Version 1 1

Student name:__________

1) Corporate governance can be defined as

A) the economic, legal, and institutional framework in which corporate control and cash

flow rights are distributed among shareholders, managers and other stakeholders of the company.

B) the general framework in which company management selects and monitors the

Board of Directors.

C) the rules and regulations adopted by boards of directors specifying how to manage

companies.

D) the government-imposed rules and regulations affecting corporate management.

2) When managerial self-dealings are excessive and left unchecked,

A) they can have serious negative effects on share values.

B) they can impede the proper functions of capital markets.

C) they can impede such measures as GDP growth.

D) all of the options

3) Corporate governance structure

A) varies a great deal across countries.

B) has become homogenized following the integration of capital markets.

C) has become homogenized due to cross-listing of shares of many public corporations.

D) none of the options

4) The genius of public corporations stems from their capacity to allow efficient sharing or

spreading of risk among many investors, who can buy and sell their ownership shares on liquid

stock exchanges and let professional managers run the company on behalf of shareholders. This

risk sharing stems from

Version 1 2

A) the illiquidity of the shares.

B) the limited liability of shareholders.

C) the limited liability of bondholders.

D) the limited ability of shareholders.

5) In a public company with diffused ownership, the board of directors is entrusted with

A) monitoring the auditors and safeguarding the interests of shareholders.

B) monitoring the shareholders and safeguarding the interests of management.

C) monitoring the management and safeguarding the interests of shareholders.

D) none of the options

6) The key weakness of the public corporation is

A) too many shareholders, which makes it difficult to make corporate decisions.

B) relatively high corporate income tax rates.

C) conflicts of interest between managers and shareholders.

D) conflicts of interests between shareholders and bondholders.

7) When company ownership is diffuse,

A) a “free rider” problem encourages shareholder activism.

B) the large number of shareholders ensures strong monitoring of managerial behavior

because with a large enough group, there’s almost always someone who will to incur the costs of

monitoring management.

C) most shareholders will have a strong enough incentive to incur the costs of

monitoring management.

D) a “free rider” problem discourages shareholder activism and few shareholders have a

strong enough incentive to incur the costs of monitoring management.

Version 1 3

8) In many countries with concentrated ownership

A) the conflicts of interest between shareholders and managers are worse than in

countries with diffuse ownership of firms.

B) the conflicts of interest are greater between large controlling shareholders and small

outside shareholders than between managers and shareholders.

C) the conflicts of interest are greater between managers and shareholders than between

large controlling shareholders and small outside shareholders.

D) corporate forms of business organization with concentrated ownership are rare.

9) In what country do the three largest shareholders control, on average, about 60 percent of

the shares of a public company?

A) United States

B) Canada

C) Great Britain

D) Italy

10) The public corporation

A) is jointly owned by a (potentially) large number of shareholders.

B) offers shareholders limited liability.

C) separates the ownership and control of a firm’s assets.

D) all of the options

11) The key strength(s) of the public corporation is/are

Version 1 4

A) their capacity to allow efficient risk sharing among many investors.

B) their capacity to raise large amounts of funds at relatively low cost.

C) their capacity to consolidate decision-making.

D) all of the options

12) The central issue of corporate governance is

A) how to protect creditors from managers and controlling shareholders.

B) how to protect outside investors from the controlling insiders.

C) how to alleviate the conflicts of interest between managers and shareholders.

D) how to alleviate the conflicts of interest between shareholders and bondholders.

13) In theory,

A) managers are hired by the shareholders at the annual stockholders meeting. If the

managers turn in a bad year, new ones get hired.

B) shareholders hire the managers to oversee the board of directors.

C) managers are hired by the board of directors; the board is accountable to the

shareholders.

D) none of the options

14) In the reality of corporate governance at the turn of this century,

A) boards of directors are often dominated by management-friendly insiders.

B) a typical board of directors often has relatively few outside directors who can

independently and objectively monitor the management.

C) managers of one firm often sit on the boards of other firms, whose managers are on

the board of the first firm. Due to the interlocking nature of these boards, there can exist a culture

of “I’ll overlook your problems if you overlook mine.”

D) all of the options have been true to a greater or lesser extent in the recent past.

Version 1 5

15) The strongest protection for investors is provided by

A) English common law countries, such as Canada, the United States, and the U.K.

