CHAPTER 13—MECHANISMS OF INTERNATIONAL ADJUSTMENT

MULTIPLE CHOICE

1. Which of the following does not represent an automatic adjustment in balance-of-payments

disequilibrium? Variations in:

a.

Domestic income

b.

Foreign prices

c.

Domestic prices

d.

Foreign par values

2. The balance-of-payments adjustment mechanism developed during the 1700s by the English

economist David Hume is the:

a.

Income-adjustment mechanism

b.

Flexible-exchange-rate-adjustment mechanism

c.

Price-adjustment mechanism

d.

Rank-reserve-adjustment mechanism

3. Which chain of events would promote payments equilibrium for a surplus nation, according to the

price-adjustment mechanism?

a.

Increasing money supply—increasing domestic prices—rising imports—falling exports

b.

Increasing money supply—falling domestic prices—rising imports—falling exports

c.

Decreasing money supply—increasing domestic prices—falling imports—rising exports

d.

Decreasing money supply—decreasing domestic prices—falling imports—rising exports

4. Which chain of events would promote payments equilibrium for a deficit nation, according to the

price-adjustment mechanism?

a.

Increasing money supply—increasing domestic prices—rising imports—falling exports

b.

Increasing money supply—falling domestic prices—rising imports—falling exports

c.

Decreasing money supply—increasing domestic prices—falling imports—rising exports

d.

Decreasing money supply—decreasing domestic prices—falling imports—rising exports

5. During the gold standard era, central bankers agreed to react positively to international gold flows so

as to reinforce the automatic adjustment mechanism. Which of the following best represents the above

statement?

a.

Income-adjustment mechanism

b.

Price-adjustment mechanism

c.

Rules of the game

d.

Discretionary fiscal policy

6. During the gold standard era, the “rules of the game” suggested that:

a.

Surplus countries should increase their money supplies

b.

Deficit countries should increase their money supplies

c.

Surplus and deficit countries should increase their money supplies

d.

Surplus and deficit countries should decrease their money supplies

7. Which of the following balance-of-payments adjustment mechanisms is most closely related to the

quantity theory of money?

a.

Income-adjustment mechanism

b.

Price-adjustment mechanism

c.

Interest-rate-adjustment mechanism

d.

Output-adjustment mechanism

8. Under the gold standard, a surplus nation facing a gold inflow and an increase in its money supply

would also experience a:

a.

Rise in its interest rate and a short-term financial inflow

b.

Rise in its interest rate and a short-term financial outflow

c.

Fall in its interest rate and a short-term financial inflow

d.

Fall in its interest rate and a short-term financial outflow

9. Under the gold standard, a deficit nation facing a gold outflow and a decrease in its money supply

would also experience a:

a.

Rise in its interest rate and a short-term financial inflow

b.

Rise in its interest rate and a short-term financial outflow

c.

Fall in its interest rate and a short-term financial inflow

d.

Fall in its interest rate and a short-term financial outflow

10. Assume that Canada initially faces payments equilibrium in its merchandise trade account as well as in

its capital and financial account. Now suppose that Canadian interest rates increase to levels higher

than those abroad. For Canada, this tends to promote:

a.

Net financial inflows

b.

Net financial outflows

c.

Net merchandise exports

d.

Net merchandise imports

11. Assume that Canada initially faces payments equilibrium in its merchandise trade account as well as in

its capital and financial account. Now suppose that Canadian interest rates fall to levels below those

abroad. For Canada, this tends to promote:

a.

Net financial inflows

b.

Net financial outflows

c.

Net merchandise exports

d.

Net merchandise imports

12. Suppose the United States levies an interest equalization tax, which taxes Americans on dividend and

interest income from foreign securities. Such a tax would be intended to:

a.

Encourage financial movements from the United States to overseas

b.

Discourage financial movements from the United States to overseas

c.

Discourage financial movements from overseas to the United States

d.

