Reporting and Analyzing Long-Lived Assets

9-41

194. Goodwill

a. may be expensed upon purchase if desired.

b. can be sold by itself to another company.

c. can be purchased and charged directly to stockholders’ equity.

d. is only recorded when the purchase of an entire business occurs.

195. Which of the following is not an intangible asset that is reported on the balance sheet?

a. Goodwill.

b. Trademarks.

c. Employees.

d. Copyrights.

196. Trademarks are generally shown on the balance sheet under

a. Intangibles.

b. Investments.

c. Property, Plant, and Equipment.

d. Current Assets.

197. Hopson Company incurred $600,000 of research and development costs in its laboratory

to develop a new product. It spent $80,000 in legal fees for a patent granted on January 2,

2014. On July 31, 2014, Hopson paid $60,000 for legal fees in a successful defense of the

patent. What is the total amount that should be debited to Patents through July 31, 2012?

a. $600,000.

b. $140,000.

c. $740,000.

d. Some other amount.

198. Given the following account balances at year end, compute the total intangible assets on

the balance sheet of Janssen Enterprises.

Cash $1,500,000

Accounts Receivable 4,000,000

Trademarks 1,000,000

Goodwill 2,500,000

Research & Development Costs 2,000,000

a. $9,500,000.

b. $5,500,000.

c. $3,500,000.

d. $7,500,000.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-42

199. Which of the following statements concerning financial statement presentation is false?

a. Intangibles are reported separately under Intangible Assets.

b. The balances of major classes of assets may be disclosed in the footnotes.

c. The balances of the accumulated depreciation of major classes of assets may be

disclosed in the footnotes.

d. The balances of all individual assets, as they appear in the subsidiary plant ledger,

should be disclosed in the footnotes.

200. Intangible assets

a. should be reported under the heading Property, Plant, and Equipment.

b. are not reported on the balance sheet because they lack physical substance.

c. should be reported as Current Assets on the balance sheet.

d. should be reported as a separate classification on the balance sheet.

201. A company has the following assets:

Buildings and Equipment,

less accumulated depreciation of $5,000,000 $35,000,000

Copyrights 2,400,000

Patents 10,000,000

Land 12,000,000

The total amount reported under Property, Plant, and Equipment would be

a. $59,400,000.

b. $47,000,000.

c. $57,000,000.

d. $49,400,000.

202. Plant assets are ordinarily presented in the balance sheet

a. at current market values.

b. at replacement costs.

c. at cost less accumulated depreciation.

d. in a separate section along with intangible assets.

203. A company has the following assets:

Buildings and Equipment,

less accumulated depreciation of $4,000,000 $18,000,000

Copyrights 1,500,000

Patents 3,000,000

Land 5,000,000

The total amount reported under Property, Plant, and Equipment would be

a. $27,500,000.

b. $22,000,000.

c. $24,500,000.

d. $23,000,000.

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-43

*204. A company purchased office equipment for $30,000 and estimated a salvage value of

$6,000 at the end of its 10-year useful life. The constant percentage to be applied against

book value each year if the double-declining-balance method is used is

a. 10%.

b. 15%.

c. 20%.

d. 2%.

*205. A company purchased factory equipment for $350,000. It is estimated that the equipment

will have a $35,000 salvage value at the end of its estimated 5-year useful life. If the

company uses the double-declining-balance method of depreciation, the amount of annual

depreciation recorded for the second year after purchase would be

a. $140,000.

b. $84,000.

c. $126,000.

d. $75,600.

*206. A plant asset cost $128,000 and is estimated to have a $16,000 salvage value at the end

of its 8-year useful life. The annual depreciation expense recorded for the third year using

the double-declining-balance method would be

a. $10,720.

b. $18,000.

c. $15,750.

d. $12,250.

*207. On January 1, a machine with a useful life of five years and a residual value of $40,000

was purchased for $120,000. What is the depreciation expense for year 2 under the

double-declining-balance method of depreciation?

a. $28,800.

b. $48,000.

c. $38,400.

d. $23,040.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-44

*208. A factory machine was purchased for $70,000 on January 1, 2014. It was estimated that it

would have a $14,000 salvage value at the end of its 5-year useful life. It was also

estimated that the machine would be run 40,000 hours in the 5 years. If the actual number

of machine hours ran in 2014 was 4,000 hours and the company uses the units–of-activity

method of depreciation, the amount of depreciation expense for 2014 would be

a. $7,000.

b. $11,200.

c. $14,000.

d. $5,600.