B) French civil law countries, such as Belgium, Italy, and Mexico.

C) a weak board of directors.

D) socialized firms.

16) The public corporation has a key weakness which is

A) the conflicts of interest between bondholders and shareholders.

B) the conflicts of interest between managers and bondholders.

C) the conflicts of interest between stakeholders and shareholders.

D) the conflicts of interest between managers and shareholders.

17) The separation of the company’s ownership and control,

A) is especially prevalent in such countries as the United States and the United

Kingdom, where corporate ownership is highly diffused.

B) is especially prevalent in such countries as Italy and Mexico, where corporate

ownership is highly concentrated.

C) is a rational response to the agency problem.

D) none of the options

18) In the United States, managers are legally bound by the “duty of loyalty” to

A) the board of directors.

B) the shareholders.

C) the bondholders.

D) the government.

Version 1 6

19) In the United States, managers are bound by the “duty of loyalty” to serve the

shareholders.

A) This is an ethical, not legal, obligation.

B) This is a legal obligation.

C) This is only a moral obligation; there are no penalties.

D) none of the options

20) Outside the United States and the United Kingdom,

A) concentrated ownership of the company is more the exception than the rule.

B) diffused ownership of the company is more the exception than the rule.

C) partnerships are more important than corporations.

D) none of the options

21) A complete contract between shareholders and managers

A) would specify exactly what the manager will do under each of all possible future

contingencies.

B) would be an expensive contract to write and a very expensive contract to monitor.

C) would eliminate any conflicts of interest (and managerial discretion).

D) all of the options

22) Residual control right refers to:

Version 1 7

A) the rights or control to make decisions under contingencies that are not specifically

covered by complete contracts

B) the portion of the complete contract that deals with future contingencies forseen

C) neither the rights or control to make decisions under contingencies that are not

specifically covered by complete contracts or the portion of the complete contract that deals with

future contingencies forseen

D) both the rights or control to make decisions under contingencies that are not

specifically covered by complete contracts and the portion of the complete contract that deals

with future contingencies forseen

23) Why is it rational to make shareholders “weak” by giving control to the managers of the

firm?

A) This may be rational when shareholders may be neither qualified nor interested in

making business decisions.

B) This may be rational since many shareholders find it easier to sell their shares in an

underperforming firm than to monitor the management.

C) This may be rational to the extent that managers are answerable to the board of

directors.

D) All of the options are explanations for the separation of ownership and control.

24) Free cash flow refers to

A) a firm’s cash reserve in excess of tax obligation.

B) a firm’s funds in excess of what’s needed for undertaking all profitable projects.

C) a firm’s cash reserve in excess of interest and tax payments.

D) a firm’s income tax refund that is due to interest payments on borrowing.

25) The investors supply funds to the company but are not involved in the company’s daily

decision making. As a result, many public companies come to have

Version 1 8

A) strong shareholders and weak managers.

B) strong managers and weak shareholders.

C) strong managers and strong shareholders.

D) weak managers and weak shareholders.

26) The agency problem refers to the possible conflicts of interest between

A) self-interested managers as principals and shareholders of the firm who are the

agents.

B) altruistic managers as agents and shareholders of the firm who are the principals.

C) self-interested managers as agents and shareholders of the firm who are the

principals.

D) dutiful managers as principals and shareholders of the firm who are the agents.

27) Self-interested managers may be tempted to

A) indulge in expensive perquisites at company expense.

B) adopt anti-takeover measures for their company to ensure their personal job security.

C) waste company funds by undertaking unprofitable projects that benefit themselves

but not shareholders.

D) All of the options are potential abuses that self-interested managers may be tempted

to visit upon shareholders.

28) Suppose in order to defraud the shareholders, a manager sets up an independent company

that he owns and sells the main company’s output to this company. He would be tempted to set

the transfer price

A) below market prices.

B) above market prices.

C) at the market price.

D) in accordance with GAAP.

Version 1 9

29) Suppose in order to defraud the shareholders, a manager sets up an independent company

that he owns and buys one of the main company’s inputs of production from this company. He

would be tempted to set the transfer price

A) below market prices.

B) above market prices.

C) at the market price.

D) in accordance with GAAP.

30) Why do managers tend to retain free cash flow?

A) Managers are in the best position to decide the best use of those funds.

