8) Which of the following statements is FALSE?

A) The firm’s weighted average cost of capital (WACC) denoted rwacc is the cost of capital that reflects

the risk of the overall business, which is the combined risk of the firm’s equity and debt.

B) Intuitively, the difference between the discounted free cash flow model and the dividend-discount

model is that in the divided-discount model the firm‘s cash and debt are included indirectly through the

effect of interest income and expenses on earnings in the dividend-discount model.

C) We interpret rwacc as the expected return the firm must pay to investors to compensate them for the

risk of holding the firm’s debt and equity together.

D) When using the discounted free cash flow model we should use the firm’s equity cost of capital.

9) Which of the following statements is FALSE?

A) The long-run growth rate gFCF is typically based on the expected long-run growth rate of the firm’s

revenues.

B) Because the firm’s free cash flow is equal to the sum of the free cash flows from the firm’s current and

future investments, we can interpret the firm’s enterprise value as the total NPV that the firm will earn

from continuing its existing projects and initiating new ones.

C) If the firm has no debt then rwacc = the risk-free rate of return.

D) When using the discounted free cash flow model, we forecast the firm’s free cash flow up to some

horizon, together with some terminal (continuation) value of the enterprise.

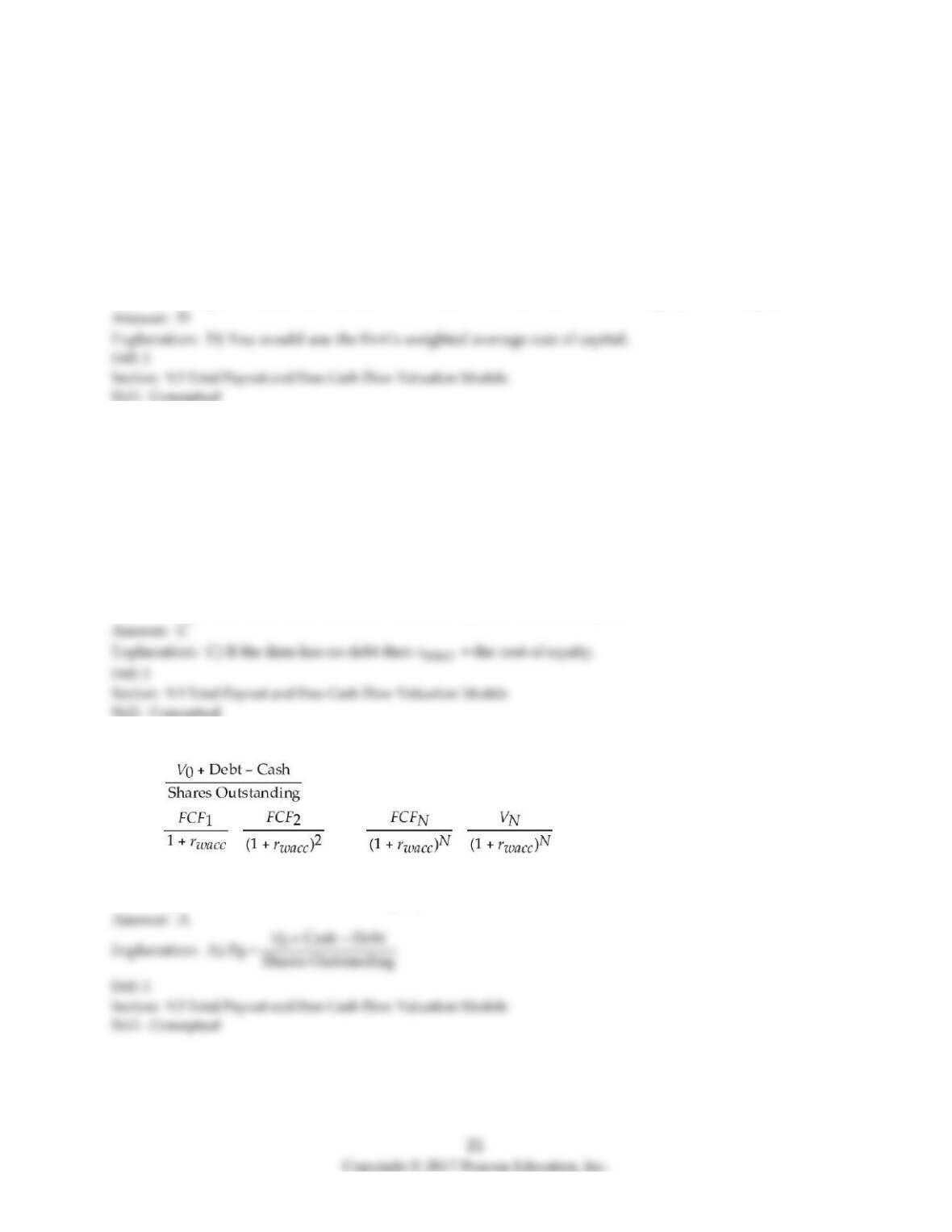

10) Which of the following equations is INCORRECT?

A) P0 =

B) V0 = + + … + +

C) Free Cash Flow = EBIT × (1 – τc) + Depreciation – Capital Expenditures – DNWC

D) Enterprise Value = Market Value of Equity + Debt – Cash

Use the following information to answer the question(s) below.

Taggart Transcontinental pays no dividends, but spent $4 billion on share repurchases last year.

