Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

33) Explain the issues involved with the Fed acting as a lender of Last Resort (LLR).

34) Explain the causes of the U.S. Savings and Loans crisis of the early 1980s.

35) Explain the difficulties in regulating international banking.

36) "The internationalization of banking has weakened national safeguards against banking collapse, but

at the same time it has made the need for effective safeguards more urgent." Discuss.

37) Why did the Fed step in to organize a rescue for Long Term Capital Management (LTCM) in

September, 1998, rather than simply letting the trouble fund fail? Was the Fed's action necessary or

advisable?

38) What is securitization?

39) Who is the Basel Committee? Discuss both their involvement in the Concordat as well the role of

the Concordat in international banking.

21.4 How Well Have International Financial Markets Allocated Capital and Risk?

1) What are three things to measure for in evaluating the performance of the capital markets?

A) level of intertemporal trade, international trade, portfolio diversification

B) level of portfolio diversification, balanced capital accounts, global inflation

C) level of portfolio diversification, intertemporal trade, efficiency of foreign exchange

D) onshore-offshore interest rate parity, level of portfolio diversification, stability of eurocurrency

market

E) onshore-offshore interest rate parity, interest parity and foreign exchange, balanced capital accounts

2) In the Interest Parity Condition, Rt - R t = (

e

Et+1

- Et)/Et + xt, where Rt - R t is the interest rate

differential and (

e

Et+1

- Et)/Et is the expected change in the exchange rate, what does xt stand for if it

potentially is a market efficient difference between the two?

A) market inefficiency

B) risk premium

C) forecast error

D) tracking error

E) excessive volatility

3) Why might a country's savings rate have a high positive correlation to its investment rate?

A) A country's gains from intertemporal trade may have been large.

B) governments' regulation to avoid inflation

C) A country's savings rate and investment rate are generally not positively correlated but rather have

negative correlation.

D) governments' regulation to avoid large current account balances

E) A government has not practiced sufficient fiscal regulation.

4) Large differences in interest rates between countries would indicate that:

A) the global market is thriving.

B) there is good communication between countries about potential global investment opportunities.

C) there are unrealized gains from trade.

D) the market is in danger of collapse.

E) the supply growth exceeds the aggregate demand.

5) Statistical studies of the relationship between interest rates and later depreciation rates show that:

A) the interest difference has been a very bad predictor in the large swings of exchange rates.

B) the interest difference has been an accurate predictor in the large swings of exchange rates.

C) the interest difference has correctly predicted the direction in which exchange rates would change.

D) the interest difference has not yet been studied as a predictor in the large swings of exchange rates.

E) the interest difference is unrelated to the large swings of exchange rates.

6) Which of the following is true about exchange rates?

A) They should not be volatile because they will determine the economic climate.

B) They are generally more volatile than stock prices.

C) They are more volatile than several underlying factors that move them such as money supplies and

fiscal variables.

D) They should be volatile because to correct price signals they adjust quickly in response to economic

news, but they are generally less volatile than stock prices.

E) They never overreact to economic news.

7) Departures from interest parity

A) can be explained using theories of risk premium.

B) cannot be explained using theories of risk premium.

C) may or may not be able to be explained using theories of risk premium, more research is needed.

D) are completely unrelated to risk premium.

E) occur when risk premium is overcalculated.

8) A random walk model can more accurately predict exchange rates as compared to a sophisticated

forecast

A) always.

B) for forecasts up to a year away.

C) for forecasts longer than a year away.

D) never.

E) because of the predictability of exchange rates.

9) How well has the international capital market perform?

10) Explain why, according to Feldstein and Horioka, one should expect that domestic investment rates

diverge widely from saving rates.

11) Explain why large interest rate differences would be strong evidence of unrealized gains from trade.

12) Discuss studies based on the interest parity conditions.

40

13) Explain the forecast error, ut+1, in terms of:

(1) Its equation (what it is equal to)

(2) How it is used

(3) Its accuracy

14) Does the interest rate parity hold in each of the following cases? In case it does not hold, calculate

the risk premium.

