with derivatives written

on the British pound.

D) Since randomness is involved, no hedging is possible.

61) Suppose a U.S. firm has an asset in Italy whose local currency price is random. For

simplicity, suppose there are only three states of the world and each state is equally likely to

occur. The future local currency price of this asset (P*) as well as the future exchange rate (S)

will be determined, depending on the realized state of the world.

State

Probability

P*

S

S× P*

1

1/3

€

1,000

$

1.40

/£

$

1,400

2

1/3

€

933

$

1.50

/£

$

1,400

3

1/3

€

875

$

1.60

/£

$

1,400

Assume that you choose to “hedge” this asset by selling forward the expected value of the euro

denominated cash flow at

F1($/£) = $1.50/€. Calculate your cash flows in each of the possible states.

A) $1,400, $1,400, $1,400

B) $1,496.6, $1,400, $1,306.40

C) $1,404, $1,404. $1,404

D) none of the options

62) Consider a U.S.-based MNC with a wholly-owned Italian subsidiary. Following a

depreciation of the dollar against the euro, which of the following conclusions are correct?

Version 1 32

A) The cash flow in euro could be altered due an alteration in the firm’s competitive

position in the marketplace.

B) A given operating cash flow in euro will be converted to a higher U.S. dollar cash

flow.

C) Both A and B are correct.

D) none of the options

63) Consider a U.S.-based MNC with a wholly-owned Italian subsidiary. Following a

depreciation of the dollar against the euro, which of the following describes the competitive

effect of the depreciation?

A) The cash flow in euro could be altered due an alteration in the firm’s competitive

position in the marketplace.

B) A given operating cash flow in euro will be translated to a higher U.S. dollar cash

flow.

C) The cash flow in euro could be altered due an alteration in the firm’s competitive

position in the marketplace, and a given operating cash flow in euro will be translated to a higher

U.S. dollar cash flow.

D) none of the options

64) Consider a U.S. MNC with operations in Great Britain. Which of the following are

potential risks following a strengthening of the dollar?

A) A pound sterling depreciation may affect operating cash flow in pounds by altering

the firm’s competitive position in the marketplace.

B) A given operating cash flow in pounds will be converted into a lower dollar amount

after the pound depreciation.

C) Both A and B are correct.

D) none of the options

65) Which of the following is false?

Version 1 33

A) The competitive effect is that a depreciation may affect operating cash flow in the

foreign currency by altering the firm’s competitive position in the marketplace.

B) The conversion effect is defined as a given operating cash flow in a foreign currency

will be converted into a lower dollar amount after a currency depreciation.

C) The competitive effect is defined as a given operating cash flow in a foreign currency

will be converted into a lower dollar amount after a currency depreciation.

D) none of the options

66) Consider a U.S.-based MNC with a wholly-owned German subsidiary. Following a

depreciation of the dollar against the euro, which of the following describes the conversion effect

of the depreciation?

A) The cash flow in euro could be altered due a change in the firm’s competitive

position in the marketplace.

B) A given operating cash flow in euro will be translated to a higher U.S. dollar cash

flow.

C) Both A and B are correct.

D) none of the options

67) Consider a U.S.-based MNC with a wholly-owned French subsidiary. Following a

depreciation of the dollar against the euro, which of the following best describes the mechanism

of any effect of the depreciation?

A) The change in the cash flow in euro due an alteration in the firm’s competitive

position in the marketplace is in part a function of the elasticity of demand for the firm’s product.

B) A given operating cash flow in euro will be translated to a higher U.S. dollar cash

flow regardless of the firm’s hedging program.

C) Both A and B are correct.

D) none of the options

68) Which of the following is true?

Version 1 34

A) The competitive effect is that a currency depreciation may affect operating cash flow

in the foreign currency by altering the firm’s competitive position in the marketplace.

B) The conversion effect is defined as a given accounting cash value in a foreign

currency will be converted into a lower dollar amount after currency depreciation.

C) The competitive effect is defined as a given operating cash flow in a foreign currency

will be converted into a lower dollar amount after a currency depreciation.

D) none of the options

69) Consider a U.S.-based MNC with a wholly-owned European subsidiary selling a product

sourced in euro and priced in euro with inelastic demand. Following a depreciation of the dollar

against the euro, which of the following is the truest?

A) Since they have inelastic demand, the U.S. firm can just pass through the impact of

the exchange rate change.

B) Since they have elastic demand, the U.S. firm cannot just pass through the impact of

the exchange rate change.