B) These funds are needed for undertaking profitable projects and the issue costs are

less than new issues of stocks or bonds.

C) Managers may not be acting in the shareholders best interest, and for a variety of

reasons, want to use the free cash flow.

D) none of the options

31) Managerial entrenchment efforts are clear signs of the agency problem. They include

A) anti-takeover defenses.

B) poison pills.

C) changes in the voting procedures to make it more difficult for the firm to be taken

over.

D) all of the options

32) In high-growth industries where companies’ internally generated funds fall short of

profitable investment opportunities,

Version 1 10

A) managers are less likely to waste funds in unprofitable projects.

B) managers are more likely to waste funds in unprofitable projects.

33) The agency problem tends

A) to be more serious in firms with free cash flows.

B) to be more serious in firms with excessive amounts of excess cash.

C) to be less serious in firms with few numbers of shareholders.

D) all of the options

34) Governance mechanisms that exist to alleviate or remedy the agency problem include:

A) independent board of directors & incentive contracts.

B) concentrated ownership & Accounting transparency

C) shareholder activism & overseas stock listings

D) all of the options

Version 1 11

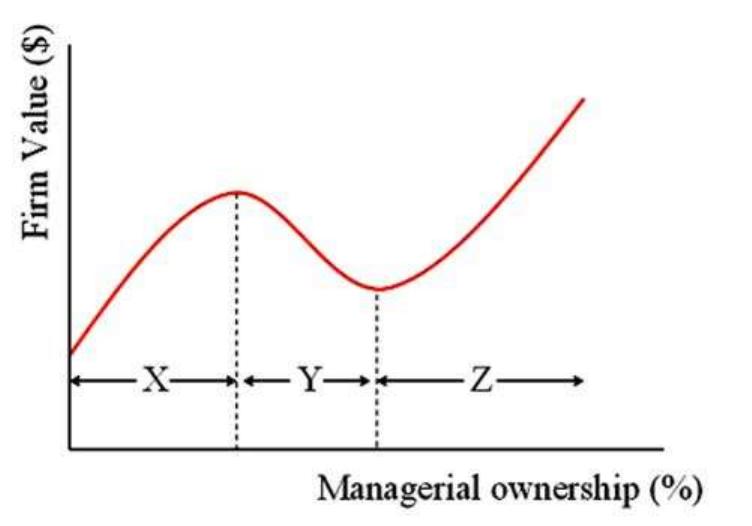

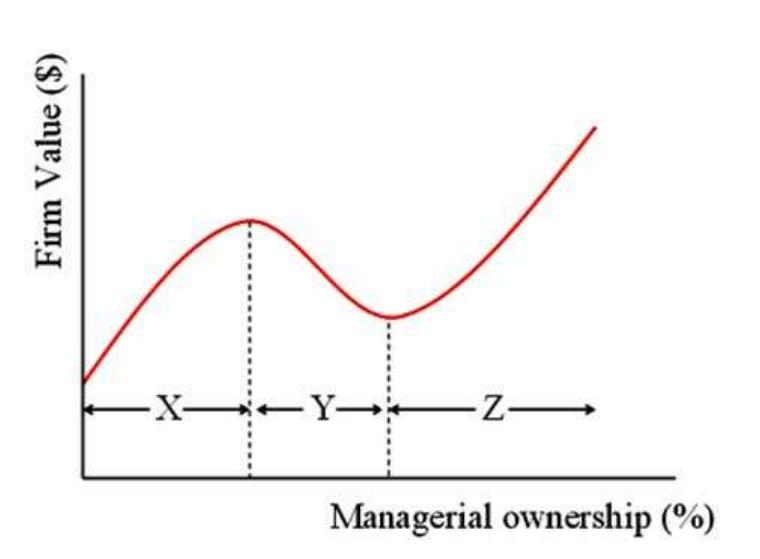

35) In the graph, X, Y, and Z represent

A) entrenchment, alignment, entrenchment.

B) alignment, entrenchment, alignment.

C) misalignment and alignment.

D) agency costs of debt and equity.

Version 1 12

36) Morck, Shleifer, and Vishny (1988) studied the relationship between managerial

ownership share and firm value for Fortune 500 U.S. companies. The results of their analysis

suggested that the first turning point (the first vertical, dashed line between X and Y) is reached

at __________ percent and the second turning point (the second vertical, dashed line between Y

and Z) at about __________ percent, respectively.

