Version 1 1

Student name:__________

1) Under the investment dollar premium system,

A) U.K. residents received a premium over the prevailing commercial exchange rate

when they sold foreign securities and repatriated the funds to the U.K.

B) U.K. residents had to pay a premium over the prevailing commercial exchange rate

when they bought foreign currencies to invest in foreign securities.

C) none of the options

2) Foreign equities as a proportion of U.S. investors’ portfolio wealth rose from about 1

percent in the early 1980s to about _______ by 2018.

A) 10 percent

B) 25 percent

C) 35 percent

D) 67 percent

3) In the context of investments in securities (stocks and bonds), portfolio risk

diversification refers to

A) the time-honored adage “Don’t put all your eggs in one basket.”

B) investors’ ability to reduce portfolio risk by holding securities that are less than

perfectly correlated.

C) the fact that the less correlated the securities in a portfolio, the lower the portfolio

risk.

D) all of the options

Version 1 2

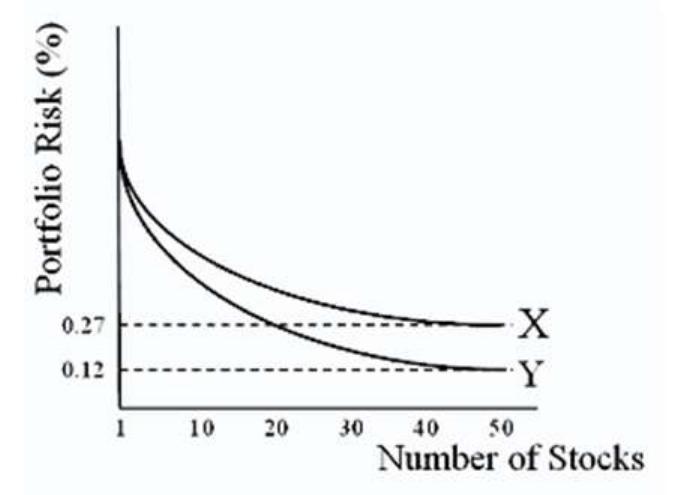

4) In the graph at shown, X and Y represent

A) U.S. stocks and global stocks, respectively.

B) global stocks and U.S. stocks, respectively.

C) systematic risk and unsystematic risk.

D) none of the options

5) Systematic risk is

A) diversifiable risk.

B) the risk that remains until investors fully diversify their portfolio holdings.

C) non-diversifiable risk and the risk that remains even after investors fully diversify

their portfolio holdings.

D) none of the options

6) Investors can reduce portfolio risk by

Version 1 3

A) holding securities that are less than perfectly correlated.

B) diversifying portfolio holdings internationally.

C) both A and B.

D) neither A or B.

7) Investors can enhance benefits from international diversification by using

A) industry funds.

B) factor funds.

C) style funds.

D) all of the options.

8) The “world beta” measures the

A) unsystematic risk.

B) sensitivity of returns on a security to world market movements.

C) risk-adjusted performance.

D) risk of default and bankruptcy.

9) The less correlated the securities in a portfolio,

A) the lower the portfolio risk.

B) the higher the portfolio risk.

C) the lower the unsystematic risk.

D) the higher the diversifiable risk.

10) Regarding the mechanics of international portfolio diversification, which statement is

true?

Version 1 4

A) Security returns are much less correlated across countries than within a county.

B) Security returns are more correlated across countries than within a county.

C) Security returns are about as equally correlated across countries as they are within a

county.

D) none of the options

11) Systematic risk

A) is also known as non-diversifiable risk.

B) is market risk.

C) refers to the risk that remains even after investors fully diversify their portfolio

holdings.

D) all of the options

12) A fully diversified U.S. portfolio is about

A) 75 percent as risky as a typical individual stock.

B) 27 percent as risky as a typical individual stock.

C) 12 percent as risky as a typical individual stock.

D) half as risky as a fully diversified international portfolio.

13) Studies show that international stock markets tend to move more closely together when

the volatility is higher. This finding suggests that

A) investors should liquidate their portfolio holdings during turbulent periods.

B) since investors need risk diversification most precisely when markets are turbulent,

there may be less benefit to international diversification for investors who liquidate their

portfolio holdings during turbulent periods.