C) Since the exchange rate movement was favorable to the U.S. firm, there is no impact

on the firm’s position.

D) none of the options.

70) A firm’s operating exposure is

A) defined as the extent to which the firm’s operating cash flows would be affected by

the random changes in exchange rates.

B) determined by the structure of the markets in which the firm sources its inputs, such

as labor and materials, and sells its products.

C) determined by the firm’s ability to mitigate the effect of exchange rate changes by

adjusting its markets, product mix, and sourcing.

D) all of the options

71) Generally speaking, a firm is subject to high degrees of operating exposure

Version 1 35

A) when its costs but not prices are sensitive to exchange rate changes.

B) when its prices but not costs are sensitive to exchange rate changes.

C) when either its cost or its price is sensitive to exchange rate changes.

D) none of the options

72) Generally speaking, when both a firm’s costs and its price are sensitive to exchange rate

changes,

A) the firm is not subject to high degrees of operating exposure.

B) the firm is subject to high degrees of operating exposure.

C) the firm should hedge.

D) none of the options

73) The firm may not be subject to high degrees of operating exposure

A) when changes in real exchange rates are exactly offset by the inflation differential.

B) when changes in nominal exchange rates are exactly matched by the inflation

differential.

C) when changes in nominal exchange rates are exactly offset by the inflation

differential.

D) none of the options

74) The firm may not be able to pass through changes in the exchange rate

A) in markets with high product differentiation.

B) in markets with high price inelasticities.

C) in markets with low product differentiation or in markets with high price elasticities.

D) none of the options

Version 1 36

75) The firm may not be able to pass through changes in the exchange rate

A) in markets with mainly domestic (foreign to the firm) competitors.

B) in markets with low price elasticities.

C) in markets with mainly domestic (foreign to the firm) competitors or in markets with

low price elasticities.

D) none of the options

76) Generally speaking, a firm is subject to high degrees of operating exposure when

A) either its cost or its price is sensitive to exchange rate changes.

B) both the cost and the price are sensitive to exchange rate changes.

C) both the cost and the price are insensitive to exchange rate changes.

D) none of the options

77) What is the objective of managing operating exposure?

A) Stabilize cash flows in the face of fluctuating exchange rates.

B) Selecting low cost production sites.

C) Increase the variability of cash flows in the face of fluctuating exchange rates.

D) Both A and C are correct.

78) What is the objective of managing operating exposure?

A) Stabilize accounting results in the face of fluctuating exchange rates.

B) Selecting low cost production sites.

C) Increase the variability of cash flows in the face of fluctuating exchange rates.

D) Both A and C are correct.

79) Managing operating exposure

Version 1 37

A) is a short-term tactical issue.

B) is a long-term issue, like selecting a site for a factory.

C) is relatively unimportant, since most MNCs have a built-in hedge.

D) Both A and C are correct.

80) Which of the following can a company use to manage operating exposure?

A) Selecting low-cost production sites, diversifying the market.

B) Low cost production sites, but not financial hedging.

C) Pursuing a flexible sourcing policy, product differentiation, R&D efforts.

D) Both A and C are correct.

81) When the domestic currency is strong or expected to become strong,

A) this could erode the competitive position of the firm’s exports.

B) this could erode the competitive position of the firm’s import competition.

C) the firm should consider locating production facilities in a foreign country where

costs are low.

D) this could erode the competitive position of the firm’s exports and the firm should

consider locating production facilities in a foreign country where costs are low.

82) A foreign country could provide low cost production sites

A) because the factors of production are underpriced.

B) because the currency is undervalued.

C) because the locals like to give away their land labor and capital to foreigners.

D) because the factors of production are underpriced and because the currency is

undervalued.

Version 1 38

83) While maintaining multiple production sites does provide a firm valuable options,

A) a firm may miss out on economies of scope.

B) a firm may miss out on economies of scale.

C) a firm may find that exchange rate changes can fully offset the advantage of multiple

manufacturing sites.

D) a firm may miss out on economies of scope and economies of scale.

84) Goldman Sachs estimates that as much as __________ percent of the pretax profits that

Porsche reported for a recent fiscal year came from skillfully executing currency options.

A) 5

B) 10

C) 15

D) 75

85) Developing multiple production sites in a variety of countries,

A) can create an excess capacity problem.

B) can lead to underutilization of domestic plants.

C) can lead to domestic job losses.

D) all of the options

86) A flexible sourcing policy

A) is primarily concerned with low-cost (and often low-quality) vendors.