None of the above

13. Assume that interest rates on comparable securities are identical in the United States and foreign

countries. Now suppose that investors anticipate that in the future the U.S. dollar will appreciate

against foreign currencies. Investment funds would thus be expected to:

a.

Flow from the United States to foreign countries

b.

Flow from foreign countries to the United States

c.

Remain totally in foreign countries

d.

Not be affected by the expected dollar appreciation

14. Suppose Japan increases its imports from Sweden, leading to a rise in Sweden’s exports and income

level. With a higher income level, Sweden imports more goods from Japan. Thus a change in imports

in Japan results in a feedback effect on its exports. This process is best referred to as the:

a.

Monetary approach to balance-of-payments adjustment

b.

Discretionary income adjustment process

c.

Foreign repercussion effect

d.

Price-specie flow mechanism

Exhibit 13.1

15. Refer to Exhibit 13.1. The value of the multiplier for the United States equals:

a.

2

b.

3

c.

4

d.

5

16. Refer to Exhibit 13.1. The change in the level of U.S. income resulting from the additional investment

spending equals

a.

$20 billion

b.

$30 billion

c.

$40 billion

d.

$50 billion

17. Refer to Exhibit 13.1. The change in the level of U.S. imports resulting from the rise in U.S. income

equals:

a.

$5 billion

b.

$10 billion

c.

$15 billion

d.

$20 billion

18. The monetary approach to balance-of-payments adjustments suggests that all payments deficits are the

result of:

a.

Too high interest rates in the home country

b.

Too low interest rates in the home country

c.

Excess money supply over money demand in the home country

d.

Excess money demand over money supply in the home country

19. The monetary approach to balance-of-payments adjustments suggests that all payments surpluses are

the result of:

a.

Too high interest rates in the home country

b.

Too low interest rates in the home country

c.

Excess money supply over money demand in the home country

d.

Excess money demand over money supply in the home country

20. Starting from a position where the nation’s money demand equals the money supply, and its balance of

payments is in equilibrium, economic theory suggests that the nation’s balance of payments would

move into a deficit position if there occurred in the nation a:

a.

Decrease in the money supply

b.

Increase in the money demand

c.

Decrease in the money demand

d.

None of the above

21. Which approach to balance-of-payments adjustment suggests that balance-of-payments surpluses are

the result of excess money demand in the home country?

a.

Absorption approach

b.

Elasticities approach

c.

Monetary approach

d.

Purchasing-power-parity approach

22. According to the “rules of the game” of the gold standard era, a country’s central bank agreed to react

to international gold flows so as to:

a.

Officially devalue a currency during eras of payments surpluses

b.

Officially revalue a currency during eras of payments deficits

c.

Offset the automatic-adjustment mechanism (e.g., prices)

d.

Reinforce the automatic-adjustment mechanism

23. According to the quantity theory of money, a change in the domestic money supply will bring about:

a.

Inverse and proportionate changes in the price level

b.

Inverse and less-than-proportionate changes in the price level

c.

Direct and proportionate changes in the price level

d.

Direct and less-than-proportionate changes in the price level

24. The formulation of the so-called income adjustment mechanism is associated with:

a.

Adam Smith

b.

David Ricardo

c.

David Hume

d.

John Maynard Keynes

25. The value of the foreign trade multiplier equals the reciprocal of the sum of the marginal propensities

to:

a.

Save plus import

b.

Import plus invest

c.

Consume plus export

d.

Save plus import

26. Starting from a position where the nation’s money demand equals the money supply and its balance of

payments is in equilibrium, economic theory suggests that the nation’s balance of payments would

move into a deficit position if there occurred in the nation:

a.

An increase in the money supply

b.

A decrease in the money supply

c.

An increase in money demand

d.

None of the above

27. Starting from a position where the nation’s money demand equals the money supply and its balance of

payments is in equilibrium, economic theory suggests that the nation’s balance of payments would

move into a surplus position if there occurred in the nation:

a.

A decrease in the money supply

b.

An increase in the money supply

c.

A decrease in the money demand

d.