A) 5; 25.

B) 15; 50.

C) 50; 75.

D) none of the options

37) Which of the following is true regarding leveraged buy-outs (LBOs)?

Version 1 13

A) LBOs involve managers or buyout partners acquiring controlling interests in public

companies, usually financed by partners’ equity.

B) Concentrated ownership and low levels of debt associated with LBOs are the

mechanism for solving the agency problem.

C) LBOs improve a company’s free cash flow and this is the mechanism by which they

can solve the agency problem.

D) LBOs involve managers or buyout partners acquiring controlling interests in public

companies (usually financed by heavy borrowing), and concentrated ownership and high levels

of debt associated with LBOs are the mechanism for solving the agency problem.

38) Tobin’s Q is

A) the ratio of the market value of company assets to the replacement costs of the assets.

B) a means to find overvalued stocks: If Q is high it means that the cost to replace a

firm’s assets is greater than the value of its stock.

C) the same as the price-to-book ratio.

D) the ratio of the market value of company assets to the replacement costs of the assets,

as well as a means to find overvalued stocks: If Q is high it means that the cost to replace a firm’s

assets is greater than the value of its stock.

39) Which of the following statements describes “activist investors”?

A) invests in stocks of a company for the explicit purpose of influencing the company’s

management

B) plays an important role in promoting shareholder’s interests.

C) can influence a company to repurchase stocks.

D) all of the above

40) Which of the following statements describes “activist shareholders”?

Version 1 14

A) wish to persuade the companies to make commitments to corporate social

responsibilities, including increasing gender and ethnic diversity on the board of directors

B) pursue their social and political agenda by promoting changes in companies’

environmental, social, and governance practices.

C) both A and B

D) none of the above

41) It is important for society as a whole to solve the agency problem, since the agency

problem

A) leads to waste of scarce resources.

B) hampers capital market functions.

C) retards economic growth.

D) all of the options

42) In the U.S., the chief role of the board of directors is

A) to hire the management team.

B) to decide on the annual capital budget.

C) to design an effective incentive compatible compensation scheme for themselves.

D) none of the options

43) In the United Kingdom, the majority of public companies

A) voluntarily abide by the Code of Best Practice on corporate governance.

B) are compelled by law to abide by the Code of Best Practice on corporate governance.

C) do not abide by the Code of Best Practice on corporate governance.

D) none of the options

Version 1 15

44) In Germany, the corporate board is

A) legally charged with representing the interests of shareholders exclusively.

B) legally charged with looking after the interests of stakeholders (e.g., workers,

creditors, etc.) in general, not just shareholders.

C) legally charged as a supervisory board only.

D) legally charged as a management board only.

45) In the United States,

A) boards of directors are legally responsible for representing the interests of the

shareholders.

B) due to the diffused ownership structure of the public company, management often

gets to choose board members who are likely to be friendly to management.

C) there is a correlation between underperforming firms and boards of directors who are

not fully independent.

D) all of the options

46) In the United States, it is not uncommon for the same person to serve as both CEO and

chairman of the board.

A) This situation must not have much conflict of interest since it is common.

B) This situation has a built-in conflict of interest.

C) This is only legal if that individual owns a controlling number of shares in the firm.

D) none of the options

47) Suppose you are the CEO of company A, and you serve on the board of company B,

while the CEO of B is on your board.

Version 1 16

A) This is a potential conflict of interest for both parties.

B) This is normal and even a desirable situation since it allows for efficient information

sharing between the firms.

C) There is a potential conflict for the shareholders of the two firms.

D) all of the options

48) In the United States, it is well documented that

A) boards dominated by their chief executives are prone to trouble.

B) public scrutiny can help improve corporate governance.

C) as public firms improve their corporate governance, the stock price goes up.

D) all of the options

49) The board of directors may grant stock options to managers. These are

A) call options.

B) put options.

C) both of the options

D) none of the options

50) If an incentive contract specifies certain accounting performance,

A) that accounting number will likely be the focus of managers.

B) managers will set aside the accounting goal if it conflicts with the goal of

maximizing shareholder wealth.

C) managers will be unable to manipulate the GAAP, so shareholders can be confident

of having their wealth maximized.