C) this kind of correlation is why international portfolio diversification is smart for

today’s investor.

D) none of the options

Version 1 5

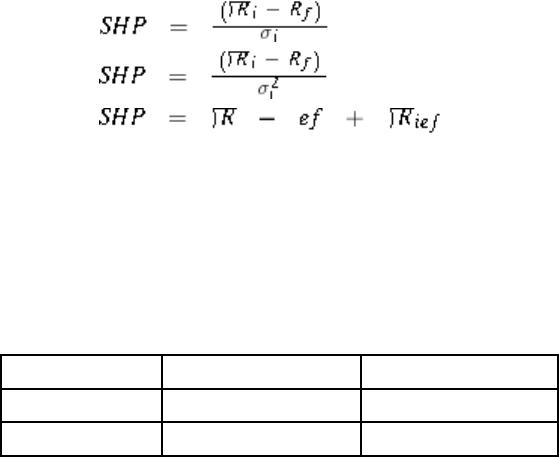

14) The “Sharpe performance measure” (SHP) is

A) a “risk-adjusted” performance measure.

B) the excess return (above and beyond the risk-free interest rate) per standard deviation

risk.

C) the sensitivity level of a national market to world market movements.

D) a “risk-adjusted” performance measure, as well as the excess return (above and

beyond the risk-free interest rate) per standard deviation risk.

15) The optimal international portfolio can be solved by maximizing the Sharpe ratio

A) SHP = [E(Rp) − Rf]/σp,

B) SHP = [R(Ep) − Rf]/σp,

C) SHP = [E(Rp) − σp,/Rf]

D) none of the options

16) The “Sharpe performance measure” (SHP) is

A)

B)

C)

D) none of the options

17) The mean and standard deviation (SD) of monthly returns, over a given period of time,

for the stock markets of two countries, X and Y, are:

Country

Mean(%)

SD(%)

X

1.57

4.87

Y

1.92

7.64

Version 1 6

Assuming that the monthly risk-free interest rate is 0.25 percent, the Sharpe performance

measures, SHP(X) and SHP(Y), and the performance ranks, respectively, for X and Y are:

A) SHP(X) = 0.271, rank = 1, and SHP(Y) = 0.219, rank = 2.

B) SHP(X) = 0.271, rank = 2, and SHP(Y) = 0.219, rank = 1.

C) SHP(X) = 18.84, rank = 1, and SHP(Y) = 23.04, rank = 2.

D) SHP(X) = 23.04, rank = 2, and SHP(Y) = 18.84, rank = 1.

18) With regard to the OIP,

A) the composition of the optimal international portfolio is identical for all investors,

regardless of home country.

B) the composition of the optimal international portfolio varies depending upon the

numeraire currency used to measure returns.

C) the composition of the optimal international portfolio is identical for all investors,

regardless of home country, if they hedge their risk with currency futures contracts.

D) the composition of the optimal international portfolio varies depending upon the

numeraire currency used to measure returns, and the composition of the optimal international

portfolio is identical for all investors (regardless of home country) if they hedge their risk with

currency futures contracts.

19) With regard to the OIP,

A) the composition of the optimal international portfolio is identical for all investors,

regardless of home country.

B) the OIP has more return and less risk for all investors, regardless of home country.

C) the composition of the optimal international portfolio is identical for all investors,

regardless of home country, if they hedge their risk with currency futures contracts.

D) none of the options

20) With regard to the OIP,

Version 1 7

A) the composition of the optimal international portfolio is identical for all investors,

regardless of home country.

B) the OIP has more return and less risk for all investors, regardless of home country.

C) the composition of the optimal international portfolio is identical for all investors of a

particular country, whether or not they hedge their risk with currency futures contracts.

D) none of the options

21) With regard to the OIP,

A) the optimal international portfolio contains investments from every country.

B) the OIP has more return and less risk for all investors.

C) the composition of the optimal international portfolio changes according to IRP.

