Quantity

Dollars

Quantity

of Pounds

per

of Pounds

Supplied

Pound

Demanded

1,000

2.00

200

800

1.80

400

600

1.60

600

400

1.40

800

200

1.20

1,000

54. Refer to Table 11.2. The equilibrium exchange rate equals:

a.

$1.20 per pound

b.

$1.40 per pound

c.

$1.60 per pound

d.

$1.80 per pound

55. Refer to Table 11.2. At the exchange rate of $1.40 per pound, there is an ____ for pounds. This

imbalance causes ____ in the price of the pound, which leads to ____ in the quantity of pounds

supplied and ____ in the quantity of pounds demanded.

a.

Excess supply, a decrease, an increase, a decrease

b.

Excess supply, an increase, a decrease, an increase

c.

Excess demand, an increase, an increase, a decrease

d.

Excess demand, an increase, a decrease, an increase

56. Refer to Table 11.2. At the exchange rate of $1.80 per pound, there is an ____ for pounds. This

imbalance causes ____ in the price of the pound, which leads to ____ in the quantity of pounds

supplied and ____ in the quantity of pounds demanded.

a.

Excess supply, a decrease, a decrease, an increase

b.

Excess supply, an increase, a decrease, an increase

c.

Excess demand, an increase, an increase, a decrease

d.

Excess demand, an increase, a decrease, an increase

Table 11.3. Key Currency Cross Rates

Dollar

Euro

Pound

Swiss Franc

Canada

1.5326

1.4400

2.2362

0.9790

Japan

124.48

116.96

181.63

79.515

Mexico

9.7410

9.1526

14.213

6.2223

Switzerland

1.5655

1.4709

2.2842

……….

U.K.

.68540

.6440

……….

.4378

Euro

1.06430

……….

1.5529

.67984

U.S.

……….

.9396

1.4591

.63877

57. Referring to Table 11.3, the cross exchange rate between the euro and Swiss franc is approximately:

a.

.68 euros per franc

b.

.68 francs per euro

c.

.64 euros per franc

d.

.64 francs per euro

58. Referring to Table 11.3, the yen cost of purchasing 100 British pounds is roughly:

a.

18,000 yen

b.

19,000 yen

c.

20,000 yen

d.

21,000 yen

Table 11.4. Forward Exchange Rates

U.S. Dollar Equivalent

Wednesday

Tuesday

Switzerland (Franc)

.6598

.6590

30-day Forward

.6592

.6585

90-day Forward

.6585

.6578

180-day Forward

.6577

.6572

59. Refer to Table 11.4. On Wednesday, the 30-day forward franc was selling at a:

a.

1 percent premium per annum against the dollar

b.

2 percent premium per annum against the dollar

c.

1 percent discount per annum against the dollar

d.

2 percent discount per annum against the dollar

60. Refer to Table 11.4. On Wednesday, the 90-day forward franc was selling at a:

a.

0.8 percent premium per annum against the dollar

b.

1.6 percent premium per annum against the dollar

c.

0.8 percent discount per annum against the dollar

d.

1.6 percent discount per annum against the dollar

61. Refer to Table 11.4. On Wednesday, the 180-day forward franc was selling at a:

a.

0.6 percent premium per annum against the dollar

b.

1.6 percent premium per annum against the dollar

c.

0.6 percent discount per annum against the dollar

d.

1.6 percent discount per annum against the dollar

62. Refer to Table 11.4. Comparing the franc’s forward rates against the franc’s spot rate, the exchange

market’s consensus is that over the period of a forward contract, the franc’s spot rate will:

a.

Depreciate against the dollar

b.

Appreciate against the dollar

c.

Remain constant against the dollar

d.

None of the above

63. The offer rate

a.

Is the price at which the bank is willing to sell a unit of foreign currency

b.

Is the price that the bank is willing to pay for a unit of foreign currency

c.

Is synonymous with the spread rate

d.

None of the above

64. When the dollar depreciates

a.

U.S. exporters tend to sell more goods in foreign markets

b.

U.S. consumers travel abroad more cheaply

c.

