Version 1 1

Student name:__________

1) The cost of capital is

A) the minimum rate of return an investment project must generate in order to pay its

financing costs.

B) the minimum rate of return an investment project must generate in order to pay its

financing costs plus a reasonable profit.

C) the maximum rate of return an investment project must generate in order to pay its

financing costs.

D) the maximum rate of return an investment project must generate in order to pay its

financing costs plus a reasonable profit.

2) For a firm that has both debt and equity in its capital structure, its financing cost can be

represented by the weighted average cost of capital that is computed by

A) weighing the pre-tax borrowing cost of the firm and the cost of equity capital, using

the debt as the weight.

B) weighing the after-tax borrowing cost of the firm and the cost of equity capital, using

the debt as the weight.

C) K = (1 − λ)Kl + λ (1 − τ)iwhere:

K = weighted average cost of capital

Kl = cost of equity capital for a leveraged firm

i = before-tax borrowing cost

τ = marginal corporate income tax rate

λ = debt-to-total-market-value ratio

D) Both B & C are correct.

3) In the notation of the book, K = (1 − λ)Kl + λ(1 − τ)i

Which of these is correct?

Version 1 2

A) The debt-to-equity ratio is λ

B) The tax rate is τ

C) The after-tax cost of debt capital is i

D) all of the options

4) In the notation of the book, K = (1 − λ)Kl + λ(1 − τ)i ; which of the following is correct?

A) The debt-to-total market value ratio is λ

B) The tax rate is i

C) The after-tax cost of debt capital is i

D) all of the options

5) In the notation of the book, K = (1 − λ)Kl + λ(1 − τ)i ; which of the following is correct?

A) The debt-to-equity ratio is λ

B) The cost of equity capital for a levered firm is K

C) The pre-tax cost of debt capital is i

D) all of the options

6) In the notation of the book, K = (1 − λ)Kl + λ(1 − τ)i ; which of the following is correct?

A) The debt-to-equity ratio is λ

B) The cost of equity capital for a levered firm is Kl

C) The after-tax cost of debt capital is i

D) all of the options

7) In the notation of the book, K = (1 − λ)Kl + λ(1 − τ)i ; which of the following is correct?

Version 1 3

A) The weighted average cost of capital for a levered firm is K

B) The tax rate is τ

C) The after-tax cost of debt capital is i

D) all of the options

8) At the optimal capital structure,

A) K = (1 − λ)Kl + λ(1 − τ)i will be minimized.

B) The debt-equity ratio will be equal to the debt-to-value ratio.

C) K = (1 − λ)Kl + λ(1 − τ)i will be maximized.

D) none of the options

9) Solve for the weighted average cost of capital.

10.60

%

=

K1

=

cost of equity capital for a leveraged firm

1/3

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

10) Solve for the weighted average cost of capital.

Version 1 4

11.20

%

=

K1

=

cost of equity capital for a leveraged firm

1/2

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

11) Solve for the weighted average cost of capital.

11.80

%

=

K1

=

cost of equity capital for a leveraged firm

3/5

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

12) Solve for the weighted average cost of capital.

12.40

%

=

K1

=

cost of equity capital for a leveraged firm

2/3

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

Version 1 5

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

13) Solve for the weighted average cost of capital.

13.00

%

=

K1

=

cost of equity capital for a leveraged firm

5/7

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

A) 8.67 percent

B) 7.60 percent

C) 7.33 percent

D) 7.14 percent

14) Solve for the weighted average cost of capital.

13.60

%

=

K1

=

cost of equity capital for a leveraged firm

3/4

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

Version 1 6

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

15) Solve for the weighted average cost of capital.

14.20

%

=

K1

=

cost of equity capital for a leveraged firm

7/9

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

16) Solve for the weighted average cost of capital.

15.40

%

=

K1

=

cost of equity capital for a leveraged firm

9/11

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

Version 1 7

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

17) Solve for the weighted average cost of capital.

16.00

%

=

K1

=

cost of equity capital for a leveraged firm

5/6

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

18) Solve for the weighted average cost of capital.

17.20

%

=

K1

=

cost of equity capital for a leveraged firm

6/7

=

λ

=

debt-to-total-market-value ratio

8.0

%

=

i

=

before-tax borrowing cost

40.0

%

=

τ

=

marginal corporate income tax rate

Version 1 8

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.57 percent

19) Solve for the weighted average cost of capital.