B) need not be confined just to materials and parts.

C) only works for manufacturing firms, not service firms.

D) puts the focus on the exchange rate at the expense of shipping rates.

Version 1 39

87) A firm that is committed to keeping manufacturing facilities in only the home country

(and not developing multiple production sites in a variety of countries) can

A) not mitigate the effects of exchange rate changes.

B) lessen the effect of exchange rate changes by sourcing from where input costs are

low.

C) focus on selling commodity products with product differentiation.

D) pursue a strategy of increasing its products price elasticity of demand.

88) If the domestic currency is strong or expected to become strong,

A) a firm can choose to locate production facilities in a foreign country where costs are

low due to either the undervalued currency or underpriced factors of production.

B) a firm should curtail R&D efforts until the exchange rate situation improves.

C) a firm should abandon international sales and focus on domestic market share.

D) the firm should focus on profiting in the currency futures market based on its

forecasts.

89) Which of the following is a true statement?

A) As long as exchange rates do not always move in the same direction, the firm can

stabilize its operating cash flows by diversifying its export market.

B) The firm should not get into new lines of business solely to diversify exchange risk

because conglomerate expansion can bring about inefficiency and losses.

C) all of the options

D) none of the options

90) A firm that is committed to keeping manufacturing facilities in only the home country

(and not developing multiple production sites in a variety of countries) can

Version 1 40

A) lessen the effect of exchange rate changes by pursuing a strategy of diversifying the

markets in which the firm’s products are sold.

B) not mitigate the effects of exchange rate changes.

C) lessen the effect of exchange rate changes by pursuing a strategy of selling

commodity products without product differentiation.

D) pursue a strategy of increasing its products price elasticity of demand.

91) It can be argued that, while financial hedging can be used to stabilize a firm’s cash flows,

A) it is not a substitute for long-term operational hedging.

B) it is therefore a substitute for long-term operational hedging.

C) it is inferior to money market hedging.

D) none of the options.

92) Investments in R&D

A) are usually a waste of time and money.

B) will likely weaken the firm’s competitive position.

C) can allow the firm to cut costs but decreases productivity.

D) can allow the firm to maintain and strengthen its competitive position, as well as cut

costs and enhance productivity.

93) The price elasticity of demand for unique products tends to be

A) highly elastic.

B) highly inelastic.

C) highly elastic and highly inelastic.

D) none of the options

Version 1 41

94) The price elasticity of demand for commodity products tends to be

A) highly elastic.

B) highly inelastic.

C) highly elastic and highly inelastic.

D) none of the options

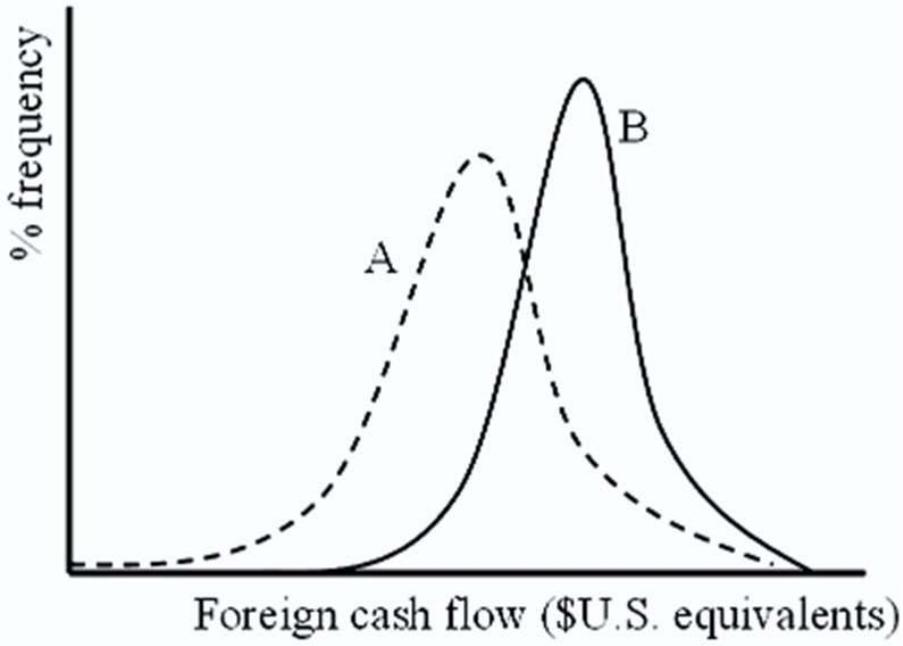

95) In the figure below, label curves A and B are, respectively,

A) unhedged and hedged.