D) none of the options

Version 1 17

51) The board of directors may grant stock options to managers

A) to save executive compensation costs.

B) to use as a substitute for bonus.

C) to align the interest of managers with that of shareholders.

D) none of the options

52) When designing an incentive contract,

A) it is important for the board of directors to set up an independent compensation

committee that can carefully design the contract and diligently monitor manager’s actions.

B) senior executives can be trusted to not abuse incentive contracts by artificially

manipulating accounting numbers since the auditors should look in to that.

C) the presence of any incentive is enough, whether it is accounting based or stock-price

based.

D) the board of directors should always give the managers a “heads I win, tails you

lose” type of option.

53) Concentrated ownership of a public company

A) is normal in the United States, following the well-publicized scandals of recent

years.

B) is relatively rare in the United States and common in many other parts of the world.

C) leads to a free-rider problem with the minority shareholders relying on the majority

shareholders to assume an undue burden in monitoring the management.

D) is the norm in Great Britain.

54) Concentrated ownership of a public company

Version 1 18

A) can be an effective way to alleviate the agency problem between shareholders and

managers.

B) is the norm in Great Britain.

C) tends to be an ineffective way to alleviate conflicts of interest between groups of

shareholders.

D) none of the options

55) The goal of greater accounting transparency

A) is to impose more rules and harsher penalties for their violation.

B) is to reduce the information symmetry between corporate insiders and the public.

C) is to encourage managerial self-dealings.

D) is to reduce the information asymmetry between corporate insiders and the public, as

well as discourage managerial self-dealings.

56) Accounting transparency

A) can only be achieved when managers commit to serving on their own audit

committee.

B) occurs when the accounting department has translucent cubicles for their workers.

C) promises to reduce the information asymmetry between corporate insiders and the

public.

D) none of the options

57) While debt can reduce agency costs between shareholders and management,

A) debt can create its own agency costs.

B) this only happens at extreme levels of debt.

C) this does not work for firms in mature industries with large cash reserves.

D) none of the options

Version 1 19

58) While debt can reduce agency costs between shareholders and management,

A) excessive debt may also induce the risk-averse managers to engage in extra risky

investment projects, causing an underinvestment problem.

B) with debt financing, companies cannot misuse debt to finance corporate empire

building.

C) excessive debt may also induce the risk-averse managers to forgo profitable but risky

investment projects, causing an underinvestment problem. Additionally, with debt financing,

companies can misuse debt to finance corporate empire building.

D) none of the options

59) For firms with free cash flows,

A) debt can be a stronger mechanism than stocks for credibly bonding managers to

release cash flows to investors.

B) equity dividends can be a stronger mechanism than bonds for credibly bonding

managers to release cash flows to investors.

C) preferred stock dividends can be a stronger mechanism than bonds for credibly

bonding managers to release cash flows to investors.

D) none of the options

60) Debt can reduce agency costs between shareholders and management, but

A) only if the firm is totally up to its eyeballs in debt.

B) only to the extent that the firm can commit all of its free cash flow.

C) excessive debt can create its own agency conflicts.

D) debt is best used as a corporate governance mechanism by young companies with

limited cash reserves.

61) Companies domiciled in countries with weak investor protection can reduce agency costs

between shareholders and management

Version 1 20

A) by moving to a better county.

B) by listing their stocks in countries with strong investor protection.

C) by voluntarily complying with the provisions of the U.S. Sarbanes-Oxley Act.

D) by having a press conference and promising to be nice to their investors.

62) Benetton, an Italian clothier, is listed on the New York Stock Exchange.

A) This decision provides their shareholders with a higher degree of protection than is

available in Italy.

B) This decision can be a signal of the company’s commitment to shareholder rights.

C) This may make investors both in Italy and abroad more willing to provide capital and

to increase the value of the pre-existing shares.

D) all of the options

63) In the United States and the United Kingdom, hostile takeovers

A) are illegal.

B) can serve as a drastic corporate governance mechanism of the last resort.

C) reinforce the notion that managers can take their control of the company for granted.

D) require management approval.

64) In many countries, hostile takeovers are relatively rare. This is so partly because of

A) the language barrier.

B) dispersed ownership in these countries.

C) cultural values and economic environments disapproving hostile corporate takeovers.

D) concentrated ownership in these countries, as well as cultural values and political

environments disapproving hostile corporate takeovers.