10.60

%

=

K1

1/3

=

λ

8.0

%

=

i

40.0

%

=

τ

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

20) Solve for the weighted average cost of capital.

11.20

%

=

K1

1/2

=

λ

8.0

%

=

i

40.0

%

=

τ

Version 1 9

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

21) Solve for the weighted average cost of capital.

11.80

%

=

K1

3/5

=

λ

8.0

%

=

i

40.0

%

=

τ

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

22) Solve for the weighted average cost of capital.

12.40

%

=

K1

2/3

=

λ

8.0

%

=

i

40.0

%

=

τ

Version 1 10

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.33 percent

23) Solve for the weighted average cost of capital.

13.00

%

=

K1

5/7

=

λ

8.0

%

=

i

40.0

%

=

τ

A) 8.67 percent

B) 8.00 percent

C) 7.60 percent

D) 7.14 percent

24) Solve for the weighted average cost of capital.

13.60

%

=

K1

3/4

=

λ

8.0

%

=

i

40.0

%

=

τ

Version 1 11

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

25) Solve for the weighted average cost of capital.

14.20

%

=

K1

7/9

=

λ

8.0

%

=

i

40.0

%

=

τ

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

26) Solve for the weighted average cost of capital.

15.40

%

=

K1

9/11

=

λ

8.0

%

=

i

40.0

%

=

τ

Version 1 12

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

27) Solve for the weighted average cost of capital.

16.00

%

=

K1

5/6

=

λ

8.0

%

=

i

40.0

%

=

τ

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.67 percent

28) Solve for the weighted average cost of capital.

17.20

%

=

K1

6/7

=

λ

8.0

%

=

i

40.0

%

=

τ

Version 1 13

A) 7.00 percent

B) 6.89 percent

C) 6.73 percent

D) 6.57 percent

29) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 1/2.

A) 1/3

B) 1/2

C) 3/5

D) 2/3

30) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 1.

A) 1/3

B) 1/2

C) 3/5

D) 2/3

31) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 1½.

A) 1/3

B) 1/2

C) 3/5

D) 2/3

32) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 2.

Version 1 14

A) 1/3

B) 1/2

C) 3/5

D) 2/3

33) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 2½.

A) 1/3

B) 1/2

C) 3/5

D) 5/7

34) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 2½.

A) 1/3

B) 1/2

C) 3/5

D) 5/7

35) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 3.

A) 3/4

B) 7/9

C) 4/5

D) 9/11

36) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 3½.

Version 1 15

A) 3/4

B) 7/9

C) 4/5

D) 9/11

37) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 4.

A) 3/4

B) 7/9

C) 4/5

D) 9/11

38) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 4½.

A) 3/4

B) 7/9

C) 4/5

D) 9/11

39) Find the debt-to-value ratio for a firm with a debt-to-equity ratio of 5.

A) 3/4

B) 7/9

C) 4/5

D) 5/6

40) Find the debt-to-equity ratio for a firm with a debt-to-total-value ratio of 1/2.

Version 1 16

A) 1

B) 2

C) 3

D) 4

41) Find the debt-to-equity ratio for a firm with a debt-to-total-value ratio of 2/3.

A) 1

B) 2

C) 3

D) 4

42) Find the debt-to-equity ratio for a firm with a debt-to-total-value ratio of 3/4

A) 1

B) 2

C) 3

D) 4

43) Find the debt-to-equity ratio for a firm with a debt-to-total-value ratio of 4/5.

A) 1

B) 2

C) 3

D) 4

44) Find the debt-to-equity ratio for a firm with a debt-to-total-value ratio of 5/6.

Version 1 17

A) 2

B) 3

C) 4

D) 5

45) Corporations are becoming multinational not only in the scope of their business activities

but also in their capital structure

A) by raising funds from domestic as well as government sources.

B) by raising funds from foreign as well as domestic sources.

C) This trend reflects not only a conscious effort on the part of firms to raise the cost of

capital by international sourcing of funds but also the ongoing liberalization and deregulation of

international financial markets that make them accessible for many firms.

D) by raising funds from foreign as well as domestic sources. This trend reflects not

only a conscious effort on the part of firms to raise the cost of capital by international sourcing of

funds, but also the ongoing liberalization and deregulation of international financial markets that

make them accessible for many firms.