*209. A machine with a cost of $480,000 has an estimated salvage value of $30,000 and an

estimated useful life of 5 years or 15,000 hours. It is to be depreciated using the units–of–

activity method of depreciation. What is the amount of depreciation for the second full

year, during which the machine was used 5,000 hours?

a. $150,000.

b. $90,000.

c. $130,000.

d. $160,000.

*210. Equipment with a cost of $480,000 has an estimated salvage value of $30,000 and an

estimated life of 4 years or 15,000 hours. It is to be depreciated using the units–of-activity

method. What is the amount of depreciation for the first full year, during which the

equipment was used 3,300 hours?

a. $120,000.

b. $135,600.

c. $99,000.

d. $112,500.

*211. Equipment with a cost of $300,000 has an estimated salvage value of $20,000 and an

estimated life of 4 years or 10,000 hours. It is to be depreciated by the units–of-activity

method. What is the amount of depreciation for the first full year, during which the

equipment was used 2,700 hours?

a. $75,000.

b. $70,000.

c. $75,600.

d. $72,500.

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-45

*212. On October 1, 2014, Hess Company places a new asset into service. The cost of the

asset is $80,000 with an estimated 5-year life and $20,000 salvage value at the end of its

useful life. What is the book value of the plant asset on the December 31, 2014, balance

sheet assuming that Hess Company uses the double-declining-balance method of

depreciation?

a. $52,000.

b. $60,000.

c. $72,000.

d. $76,000.

*213. Vickers Company uses the units-of-activity method in computing depreciation. A new plant

asset is purchased for $36,000 that will produce an estimated 100,000 units over its useful

life. Estimated salvage value at the end of its useful life is $3,000. What is the depreciation

cost per unit?

a. $3.30.

b. $3.60.

c. $0.33.

d. $0.36.

*214. Units-of-activity is an appropriate depreciation method to use when

a. it is impossible to determine the productivity of the asset.

b. the asset’s use will be constant over its useful life.

c. the productivity of the asset varies significantly from one period to another.

d. the company is a manufacturing company.

*215. The calculation of depreciation using the declining-balance method

a. ignores salvage value in determining the amount to which a constant rate is applied.

b. multiplies a constant percentage times the previous year’s depreciation expense.

c. yields an increasing depreciation expense each period.

d. multiplies a declining percentage times a constant book value.

*216. Foyle Company purchased a new van for floral deliveries on January 1, 2014. The van

cost $48,000 with an estimated life of 5 years and $12,000 salvage value at the end of its

useful life. The double-declining-balance method of depreciation will be used. What is the

depreciation expense for 2014?

a. $9,600.

b. $7,200.

c. $14,400.

d. $19,200.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-46

*217. Foyle Company purchased a new van for floral deliveries on January 1, 2013. The van

cost $48,000 with an estimated life of 5 years and $12,000 salvage value at the end of its

useful life. The double-declining-balance method of depreciation will be used. What is the

balance of the Accumulated Depreciation account at the end of 2014?

a. $7,680.

b. $23,040.

c. $30,720.

d. $11,520.

*218. Conley Company purchased equipment for $60,000 on January 1, 2012, and will use the

double-declining-balance method of depreciation. It is estimated that the equipment will

have a 5-year life and a $3,000 salvage value at the end of its useful life. The amount of

depreciation expense recognized in the year 2014 will be

a. $8,640.

b. $13,680.

c. $14,400.

d. $8,208.

*219. Interline Trucking purchased a tractor trailer for $84,000. Interline uses the units–of-activity

method for depreciating its trucks and expects to drive the truck 1,000,000 miles over its

12-year useful life. Salvage value is estimated to be $12,000. If the truck is driven 80,000

miles in its first year, how much depreciation expense should Interline record?

a. $5,333.

b. $6,720.

c. $5,760.

d. $6,222.

*220. Danford Trucking purchased a tractor trailer for $126,000. Danford uses the units–of–

activity method for depreciating its trucks and expects to drive the truck 1,000,000 miles

over its 12-year useful life. Salvage value is estimated to be $18,000. If the truck is driven

80,000 miles in its first year, how much depreciation expense should Danford record?

a. $8,000.

b. $10,080.

c. $8,640.

d. $9,333.

