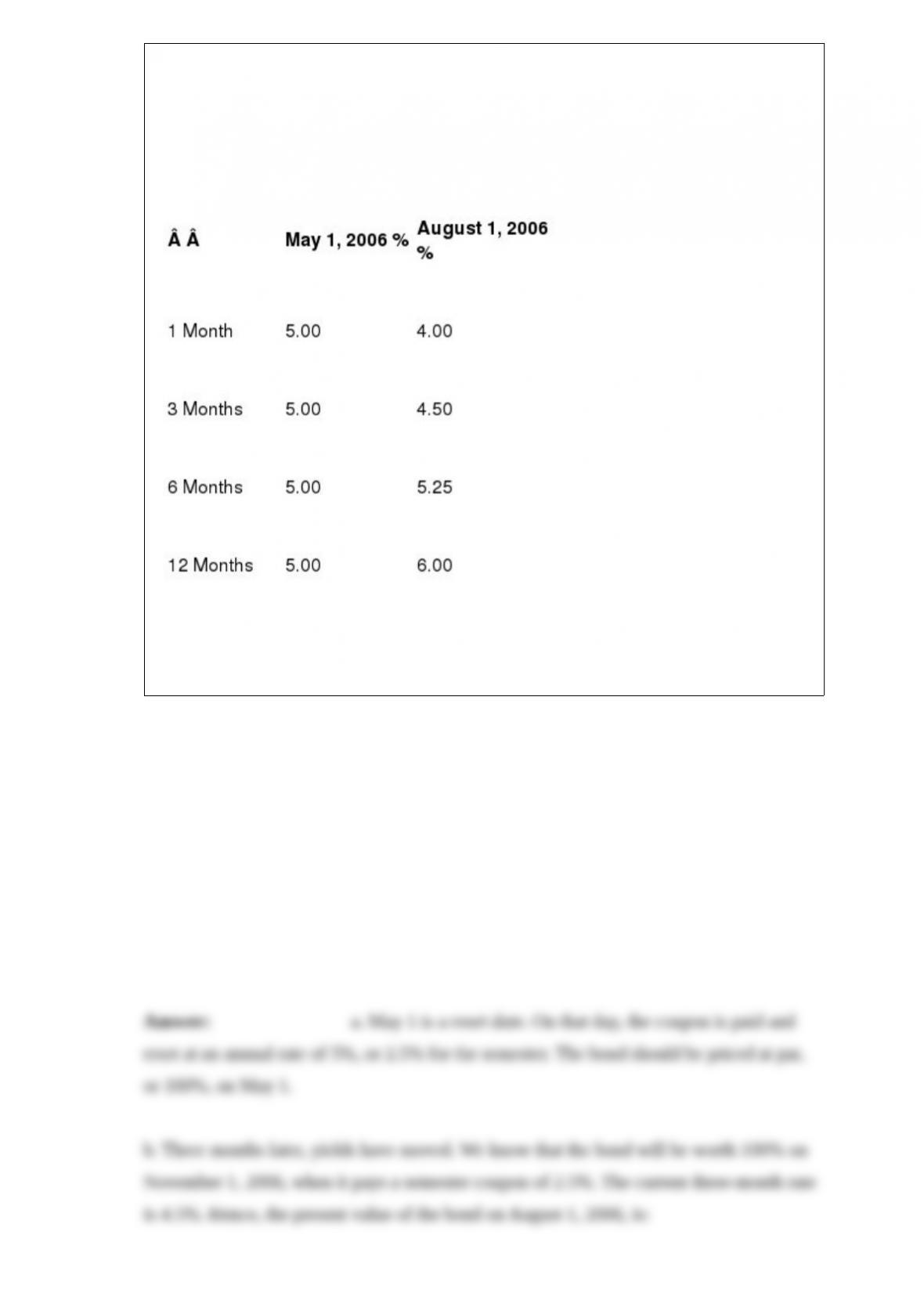

A company without default risk can issue a ten-year FRN at LIBOR. The coupon is paid

and reset semiannually. It is certain that the issuer will never have default risk and will

always be able to borrow at LIBOR. The FRN is issued on November 1, 2005, when the

six-month LIBOR is at 4.5%. Here are the dollar yield curves on two different dates:

a. What should the value of the FRN be on May 1?

b. What should the value and the clean price of the FRN be August 1, 2006?