46) Find the weighted average cost of capital for a firm that has a debt-to-equity ratio of 1½, a

tax rate of 34 percent, a levered cost of equity of 12 percent and an after-tax cost of debt of 8

percent.

A) 9.6 percent

B) 7.968 percent

C) 14 percent

D) none of the options

47) Find the weighted average cost of capital for a firm that has a debt-to-equity ratio of 1½, a

tax rate of 34 percent, a levered cost of equity of 12 percent and a pre-tax cost of debt of 10

percent.

Version 1 18

A) 9.6 percent

B) 7.968 percent

C) 8.76 percent

D) none of the options

48) Find the weighted average cost of capital for a firm that has a debt-to-equity ratio of 2, a

tax rate of 40 percent, a levered cost of equity of 12 percent and an after-tax cost of debt of 9

percent.

A) 7.6 percent

B) 7.968 percent

C) 10 percent

D) none of the options

49) Find the weighted average cost of capital for a firm that has a debt-to-equity ratio of 2, a

tax rate of 40 percent, a levered cost of equity of 12 percent and a pre-tax cost of debt of 9

percent.

A) 7.6 percent

B) 7.968 percent

C) 10 percent

D) none of the options

50) The cost of equity capital is

Version 1 19

A) the expected return on the firm’s stock that investors require.

B) frequently estimated by using the Capital Asset Pricing Model (CAPM).

C) generally considered to be a linear function of the systematic risk inherent in the

security.

D) all of the options

51) A reduced cost of equity capital increases the firm’s value

A) through revaluation of the firm’s existing cash flows from existing projects.

B) through increased investment as more projects become positive NPVs.

C) both of the options

D) none of the options

52) A value-maximizing firm would

A) undertake an investment project as long as the IRR exceeds the NPV.

B) undertake an investment project as long as the IRR is less than the cost of capital.

C) undertake an investment project as long as the IRR exceeds the cost of capital.

D) none of the options

53) Using the notation of the text, the CAPM states

A)

B)

C)

D) none of the options

Version 1 20

54) The common stock of Kansas City Power and Light has a beta of 0.80. The Treasury bill

rate is 4 percent and the market risk premium is 8 percent. What is their cost of equity capital?

A) 12.0 percent

B) 10.4 percent

C) 7.20 percent

D) 6.4 percent

55) The market risk premium

A) can be defined by the difference between the expected market return and the risk-

free rate.

B) is the reward for bearing nondiversifiable risk.

C) is the slope of the security market line.

D) can be expressed as

56) Compute the debt-to-equity ratio for a firm that has a debt-to-value ratio of 60 percent.

A) 1/3

B) 2/5

C) 3/2

D) none of the options

57) Compute the debt-to-total-value ratio for a firm that has a debt-to-equity ratio of 2.

A) 1/3

B) 2/5

C) 3/2

D) 2/3

Version 1 21

58) Micro Spinoffs, Inc., issued 20-year debt one year ago today at par value with a coupon

rate of 9 percent, paid annually. Today, the debt is selling at $1,050. If the firm’s tax rate is 34

percent, what is its after-tax cost of debt?

A) 9 percent

B) 8.46 percent

C) 5.94 percent

D) 5.58 percent

59) The firm’s tax rate is 34 percent. The firm’s pre-tax cost of debt is 8 percent; the firm’s

debt-to-equity ratio is 4; the risk-free rate is 3 percent; the beta of the firm’s common stock is 1.5;

the market risk premium is 9 percent. What is the firm’s cost of equity capital?

A) 33.33 percent

B) 10.85 percent

C) 13.12 percent

D) 16.50 percent

60) Systematic risk refers to

A) the diversifiable (company specific) risk of an asset.

B) the nondiversifiable (market) risk of an asset.

C) economic and political risk.

D) the risk that can be hedged.

61) The firm’s tax rate is 34 percent. The firm’s pre-tax cost of debt is 8 percent; the firm’s

debt-to-equity ratio is 4; the risk-free rate is 3 percent; the beta of the firm’s common stock is 1.5;

the market risk premium is 9 percent. Calculate the weighted average cost of capital.

Version 1 22

A) 33.33 percent

B) 8.09 percent

C) 9.02 percent

D) 16.5 percent

62) The formula for beta is

A)

B)

C)

D)

63) In the Capital Asset Pricing Model (CAPM), the term Beta, β, is

A) a measure of systematic risk inherent in a security.