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-47

*221. All of the following statements are true regarding the declining-balance method of

depreciation except

a. the declining-balance method ignores salvage value when calculating depreciation.

b. the declining-balance method produces lower depreciation expense in the early years

as opposed to the later years.

c. the declining-balance method is compatible with the matching principle.

d. the declining-balance method is appropriate when assets lose their usefulness rapidly.

Answers to Multiple Choice Questions

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

9-48

BRIEF EXERCISES

Be. 222

Indicate whether each of the following expenditures should be classified as land (L), land

improvements (LI), buildings (B), equipment (E), or none of these (X).

_____ 1. Parking lots

_____ 2. Electricity used by a machine

_____ 3. Excavation costs

_____ 4. Interest on building construction loan

_____ 5. Cost of trial runs for machinery

_____ 6. Drainage costs

_____ 7. Cost to install a machine

_____ 8. Fences

_____ 9. Unpaid (past) property taxes assumed

_____10. Cost of tearing down a building when land and a building on it are purchased

Be. 223

Indicate whether each of the following expenditures should be classified as land (L), land

improvements (LI), buildings (B), equipment (E), or none of these (X).

_____ 1. Computer installation cost

_____ 2. Driveway cost

_____ 3. Architect’s fee

_____ 4. Surveying costs

_____ 5. Grading costs

_____ 6. Cost of lighting for parking lot

_____ 7. Insurance while in transit and freight on computer purchased

_____ 8. Material and labor costs incurred to construct factory

_____ 9. Cost of tearing down a warehouse on land just purchased

_____10. Utility cost during first year

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-49

Be. 224

Dobler Company purchased factory equipment with an invoice price of $78,000. Other costs

incurred were freight costs, $1,300; installation wiring and foundation, $2,200; material and labor

costs in testing equipment, $700; oil lubricants and supplies to be used with equipment, $500; fire

insurance policy covering equipment, $1,500. The equipment is estimated to have a $5,000

salvage value at the end of its 8-year useful service life.

Instructions

(a) Compute the acquisition cost of the equipment. Clearly identify each element of cost.

(b) If the straight-line method of depreciation was used, the annual rate applied to the

depreciable cost would be __________.

Be. 225

Revson Corporation purchased land adjacent to its plant to improve access for trucks making

deliveries. Expenditures incurred in purchasing the land were as follows: purchase price,

$55,000; broker’s fees, $6,000; title search and other fees, $5,000; demolition of an old building

on the property, $5,700; grading, $1,200; digging foundation for the road, $3,000; laying and

paving driveway, $25,000; lighting $7,500; signs, $1,500. List the items and amounts that should

be included in the Land account.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-50

Be. 226

Equipment was acquired on January 1, 2010, at a cost of $75,000. The equipment was originally

estimated to have a salvage value of $5,000 and an estimated life of 10 years. Depreciation has

been recorded through December 31, 2013, using the straight-line method. On January 1, 2014,

the estimated salvage value was revised to $7,000 and the useful life was revised to a total of 8

years.

Instructions

Determine the depreciation expense for 2014.

Be. 227

Equipment was acquired on January 1, 2011, at a cost of $170,000. The equipment was originally

estimated to have a salvage value of $10,000 and an estimated life of 10 years. Depreciation has

been recorded through December 31, 2013, using the straight-line method. On January 1, 2014,

the estimated salvage value was revised to $16,000 and the useful life was revised to a total of 8

years.

Instructions

Determine the depreciation expense for 2014.

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-51

Solution 227 (Cont.)

Be. 228

Gunselman Company purchased a machine on January 1, 2014. In addition to the purchase price

paid, the following additional costs were incurred:

(a) sales tax paid on the purchase price,

(b) transportation and insurance costs while the machinery was in transit from the seller,

(c) personnel training costs for initial operation of the machinery,

(d) installation costs necessary to secure the machinery to the building flooring,

(e) major overhaul to extend the life of the machinery,

(f) lubrication of the machinery gearing before the machinery was placed into service,

(g) lubrication of the machinery gearing after the machinery was placed into service, and

(h) annual city operating license.