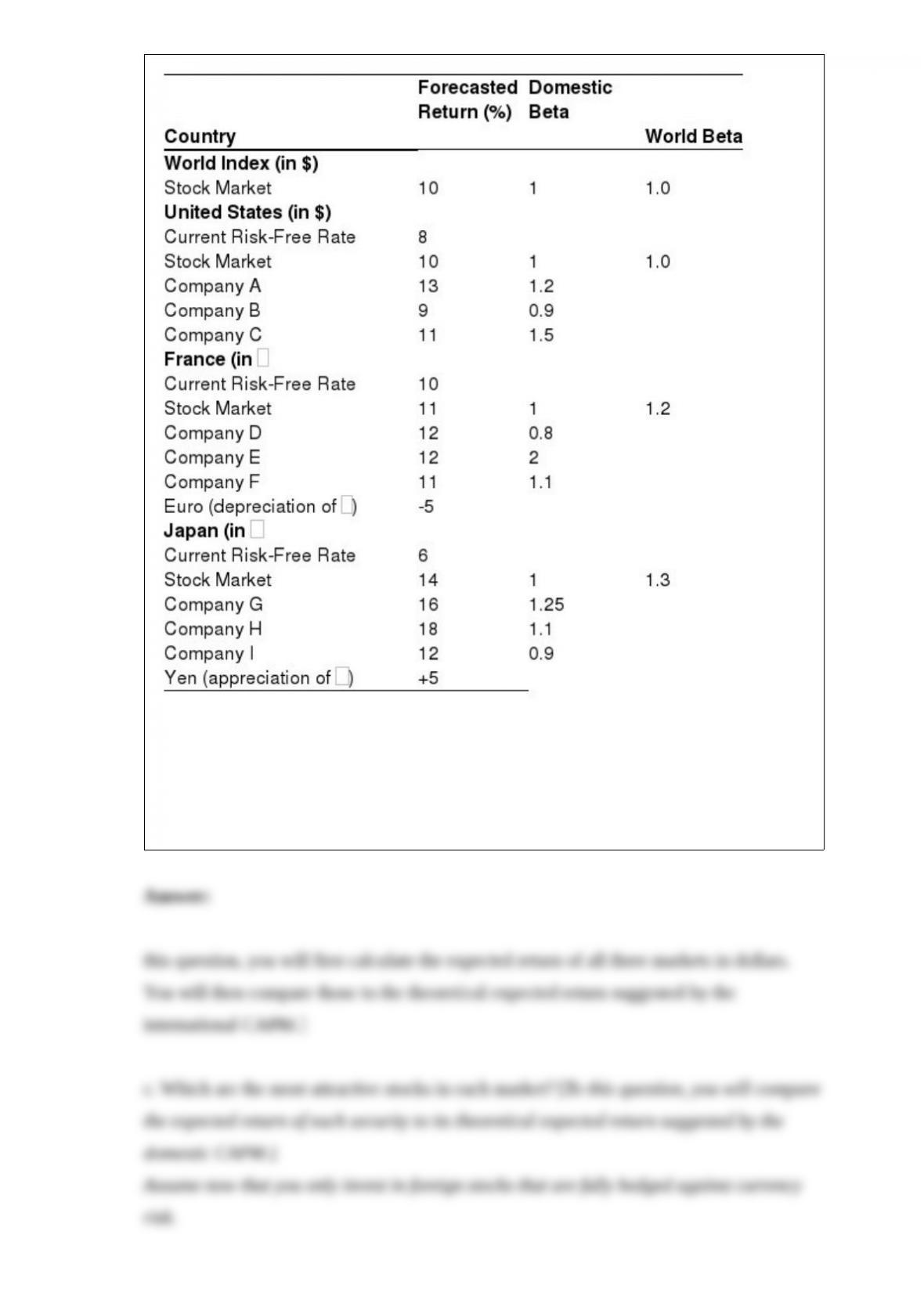

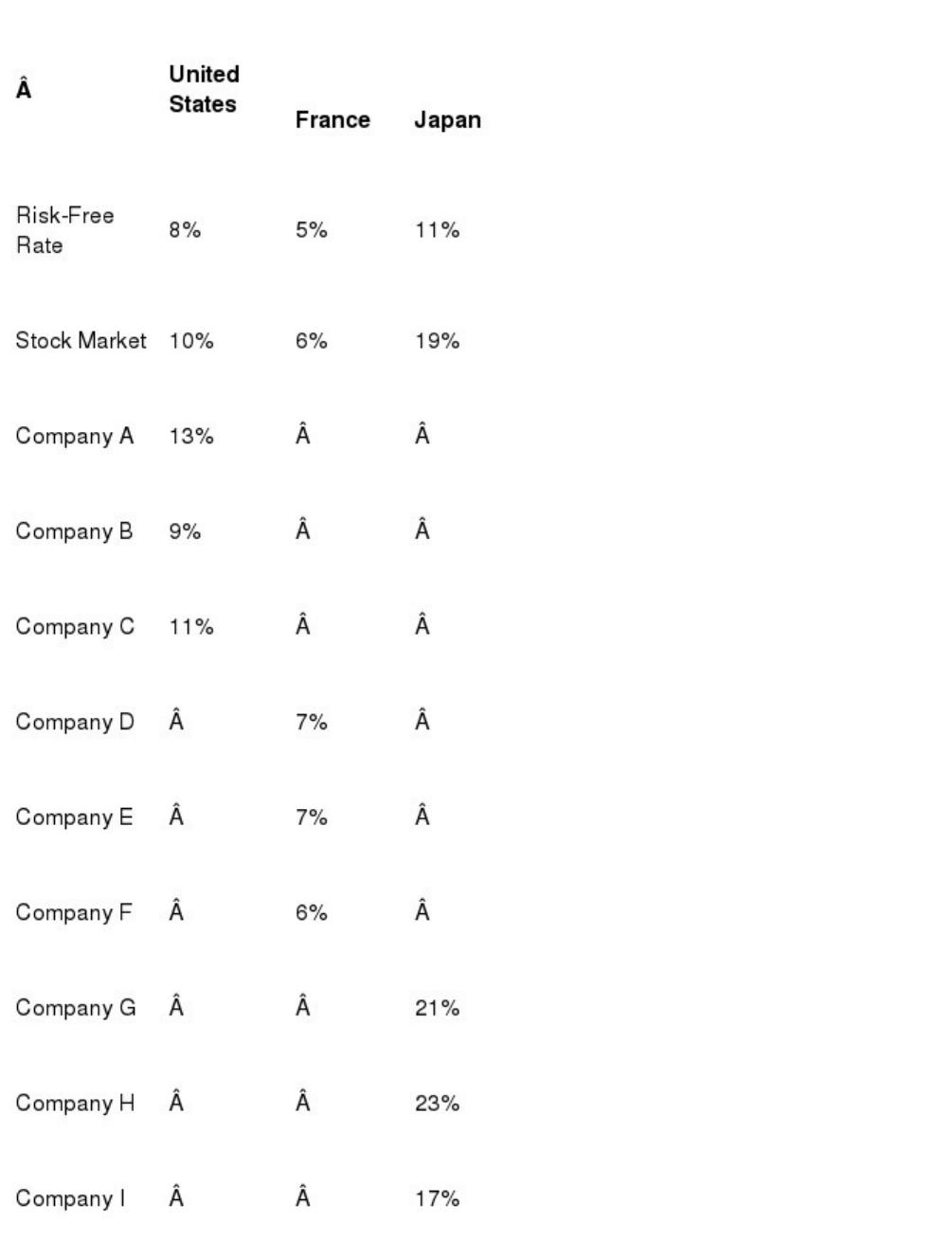

You are a U.S. pension fund that cares about dollar return. You believe in the

“multicountry approach” to asset pricing but feel that currency premiums are equal to

zero (so you do not care about currency exposures). The multicountry approach

assumes that national equity markets are priced globally and that securities of each

country are priced relative to their national market. In other words, each security is

influenced by its national market factor, which in turn is influenced by the world market

factor, and, possibly, by currency factors. This implies that the world beta of security i (

, or sensitivity to the world market), is equal to the product of the local beta of

security i ( , or sensitivity to the local market) times the world beta of its local market

( ).

In your portfolio construction, you apply a traditional two-step procedure where, you

first decide on country allocation and then on security selection within each country.

The following are your forecasts for the coming year, the betas of stocks calculated

relative to their domestic index, as well as the betas of the national stock markets

relative to the world index. All forecasts are measured in their local currency.

Assume that you do not hedge currency risks.

a. Write the international CAPM equations that would hold for each national market

and security. Express it in dollars and in the security’s local currency.

b. Which national market should you under/overweight in your global portfolio? [To