B) hedged and unhedged.

C) normal and abnormal.

D) none of the options

Version 1 42

96) Investment in R&D activities can allow the firm to maintain and strengthen its

competitive position in the face of adverse exchange rate movements. The mechanism for this

includes

A) successful R&D efforts allowing the firm to cut costs and enhance productivity.

B) R&D efforts leading to the introduction of new and unique products for which

competitors offer no close substitutes—since the demand for unique products tends to be highly

inelastic the firm would be less exposed to exchange risk.

C) successful R&D efforts creating a perception among consumers that its product is

indeed different from those offered by competitors. Once the firm’s product acquires a unique

identity, its demand is less likely to be price-sensitive.

D) all of the options

97) If the stock market of a foreign country is consistently up when the dollar value of the

currency is down,

A) there may not be a great deal of exchange rate risk for a U.S.-based investor.

B) there will be a great deal of exchange rate risk for a U.S.-based investor.

C) then investors can ignore diversification.

D) none of the options

98) In the case application, “Exchange Risk Management at Merck”, Merck considered the

alternative of financial hedging. Which of the following steps was not used by Merck for

financial hedging?

A) Exchange forecasting and hedging rationale

B) Assessing strategic plan impact and financial instruments

C) Hedging program

D) none of the options

Version 1 43

99) Which of the following steps Merck used for financial hedging describes the process of

reviewing the likelihood of adverse exchange movements, which includes polling outside

forecasters for the dollar over the planning horizon?

A) Exchange forecasting

B) Hedging rationale

C) Assessing strategic plan impact

D) Hedging program

100) Which of the following steps Merck used for financial hedging describes the process of

projecting and comparing cash flows and earnings under the alternative exchange rate scenarios

(i.e. strong and weak dollar scenarios).

A) Exchange forecasting

B) Hedging rationale

C) Assessing strategic plan impact

D) Hedging program

101) Which of the following steps Merck used for financial hedging describes the process of

focusing on the objective of maximizing long-term cash flows and on the potential effect of

exchange rate movements on the firm’s ability to meet its strategic objectives.

A) Exchange forecasting

B) Hedging rationale

C) Assessing strategic plan impact

D) Hedging program

102) Which of the following steps Merck used for financial hedging describes the process of

formulating an implementation strategy regarding the term of the hedge, the strike price of the

currency options, and the percentage of income to be covered?

Version 1 44

A) Exchange forecasting

B) Hedging rationale

C) Assessing strategic plan impact

D) Hedging program

103) Suppose that you hold a piece of land in the city of London that you may want to sell in

one year. As a U.S. resident, you are concerned with the dollar value of the land. Assume that if

the British economy booms in the future, the land will be worth £2,000, and one British pound

will be worth $1.80. If the British economy slows down, on the other hand, the land will be

worth less, say, £1,500, but the pound will be stronger, say, $2.20/£. You feel that the British

economy will experience a boom with a 60 percent probability and a slowdown with a 40 percent

probability.

Estimate your exposure (b) to the exchange risk.

104) Suppose that you hold a piece of land in the city of London that you may want to sell in

one year. As a U.S. resident, you are concerned with the dollar value of the land. Assume that if

the British economy booms in the future, the land will be worth £2,000, and one British pound

will be worth $1.80. If the British economy slows down, on the other hand, the land will be

worth less, say, £1,500, but the pound will be stronger, say, $2.20/£. You feel that the British

economy will experience a boom with a 60 percent probability and a slowdown with a 40 percent

probability.

Compute the variance of the dollar value of your property that is attributable to exchange rate

uncertainty.

Version 1 45

105) Suppose that you hold a piece of land in the city of London that you may want to sell in

one year. As a U.S. resident, you are concerned with the dollar value of the land. Assume that if

the British economy booms in the future, the land will be worth £2,000, and one British pound

will be worth $1.80. If the British economy slows down, on the other hand, the land will be

worth less, say, £1,500, but the pound will be stronger, say, $2.20/£. You feel that the British

economy will experience a boom with a 60 percent probability and a slowdown with a 40 percent

probability.

Discuss how you can hedge your exchange risk exposure and also examine the consequences of

hedging.

Version 1 46

Answer Key

Test name: chapter 9

Version 1 47

Version 1 48

Version 1 49