D) none of the options

22) Emerald Energy is an oil exploration and production company that trades on the London

Stock Exchange. Assume that when purchased by an international investor the stock’s price and

the exchange rate were £5 and £0.64/$1.00 respectively. At selling time, one year after the

purchase date, they were £6 and £0.60/$1.00. Calculate the investor’s annual percentage rate of

return in terms of the U.S. dollars.

A) 0.20 percent

B) 20.00 percent

C) 1.28 percent

D) 28.00 percent

23) Emerald Energy is an oil exploration and production company that trades on the London

Stock Exchange. Over the past year, the stock has enjoyed a 20 percent return in pound terms,

but over the same period, the exchange rate has fallen from $2.00 = £1 to $1.80 = £1. Calculate

the investor’s annual percentage rate of return in terms of the U.S. dollars.

Version 1 8

A) 3.5 percent

B) 9.25 percent

C) 8 percent

D) There is not enough information to compute the investor’s annual percentage rate of

return in terms of the U.S. dollars.

24) Emerald Energy is an oil exploration and production company that trades on the London

Stock Exchange. Over the past year, the stock has gone from £50 per share to £55, but over the

same period, the dollar has appreciated from $1.21 = £1 to $1.10 = £1. Calculate the U.S.

investor’s annual percentage rate of return in terms of the U.S. dollars.

A) 3.5 percent

B) −1 percent

C) 0 percent

D) There is not enough information to compute the investor’s annual percentage rate of

return in terms of the U.S. dollars.

25) Bema Gold is an exploration and production company that trades on the Toronto Stock

Exchange. Assume that when purchased by an international investor the stock’s price and the

exchange rate were CAD5 and CAD1.0/USD0.72 respectively. At selling time, one year after the

purchase date, they were CAD6 and CAD1.0/USD1.0. Calculate the U.S. investor’s annual

percentage rate of return in terms of the U.S. dollars.

A) −13.60 percent

B) 66.67 percent

C) 38.89 percent

D) 28.00 percent

Version 1 9

26) The realized dollar returns for a U.S. resident investing in a foreign market will depend

on the return in the foreign market as well as on the exchange rate fluctuations between the

dollar and the foreign currency.

Calculate the variance of the monthly rate of return in dollar terms, if the variance of the

foreign market’s return (in terms of its own currency) is 1.14, the variance between the U.S.

dollar and the foreign currency is 17.64, the covariance is 2.34, and the contribution of the cross-

product term is 0.04.

A) 21.16

B) 23.50

C) 26.89

D) 28.65

27) Emerald Energy is an oil exploration and production company that trades on the London

Stock Exchange. Assume that when purchased by an international investor the stock’s price and

the exchange rate were £5 and £0.64/$1.00 respectively. At selling time, one year after purchase,

they were £6 and £0.60/$1.00. Suppose the investor had sold £5, the principal investment

amount, forward at the forward exchange rate of £0.60/$1.00 at the same time that the stock was

purchased. The dollar rate of return would be

A) 0.20 percent.

B) 20.00 percent.

C) 28.00 percent.

D) 30.00 percent.

28) Assume that you have invested $100,000 in British equities. When purchased, the stock’s

price and the exchange rate were £50 and £0.50/$1.00 respectively. At selling time, one year

after purchase, they were £60 and £0.60/$1.00. If the investor had sold £50,000 forward at the

forward exchange rate of £0.55/$1.00, the dollar rate of return would be

A) 10.90 percent.

B) 7.58 percent.

C) 28.00 percent.

D) 9.09 percent.

Version 1 10

29) Assume that you have invested $100,000 in Japanese equities. When purchased, the

stock’s price and the exchange rate were ¥100 and ¥100/$1.00 respectively. At selling time, one

year after purchase, they were ¥110 and ¥110/$1.00. If the investor had sold ¥10,000,000

forward at the forward exchange rate of ¥105/$1.00 the dollar rate of return would be

A) −27.27 percent.

B) 4.33 percent.

C) 28.00 percent.

D) −9.09 percent.

30) Assume that you have invested $100,000 in Japanese equities. When purchased the

stock’s price and the exchange rate were ¥100 and ¥100/$1.00 respectively. At selling time, one

year after purchase, they were ¥110 and ¥110/$1.00. The dollar rate of return would be

A) 0 percent.

B) 4.32 percent.