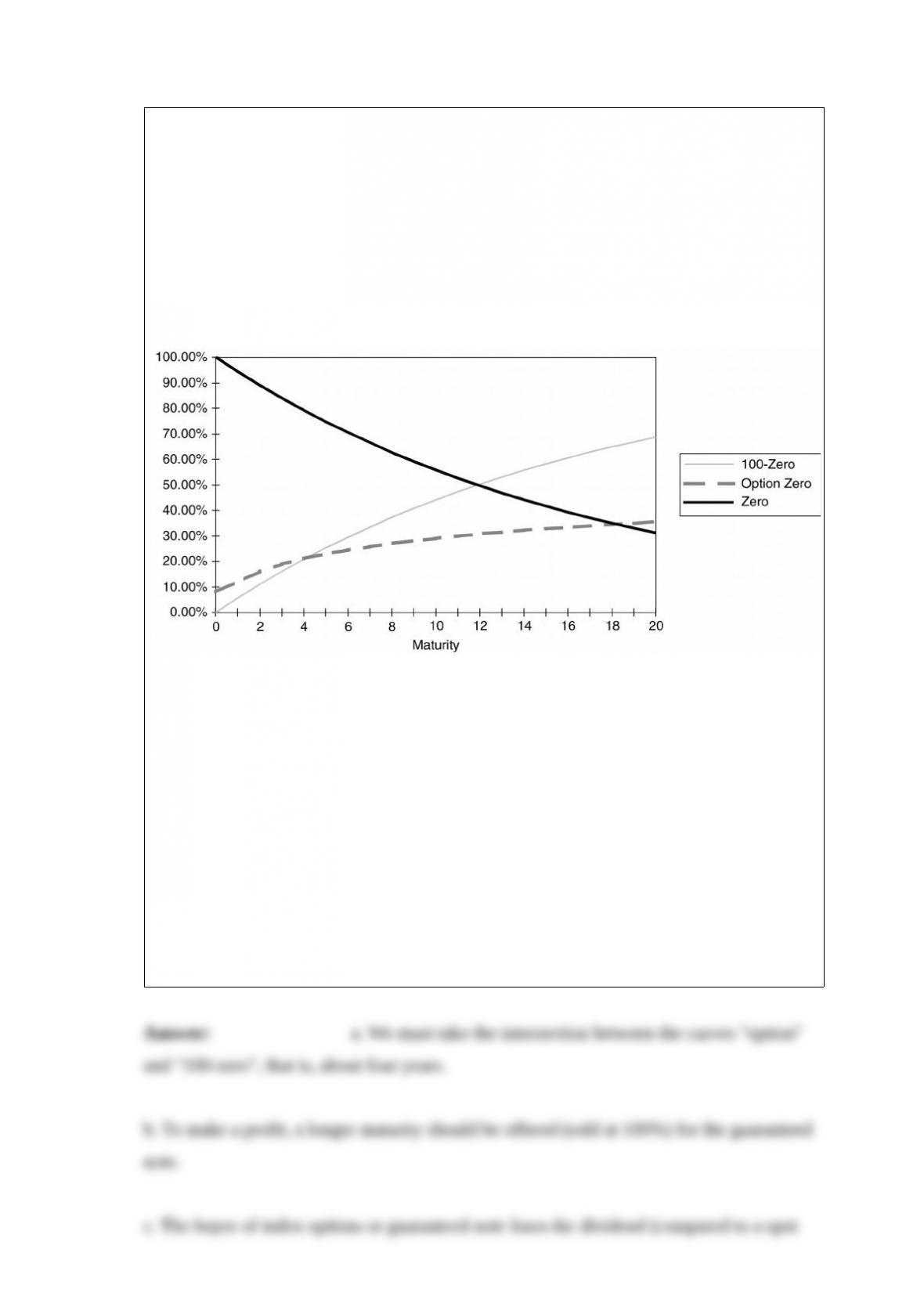

You’re a banker. A client wishes to buy a guaranteed note with a 100% indexation to the

stock index’s growth. In other words, he does not want any coupon but requires 100%

of the index growth. You wonder about the maturity of such a note. You check the

prices of various index calls traded on the market for different maturities. Their strike is

the current index level and their price is expressed as a percentage of this level. (For

instance, if the CAC is worth 3,000, the strike is 3,000, and the one-year maturity call

trades at 11% of 3,000. You also check the price of a zero-coupon in percentage for

various maturities. The following graph shows, for each a maturity, the price of the

option, that of the zero-coupon and 100%-zero.

a. What is the maturity of the guaranteed note (Coupon = 0%, indexation = 100%)?

Justify.

b. If as a banker, you want to make a profit, should you lengthen or shorten the maturity

of that note? Explain why.

c. Everything remaining constant (i.e., same volatility and interest rate), should the

maturity

of the guaranteed note be shorter or longer if the index pays a low dividend rather than

a

high one? Why?

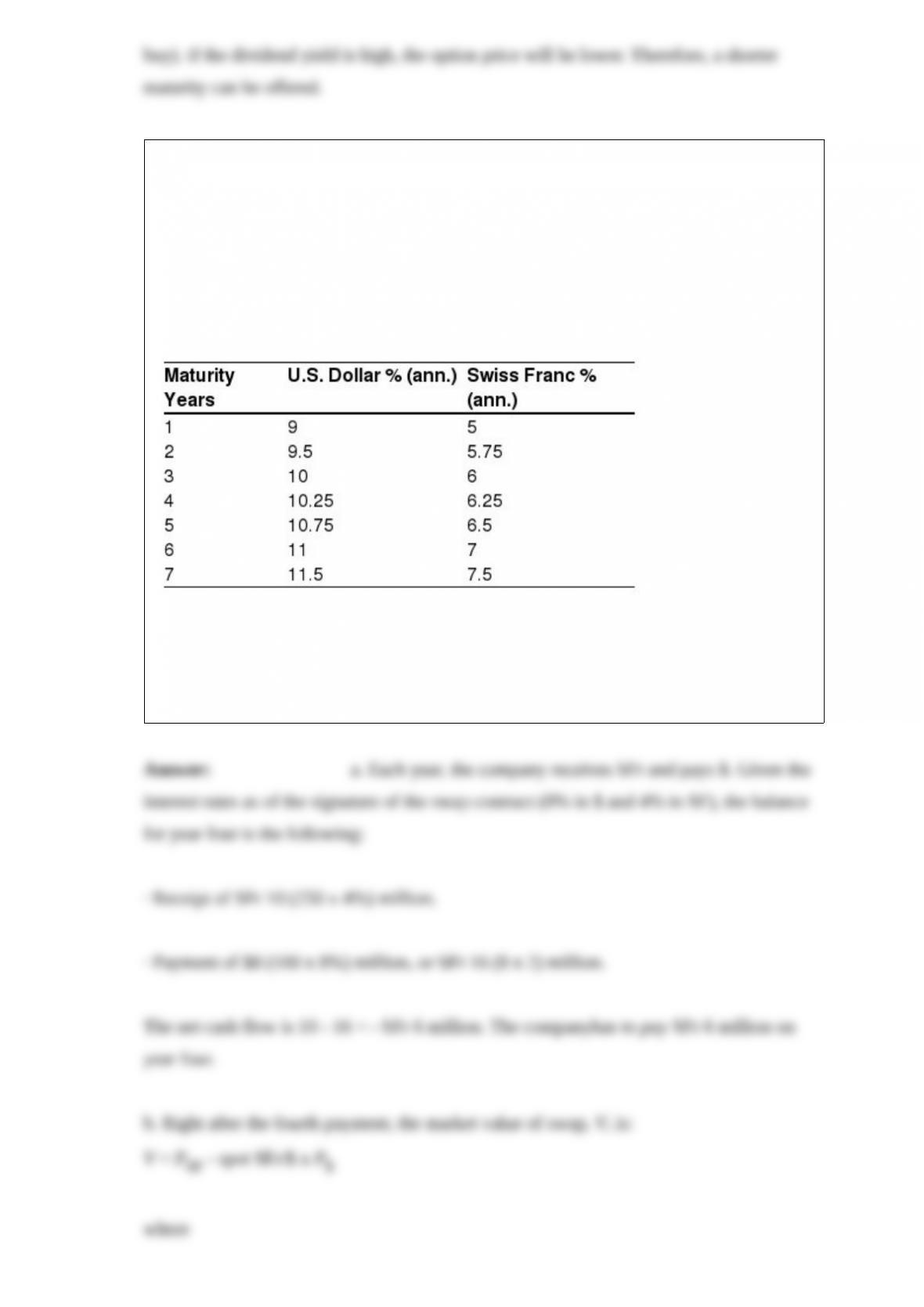

Four years ago, a Swiss firm contracted a currency swap of US$100 million for 250

million Swiss francs (SFr), with a maturity of seven years. The swap fixed rates are 8%

in dollars and 4% in francs, and swap payments are annual. The Swiss firm contracted

to pay dollars and receive francs. The market conditions are now (exactly four years

later) as follows:

Spot exchange rate: 2.00 Swiss francs/U.S. dollar.

Term structure of zero swap rates:

a. What should the swap payment (receipt) be at the end of the fourth year, that is,

today?

b. Right after this payment, what is the swap market value for the Swiss firm?

The U.S. Department of Justice (DoJ) uses the Herfindahl Index to evaluate the impact

of a proposed horizontal merger between firms on the degree of market concentration.

The following text is an extract of the official document found in 2003 on the DoJ Web

site:

Market concentration is a function of the number of firms in a market and their

respective market shares. As an aid to the interpretation of market data, the Agency will

use the Herfindahl€Hirschman Index (“HHI”) of market concentration. The HHI is

calculated by summing the squares of the individual market shares of all the

participants [€¦].