B) calculated as the “covariance of future returns between a specific security and the

market portfolio” divided by the “variance of returns of the market portfolio.”

C) Both A & B are correct.

D) none of the options

Version 1 23

64) Assume that XYZ Corporation is a levered company with the following information:

Kl = cost of levered equity capital for XYZ = 13 percent

i = before-tax borrowing cost = 8 percent

t = marginal corporate income tax rate = 30 percent

If XYZ’s debt-to-total-market-value ratio is 40 percent, then its weighted average cost of capital,

K, is

A) 8 percent.

B) 9 percent.

C) 10 percent.

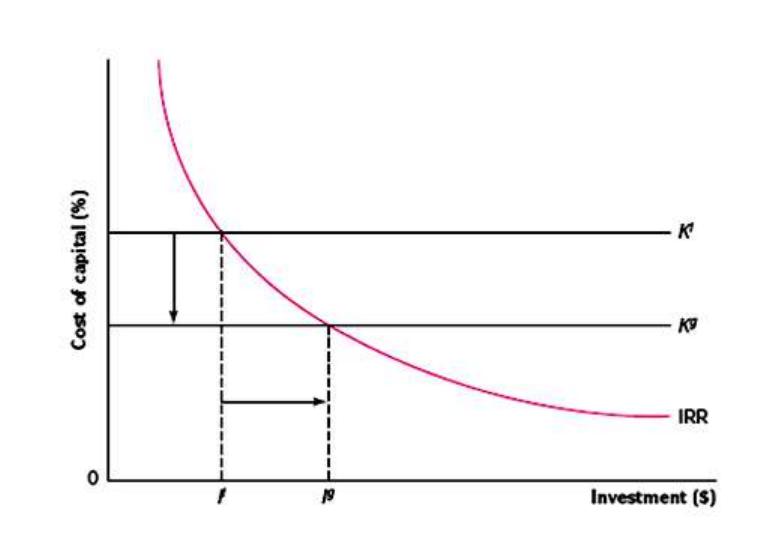

D) 12 percent.

65) In the graph,

Version 1 24

A) Kl and Kg represent, respectively, the cost of capital under international and local

capital structures; IRR represents the internal rate of return on investment projects; Il and Ig

represent, respectively, the optimal investment outlays under the alternative capital structures.

B) Kl and Kg represent, respectively, the cost of capital under local and international

capital structures; IRR represents the internal rate of return on investment projects; Il and Ig

represent the optimal investment outlays under the alternative capital structures.

C) both of the options

D) none of the options

66) Suppose that the firm’s cost of capital can be reduced from Kl under the local capital

structure to Kg under an internationalized capital structure. The take-away lesson from the graph

is that

Version 1 25

A) the firm can then increase its profitable investment outlay from Il to Ig,

contributing to the firm’s value.

B) a reduced cost of capital increases the firm’s value not only through increased

investments in new projects but also through revaluation of the cash flows from existing projects.

C) Kl and Kg represent, respectively, the cost of capital under local and international

capital structures; IRR represents the internal rate of return on investment projects; Il and Ig

represent the optimal investment outlays under the alternative capital structures.

D) all of the options

67) For a firm confronted with a fixed schedule of possible new investments, any policy that

lowers the firm’s cost of capital will increase the profitable capital expenditures the firm takes on

and increase the wealth of the firm’s shareholders. One such policy is

A) internationalizing the firm’s capital budgeting opportunities.

B) internationalizing the firm’s cost of capital.

C) investing in riskier projects financed with debt.

D) none of the options

68) For most countries and most firms, the domestic country beta

A) can be no lower than its world beta.

B) is normally much smaller than the world beta.

C) is normally much higher than the world beta.

D) is exactly equal to the world beta.

69) Suppose the domestic U.S. beta of IBM is 1.0, that is , and that the expected

return on the U.S. market portfolio is percent, and that the U.S. T-bill rate is 6 percent.

If the world beta measure of IBM is then we can say

Version 1 26

A) that if the U.S. markets are fully integrated with the rest of the world, IBM’s cost of

equity capital would be 20 percent lower than if U.S. markets were segmented.

B) that if the U.S. markets are fully integrated with the rest of the world, IBM’s cost of

equity capital would be 10 percent lower than if U.S. markets were segmented.

C) that if the U.S. markets are fully integrated with the rest of the world, IBM’s cost of

equity capital would be one-third lower than if U.S. markets were segmented.