C) 28 percent.

D) −9.09 percent.

31) Suppose you are a euro-based investor who just sold Microsoft shares that you had

bought six months ago. You had invested €10,000 to buy Microsoft shares for $120 per share;

the exchange rate was $1.55 per euro. You sold the stock for $135 per share and converted the

dollar proceeds into euro at the exchange rate of $1.50 per euro. Compute the rate of return on

your investment in euro terms.

A) 12.50 percent

B) 16.25 percent

C) 28.00 percent

D) −9.09 percent

Version 1 11

32) Suppose you are a euro-based investor who just sold Microsoft shares that you had

bought six months ago. You had invested €10,000 to buy Microsoft shares for $120 per share;

the exchange rate was $1.55 per euro. You sold the stock for $135 per share and converted the

dollar proceeds into euro at the exchange rate of $1.50 per euro. How much of the return is due

to the exchange rate movement?

A) 3.76 percent

B) 3.33 percent

C) 12.50 percent

D) 16.25 percent

33) Which of the following is a true statement?

A) Generally, exchange rate volatility is greater than bond market volatility.

B) When investing in international bonds, it is essential to control exchange risk to

enhance the efficiency of international bond portfolios.

C) The real-world evidence suggests that investing in Swiss bonds largely amounts to

investing in Swiss currency.

D) all of the options

34) Compared with bond markets

A) the risk of investing in foreign stock markets is, to a lesser degree, attributable to

exchange rate uncertainty.

B) the risk of investing in foreign stock markets is, to a much greater degree,

attributable to exchange rate uncertainty.

C) exchange risk is lower than default risk and interest rate risk.

D) all of the options

Version 1 12

35) Exchange rate fluctuations contribute to the risk of foreign investment through three

possible channels

1. (i) the volatility of the investment due to the volatility of the exchange rate

2. (ii) the contribution of the cross-product term

3. (iii) its covariance with the local market returns

Which of the following contributes and accounts for most of the volatility?

A) (i) and (ii)

B) (ii) and (iii)

C) (i) and (iii)

D) only (ii)

36) In May 1995 when the exchange rate was 80 yen per dollar, Japan Life Insurance

Company invested ¥800,000,000 (i.e., $10,000,000) in pure-discount U.S. bonds. The

investment was liquidated one year later when the exchange rate was 110 yen per dollar. If the

rate of return earned on this investment was 46 percent in terms of yen, calculate the dollar

amount that the bonds were sold at.

A) $10,618,182

B) $10,720,000

C) $14,600,000

D) none of the options

37) Recent studies show that when investors control exchange risk by using currency forward

contracts,

A) they can substantially enhance the efficiency of international bond portfolios.

B) they can substantially enhance the efficiency of international stock portfolios.

C) the risk of investing in foreign stock markets can be completely hedged.

D) they can substantially enhance the efficiency of international bond and stock

portfolios.

Version 1 13

38) Recent studies show that when investors control exchange risk by using currency forward

contracts to hedge,

A) international bond portfolios outperform domestic bond portfolios.

B) international bond portfolios dominate domestic stock portfolios in terms of risk-

return efficiency.

C) international bond portfolios outperform domestic bond portfolios, and also dominate

domestic stock portfolios in terms of risk-return efficiency.

D) none of the options

39) Advantages of investing in U.S.-based international mutual funds include

A) lower transactions costs relative to direct investing.

B) circumvention of many legal and institution barriers to direct portfolio investment in

many foreign markets.

C) professional management, potentially expertise in security selection, definitely

record-keeping.

D) all of the options

40) By investing in international mutual funds, investors can

i) save any extra transaction and/or information costs they may have to incur when they

attempt to invest directly in foreign markets

ii) circumvent many legal and institutional barriers to direct portfolio investments in foreign

markets

iii) potentially benefit from the expertise of professional fund managers

A) i).

B) i) and ii)

C) ii) and iii).

D) i), ii), and iii)

Version 1 14

41) The record of investing in U.S.-based MNCs

A) shows that the share prices of U.S.-based MNCs behave much like those of domestic

firms, without providing effective international diversification.

B) shows that the share prices of U.S.-based MNCs behave much differently than those

of domestic firms, providing effective international diversification.