Version 1 21

65) After a hostile takeover,

A) the existing management team is usually fired.

B) the existing management team is usually retained at a higher wage.

C) a combination of Answers A and B.

D) none of the options

66) In a hostile takeover attempt, the bidder typically

A) makes a tender offer to the target shareholders at a price substantially less than the

prevailing share price.

B) makes a tender offer to the target shareholders at the prevailing share price.

C) makes a tender offer to the target shareholders at a price substantially exceeding the

prevailing share price.

D) seeks to merge with the target company with an exchange of shares.

67) Suppose the managers of a company have driven the stock price down because they have

spent the investors’ money on lavish perquisites like golf club memberships.

A) This situation may prompt a corporate raider to buy up the shares of the firm in a

hostile takeover.

B) If the hostile takeover is successful, the managers will probably lose their jobs in the

ensuing restructuring.

C) If the restructuring is successful, the corporate raider can sell his shares at a profit.

D) all of the options

68) Private benefits of corporate control will tend to be higher in

A) French civil law countries than in English common law countries.

B) English common law countries than in French civil law countries.

C) French civil law countries than in Scandinavian civil law countries.

D) English common law countries than in German civil law countries.

Version 1 22

69) English common law countries tend to provide a stronger protection of shareholder rights

than French civil law countries because

A) the former countries tend to be more democratic than the latter.

B) the former countries tend to protect property rights better than the latter.

C) the former countries tend to have more separation of power than the latter.

D) all of the options

70) Many companies issue shares with differential voting rights, deviating from the one-share

one-vote principle.

A) By accumulating superior voting shares, investors can acquire cash flow rights

exceeding control rights.

B) The price of the voting shares is usually twice the price of the voting shares.

C) By accumulating superior voting shares, investors can acquire control rights

exceeding cash flow rights.

D) none of the options

71) Studies show that the quality of law enforcement, as measured by the rule of law index,

will tend to be

A) higher in French civil law countries than in English common law countries.

B) higher in English common law countries than in Scandinavian civil law countries.

C) highest in Scandinavian civil law countries and German civil law countries.

D) highest in English common law countries.

72) Suppose Mr. Lee and his relatives hold 30 percent of shares outstanding of Samsung Life,

which in turn holds 20 percent of Samsung Electronics. What is the cash flow right of the Lee

family in Samsung Electronics?

Version 1 23

A) 50 percent

B) 10 percent

C) 20 percent

D) 6 percent

73) Concentrated corporate ownership is most prevalent in

A) Italy.

B) the U.K.

C) the U.S.

D) Australia.

74) In countries with concentrated ownership,

A) hostile takeovers are quite rare.

B) hostile takeovers are quite common.

75) A pyramidal ownership structure is one in which

A) a shareholder controls a holding company that owns a controlling block of another

company, which in turn owns controlling interests in yet another company, and so on.

B) equity cross-holdings among a group of companies, such as keiretsu and chaebols,

can be used to concentrate and leverage voting rights to acquire control.

C) a combination of these schemes may also be used to leverage control in a pyramidal

ownership structure.

D) none of the options

76) What is the difference between control rights and cash flow rights?

Version 1 24

A) Since all shareholders benefit only from pro-rata cash flows, control rights and cash

flow rights are the same thing.

B) Large investors may be able to derive private benefits from control, thus control

rights can exceed cash flow rights.

C) Cash flow rights are more important than control rights since the only reason to

invest in anything is to generate cash.

D) none of the options

77) The key to extracting private benefits of control that are not shared by other shareholders

on a pro rata basis is to

A) become a large shareholder and acquire control rights exceeding cash flow rights.

B) buy a large block of nonvoting shares.

C) sell your shares in a tender offer.

D) force the firm into bankruptcy.

78) The voting premium, defined as the total vote value (value of a vote times the number of

votes) as a proportion of the firm’s equity market value is only about 2 percent in the United

States and 36 percent in Mexico, suggesting that in Mexico,

A) dominant shareholders extract substantial private benefits of control.

B) dominant shareholders overpay and thus fail to extract substantial private benefits.

C) minority shareholders share in the private benefits of control.

D) none of the options

79) Unless investors can derive significant private benefits of control,

A) they will pay small premiums for voting shares over nonvoting shares.