More foreign tourists can afford to visit the United States

d.

both a and c

65. When the dollar gets stronger

a.

U.S. firms become more competitive in international market

b.

Foreign tourists travel in the U.S. at a higher cost

c.

U.S. inflation increases

d.

U.S. consumers face higher prices on foreign goods

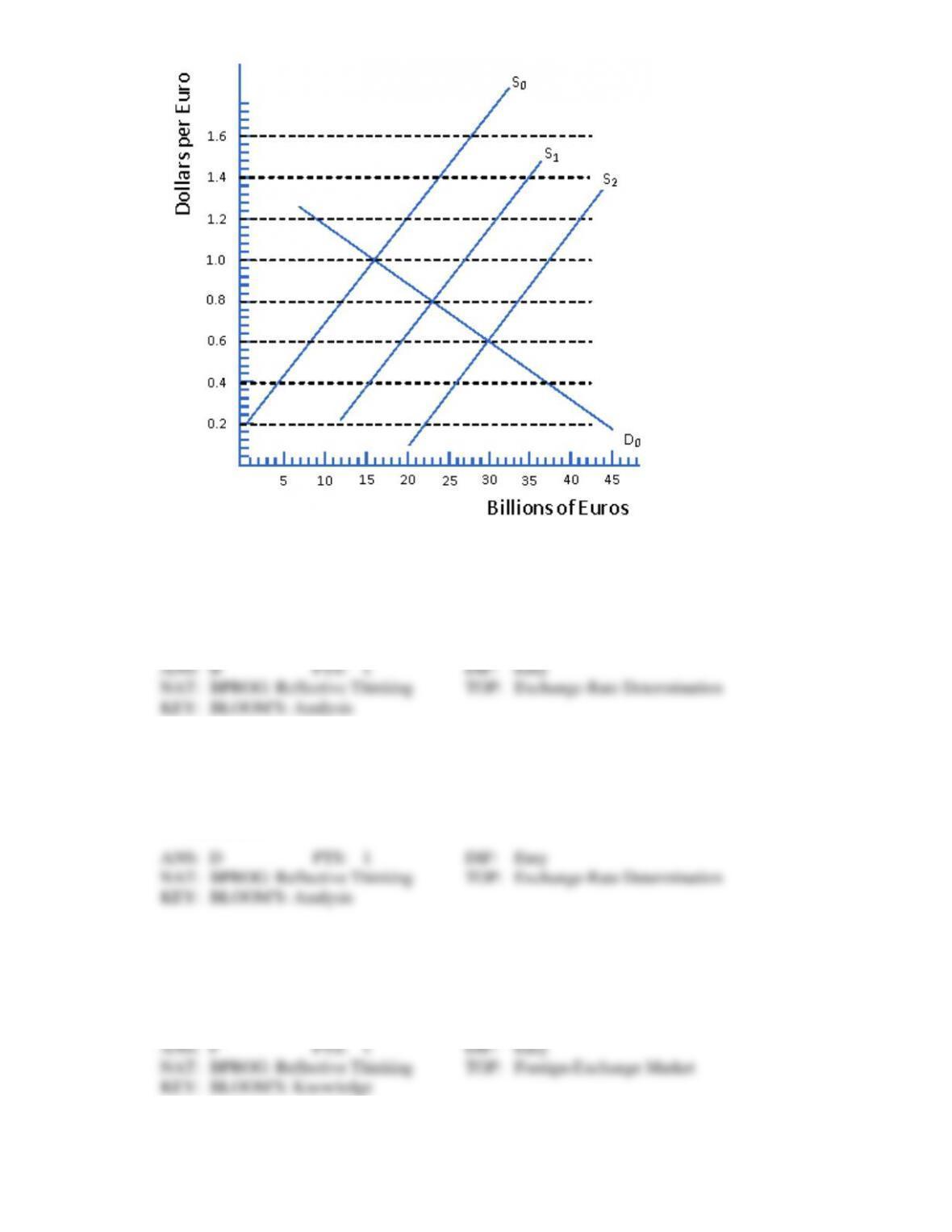

66. Refer to Figure 11.3. If the supply curve is represented by S0, the equilibrium exchange rate is

a.