Instructions

Indicate whether the items (a) through (h) are capital or revenue expenditures in the spaces

provided: C = Capital, R = Revenue.

(a)_____________ (b)______________ (c)______________ (d)______________

(e)_____________ (f)______________ (g)______________ (h)______________

Be. 229

Identify the following expenditures as capital expenditures or revenue expenditures.

(a) Replacement of worn out gears on factory machinery.

(b) Construction of a new wing on an office building.

(c) Painting the exterior of a building.

(d) Oil change on a company truck.

(e) Replacing an old computer chip with a faster chip, which increases productive capacity. No

extension of useful life expected.

(f) Overhaul of a truck motor. One year extension in useful life is expected.

(g) Purchased a wastebasket at a cost of $10.

(h) Painting and lettering of a used truck upon acquisition of the truck.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-52

Be. 230

For each item listed below, enter a code letter in the blank space to indicate the allocation

terminology for the item. Use the following codes for your answer:

A—Amortization D—Depreciation N—None of these

____ 1. Copyrights _____ 6. Research and Development Costs

____ 2. Land _____ 7. Equipment

____ 3. Buildings _____ 8. Franchises

____ 4. Patents _____ 9. Annual licensing fees

____ 5. Trademarks _____ 10. Land Improvements

Be. 231

Using the following data for Hayes, Inc., compute its asset turnover ratio and the return on assets

ratio.

Hayes, Inc.

Net Income 2014 $ 123,000

Total Assets 12/31/14 2,243,000

Total Assets 12/31/13 1,880,000

Net Sales 2014 2,135,000

Reporting and Analyzing Long-Lived Assets

9-53

Be. 232

Indicate in the blank spaces below, the section of the balance sheet where the following items are

reported. Use the following code to identify your answer:

PPE Property, Plant, and Equipment

I Intangibles

O Other

N/A Not on the balance sheet

_____ 1. Goodwill _____ 6. Research and Development Costs

_____ 2. Land Improvements _____ 7. Land

_____ 3. Buildings _____ 8. Franchises

_____ 4. Accumulated Depreciation _____ 9. Licenses

_____ 5. Trademarks _____ 10. Equipment

*Be 233

Kinney Company purchased a truck for $66,000. The company expected the truck to last four

years or 100,000 miles, with an estimated residual value of $8,000 at the end of that time. During

the second year the truck was driven 27,000 miles. Compute the depreciation for the second year

under each of the methods below and place your answers in the blanks provided.

Units-of-activity $

Double-declining-balance $

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-54

EXERCISES

Ex. 234

For each entry below make a correcting entry if necessary. If the entry given is correct, then state

“No entry required.”

(a) The $70 cost of repairing a printer was charged to Equipment.

(b) The $5,500 cost of a major engine overhaul was debited to Maintenance and Repairs

Expense. The overhaul is expected to increase the operating efficiency of the truck.

(c) The $6,000 closing costs associated with the acquisition of land were debited to Operating

Expenses.

(d) A $300 charge for transportation expenses on new equipment purchased was debited to

Freight-In.

Ex. 235

Kendrick Company was organized on January 1. During the first year of operations, the following

expenditures and receipts were recorded in random order.

Debits

1. Cost of real estate purchased as a plant site (land and building) $ 130,000

2. Accrued real estate taxes paid at the time of the purchase of the real estate 4,000

3. Cost of demolishing building to make land suitable for construction of a new

building 10,000

4. Architect’s fees on building plans 14,000

5. Excavation costs for new building 30,000

6. Cost of filling and grading the land 5,000

7. Insurance and taxes during construction of building 6,000

8. Cost of repairs caused by a small fire shortly after completion of building 7,000

9. Interest paid during the year, of which $45,000 pertains to the construction

period 74,000

10. Full payment to building contractor 955,000

11. Cost of parking lots and driveways 36,000

12. Real estate taxes paid for the current year on the land 4,000

Total Debits $1,275,000

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-55

Ex. 235 (Cont.)

Credits

13. Insurance proceeds for fire damage $3,000

14. Proceeds from salvage of demolished building 3,500

Total Credits $6,500

Instructions

Analyze the foregoing transactions using the following tabular arrangement. Insert the number of

each transaction in the Item space and insert the amounts in the appropriate columns.