B) they will pay moderate premiums for voting shares over nonvoting shares.

C) they will pay substantial premiums for voting shares over nonvoting shares.

D) they will not pay substantial premiums for voting shares over nonvoting shares.

Version 1 25

80) The formula to compute the value of the “block premium” is

A)

Price per share paid for the control block – the exchange price after

the control transaction

the exchange price after the announcement of the control transaction

B)

Price per share paid for the control block – the exchange price after

the control transaction

price per share paid for the control block

C)

the exchange price after the control transaction – price per share

paid for the control block

price per share paid for the control block

D)

Price per share paid for the control block – the exchange price after

the control transaction

the exchange price prior to the announcement of the control

transaction

81) The value of private benefits of control may be measured using

A) the difference in value between non-voting shares and voting shares.

B) “block premium,” the difference between the price per share paid for a control block

of shares versus the exchange price of regular shares.

C) the difference in value between non-voting shares and voting shares or “block

premium,” the difference between the price per share paid for a control block of shares versus the

exchange price of regular shares.

D) none of the options

Version 1 26

82) Several studies document the empirical link between

A) weak investor protection and GDP growth.

B) financial development and economic growth.

C) growth in GDP and concentrated ownership.

D) none of the options

83) Financial development can contribute to economic growth in what way(s)?

A) Financial development enhances savings.

B) Financial development channels savings toward real investments in productive

capacities.

C) Financial development enhances the efficiency of investment allocation through the

monitoring and signaling functions of capital markets.

D) all of the options

84) Comparing the U.S. with the German and Japanese corporate governance systems,

A) the U.S. system is “market centered.”

B) the German and Japanese systems are “bank centered.”

C) it seems fair to say that no country has a perfect system.

D) all of the options.

85) The objective of corporate governance reform should be what?

A) Strengthen the protection of outside investors from expropriation by managers.

B) Strengthen the protection of outside investors from expropriation by controlling

insiders.

C) Strengthen the protection of outside investors from expropriation by managers and

controlling insiders.

D) none of the options

Version 1 27

86) One of the objectives of corporate governance reform is to,

A) introduce expensive and burdensome accounting reforms.

B) strengthen the protection of outside investors from expropriation by managers and

controlling insiders.

C) provide taxpayer financing for corporate raiders to strengthen the discipline of the

marketplace.

D) none of the options

87) In the U.S., corporate governance reform has included all of the following except

A) strengthen the independence of boards of directors.

B) enhancing the transparency and disclosure of financial statements.

C) energizing the regulatory and monitoring functions of the SEC.

D) requiring auditors to sit on the boards of directors.

88) The Sarbanes-Oxley Act of 2002 stipulates that

A) a public accounting oversight board be created.

B) the company should appoint independent financial experts to its audit committee.

C) both CEO and CFO sign off on the company’s financial statements.

D) all of the options

89) The Sarbanes-Oxley Act of 2002

A) applies to all U.S. firms.

B) applies to listed companies.

C) applies to issuers whose securities are traded on an over-the-counter bulletin board.

D) all of the options

Version 1 28

90) The Sarbanes-Oxley Act of 2002

A) has had the consequence that many foreign firms have de-listed in the U.S.

exchanges and listed their shares on the London Stock Exchange and other European exchanges.

B) has increased the pace of foreign firms listing their shares in the U.S.

C) has increased the pace of foreign firms listing their shares in the U.S. and has also

had the consequence that many foreign firms have de-listed in the U.S. exchanges and listed their

shares on the London Stock Exchange and other European exchanges.

D) all of the options

91) The cost of compliance with the Sarbanes-Oxley Act

A) is a small amount, since most firms were playing by rules to begin with.

B) disproportionately affects small firms.

C) is paid for with tax credits for firms found to be in compliance.

D) all of the options

92) One implication of the Sarbanes-Oxley Act is that companies must appoint independent

“financial experts” to their committees. Which of the major components is associated with this

objective?

A) Accounting regulation

B) Audit committee

C) Internal control assessment

D) Executive responsibility

93) The major components of the Sarbanes-Oxley Act are

Version 1 29

A) accounting regulation: The creation of a public accounting oversight board charged

with overseeing the auditing of public companies, and restricting the consulting services that

auditors can provide to clients.

B) audit committee: The company should appoint independent “financial experts” to its

audit committee.