$1.20

b.

$1.00

c.

$0.80

d.

$0.60

67. Refer to Figure 11.3. If the supply curve shifts from S2 to S1

a.

the dollar has depreciated relative to the Euro

b.

the euro has appreciated relative to the dollar

c.

the euro has depreciated relative to the dollar

d.

both a and b

TRUE/FALSE

1. Similar to stock and commodity exchanges, the foreign exchange market is an organized structure with

a central meeting place and formal licensing requirements.

2. Most foreign exchange transactions are conducted between commercial banks and household

customers.

3. Foreign-exchange brokers help commercial banks carry out foreign exchange trading and maintain

desired balances of foreign exchange.

4. A person needing foreign exchange immediately would purchase it on the spot market.

5. Most foreign exchange trading is carried out in the forward market.

6. Swap transactions among commercial banks involve the conversion of one currency to another at one

point with an agreement to reconvert it back into the original currency at some point in the future.

7. The bid rate refers to the price at which a bank is willing to sell a unit of foreign currency; the offer

rate is the price at which a bank is willing to buy a unit of foreign currency.

8. A commercial bank profits from foreign-exchange trading when its bid rate exceeds its offer rate.

9. The “spread” is a bank’s profit margin on foreign exchange trading and equals the difference between

the bid rate and the offer rate.

10. If Citibank quoted bid and offer rates for the Swiss franc at $.4850/$.4854, the bank would be prepared

to buy, say, 1 million francs for $485,000 and sell them for $485,400.

11. If Chase Manhattan Bank quotes bid and offer rates for the Swiss franc at $.5250/$.5260, the bank

would realize profits of $1,000 on the purchase and sale of 1 million francs.

12. If a Citibank dealer expects the Swiss franc to appreciate against the U.S. dollar, she will attempt to

lower both bid and offer rates for the franc, attempting to persuade other dealers to buy francs from

Citibank and dissuade other dealers from selling francs to Citibank.

13. If a Citibank dealer expects the Swiss franc to depreciate in the future, he will lower bid and offer rates

for the franc in order to discourage other dealers from selling francs to Citibank and persuade other

dealers to buy francs from Citibank.

14. If it takes $0.18544 to purchase 1 French franc, it takes 5.3926 francs to purchase $1.

15. If it takes 113.28 yen to buy $1, it takes $.009624 to buy 1 yen.

16. If it takes $1.5515 to buy 1 pound and $0.6845 to buy 1 franc, it takes 2.27 francs to buy 1 pound.

17. “Futures” currency contracts are issued by commercial banks and are tailored in size to the needs of

the exporter or importer, while “forward” currency contracts are issued by the International Monetary

Market in standardized round lots.

18. A foreign currency option is an agreement between a holder (corporation) and a writer (commercial

bank) giving the holder the right to buy or sell a certain amount of foreign currency at any time

through some specified date.

19. A “call” option gives General Motors the right to sell pounds at a specified price, while a put option

gives General Motors the right to buy pounds at a specified price.

20. The demand for foreign exchange is derived from credit transactions on the balance of payments.

21. The U.S. demand for pounds is derived from U.S. exports to the United Kingdom, U.K. investments in

the United States, and U.K. tourist expenditures in the United States.

22. As the dollar’s exchange value appreciates against the pound, U.S. residents tend to import more

British goods and thus demand more pounds.

23. As the dollar depreciates against the peso, U.S. residents tend to import more Mexican goods and thus

demand more pesos.

24. The supply of francs is derived from the desire of the Swiss to purchase German goods, make

investments in Germany, repay debts to German lenders, and extend transfer payments to German

residents.

25. The demand schedule for Swiss francs is always downsloping while the supply schedule of francs is

always upsloping.

26. The supply schedule of yen has a positive-sloping region which corresponds to the inelastic region on

the Japanese demand schedule for foreign currency.

27. The supply schedule of pesos has a negative-sloping region corresponding to the inelastic region on

the Mexican demand schedule for foreign currency.