The Agency divides the spectrum of market concentration as measured by the HHI into

three regions that can be broadly characterized as unconcentrated (HHI below 1,000),

moderately concentrated (HHI between 1,000 and 1,800), and highly concentrated (HHI

above 1,800). Although the resulting regions provide a useful framework for merger

analysis, the numerical divisions suggest greater precision than is possible with the

available economic tools and information. Other things being equal, cases falling just

above and just below a threshold present comparable competitive issues.

1.51 General Standards

In evaluating horizontal mergers, the Agency will consider both the post-merger market

concentration and the increase in concentration resulting from the merger. Market

concentration is a useful indicator of the likely potential competitive effect of a merger.

The general standards for horizontal mergers are as follows:

a. Post-Merger HHI below 0.10. The Agency regards markets in this region to be

unconcentrated. Mergers resulting in unconcentrated markets are unlikely to have

adverse competitive effects and ordinarily require no further analysis.

b. Post-Merger HHI between 0.10 and 0.18. The Agency regards markets in this region

to be moderately concentrated. Mergers producing an increase in the HHI of less than

0.01 points in moderately concentrated markets, post-mergers are unlikely to have

adverse competitive consequences and ordinarily require no further analysis. Mergers

producing an increase in the HHI of more than 0.01 points in moderately concentrated

markets, post-mergers potentially raise significant competitive concerns depending on

the factors set forth in Section 2-5 of the Guidelines.

c. Post-Merger HHI above 0.18. The Agency regards markets in this region to be highly

concentrated. Mergers producing an increase in the HHI of less than 0.005 points, even

in highly concentrated markets, post-mergers are unlikely to have adverse competitive

consequences and ordinarily require no further analysis. Mergers producing an increase

in the HHI of more than 0.005 points in highly concentrated markets, post-mergers

potentially raise significant competitive concerns, depending on the factors set forth in

Section 2-5 of the Guidelines. Where the post-merger HHI exceeds 0.18, it will be

presumed that mergers producing an increase in the HHI of more than 0.01 points are

likely to create or enhance market power or facilitate its exercise. The presumption may

be overcome by a showing that factors set forth in Section 2-5 of the Guidelines make it

unlikely that the merger will create or enhance market power or facilitate its exercise, in

light of market concentration and market shares.

Source: http://www.usdoj.gov/atr/public/guidelines/horiz_book/hmg1.html, June 2003.

Note: The appellations Herfindahl€Hirschman Index (“HHI”) or Herfindahl Index (“H”)

are used interchangeably. The DoJ expresses the Index in squared percent, for example

(10%)2 =100, rather than (10%)2 = (0.10)2 = 0.01. With their units, the index is equal to

100 x 100 = 10,000 times the same index calculated in International Investments. To be

consistent, we took the liberty to transform their units into ours.

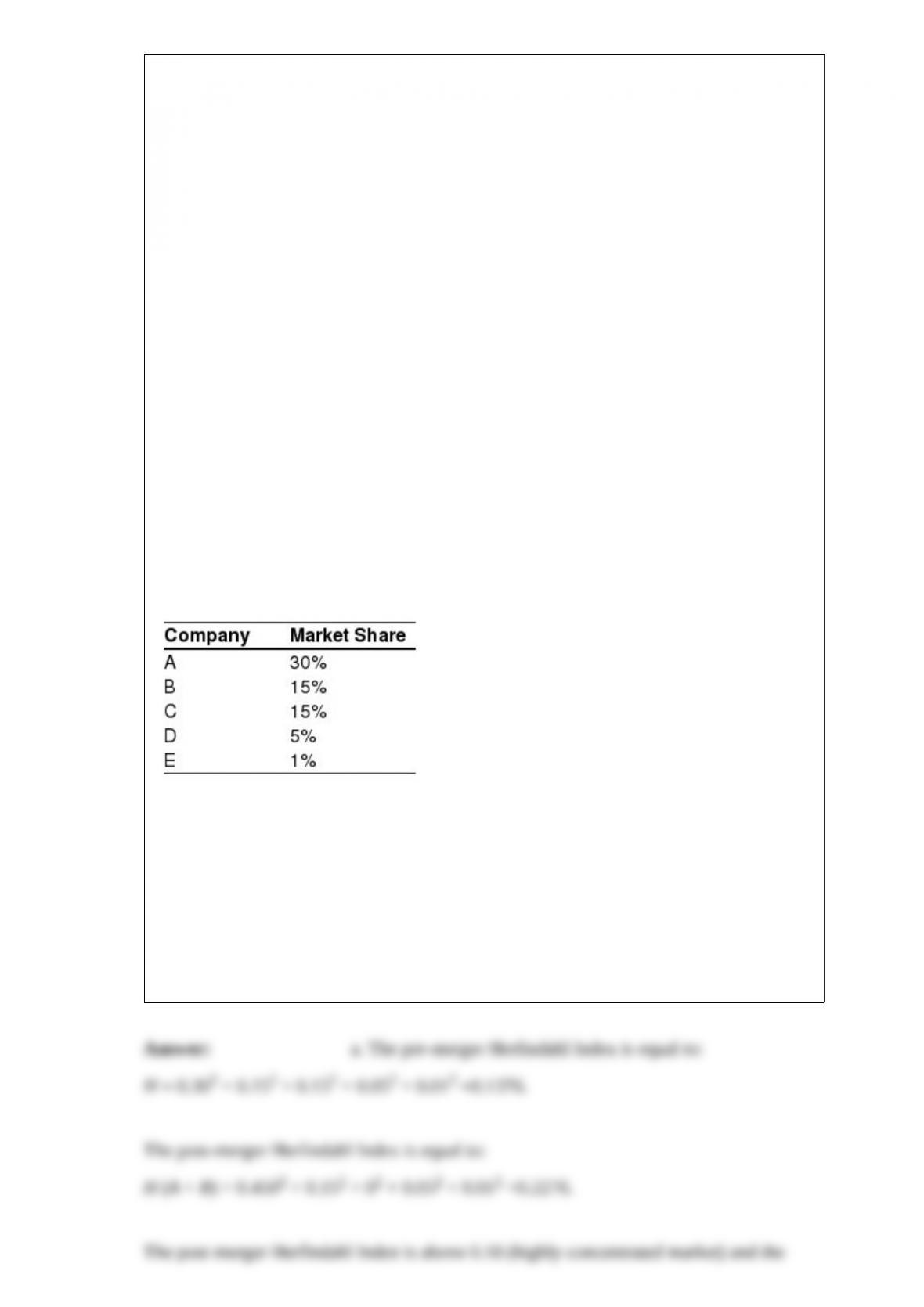

a. You consider an industry with numerous very small firms and five large firms. Their

market shares are as follows:

Companies A and B merge, what should the reaction of the DoJ be according to the

Agency’s standards?

b. Consider now that the merger is between companies A and D. What should the

reaction of the DoJ be according to the Agency’s standards?

c. Consider now that the merger is between Companies A and E. What should the

reaction of the DoJ be according to the Agency’s standards?

A company has 500,000 shares outstanding at 20 per share. To its management, the

company grants employee stock options on 10,000 shares. Five thousand of these

options can be exercised at a price of 21 any time during the next five years. For five

years, the employees thus have the right but not the obligation to purchase shares at the

21 price, regardless of the prevailing market price of the stock. Another 5,000 of these

options can be exercised at a price of 25 any time during the next

five years. For five years, the employees thus have the right but not the obligation to

purchase shares at the 25 price, regardless of the prevailing market price of the stock.