C) internal control assessment: Public companies and their auditors should assess the

effectiveness of internal control of financial record keeping and fraud prevention.

D) executive responsibility: Chief executive and finance officers (CEO and CFO) must

sign off on the company’s quarterly and annual financial statements. If fraud causes an

overstatement of earnings, these officers must return any bonuses.

E) all of the options

94) The key requirements of the Sarbanes-Oxley Act state that

A) boards of directors should include at least three outside directors.

B) the positions of CEO and chairman of the board should not reside in the same

individual.

C) compliance is mandatory for public corporations, optional for listed non-public

corporations.

D) none of the options.

95) Since the passage of the Sarbanes-Oxley Act,

A) some foreign firms have chosen to list their shares on the London Stock Exchange

and other European exchanges, instead of U.S. exchanges, to avoid the costly compliance.

B) the pace of foreign firms listing their shares in the U.S. has increased.

C) the firms have passed this increased cost on to their customers.

D) none of the options

96) The major components of the Sarbanes-Oxley Act include all of the following except

Version 1 30

A) accounting regulation: The creation of a public accounting oversight board charged

with overseeing the auditing of public companies, and restricting the consulting services that

auditors can provide to clients.

B) audit committee: The company should appoint independent “financial experts” to its

audit committee.

C) shareholder voting rights reform: “One share one vote” is now the law of the land.

D) executive responsibility: CEOs and CFOs must sign off on the company’s financial

statements.

97) The Dodd-Frank Act was passed

A) in 1933.

B) in 2010.

C) in 1933 and repealed in 2010.

D) none of the options

98) The Cadbury Code has not been legislated into law, and compliance with the code is

voluntary.

A) However, the London Stock Exchange (LSE) currently requires that each listed

company show whether the company is in compliance with the code and explain why if it is not.

B) This “comply or explain” approach has apparently persuaded many companies to

comply rather than explain.

C) Currently, 90 percent of all LSE-listed companies have adopted the Cadbury Code.

D) all of the options

99) Following the adoption of the Cadbury Code of Best Practice joint CEO/COB positions

declined

Version 1 31

A) from 27 percent of the companies before the adoption to 15 percent afterwards.

B) from 37 percent of the companies before the adoption to 15 percent afterwards.

C) from 47 percent of the companies before the adoption to 15 percent afterwards.

D) from 57 percent of the companies before the adoption to 15 percent afterwards.

100) Following the adoption of the Cadbury Code of Best Practice,

A) joint CEO/COB (chief executive officer and chairman of the board) positions

declined.

B) there has been a significant impact on the internal governance mechanisms of U.K.

companies.

C) CEOs have become more sensitive to company performance, strengthening

managerial accountability and weakening managerial entrenchment.

D) all of the options

101) Even though compliance with the Cadbury Code of Best Practice is voluntary,

A) the Cadbury Code has made a significant impact on the internal governance

mechanisms of U.K. companies.

B) the job security of U.K. chief executives has become more sensitive to the company

performance, strengthening managerial accountability and weakening its entrenchment.

C) joint CEO/COB (chief executive officer and chairman of the board) positions

declined.

D) all of the options

102) The key requirements of the Cadbury Code of Best Practice state that

Version 1 32

A) boards of directors should include no more than three outside directors.

B) the positions of CEO and chairman of the board must be the same individual.

C) Both Answers A and B are correct

D) boards of directors should include at least three outside directors and the positions of

CEO and chairman of the board should not reside in the same individual.

103) The key requirements of the Cadbury Code of Best Practice state that

A) the compensation, nominating, and audit committees to be entirely composed of

independent directors.

B) the positions of CEO and chairman of the board should not reside in the same

individual.

C) listed companies to have boards of directors with a majority of independents.

D) none of the options

104) In May 2018, the U.S. congress passed a new law called the Economic Growth,

Regulatory Relief, and Consumer Protection act that significantly weakened which previous Act?

A) the Dodd-Frank Act

B) the Volker Rule Act

C) the previous Consumer Protection Act

D) none of the options

105) Countries with strong shareholder protection tend to have more valuable stock markets

and more companies listed on stock exchanges per capita than countries with weak protection.

⊚ true

⊚ false

Version 1 33

Answer Key

Test name: chapter 4

Version 1 34

Version 1 35

Version 1 36