None of the above

28. Starting from a position where the nation’s money demand equals the money supply and its balance of

payments is in equilibrium, economic theory suggests that the nation’s balance of payments would

move into a surplus position if there occurred in the nation:

a.

An increase in the money demand

b.

A decrease in the money demand

c.

An increase in the money supply

d.

None of the above

29. Assume identical interest rates on comparable securities in the United States and foreign countries.

Suppose investors anticipate that in the future the U.S. dollar will depreciate against foreign

currencies. Investment funds would tend to:

a.

Flow from the United States to foreign countries

b.

Flow from foreign countries to the United States

c.

Remain totally in foreign countries

d.

Remain totally in the United States

30. Suppose that rising U.S. income leads to higher sales and profits in the United States. This would

likely result in:

a.

Increasing portfolio investment into the United States

b.

Decreasing portfolio investment into the United States

c.

Increasing direct investment into the United States

d.

Decreasing direct investment into the United States

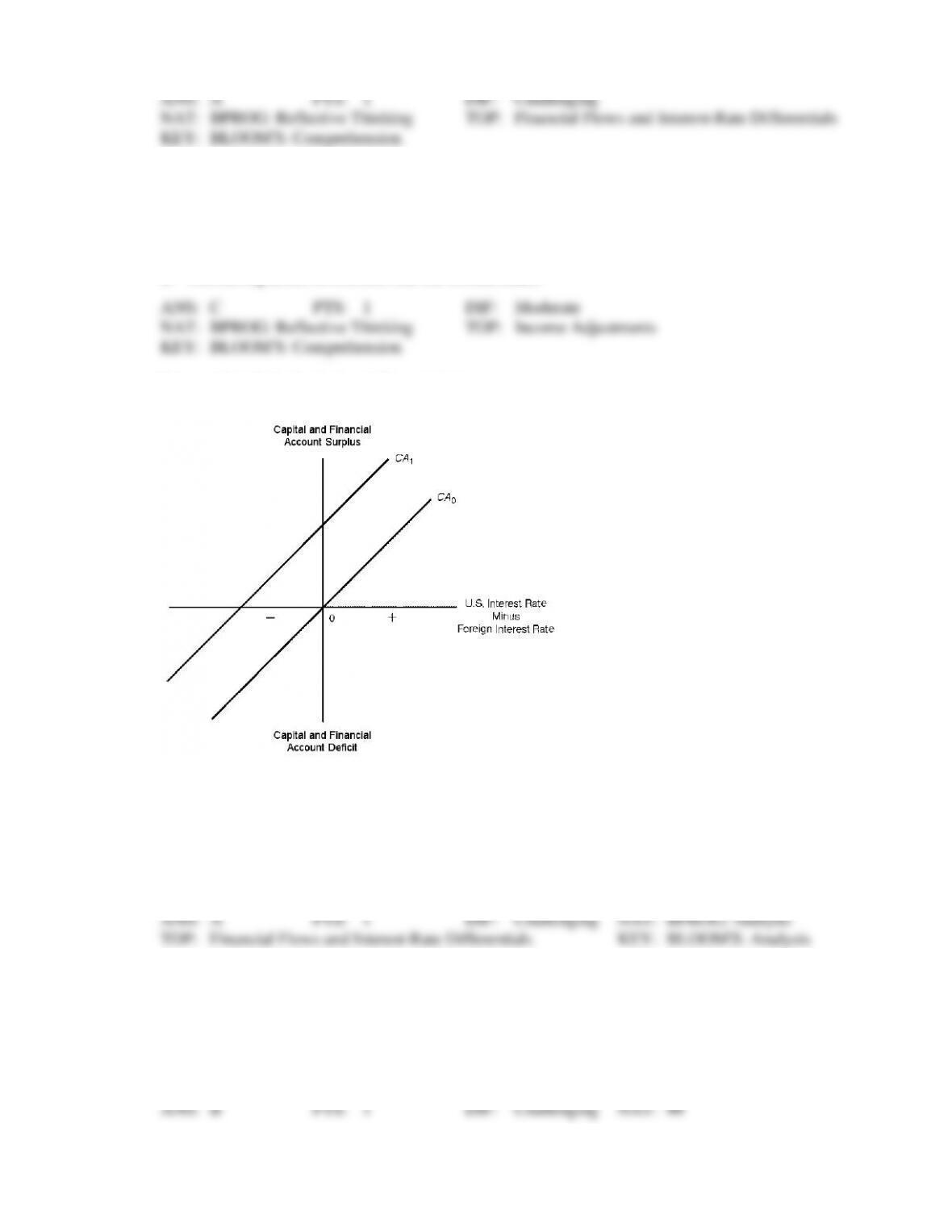

Figure 13.1. U.S. Capital and Financial Account

31. Refer to Figure 13.1. Upward movements along U.S. capital and financial account schedule CA0

would be caused by:

a.

U.S. interest rates rising relative to foreign interest rates

b.

U.S. interest rates falling relative to foreign interest rates

c.

Taxes placed on income earned by U.S. residents from their foreign investments

d.

Taxes placed on income earned by foreign residents from their U.S. investments

32. Refer to Figure 13.1. Downward movements along U.S. capital and financial account schedule CA0

would be caused by:

a.

U.S. interest rates rising relative to foreign interest rates

b.

U.S. interest rates falling relative to foreign interest rates

c.

Taxes placed on income earned by U.S. residents from their foreign investments

d.

Taxes placed on income earned by foreign residents from their U.S. investments

33. Refer to Figure 13.1. The U.S. capital and financial account schedule would shift upward from CA0 to

CA1 if:

a.

U.S. interest rates exceeded foreign interest rates