28. If the Swiss demand for dollars is elastic, a depreciation of the dollar against the franc will lead to a

greater quantity of francs being supplied to the foreign exchange market to obtain dollars.

29. If the Swiss demand for dollars is inelastic, an appreciation of the dollar against the franc will lead to a

greater quantity of francs being supplied to the foreign exchange market to obtain dollars.

30. If the Swiss demand for dollars is elastic, an appreciation of the dollar against the franc will lead to a

greater quantity of francs being supplied to the foreign exchange market to obtain dollars.

31. If the Swiss demand for dollars is inelastic, a depreciation of the dollar against the franc will lead to a

greater quantity of francs being supplied to the foreign exchange market to obtain dollars.

32. Movements along the demand schedule for pounds are caused by changes in the pound’s exchange

rate.

33. Given an upward-sloping supply schedule of pounds and a downward-sloping demand schedule for

pounds, an increase in the demand schedule causes an appreciation of the dollar against the pound.

34. Given an upward-sloping supply schedule of pounds and a downward-sloping demand schedule for

pounds, a decrease in the demand schedule causes an appreciation of the dollar against the pound.

35. Given an upward-sloping supply schedule of pounds and a downward-sloping demand schedule for

pounds, an increase in the supply schedule causes an appreciation of the dollar against the pound.

36. Given an upward-sloping supply schedule of pounds and a downward-sloping demand schedule for

pounds, a decrease in the supply schedule causes an appreciation of the dollar against the pound.

37. The trade-weighted dollar is the weighted average of the exchange rates between the dollar and the

most important industrial-country trading partners of the United States.

38. If the trade-weighted dollar moves from an index value to 100 to 110, the dollar depreciates by 10

percent against the trade-weighted averages of the exchange rates of the major trading partners of the

United States.

39. An increase in the trade-weighted value of the dollar indicates a dollar appreciation relative to the

currencies of its major trading partners and a worsening of U.S. international competitiveness.

40. With arbitrage, a trader attempts to purchase a foreign currency at a low price and, at a later date, resell

the currency at a higher price in order to make a profit.

41. Arbitrage results in a riskless profit since a trader purchases a currency at a low price and

simultaneously resells it at a higher price.

42. If the exchange rate is $0.01 per yen in New York and $0.015 per yen in Tokyo, an arbitrager could

profit by buying yen in Tokyo and simultaneously sell them in New York.

43. Currency arbitrage tends to result in identical yen/dollar exchange rates in New York and in Tokyo.

44. In the forward market, the exchange rate is agreed on at the time of the currency contract, but payment

is not made until the future delivery of the currency actually takes place.

45. If the spot price of the Swiss franc is $0.4020 and the 90-day forward franc sells for $0.4026, the franc

is at a 90-day forward discount of $0.0006, or at a 0.2 percent forward discount per annum against the

dollar.

46. Suppose that Sears owes 1 million yen to a Japanese electronics manufacturer in 3 months. It could

hedge against the risk of a depreciation of the dollar against the yen by contracting to purchase 1

million yen in the forward market, at today’s forward rate, for delivery in 3 months.

47. Assume that Boeing anticipates receiving 20 million yen in 3 months from exports of jumbo jets to a

Japanese airline. The firm could hedge against the risk of a depreciation of the dollar against the yen

by contracting to sell its expected yen proceeds for dollars in the forward market at today’s forward

rate.

48. A U.S. investor’s extra rate of return on an investment in France, as compared to the United States,

equals the interest-rate differential adjusted for any change in the dollar/franc exchange rate.

49. A currency speculator’s goal is to buy a currency at a low price and immediately resell it at a higher

price, thus realizing a riskless profit.

50. Stabilizing speculation reinforces market forces by intensifying an appreciation or a depreciation in a

currency’s exchange value.

SHORT ANSWER

1. What foreign exchange transactions do banks typically engage in?

2. How is the equilibrium rate of exchange determined?

ESSAY

1. Is it possible to trade foreign exchange in the futures market? How does such trading differ from the

forward market?

2. Where are foreign currency options traded?