D) none of the options

70) Studies suggest that international capital markets are not segmented anymore

A) and are therefore fully integrated.

B) but are not as yet fully integrated.

C) so cross-listing of shares will not lower a firm’s cost of capital.

D) none of the options

71) Compute the domestic country beta of Stansfield Bicycles as well as its world beta.

Correlation Coefficients

Stansfield

England

World

SD(%)

A) 1.00 and 0.80 respectively

B) 0.80 and 0.00 respectively

C) 4.50 and 4.00 respectively

D) none of the options

72) Suppose that the British stock market is segmented from the rest of the world. Using the

CAPM and a risk-free rate of 5 percent, estimate the equity cost of capital for Stansfield.

Correlation Coefficients

Version 1 27

Stansfield

England

World

SD(%)

A) 14 percent

B) 12 percent

C) 9 percent

D) none of the options

73) Suppose that the British stock market is integrated with the rest of the world and

Stansfield Company has made its shares tradable internationally via cross-listing on the NYSE.

Using the CAPM and a risk-free rate of 5 percent, estimate the equity cost of capital for

Stansfield.

Correlation Coefficients

Stansfield

England

World

SD(%)

A) 12 percent

B) 10.60 percent

C) 6.60 percent

D) None of the options

74) Assume that XYZ Corporation is a leveraged company with the following information:

Kl = cost of equity capital for XYZ = 13 percent

i = before-tax borrowing cost = 8 percent

t = marginal corporate income tax rate = 30 percent

If XYZ’s debt-to-total-market-value ratio is 40 percent, then its weighted average cost of capital,

K, is:

A) 8 percent

B) 9 percent

C) 10 percent

D) 12 percent

Version 1 28

75) Assume that XYZ Corporation is a leveraged company with the following information:

Kl = cost of equity capital for XYZ = 13 percent

i = before-tax borrowing cost = 8 percent

t = marginal corporate income tax rate = 30 percent

Calculate the debt-to-total-market-value ratio that would result in XYZ having a weighted

average cost of capital of 9.3 percent.

A) 35 percent

B) 40 percent

C) 45 percent

D) 50 percent

76) Assume that the risk-free rate of return is 4 percent, and the expected return on the

market portfolio is 10 percent. If the systematic risk inherent in the stock of ABC Corporation is

1.80, using the Capital Asset Pricing Model (CAPM) calculate the expected return of ABC.

A) 14.0 percent

B) 14.8 percent

C) 16.0 percent

D) 16.8 percent

77) In the real world, does the cost of capital differ among countries?

A) Yes

B) No

Version 1 29

78) Recent studies suggest that agency costs of managerial discretion are lower in Japan than

in the United States. This suggests that

A) the cost of capital can be lower in Japan than the United States, but only if

international financial markets are not fully integrated.

B) the cost of capital can be lower in Japan than the United States, even if international

financial markets are fully integrated.

C) the cost of capital will be higher in Japan than the United States, even if international

financial markets are fully integrated.

D) none of the options

79) Which of the following statements regarding cross-border listings of shares is not true?

A) Cross-listing shares may not be used as the “acquisition currency” for taking over

foreign companies.

B) Cross-listing may improve the company’s corporate governance and transparency.

C) Cross-listing can enhance the liquidity of the company’s stock.

D) Cross-listing enhances the visibility of the company’s name and its products in

foreign marketplaces.

Version 1 30

80) The following is an outline of certain potential benefits as well as costs associated with

the cross-border listings of stocks:

1. (i) the company can expand its potential investor base

2. (ii) issues involving the disclosure and listing requirements

3. (iii) creates a secondary market for the company’s shares

4. (iv) volatility spillover from the overseas markets

5. (v) liquidity

6. (vi) control of the company by foreigners

7. (vii) enhances the visibility of the company’s name and its products in foreign marketplaces

Which of the following represent all the potential benefits of the cross-border listings of

stocks?

A) (i), (ii), and (iii)

B) (ii), (iv), and (vi)

C) (i), (iii), (v), and (vii)

D) (iv), (v), (vi), and (vii)

Version 1 31

81) The following is an outline of certain potential benefits as well as costs associated with

the cross-border listings of stocks:

1. (i) the company can expand its potential investor base

2. (ii) issues involving the disclosure and listing requirements

3. (iii) creates a secondary market for the company’s shares

4. (iv) volatility spillover from the overseas markets

5. (v) liquidity

6. (vi) control of the company by foreigners

7. (vii) enhances the visibility of the company’s name and its products in foreign marketplaces

Which of the following represent all the potential costs of the cross-border listings of stocks?