C) shows that the share prices of U.S.-based MNCs behave much like the currency

returns of their foreign markets.

D) none of the options

42) U.S.-based mutual funds known as country funds:

A) Invest in the government securities of different sovereign governments, giving risk-

free portfolios effective exchange rate diversification.

B) Invests exclusively in stocks of a single country.

C) Invests exclusively in government securities of a single country.

D) none of the options

43) Advantages of investing in mutual funds known as country funds include

A) speculation in a single foreign market at minimum cost.

B) using them as building blocks of a personal international portfolio.

C) diversification into emerging markets that are otherwise practically inaccessible.

D) all of the options

44) A closed-end mutual fund

A) invests in bonds of a particular maturity, and when they mature, the fund closes.

B) trades on a stock exchange just like a publicly traded corporation.

C) always trades at Net Asset Value.

D) all of the options

Version 1 15

45) With regard to the past price performance of closed-end mutual funds

A) most funds have traded at both a premium and a discount to NAV.

B) most funds trade on a stock exchange just like a publicly traded corporation.

C) suggests the risk-return characteristics can be quite different from those of the

securities underlying the fund.

D) all of the options

46) With regard to the past price performance of U.S.-based closed-end country funds,

A) most CECFs behave more like U.S. securities than their corresponding NAVs.

B) most CECFs have track records nearly identical to their currency returns.

C) most CECFs have stock betas of around zero when measured against the S&P 500.

D) none of the options

47) The majority of ADRS

A) are from such developed countries as Australia and Japan.

B) are from developing nations.

C) are from emerging markets.

D) are from both developing nations and emerging markets.

48) American Depository Receipt (ADRs) represent foreign stocks

A) denominated in U.S. dollars that trade on European stock exchanges.

B) denominated in U.S. dollars that trade on a U.S. stock exchange.

C) denominated in a foreign currency that trade on a U.S. stock exchange.

D) non-registered (bearer) securities.

Version 1 16

49) Hedge fund advisors typically receive a management fee, often ________ of the fund

asset value as compensation, plus performance fee that can be 20-25 percent of capital

appreciation.

A) 1 to 2 percent

B) 10 to 20 basis points

C) 10 percent

D) none of the options

50) Hedge fund advisors typically receive a “2-plus-twenty” management fee

A) meaning 2 percent per year of the assets under management, plus performance fee of

20 percent of any capital appreciation.

B) meaning 2 percent per year of the assets under management, plus performance fee of

20 basis points.

C) meaning 2 percent per year of the assets under management, plus performance fee of

20 percent of the excess return.

D) meaning 2 percent per year of the assets under management, plus performance fee 20

percent of gross return net of the risk-free rate.

51) Hedge funds

A) do not register as an investment company and are not subject to reporting or

disclosure requirements.

B) have experienced phenomenal growth in recent years.

C) tend to have relatively low correlations with various stock market benchmarks.

D) all of the options

52) Explanations for Home Bias include

Version 1 17

A) domestic securities may provide investors with certain extra services, such as

hedging against domestic inflation that foreign securities do not.

B) there may be barriers, formal or informal, to investing in foreign securities.

C) investors may face country-specific inflation in violation of PPP.

D) all of the options

53) When a country is more remote, with an uncommon language

A) domestic investors tend to invest more in the country’s market and less abroad.

B) foreign investors tend to invest less in the country’s market.

C) domestic investors tend to invest more in the country’s market.

D) Both A and B are correct.

54) The degree of home bias varies across investors.

A) Wealthier, more experienced, and sophisticated investors are less likely to exhibit

home bias.

B) Wealthier, more experienced, and sophisticated investors are more likely to exhibit

home bias.

C) Wealthier, more experienced, and sophisticated investors are less likely to invest in

foreign securities.

D) None of the options

55) Current research suggests that

A) investors can get more diversification with shares of domestic, large-cap stocks.

B) investors can get more diversification with shares of domestic, small-cap stocks.

C) investors can get more diversification with shares of foreign, large-cap stocks.

D) investors can get more diversification with shares of foreign, small-cap stocks.