The company’s auditor can provide an estimate of the options’ value. Using price

volatility estimates for the stock, a standard Black-Scholes’ valuation model gives an

estimated value of 12 per share option with an exercise price of 21 and of 7 per

share option with an exercise price of 2 Without expensing the options, the company’s

pretax earnings are reported as 10 million.

a. What are the pretax earnings per share without expensing the share options granted?

b. What are the pretax earnings per share with expensing the share options granted?

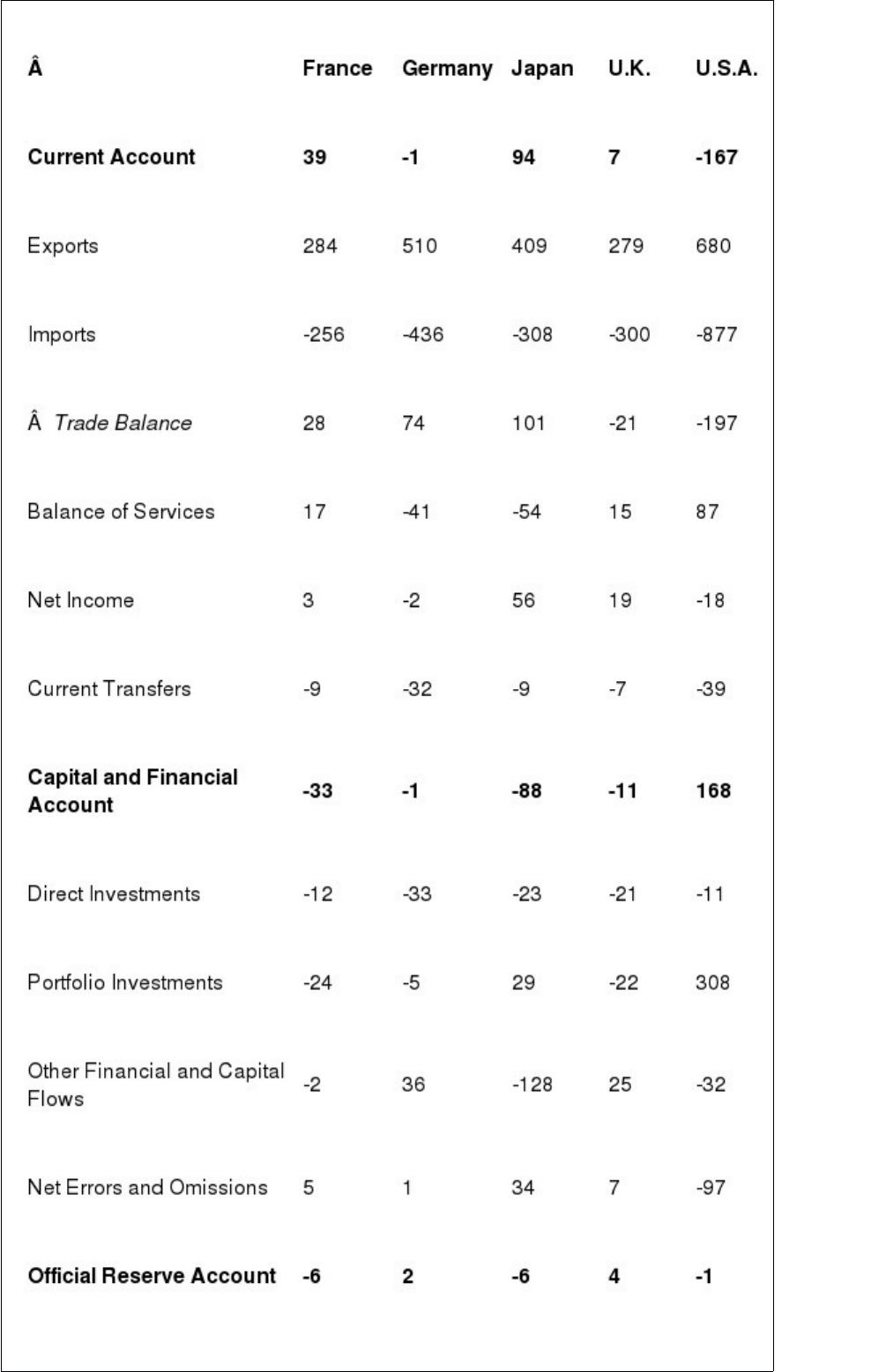

The exhibit below presents the 1997 balance of payments statistics for France,

Germany, Japan, the United Kingdom, and the United States. The various balance of

payments items have been aggregated using the presentation outlined in Chapter 2.

EXHIBIT: 1997 Balance of Payments of Five Major Countries

Billions of U.S. Dollars

Source: Adapted from International Monetary Fund, International Financial Statistics,

1998 Yearbook. a. Provide an analysis of the U.S. balance of payments. b. Provide an

analysis of the British balance of payments. c. Provide an analysis of the French

balance of payments. d. Provide a brief analysis of the Japanese balance of payments. e.

Provide a brief analysis of the German balance of payments.