A) (i), (ii), and (iii)

B) (ii), (iv), and (vi)

C) (i), (iii), (v), and (vii)

D) (iv), (v), (vi), and (vii)

82) Which of the following statement is not a downside to overseas listings?

A) It can be costly to meet the disclosure and listing requirements imposed by the

foreign exchange and regulatory authorities.

B) Controlling insiders may find it difficult to continue to derive private benefits once

the company is cross-listed on domestic exchanges

C) Once a company’s stock is traded in overseas markets, there can be volatility

spillover from those markets.

D) Once a company’s stock is made available to foreigners, they might acquire a

controlling interest and challenge the domestic control of the company.

Version 1 32

83) An extensive study by Karolyi (1996) reports

i) the share price reacts favorably to cross-border listings.

ii) the total postlisting trading volume increases on average, and, for many issues, home-market

trading volume also increases

iii) liquidity of trading in shares improves overall

iv) the stock’s exposure to domestic market risk is significantly reduced and is associated with

only a small increase in global market risk

v) cross-border listings resulted in a net reduction in the cost of equity capital of 114 basis points

on average

vi) stringent disclosure requirements are the greatest impediment to cross-border listings

A) i), ii), and iii).

B) iii), iv), and v)

C) iv), v), and vi)

D) i), ii), iii), iv), v), and vi)

84) A firm may cross-list its share to

A) establish a broader investor base for its stock.

B) establish name recognition in foreign capital markets, thus paving the way for the

firm to source new equity and debt capital from investors in different markets.

C) expose the firm’s name to a broader investor and consumer groups.

D) all of the options

85) Companies domiciled in countries with weak investor protection can reduce agency costs

between shareholders and management

Version 1 33

A) by moving to a better county.

B) by listing their stocks in countries with strong investor protection.

C) by voluntarily complying with the provisions of the U.S. Sarbanes-Oxley Act.

D) having a press conference and promising to be nice to their investors.

86) Benetton, an Italian clothier, is listed on the New York Stock Exchange.

A) This decision provides their shareholders with a higher degree of protection than is

available in Italy.

B) This decision can be a signal of the company’s commitment to shareholder rights.

C) This may make investors both in Italy and abroad more willing to provide capital and

to increase the value of the pre-existing shares.

D) all of the options

87) In the real world, many firms that have cross-listed their shares on the U.S. markets have

experienced a reduction in the cost of capital. This effect was greater for

A) Australian firms than for Canadian firms.

B) United States firms than for Mexican firms.

C) bonds than for stocks.

D) none of the options

88) To maximize the benefits of partial integration of capital markets

Version 1 34

A) a country should choose to internationally cross-list those assets that are least

correlated with the domestic market portfolio.

B) a country should choose to internationally cross-list those assets that are most highly

correlated with the domestic market portfolio.

C) a country should choose to internationally cross-list those assets that are uncorrelated

with the domestic market portfolio.

D) none of the options

89) One explanation for foreign equity ownership restrictions

A) is to make it difficult or impossible for foreigners to gain control of a domestic

company.

B) is to expropriate wealth from domestic shareholders.

C) is the arguments in favor of free trade.

D) none of the options

90) One likely effect of a company or government instituting foreign equity ownership

restrictions is

A) a decrease in domestic stock prices.

B) an increase in domestic stock prices.

C) a transfer of wealth from international shareholders to domestic shareholders.

D) none of the options

91) The pricing-to-market phenomenon

Version 1 35

A) describes the potential effect of foreign equity ownership restrictions.

B) describes the premium or discount faced by foreign shareholders relative to domestic

investors in the price of a stock due to legal restrictions imposed on foreign equity ownership.

C) was evidenced in the relative prices of Nestlé shares prior to November 17, 1988.

D) all of the options

92) The Nestlé episode shows

A) that political risk can exist in a country like Switzerland, long considered a haven

from such risk.

B) the pricing to market phenomenon exists.

C) it is possible to expropriate wealth from one group of shareholders and transfer it to

another group.

D) all of the options

93) Shares can exhibit a dual pricing or __________ phenomenon because of the constraint

in limiting desired foreign ownership, resulting in foreign and domestic investors facing different

market share prices.