Item Land Buildings Other Account Title

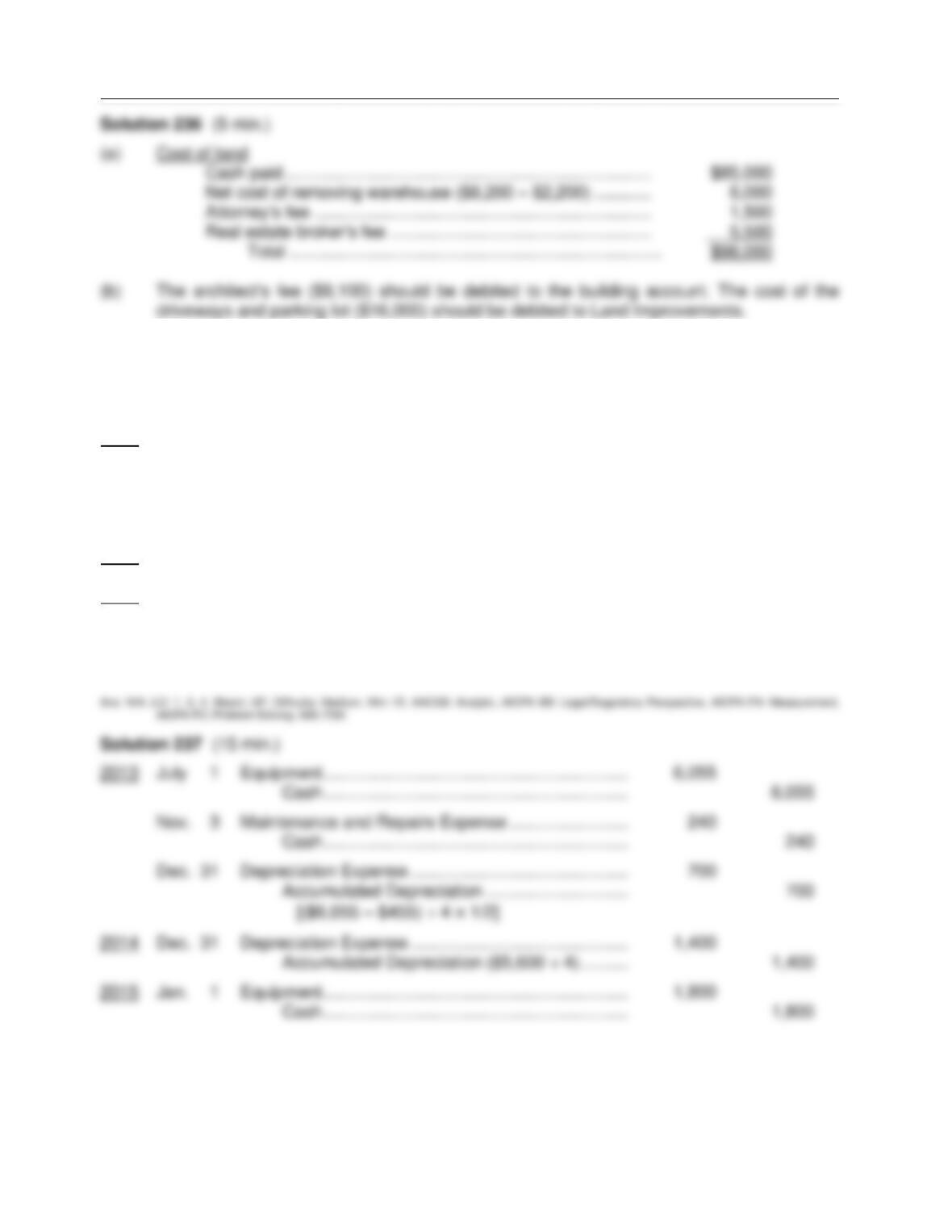

Ex. 236

On March 1, 2014, Geoffrey Company acquired real estate, on which it planned to construct a

small office building, by paying $85,000 in cash. An old warehouse on the property was

demolished at a cost of $8,200; the salvaged materials were sold for $2,200. Additional

expenditures before construction began included $1,500 attorney’s fee for work concerning the

land purchase, $5,500 real estate broker’s fee, $9,100 architect’s fee, and $16,000 to put in

driveways and a parking lot.

Instructions

(a) Determine the amount to be reported as the cost of the land.