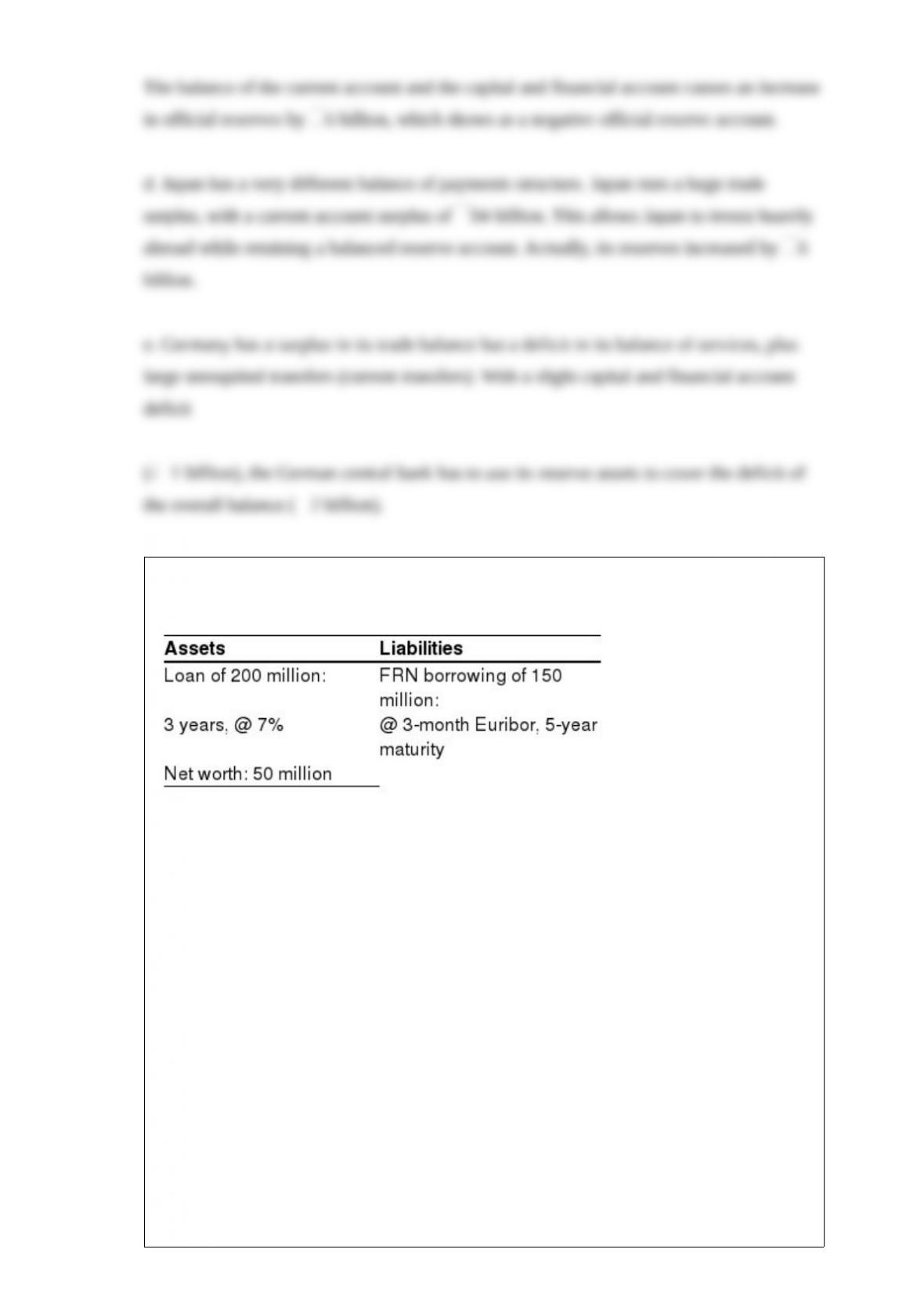

A small Dutch bank has the following balance sheet (in euros), based on historical or

nominal values.

All assets and liabilities are denominated in euros. The bank borrows short-term on the

Euro-currency market. The bank and its client are AAA quality. The net worth is

calculated as the difference between the value of assets and liabilities. The current euro

term structure for AAA borrowers is flat at 6.5%.

a. Value the balance sheet based on market value.

b. Compute the interest-rate sensitivity (duration) of the asset. Infer the interest rate

sensitivity of the net worth of the bank. For example, how much would stockholders

lose if euro interest rates moved up by 0.10%? (Assume that the interest rate sensitivity

of an floating-rate note (FRN) is zero, as the coupon is reset to the market interest rate.)

c. The bank fears a rise in all euro interest rates. The current market conditions for

interest rate swaps in euros are as follows:

· With a maturity of three years are: 6.5% against Euribor.

· With a maturity of five years are: 6.75% against Euribor.

What would you do to hedge this interest rate risk?

d. The next day, all interest rates move up to 8%. Value again the balance sheet,

assuming that the floating-rate debt remains at 100% and that the bank has undertaken

the swap that you recommended. Is the hedge perfect? Why?

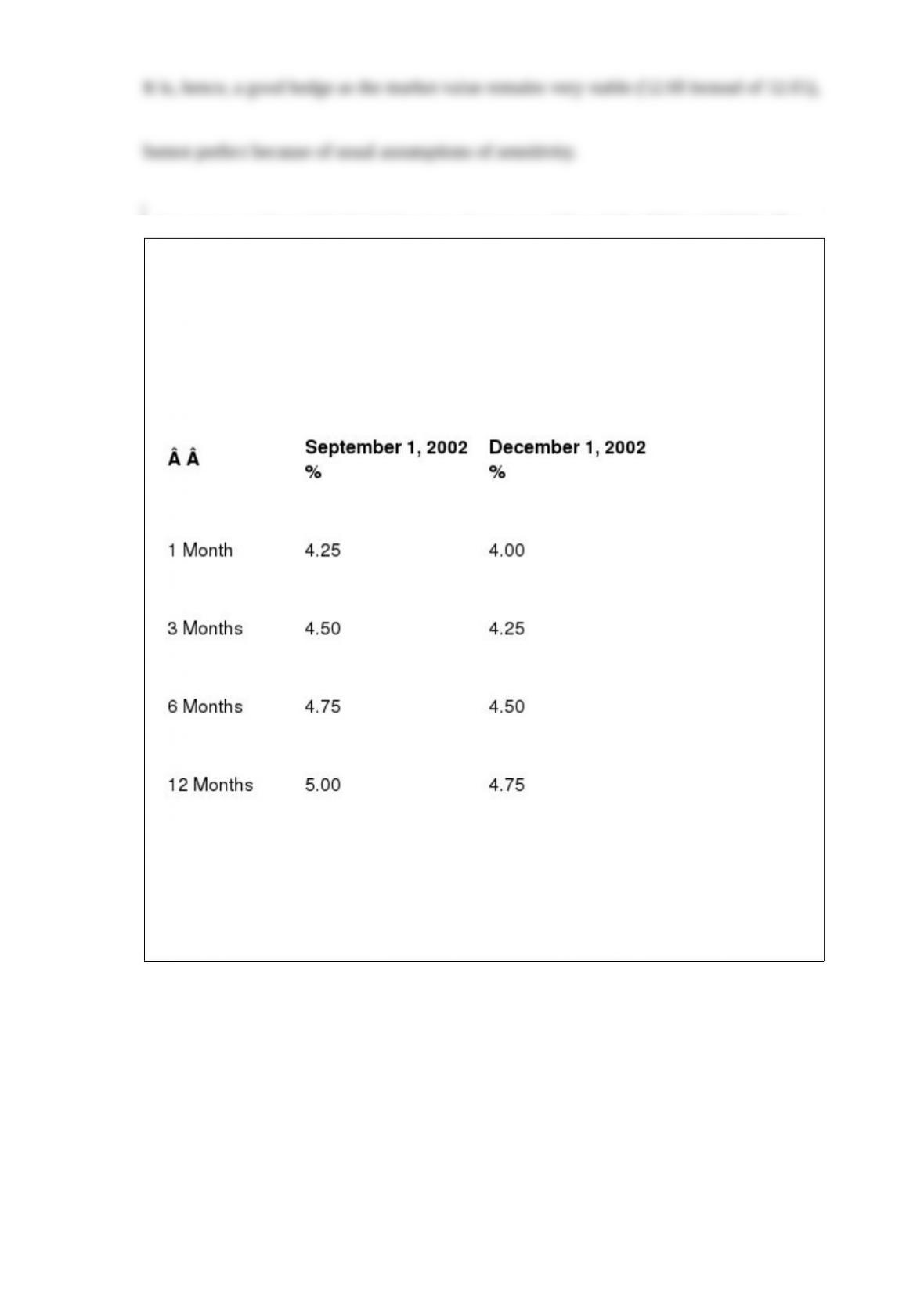

A company without default risk has issued a perpetual Eurodollar FRN at LIBOR. The

coupon is paid and reset semiannually. It is certain that the issuer will never have

default risk, and will always be able to borrow at LIBOR. The FRN is issued on March

1, 2002, when the six-month LIBOR is at 5%. The Eurodollar yield curve on September

1, 2002, and December 1, 2002, is as follows.

a. What is the coupon paid on September 1, 2002, per $1,000 FRN?

b. What is the new value of the coupon set on the FRN on September 1, 2002?

c. What is the new value and clean price of the FRN on December 1, 2002?

The French luxury-goods company LVMH, Louis Vuitton-Mo«t Hennesy, issued a

series of perpetual floating-rate notes on the international capital market in the 1990s.

These bonds have the advantage of being quasi-equity, while benefiting from favorable

tax treatment. Pioneered by state-owned French firms that cannot sell stock to the

public, and subsequently used by a number of private European companies that were

reluctant to dilute their stocks, the subordinated perpetual floating-rate note is an

instrument that remains outstanding in name only. These securities are called instantly

repackaged perpetuals, or IRPs.