A. Rt = 5, = 3, Et = 5, = 7

B. Rt = 6, = 3, Et = 5,

e

Et+1

= 7

C. Rt = 7, = 3, Et = 5,

e

Et+1

= 7

D. Rt = 8, = 3, Et = 5,

e

Et+1

= 7

E. Rt = 5, = 4, Et = 5,

e

Et+1

= 7

41

F. Rt = 5, = 5, Et = 5,

e

Et+1

= 7

G. Rt = 5, = 6, Et = 5,

e

Et+1

= 7

H. Rt = 5, = 3, Et = 6,

e

Et+1

= 7

I. Rt = 5, = 3, Et = 7,

e

Et+1

= 7

J. Rt = 5, = 3, Et = 8,

e

Et+1

= 7

K. Rt = 5, = 3, Et = 5,

e

Et+1

= 8

L. Rt = 5, = 3, Et = 5,

e

Et+1

= 9

M. Rt = 5, = 3, Et = 5, = 10

42

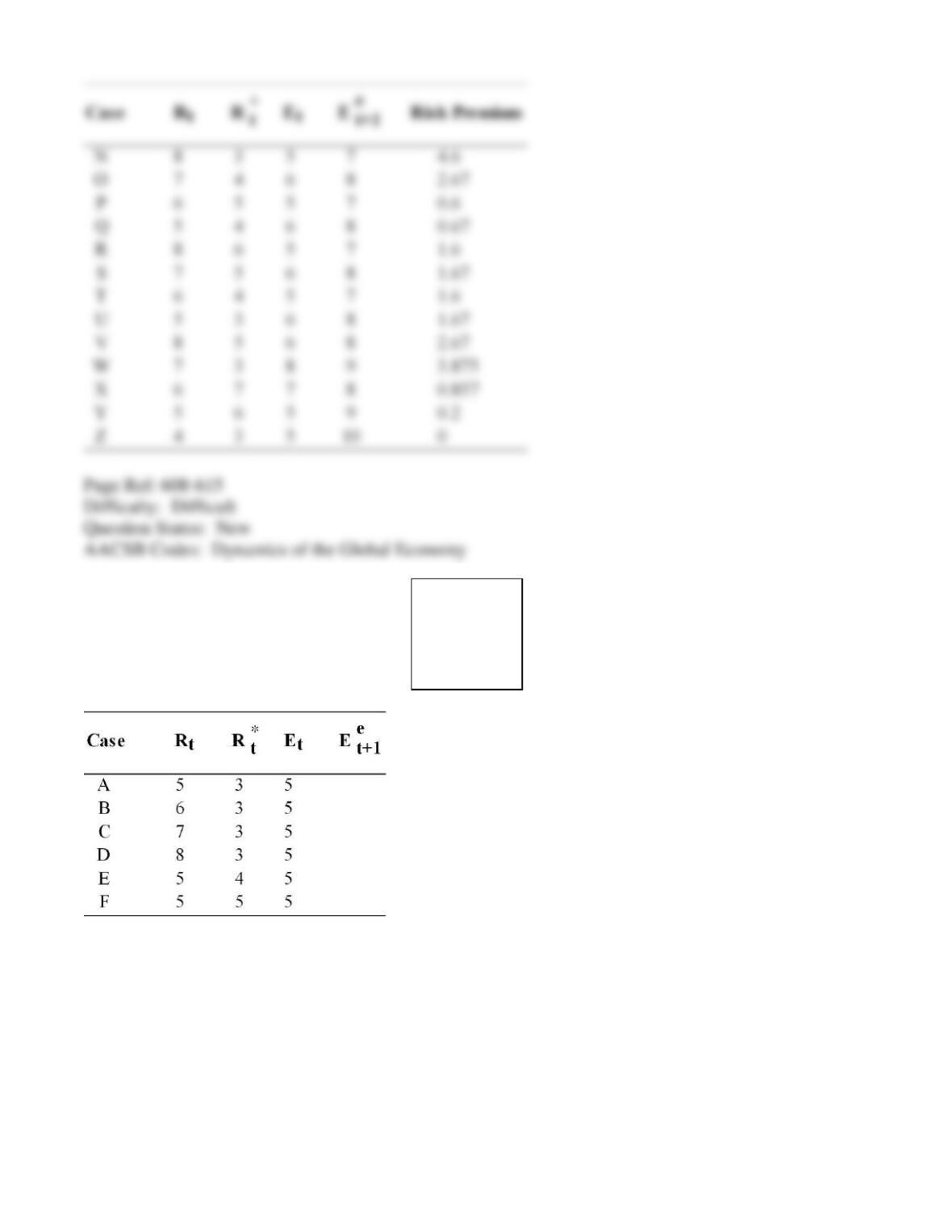

15) Does the interest rate parity hold in each of the following cases? In case it does not hold, calculate

the risk premium.