(b) For each cost not used in part (a), indicate the account to be debited.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-56

Ex. 237

Mark’s Repair Service uses the straight-line method of depreciation. The company’s fiscal year

end is December 31. The following transactions and events occurred during the first three years.

2013 July 1 Purchased equipment from the Equipment Center for $5,500 cash plus sales

tax of $305, and shipping costs of $250.

Nov. 3 Incurred ordinary repairs on computer of $240.

Dec. 31 Recorded 2013 depreciation on the basis of a four-year life and estimated

salvage value of $455

2014 Dec. 31 Recorded 2014 depreciation.

2015 Jan. 1 Paid $1,800 for a major upgrade of the equipment. This expenditure is

expected to increase the operating efficiency and capacity of the equipment.

Instructions

Prepare the necessary entries. (Show computations.)

Reporting and Analyzing Long-Lived Assets

FOR INSTRUCTOR USE ONLY

9-57

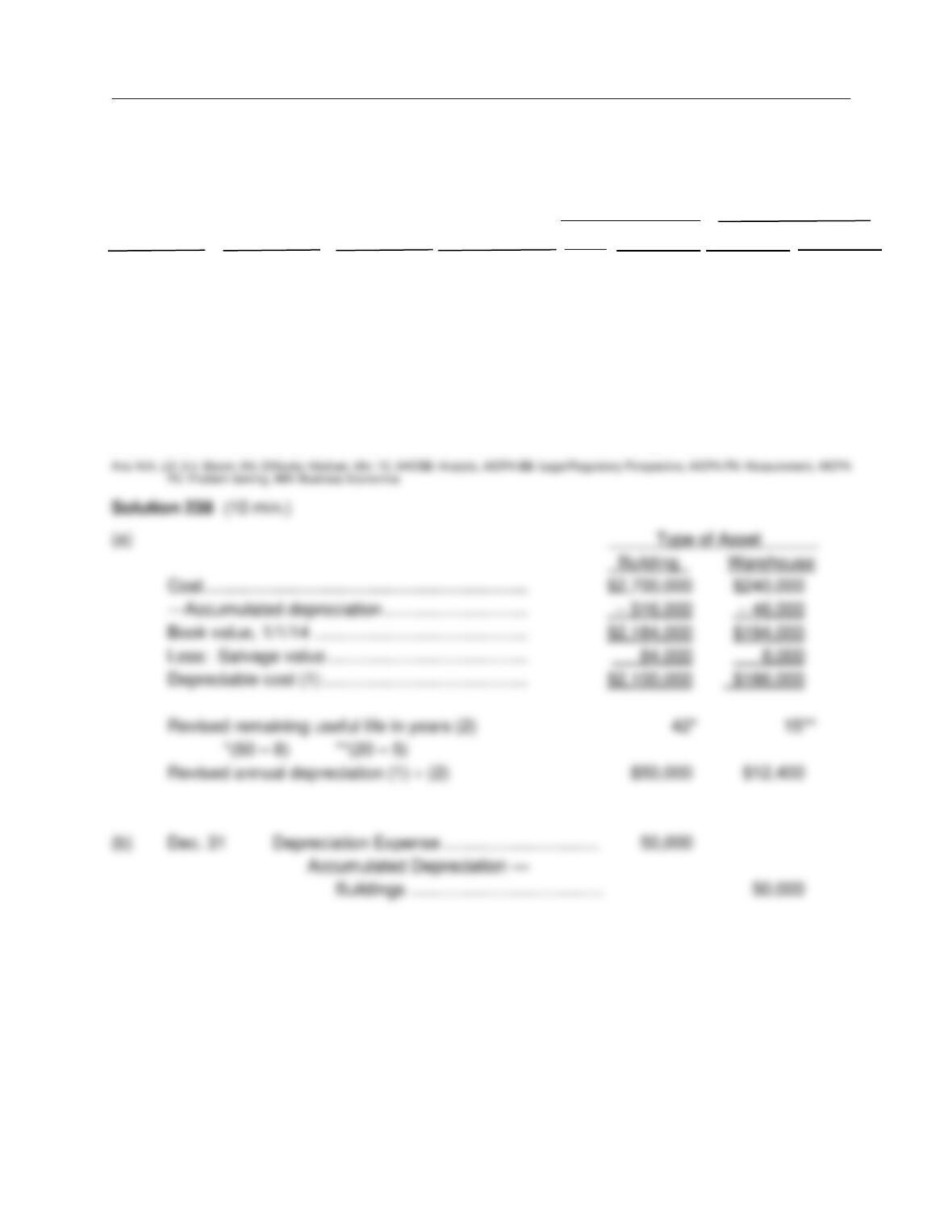

Ex. 238

Mike Geary, the controller of Shellhammer Company, has reviewed the expected useful lives and

salvage values of selected depreciable assets at the beginning of 2014. Here are his findings:

Type of

Asset

Date

Acquired

Cost

Accumulated

Depreciation,

Jan. 1, 2014

Useful Life

(in Years)

Salvage Value

Old

Proposed

Old

Proposed

Building

Jan. 1, 2006

$2,700,000

$516,000

40

50

$120,000

$84,000

Warehouse

Jan. 1, 2009

240,000

46,000

25

20

10,000

8,000

All assets are depreciated by the straight-line method. Shellhammer Company uses a calendar

year in preparing annual financial statements. After discussion, management has agreed to

accept Mike‘s proposed changes. (The “Proposed” useful life is total life, not remaining life.)

Instructions

(a) Compute the revised annual depreciation on each asset in 2014. (Show computations.)

(b) Prepare the entry (or entries) to record depreciation on the building in 2014.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-58

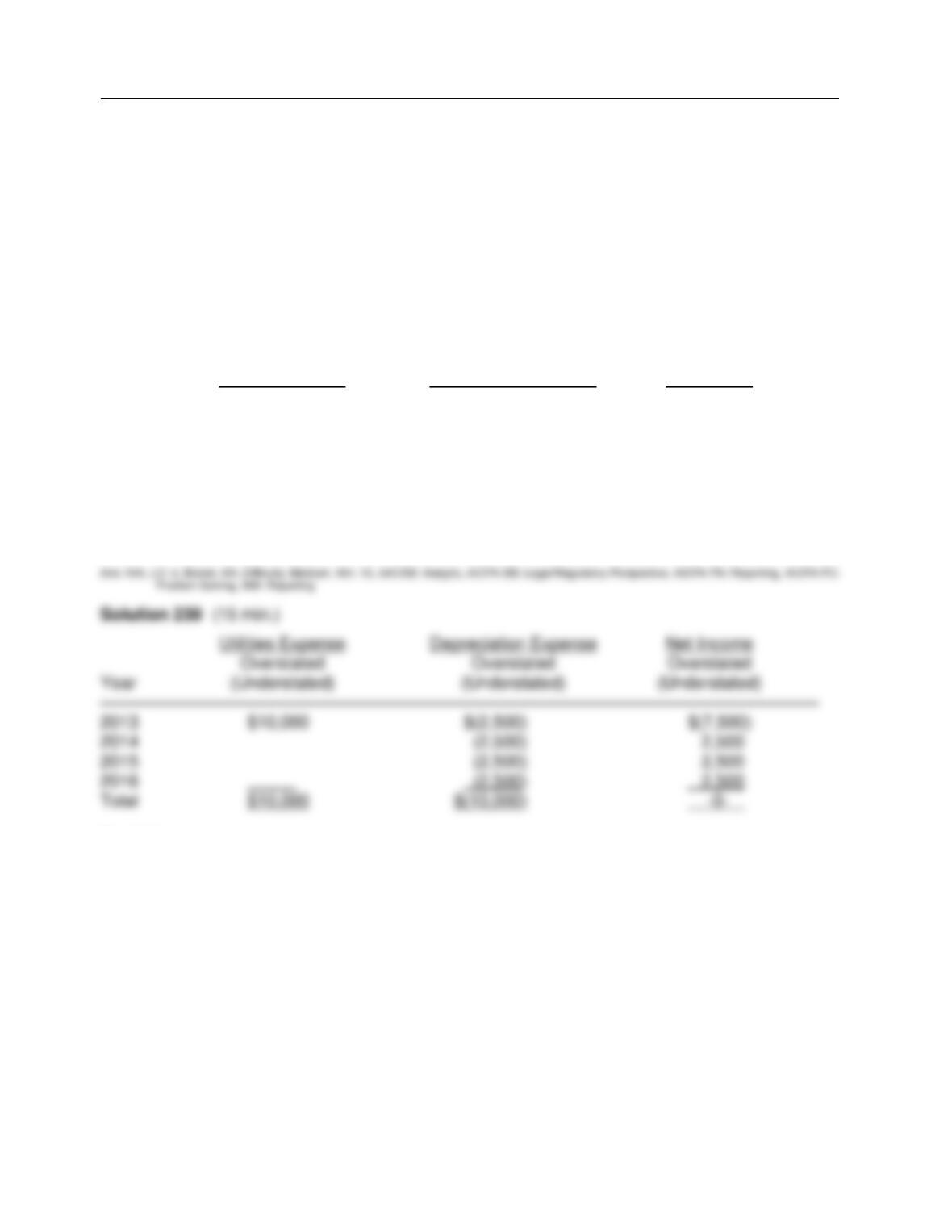

Ex. 239

On January 1, 2012, Keller Company purchased and installed a telephone system at a cost of

$20,000. The equipment was expected to last five years with a salvage value of $3,000. On

January 1, 2013, more telephone equipment was purchased to tie-in with the current system for

$10,000. The new equipment is expected to have a useful life of four years. Through an error, the

new equipment was debited to Utilities Expense. Keller Company uses the straight-line method of

depreciation.

Instructions

Prepare a schedule showing the effects of the error on Utilities Expense, Depreciation Expense,

and Net Income for each year and in total beginning in 2013 through the useful life of the new

equipment.

Utilities Expense Depreciation Expense Net Income

Overstated Overstated Overstated

Year (Understated) (Understated) (Understated)

——————————————————————————————————————————

2013

2014

2015

2016

Ex. 240

(a) Faster Company purchased equipment in 2007 for $104,000 and estimated an $8,000

salvage value at the end of the equipment’s 10-year useful life. At December 31, 2013, there

was $67,200 in the Accumulated Depreciation account for this equipment using the straight–

line method of depreciation. On March 31, 2014, the equipment was sold for $21,000.

Prepare the appropriate journal entries to remove the equipment from the books of Faster

Company on March 31, 2014.

(b) Lewis Company sold equipment for $11,000. The equipment originally cost $25,000 in 2011