b.

Foreign interest rates exceeded U.S. interest rates

c.

Taxes were placed on income earned by U.S. residents from their foreign investments

d.

Taxes were placed on income earned by foreign residents from their U.S. investments

34. Refer to Figure 13.1. The U.S. capital and financial account schedule would shift upward from CA0 to

CA1 if:

a.

U.S. residents receive subsidies to invest in foreign nations

b.

U.S. interest rates rise relative to foreign interest rates

c.

Taxes are reduced on income earned by U.S. residents from their foreign investments

d.

Expected profits decline on U.S. investments in foreign manufacturing

35. Refer to Figure 13.1. The U.S. capital and financial account schedule would shift upward from CA0 to

CA1 if:

a.

U.S. political stability improves relative to foreign political stability

b.

U.S. interest rates rise relative to foreign interest rates

c.

Taxes are placed on income earned by U.S. residents from foreign investments

d.

Restrictions are imposed on international loans granted by foreign banks

36. Refer to Figure 13.1. U.S. capital and financial account schedule CA0 would shift upwards, or

downwards, for all of the following reasons except:

a.

U.S. residents being taxed on income earned from foreign investments

b.

U.S. banks being restricted on loans that can be made abroad

c.

U.S. political stability changing relative to foreign political stability

d.

U.S. interest rates changing relative to foreign interest rates

Table 13.1. Canada‘s Saving, Investment, Import, and Export Functions (in billions of dollars)

Under a System of Fixed Exchange Rates

Export Function

X = 3000

Investment Function

I = 1000

Saving Function

S = -1000 + 0.2Y

Import Function

M = 500 + 0.25Y

37. Referring to Table 13.1, if Canada’s income rises by $200 billion, saving would rise by:

a.

$10 billion

b.

$20 billion

c.

$30 billion

d.

$40 billion

38. Referring to Table 13.1, if Canada’s income rises by $200 billion, imports would rise by:

a.

$50 billion

b.

$75 billion

c.

$100 billion

d.

$125 billion

39. Referring to Table 13.1, Canada’s foreign trade multiplier equals:

a.

1.75

b.

2.05

c.

2.22

d.

2.64

40. Referring to Table 13.1, Canada’s equilibrium level of income is:

a.

$8000 billion

b.

$9000 billion

c.