Version 1 18

56) The return and variance of return to a U.S. dollar based investor from investing in

individual foreign security i are given by:

A) Ri$ = (1 + Ri)(1 + ei) − 1 and Var(Ri$) = Var(Ri)

B) Ri$ = Ri + ei and Var(Ri$) = Var(Ri) + Var(ei)

C) Ri$ = (1 + Ri)(1 + ei) – 1 and Var(Ri$) = Var(Ri) + Var(ei) + 2Cov(Ri, ei)

D) none of the options

57) Consider a simple exchange risk hedging strategy in which the U.S. dollar based investor

sells the expected foreign currency proceeds of a risky investment forward. Although the

expected foreign investment proceeds will be converted into U.S. dollars at the known forward

exchange rate under this strategy, the unexpected portion of the foreign investment proceeds

A) will have to be converted into U.S. dollars at the uncertain forward spot exchange

rate.

B) will have to be converted into U.S. dollars at the uncertain future spot exchange rate.

C) will have to be converted into U.S. dollars at the uncertain swap exchange rate.

D) none of the options

58) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock. One year after investment, the stock pays a £1 dividend, and

sells for £55 the exchange rate has changed from €1.25 per pound to €1.30 per pound.

59) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock using 50 percent margin. One year after investment, the stock

pays a £1 dividend, and sells for £54. In the meantime, the exchange rate has changed from

€1.25 per pound to €1.30 per pound. The interest on the margin loan is 1 percent per year. The

margin loan was denominated in pounds.

Version 1 19

60) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock. The stock pays a £0.30 quarterly dividend, and after one year

the investment sells for £55.20. The exchange rate has changed from €1.25 per pound to €1.30

per pound.

61) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock on margin with only 40 percent down and 60 percent borrowed.

The stock pays a £0.30 quarterly dividend, and after one year the investment sells for £54. The

exchange rate has changed from €1.25 per pound to €1.30 per pound. The interest on the margin

loan is 1 percent per year. The margin loan is denominated in pounds.

62) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock. One year after investment, the stock has no value since the firm

is bankrupt. Meanwhile the exchange rate has changed from €1.25 per pound to €1.30 per pound,

and he sold £8,000 forward at the forward rate of €1.28 per pound.

63) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock. One year after investment, the stock pays a $1 dividend, and

sells for $54. The exchange rate has changed from €0.625 per dollar to €0.6875 per dollar.

Version 1 20

64) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock using 50 percent margin. One year after investment, the stock

pays a $1 dividend and sells for $54. The exchange rate has changed from €0.625 per dollar to

€0.6875 per dollar. The interest on the margin loan is 1 percent per year. The margin loan was

denominated in dollars.

65) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock. The stock pays a $0.30 quarterly dividend, and after one

year the investment sells for $54. The exchange rate has changed from €0.625 per dollar to

€0.6875 per dollar.

66) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock on margin with only 40 percent down and 60 percent

borrowed. The stock pays a $0.30 quarterly dividend, and after one year the investment sells for

$54. The exchange rate has changed from €0.625 per dollar to €0.6875 per dollar. The interest on

the margin loan is 1 percent per year. The margin loan is denominated in dollars.

Version 1 21

67) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock. One year after investment, the stock pays a $1 dividend, and

sells for $54. The exchange rate has changed from €0.625 per dollar to €0.6875 per dollar.

68) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock. One year after investment, the stock pays a $1 dividend and

sells for $54. The exchange rate has changed from €0.625 per dollar to €0.6875 per dollar,

although he sold $16,000 forward at the forward rate of €0.65 per dollar.

69) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a $50 American stock. One year after investment, the stock has no value since the

firm is bankrupt. Meanwhile the exchange rate has changed from €0.625 per dollar to €0.6875

per dollar, and he sold $16,000 forward at the forward rate of €0.65 per dollar.

70) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock. One year after investment, the stock pays a £1 dividend, and

sells for £54. Spot exchange rates at the start and end of the year are shown in the table.

T = 0

T = 1

Euro

1.60

1.60

Pound

2.00

2.08

Version 1 22

71) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock using 50 percent margin. One year after investment, the stock

pays a £1 dividend, and sells for £54. The interest on the margin loan is 1 percent per year. The

margin loan was denominated in pounds.