and $6,000 was spent on a major overhaul in 2014 (charged to the Equipment account).

Accumulated Depreciation on the equipment to the date of disposal was $20,000.

Prepare the appropriate journal entry to record the disposition of the equipment.

Reporting and Analyzing Long-Lived Assets

9-59

Ex. 240 (Cont.)

(c) Selby Company sold equipment that had a book value of $13,500 for $15,000. The

equipment originally cost $45,000 and it is estimated that it would cost $57,000 to replace

the equipment.

Prepare the appropriate journal entry to record the disposition of the equipment.

Ex. 241

Prepare the journal entries to record the following transactions for Reese Company, which has a

calendar year end and uses the straight-line method of depreciation.

(a) On September 30, 2014, the company sold old equipment for $46,000. The equipment was

purchased on January 1, 2012, for $96,000 and was estimated to have a $16,000 salvage

value at the end of its 5-year life. Depreciation on the equipment has been recorded through

December 31, 2013.

(b) On June 30, 2014, the company sold old equipment for $24,000. The equipment originally

cost $36,000 and had accumulated depreciation to the date of disposal of $15,000.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

9-60

Ex. 242

a. A machine that cost $36,000 and on which $26,500 of depreciation had been recorded was

disposed of for $10,200. Indicate whether a gain or loss should be recorded, and for what

amount.

b. Assume that the machine of Part a, above, was instead discarded. Indicate whether a gain or

loss should be recorded, and for what amount.

c. Assume that the machine of Part a, above, was instead sold for $9,400. Indicate whether a

gain or loss should be recorded, and for what amount.

Ex. 243

Presented below are selected transactions for the Tinker Company for 2015.

Jan. 1 Retired a piece of equipment that was purchased on January 1, 2005. The equipment

cost $75,000 on that date, and had a useful life of 10 years with no salvage value.

April 30 Sold equipment for $38,000 that was purchased on January 1, 2012. The equipment

cost $105,000, and had a useful life of 5 years with no salvage value.

Dec. 31 Discarded equipment that was purchased on June 30, 2011. The equipment cost

$42,000 and was depreciated on a 5-year useful life with a salvage value of $2,000.