A) cost-to-foreign

B) pricing-to-market

C) cost-to-market

D) currency-to-market

Version 1 36

94) The majority of publicly traded Swiss corporations have up to three classes of common

stock:

1.Registered stock

2. Voting bearer stock

3. Nonvoting bearer stock

Until 1989, foreigners were not allowed to buy registered stocks. In the case of Nestlé this had

the effect of

A) distorting the prices of registered stock downward.

B) distorting the prices of registered stock upward.

C) this had no effect on prices.

D) none of the options

95) With regard to the financial structure of a foreign subsidiary,

A) using local financing can reduce political risk.

B) a MNC that finances a foreign investment with home-country equity faces greater

risk of expropriation than if it had financed the investment with at least some local debt or

equity.

C) there may be advantages other than a reduction in political risk that encourage MNCs

to finance foreign subsidiaries with local money.

D) all of the options

96) According to Lessard and Shapiro (1984) which of the following is not an approach to

determining the subsidiary’s financial structure.

Version 1 37

A) Conform to the parent company’s norm.

B) Conform to the local norm of the country where the subsidiary operates.

C) Vary judiciously to capitalize on opportunities to lower taxes, reduce financing costs

and risks, and take advantage of various market imperfections.

D) none of the options

97) With regard to the financial structure of a foreign subsidiary

A) one option is to conform to the parent company’s capital structure.

B) one option is to conform to the local norm of the country where the subsidiary

operates.

C) one option is to vary judiciously to capitalize on opportunities to lower taxes, reduce

financing costs and risks, and take advantage of market imperfections.

D) all of the options

98) When the parent company is fully responsible for the subsidiary’s obligations,

A) the independent financial structure of the subsidiary is irrelevant.

B) potential creditors will examine the parent’s overall financial condition, not the

subsidiary’s.

C) the independent financial subsidiary can have the same capital structure as the parent.

D) all of the options

99) A recent study of MNCs suggests that when a foreign subsidiary’s obligations cannot be

met with locally generated revenues,

Version 1 38

A) parent firms bail out their subsidiaries regardless of circumstances.

B) that parent firms routinely allow subsidiaries to default.

C) most subsidiaries are financed almost entirely with banker’s acceptances.

D) none of the options

100) When the choice of financing a foreign subsidiary is between external debt and equity

financing

A) political risk considerations tend to favor the latter.

B) political risk considerations tend to favor the former.

C) political risk is separate from financial risk and so does not enter into a discussion of

debt equity ratios.

D) none of the options

101) When the choice of financing a foreign subsidiary is between external debt and equity

financing

A) many host governments tolerate the repatriation of funds in the form of interest much

better than dividends.

B) debt financing is generally secured from the World Bank, but only in developed

countries.

C) many host governments tolerate the repatriation of funds in the form of dividends

much better than interest.

D) none of the options

102) The parent company should decide the financing method for its own subsidiaries

Version 1 39

A) with a view toward minimizing the parent’s overall cost of capital.

B) by copying the norms of the host country.

C) with a view toward gaming the bankruptcy system of the host country.

D) none of the options

103) The required return on equity for a levered firm is 10.60 percent. The debt to equity ratio

is 1/2, the tax rate is 40 percent, the pre-tax cost of debt is 8 percent. Find the cost of capital if

this firm were financed entirely with equity.

A) 10 percent

B) 12 percent

C) 8.67 percent

D) none of the options

104) The required return on equity for an all-equity firm is 10.0 percent. They are considering

a change in capital structure to a debt-to-equity ratio of 1/2, the tax rate is 40 percent, the pre-tax

cost of debt is 8 percent. Find the new cost of capital if this firm changes capital structure.

A) 14.93 percent

B) 8.67 percent

C) 7.40 percent

D) none of the options

105) The required return on equity for an all-equity firm is 10.0 percent. They currently have a

beta of one and the risk-free rate is 5 percent and the market risk premium is 5 percent. They are

considering a change in capital structure to a debt-to-equity ratio of 1/2, the tax rate is 40

percent, the pre-tax cost of debt is 8 percent. Find the beta if this firm changes capital structure.

Version 1 40

A) 1.12 percent

B) 10 percent

C) 7.4 percent

D) none of the options

Version 1 41

Answer Key

Test name: chapter 17

Version 1 42

Version 1 43

Version 1 44