T = 0

T = 1

Euro

1.60

1.60

Pound

2.00

2.08

72) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock. The stock pays a £0.30 quarterly dividend, and after one year

the investment sells for £54.

T = 0

T = 1

Euro

1.60

1.60

Pound

2.00

2.08

Version 1 23

73) Calculate the euro-based return an Italian investor would have realized by investing

€10,000 into a £50 British stock on margin with only 40 percent down and 60 percent borrowed.

The stock pays a £0.30 quarterly dividend, and after one year the investment sells for £54. The

interest on the margin loan is 1 percent per year. The margin loan is denominated in pounds.

Spot dollar exchange rates at the start and end of the year are shown in the table.

T = 0

T = 1

Euro

1.60

1.60

Pound

2.00

2.08

74) The stock market of country A has an expected return of 5 percent, and standard

deviation of expected return of 8 percent. The stock market of country B has an expected return

of 15 percent and standard deviation of expected return of 10 percent.

Find the expected return of a portfolio with half invested in A and half invested in B.

75) The stock market of country A has an expected return of 5 percent, and standard

deviation of expected return of 8 percent. The stock market of country B has an expected return

of 15 percent and standard deviation of expected return of 10 percent.

Assume that the correlation of expected return between A and B is negative 1. Calculate the

standard deviation of expected return of a portfolio with half invested in A and half invested in

B.

Version 1 24

76) The stock market of country A has an expected return of 5 percent, and standard

deviation of expected return of 8 percent. The stock market of country B has an expected return

of 15 percent and standard deviation of expected return of 10 percent.

Find the Global Minimum Variance Portfolio.

77) The stock market of country A has an expected return of 8 percent, and standard

deviation of expected return of 5 percent. The stock market of country B has an expected return

of 16 percent and standard deviation of expected return of 10 percent.

Find the expected return of a portfolio with half invested in A and half invested in B.

78) The stock market of country A has an expected return of 8 percent, and standard

deviation of expected return of 5 percent. The stock market of country B has an expected return

of 16 percent and standard deviation of expected return of 10 percent.

Assume that the correlation of expected return between A and B is negative 1. Calculate the

standard deviation of expected return of a portfolio with half invested in A and half invested in

B.

79) The stock market of country A has an expected return of 8 percent, and standard

deviation of expected return of 5 percent. The stock market of country B has an expected return

of 16 percent and standard deviation of expected return of 10 percent.

Assume that the correlation of expected returns between A and B is negative 1.

Is it reasonable to conclude that your portfolio is on the efficient frontier? If not, then prove

your point by finding just one portfolio weighting between A and B that offers more return with

less risk. If you think it is on the efficient frontier, why do you think this?

Version 1 25

80) The stock market of country A has an expected return of 8 percent, and standard

deviation of expected return of 5 percent. The stock market of country B has an expected return

of 16 percent and standard deviation of expected return of 10 percent.

Find the Global Minimum Variance Portfolio.

81) The stock market of country A has an expected return of 5 percent, and a standard

deviation of expected return of 8 percent. The stock market of country B has an expected return

of 15 percent and a standard deviation of expected return of 10 percent.

Calculate the expected return of a portfolio that is half invested in A and half in B.

82) The stock market of country A has an expected return of 5 percent, and a standard

deviation of expected return of 8 percent. The stock market of country B has an expected return

of 15 percent and a standard deviation of expected return of 10 percent.

Assume that the correlation of expected return between security A and B is 0.2. Calculate the

standard deviation of expected return of a portfolio that has half of its money invested in A and

half in B.

Version 1 26

83) The stock market of country A has an expected return of 5 percent, and a standard

deviation of expected return of 8 percent. The stock market of country B has an expected return

of 15 percent and a standard deviation of expected return of 10 percent.

Is it reasonable to conclude that your portfolio is on the efficient frontier? If not, then prove

your point by finding just one portfolio weighting between A and B that offers more return with

less risk. If you think it is on the efficient frontier, why do you think this? Either way, your

answer should include verification.

Version 1 27

Answer Key

Test name: chapter 15

Version 1 28

Version 1 29