N. Rt = 8, = 3, Et = 5, = 7

O. Rt = 7, = 4, Et = 6, = 8

P. Rt = 6, = 5, Et = 5, = 7

Q. Rt = 5, = 4, Et = 6, = 8

R. Rt = 8, = 6, Et = 5, = 7

S. Rt = 7, = 5, Et = 6, = 8

43

T. Rt = 6, = 4, Et = 5, = 7

U. Rt = 5, = 3, Et = 6, = 8

V. Rt = 8, = 5, Et = 6, = 8

W. Rt = 7, = 3, Et = 8, = 9

X. Rt = 6, = 7, Et = 7, = 8

Y. Rt = 5, = 6, Et = 5, = 9

Z. Rt = 4, = 3, Et = 5, = 10

Answer:

44

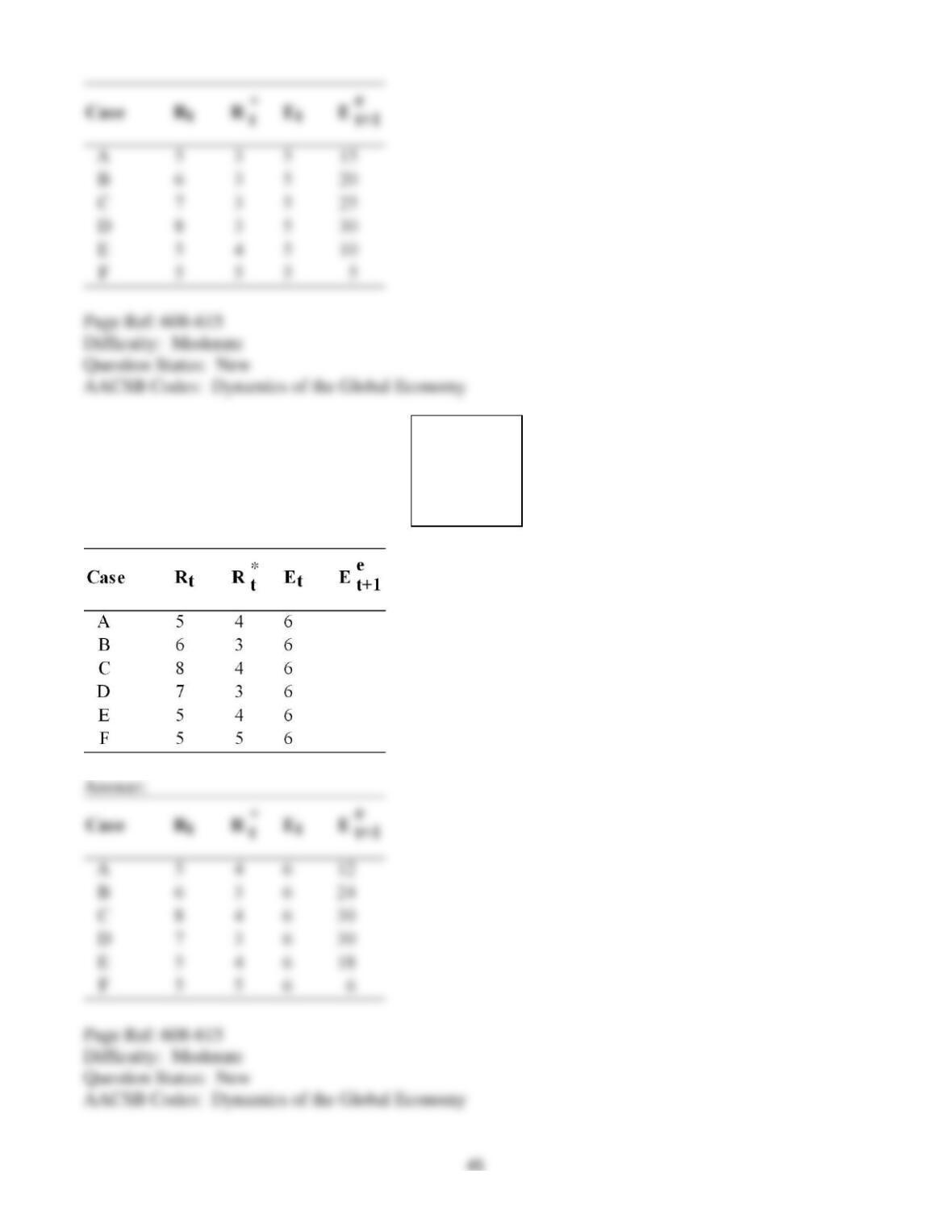

16) Assume interest parity holds. Calculate for each of the following cases.

Answer:

17) Assume interest parity holds. Calculate for each of the following cases.

46

18) Does the interest rate parity hold in each of the following cases by using the formula

Rt - Rt = (Ee+1 - Et)/Et ? In case it does not hold, calculate the risk premium.

1. Rt = 5, = 3, Et = 5, = 17

2. Rt = 6, = 4, Et = 5, = 5

3. Rt = 7, = 5, Et = 5, = 8

4. Rt = 8, = 3, Et = 5, = 15

5. Rt = 5, = 4, Et = 6, = 6

6. Rt = 5, = 5, Et = 3, = 10

7. Rt = 5, = 6, Et = 2, = 8

8. Rt = 5, = 3, Et = 0, = 20

47

9. Rt = 5, = 9, Et = 7, = 3

10. Rt = 5, = 10, Et = 8, = 7