After a 5-billion franc issue in 1990, LVMH sold, in March 1992, 1.5 billion francs of

IRPs. The company received 1.1 billion francs, the remaining 400 million being

transferred to an offshore trust. The trust used the proceeds to buy fifteen-year

zero-coupon bonds issued by banks underwriting the LVMH issue or by sovereign

borrowers such as Denmark and Austria. The 400-million investment in zero-coupon

bonds will be redeemed for 1.5 billion in fifteen years. The IRPs have the peculiarity

that they pay interest only for the first fifteen years; the interest becomes nil thereafter.

After these fifteen years, the trust is committed to repurchase the perpetuals at their face

value of 1.5 billion francs. The trust, especially set up for this purpose, will then hold

the IRPs forever, but their market value has become zero as they are perpetuals, which

pay no interest. The semiannual coupon was set at six-month PIBOR (Paris InterBank

Offer Rate) plus ½%.

From an accounting viewpoint, these IRPs are treated as new equity of LVMH, because

they are perpetual. From a tax viewpoint, the interest paid on the IRPs during fifteen

years can be deducted as interest expense (while dividend payments are not tax

deductible).

a. Assume that you are an investment banker proposing such an IRP to a potential

client. Explain in detail the advantage of such a package relative to a plain-vanilla

fifteen-year FRN, or relative to a new stock issue.

b. In 1990, the French tax authorities decided to allow a write-off of interest expense for

only the net amount of capital that the issuer actually takes on its books (1.1 billion for

LVMH). Why does this decision reduce the attraction of issuing IRPs?

c. Following the 1992 LVMH issue, the tax authorities decide to introduce a new

regulation for trusts, whereby capital gains would be taxed at the normal income tax

rate. In effect, the trust would make a capital gains equal to the difference between the

face value of the zero-coupon bonds and their issue price. This basically shut the market

for IRPs. Why?

A dollar-Swiss franc swap with a maturity of five years was contracted by Papaf Inc.

three years ago. Papaf swapped $100 million for CHF 250 million. The swap payments

were annual, based on market interest rates of 8% in dollars and 4% in CHF. In other

words, Papaf Inc. contracted to pay dollars and receive CHF. The current spot exchange

rate is 2 CHF/$, and the current interest rates are 6% in CHF and 10% in $ (the term

structures are flat).

a. What is the swap payment at the end of year three? Does Papaf pay or receive?

b. On the final date of the swap, the spot exchange rate is 1.5 CHF/$.

What is the final swap payment at the end of year five?

A five-year currency swap involves two AAA borrowers and has been set at current

market interest rates. The swap is for US$100 million against AUD 200 million at the

current spot exchange rate of AUD/$ 2.00. The interest rates are 10% in U.S. dollars

and 7% in Australian dollars, or annual swaps of US$10 million for AUD 14 million. A

year later, the interest rates have dropped to 8% in U.S. dollars and 6% in Australian

dollars, and the exchange rate is now AUD/$ 1.9.

a. What should the market value of the swap be in the secondary market?

Assume now that the swap is instead a currency-interest rate swap whereby the dollar

interest is set at LIBOR.

b. What would the market value of the currency-interest rate swap be if these conditions

prevailed a year later?

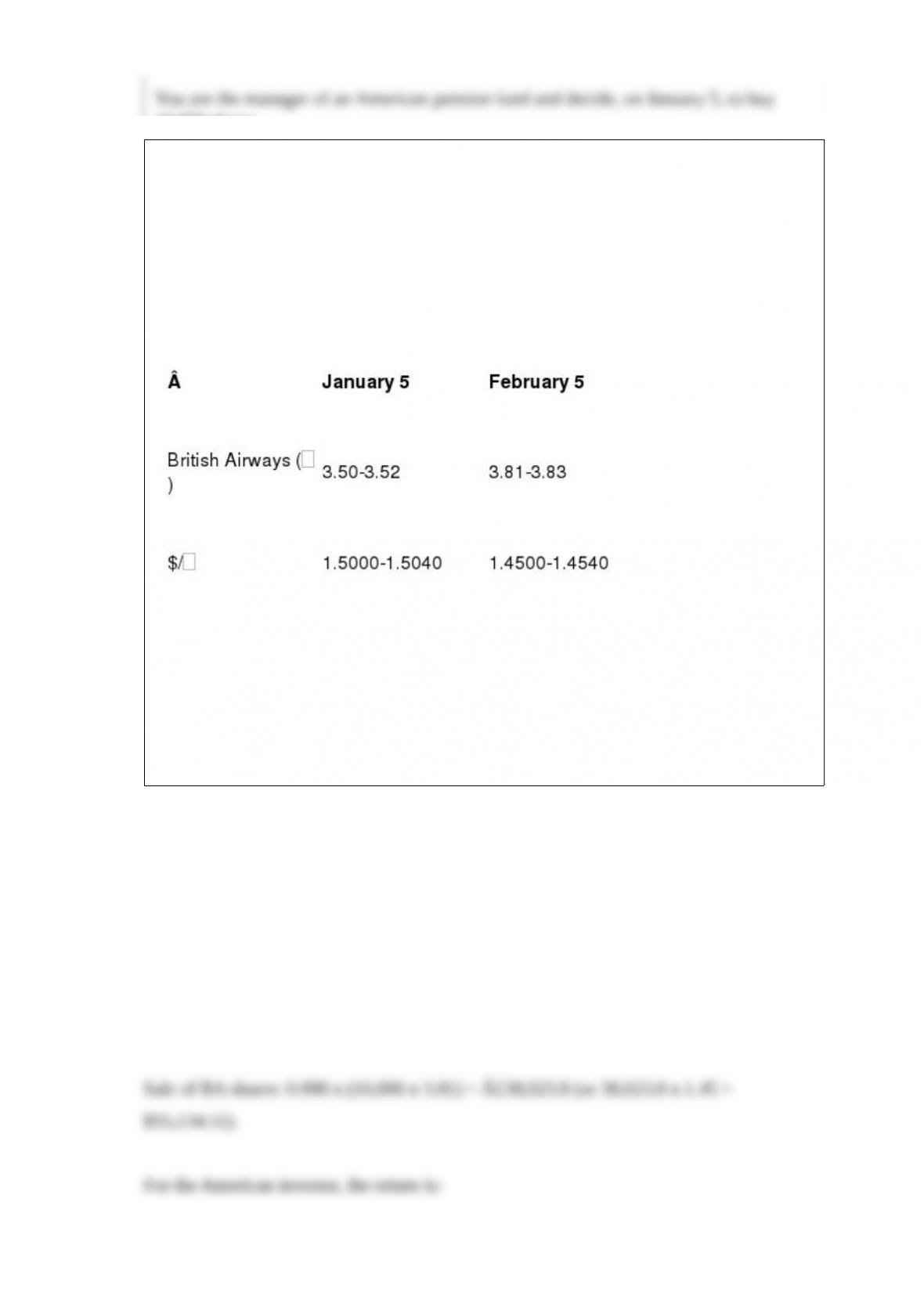

You are the manager of an American pension fund and decide, on January 5, to buy

10,000 shares

of British Airways (BA) listed in London. You sell them on February 5. Here are the

quotes that

you can use:

You must pay the U.K. broker a commission of 0.2% of the transaction value (on the

purchase and on the sale). There is a 0.5% U.K. securities transaction tax on purchase

(but not on the sale); this tax cannot be recovered. Foreign exchange rates are the net of

commissions and taxes. a. What is your dollar rate of return on the operation? b. Would

the rate of return be the same for a British investor using the British pound as a

reference currency?

An FRN is a bond that pays a quarterly or semiannual coupon indexed on a short-term

interest rate such as the LIBOR.

a. Why does it make sense to use a short-term interest rate as the index?

b. Why are banks heavy issuers of FRNs?