$10,000 billion

d.

$11,000 billion

41. Refer to Table 13.1. If improved business optimism leads to increases in Canada’s planned investment

spending from $1000 billion to $1200 billion, Canada’s equilibrium income rises by approximately:

a.

$444 billion

b.

$555 billion

c.

$666 billion

d.

$777 billion

42. Refer to Table 13.1. If weak economic conditions abroad result in Canada’s exports falling from $3000

billion to $2500 billion, Canada’s equilibrium income falls by approximately:

a.

$888 billion

b.

$990 billion

c.

$1110 billion

d.

$1220 billion

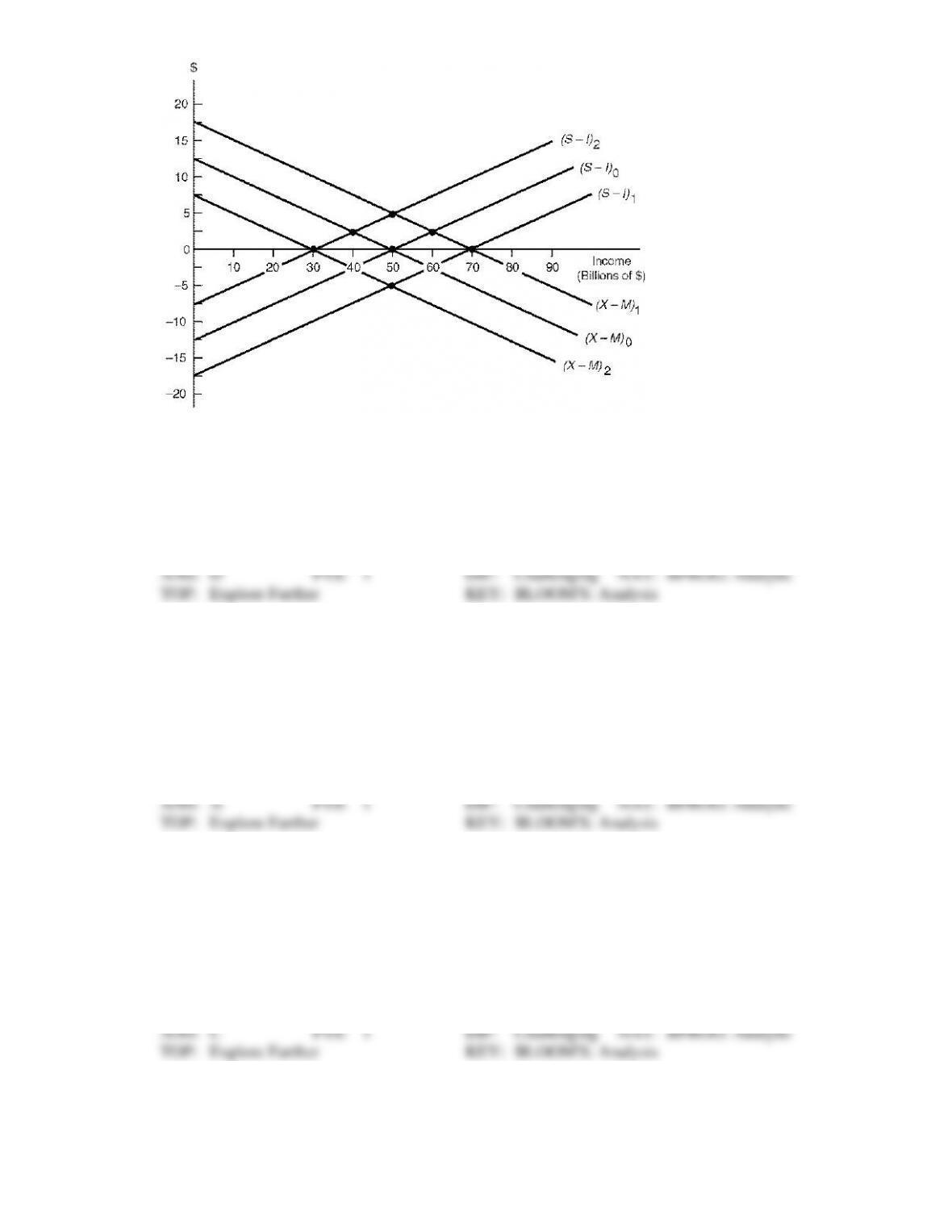

Figure 13.2. Australian Economy Under a Fixed Exchange Rate System

43. Refer to Figure 13.2. The slope of the (X-M) schedule and (S-I) schedule indicates that Australia’s

foreign trade multiplier is:

a.

0.5

b.

1.0

c.

1.5

d.

2.0

44. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S-I)0 intersects (X-M)0,

suppose that improving economic conditions abroad lead to an autonomous increase in Australian

exports of $5 billion. Australian income thus ____ which leads to Australia’s trade account moving to a

____.

a.

Rises to $60 billion, surplus of $2.5 billion

b.

Rises to $60 billion, surplus of $5 billion

c.

Falls to $40 billion, deficit of $2.5 billion

d.

Falls to $40 billion, deficit of $5 billion

45. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S- I)0 intersects (X-M)0,

suppose that worsening economic conditions abroad lead to an autonomous decrease in Australian

exports of $5 billion. Australian income thus ____ which leads to Australia’s trade account moving to a

____.

a.

Rises to $60 billion, surplus of $2.5 billion

b.

Rises to $60 billion, surplus of $5 billion

c.

Falls to $40 billion, deficit of $2.5 billion

d.

Falls to $40 billion, deficit of $5 billion

46. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S-I)0 intersects (X-M)0,

suppose that improving profit expectations lead to an autonomous increase in Australian investment of

$5 billion. Australian income thus ____ which leads to Australia’s trade account moving to a ____.