Four companies belong to a group and are listed on a stock exchange. The

cross-holdings of these companies are as follows.

· Company A owns 30% of Company B and 10% of Company C.

· Company B owns 10% of Company C.

· Company C owns 10% of Company A, 10% of Company B, and 25% of Company D.

· Company D owns 10% of company B.

Each company has a market capitalization of 50 billion. You wish to adjust for

cross-holding to reflect the weights of these companies in a market-capitalization

weighted index.

a. What adjustments would you make in the market capitalization of each company to

reflect the free float?

b. What would be the total adjusted market capitalization of the four companies?

The current euro yield curve on the euro Eurobond market is flat at 4% for top-quality

borrowers. A French company of good standing can issue plain-vanilla straight and

floating-rate dollar Eurobonds at the following conditions:

·Bond A: Straight bond. Five-year straight dollar Eurobond with a coupon of 4%.

·Bond B: Floating rate note (FRN). Five-year dollar FRN with a semiannual coupon set

at London InterBank Offered Rate (LIBOR).

An investment banker proposes to the French company to issue bull and/or bear FRNs

at the following conditions:

·Bond C: Bull FRN. Five-year FRN with a semiannual coupon set at:

7.60% – LIBOR.

·Bond D: Bear FRN. Five-year FRN with a semiannual coupon set at:

2 x LIBOR – 4.2%.

The floor on all coupons is zero. The investment bank also proposes a five-year floor

option at 2.1%. This floor will pay to the French company the difference between 2.1%

and LIBOR, if it is positive, or zero if LIBOR is above 2.1%. The cost of this floor is

spread over the payment dates and set at an annual 0.05%. The bank also proposes a

five-year cap at 7.60%. The annual premium on the cap is 0.1%. The company can also

enter in a five-year interest-rate swap of 4% fixed against LIBOR.

a. Assume that the French company issues Bonds C and D in equal proportions. Is it

more advantageous than issuing Bonds A and B in equal proportion and why?

b. Find out the borrowing cost reduction that can be achieved by issuing the bull Note C

compared to issuing a fixed-coupon straight Bond A at 4%.

c. Find out the borrowing cost reduction that can be achieved by issuing the bull Note C

compared to issuing a plain-vanilla FRN B at LIBOR.

d. Find out the borrowing cost reduction that can be achieved by issuing the bear Note

D compared to issuing a fixed-coupon straight Bond A at 4%.

e. Find out the borrowing cost reduction that can be achieved by issuing the bear Note

D compared to issuing a plain-vanilla FRN B at LIBOR.

The current yield curve on the international bond market in euro is flat at 4% for

top-quality borrowers. A French company of good standing can issue plain-vanilla

straight and floating-rate bonds at the following conditions:

· Bond A: Straight Bond. Five-year straight bond with a fixed coupon of 4%.

· Bond B: FRN. Five-year dollar FRN with a semiannual coupon set at LIBOR.

An investment banker proposes to the French company to issue bull and/or bear FRNs

at the following conditions:

· Bond C: Bull FRN. Five-year FRN with a semiannual coupon set at:

7.60% – LIBOR.

· Bond D: Bear FRN. Five-year FRN with a semiannual coupon set at:

2 xLIBOR – 4.2%.

The floor on all coupons is zero. The investment bank also proposes a five-year floor

option at a strike of 2.1%. This floor will pay to the French company the difference

between 2.1% and LIBOR, if it is positive, or zero if LIBOR is above 2.1%. The cost of

this floor is spread over the payment dates and set at an annual 0.05%. The bank also

proposes a five-year cap at a strike of 7.60%. The annual premium on the cap is 0.1%.

The company can also enter in a five-year interest-rate swap 4% fixed against LIBOR.

a. Assume that the French company issues Bonds C and D in equal proportions. Is it

more advantageous than issuing Bonds A and B in equal proportion and why?

b. Find out the borrowing cost reduction that can be achieved by issuing the bull note

compared to issuing a fixed-coupon straight bond at 4%.

c. Find out the borrowing cost reduction that can be achieved by issuing the bull note

compared to issuing a plain-vanilla FRN at LIBOR.

d. Find out the borrowing cost reduction that can be achieved by issuing the bear note

compared to issuing a fixed-coupon straight bond at 4%.

e. Find out the borrowing cost reduction that can be achieved by issuing the bear note

compared to issuing a plain-vanilla FRN at LIBOR.

If the exchange rate value of the euro goes from U.S. 1.15 to U.S. 1.05, then:

a. The euro has appreciated, and Europeans will find U.S. goods cheaper.

b. The euro has appreciated, and Europeans will find U.S. goods more expensive.

c. The euro has depreciated, and Europeans will find U.S. goods more expensive.

d. The euro has depreciated, and Europeans will find U.S. goods cheaper.

Take the example of two straight yen Eurobonds with the same maturity of five years.

Bond A has a coupon of 12% and Bond B a coupon of 8%. The current market interest

rate on yen bonds is 9%. These two bonds have the same yield-to-maturity of 10% and

are correctly priced at 111.67% for Bond A and 96.11% for Bond B. What would be the

yield-to-maturity indicated by the simple yield calculation?

Why are futures contracts commonly believed to be less subject to default risk than

forward contracts?

In the early 1990s, France and Germany had similar current and forecasted inflation

rates. However, political/economic uncertainties were higher in France, where several

political changes in the 1980s had led to several devaluations of the French franc. Do

you expect to observe equal interest rates in the two countries? Why or why not?

Assume that an AAA customer pays 8% on a five-year loan and can contract a five-year

interest

rate swap (paying fixed) at 8% against LIBOR. Assume that a BBB customer pays (8 +

m)% on a

five-year loan and can contract a five-year interest rate swap (paying fixed) at (8 + )%

against LIBOR. Should a customer pay the same credit-quality spread (m and ) on a

loan and on a swap?

Here are some quotes of the Swiss franc/U.S. dollar spot exchange rate given

simultaneously on the phone by three banks:

Bank A: 1.3435-1.3440

Bank B: 1.3435-1.3445

Bank C: 1.3445-1.3450

Are these quotes reasonable? Do you have an arbitrage opportunity?

An asset has a beta of 1.20. The variance of returns on a market index, is 225. If the

variance of returns for the asset is 400, what proportion of the asset’s total risk is

systematic, and what proportion is residual risk?

A Japanese pension fund wants to invest 1 billion in U.S. equity. Its board of trustees

must decide whether to invest in a commingled index fund tracking the S&P index or

give the money to an active manager. The board learns that this active manager turns

the portfolios over about twice a year. Given the size of the account, the overall

transaction costs are likely to be an average of 0.75% of each transaction€s value. The

active manager charges 0.5% in annual management fees, and the indexer charges

0.15%. By how much should the active manager outperform the index to cover the

extra costs in the form of fees and transaction costs on the annual turnover?

Guaranteed note.

You are a young banker offering a client to issue a guaranteed note. The yield curve is

flat at 9% for each maturity. Options on the stock index are offered by banks. A

at-the-money call with a two-year maturity trades at 12% of the index value, whereas a

three-year call is worth 15% of the index.

You wonder about the characteristics of the bond. If you offer a high coupon, the

indexation will be low. Therefore, you decide to compute the indexation levels in

accordance to the current market conditions for maturities of two and three years and

coupon levels of 0%, 2%, and 5%.

The current Swiss franc/U.S. dollar spot exchange rate is 2 Swiss francs per dollar, or

=2.

The expected inflation over the coming year is 2% in Switzerland and 5% in the United

States.

What is the expected value for the spot exchange rate a year from now, according to

purchasing power parity?