a.

Rises to $60 billion, deficit of $2.5 billion

b.

Rises to $60 billion, deficit of $5 billion

c.

Falls to $40 billion, surplus of $2.5 billion

d.

Falls to $40 billion, surplus of $5 billion

47. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S-I)0 intersects (X-M)0,

suppose that worsening profit expectations lead to an autonomous decrease in Australian investment of

$5 billion. Australian income thus ____ which leads to Australia’s trade account moving to a ____.

a.

Rises to $60 billion, deficit of $2.5 billion

b.

Rises to $60 billion, deficit of $5 billion

c.

Falls to $40 billion, surplus of $2.5 billion

d.

Falls to $40 billion, surplus of $5 billion

48. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S-I)0 intersects (X-M)0,

suppose that increased thriftiness leads to an autonomous increase in Australian saving of $5 billion.

Australian income thus ____ which leads to Australia’s trade account moving to a ____.

a.

Rises to $60 billion, deficit of $2.5 billion

b.

Rises to $60 billion, deficit of $5 billion

c.

Falls to $40 billion, surplus of $2.5 billion

d.

Falls to $40 billion, surplus of $5 billion

49. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S-I)0 intersects (X-M)0,

suppose that dwindling thriftiness leads to an autonomous decrease in Australian saving to $5 billion.

Australian income thus ____ which leads to Australia’s trade account moving to a ____.

a.

Rises to $60 billion, deficit of $2.5 billion

b.

Rises to $60 billion, deficit of $5 billion

c.

Falls to $40 billion, surplus of $2.5 billion

d.

Falls to $40 billion, surplus of $5 billion

50. Refer to Figure 13.2. Starting at equilibrium income $50 billion, where (S-I)0 intersects (X-M)0,

suppose that changing preferences lead to an autonomous increase in Australian imports of $5 billion.

Australian income thus ____ which leads to Australia’s trade account moving to a ____.

a.

Rises to $60 billion, surplus of $2.5 billion

b.

Rises to $60 billion, surplus of $5 billion

c.

Falls to $40 billion, deficit of $2.5 billion

d.

Falls to $40 billion, deficit of $5 billion