Taggart’s equity cost of capital is 13% and the amount spent on repurchases is expected to grow by 5%

per year. Taggart currently has 2 billion shares outstanding.

11) Taggart’s market capitalization is closest to:

A) $25 billion

B) $31 billion

C) $40 billion

D) $50 billion

12) Taggart’s stock price is closest to:

A) $12.50

B) $15.40

C) $20.00

D) $25.00

Use the following information to answer the question(s) below.

Wyatt Oil, an all-equity financed firm, has just reported EPS of $4.00 per share. Despite an economic

downturn, Wyatt is confident regarding its current investment opportunities, but due to the current

financial crisis, Wyatt does not wish to fund these investments externally. Wyatt‘s board has therefore

decided to suspend its stock repurchase plan and cut its dividend to $1 per share (from its current level

of $2 per share) and retain these funds instead. The firm just paid its current dividend of $1.00 per share

and expects to keep its dividend at $1 per share next year as well. In subsequent years, it expects its

growth opportunities to slow, and it will still be able to fund its growth internally with a target 40%

dividend payout ratio, and reinitiating its stock repurchase plan for a total payout rate of 60%. All

dividends and repurchases occur at the end of each year.

Wyatt’s existing operations are expected to generate the current level of earnings per share in the future.

Assume that the return on new investments is 16% and that reinvestments will account for all future

earnings growth. Wyatt’s current equity cost of capital is 12%.

13) Wyatt’s expected EPS in two years is closest to:

A) $4.48

B) $4.64

C) $5.04

D) $5.38

14) Wyatt’s current stock price is closest to:

A) $51.23

B) $54.00

C) $49.11

D) $61.38

15) The Rufus Corporation has 125 million shares outstanding and analysts expect Rufus to have

earnings of $500 million this year. Rufus plans to pay out 40% of its earnings in dividends and they

expect to use another 20% of their earnings to repurchase shares. If Rufus’ equity cost of capital is 15%

and Rufus’ earnings are expected to grow at a rate of 3% per year, then the value of a share of Rufus

stock is closest to:

A) $13.35

B) $33.50

C) $20.00

D) $16.00

Use the information for the question(s) below.

You expect CCM Corporation to generate the following free cash flows over the next five years:

Year

1

2

3

4

5

FCF ($ millions)

25

28

32

37

40

Following year five, you estimate that CCM‘s free cash flows will grow at 5% per year and that CCM’s

weighted average cost of capital is 13%.

16) The enterprise value of CCM corporation is closest to:

A) $396 million

B) $290 million

C) $382 million

D) $350 million

17) If CCM has $200 million of debt and 8 million shares of stock outstanding, then the share price for

CCM is closest to:

A) $49.50

B) $12.50

C) $19.35

D) $24.50

18) If CCM has $150 million of debt and 12 million shares of stock outstanding, then the share price for

CCM is closest to:

A) $49.50

B) $11.25

C) $20.50

D) $22.75

Use the information for the question(s) below.

Defenestration Industries plans to pay a $4.00 dividend this year and you expect that the firm’s earnings

are on track to grow at 5% per year for the foreseeable future. Defenestration’s equity cost of capital is

13%.

19) Assuming that Defenestration’s dividend payout rate and expected growth rate remain constant,

and Defenestration does not issue or repurchase shares, then Defenestration’s stock price is closest to:

A) $50.00

B) $32.30

C) $22.25

D) $30.75

20) Suppose that Defenestration decides to pay a dividend of only $2 per share this year and use the

remaining $2 per share to repurchase stock. If Defenestration’s payout rate remains constant, then

Defenestration’s stock price is closest to:

A) $50.00

B) $22.25

C) $32.30

D) $30.75

28

21) Suppose that Defenestration decides to pay a dividend of only $2 per share this year and use the

remaining $2 per share to repurchase stock. If Defenestration maintains this dividend and total payout

rate, then the rate at which Defenestration’s dividends and earnings per share are expected to grow is

closest to:

A) 7%

B) 13%

C) 9%

D) 5%

22) A firm’s net investment is:

A) its capital expenditures in excess of depreciation.

B) its free cash flow net of increases in working capital.

C) its enterprise value in excess of debt owed.

D) the market value of equity plus debt.

Use the information for the question(s) below.

You expect DM Corporation to generate the following free cash flows over the next five years:

Year

1

2

3

4

5

FCF ($ millions)

75

84

96

111

120

Beginning with year six, you estimate that DM‘s free cash flows will grow at 6% per year and that DM‘s

weighted average cost of capital is 15%.

23) Calculate the enterprise value for DM Corporation.

24) If DM has $500 million of debt and 14 million shares of stock outstanding, then what is the price per

share for DM Corporation?

9.4 Valuation Based on Comparable Firms

1) Which of the following statements is FALSE?

A) Even two firms in the same industry selling the same types of products, while similar in many

respects, are likely to be of different size or scale.

B) In the method of comparables, we estimate the value of the firm based on the value of other,

comparable firms or investments that we expect will generate very similar cash flows in the future.

C) Consider the case of a new firm that is identical to an existing publicly traded company. If these

firms will generate identical cash flows, the Law of One Price implies that we can use the value of the

existing company to determine the value of the new firm.

D) A valuation multiple is a ratio of some measure of the firm’s scale to the value of the firm.

2) Which of the following statements is FALSE?

A) The most common valuation multiple is the price-earnings (P/E) ratio.

B) You should be willing to pay proportionally more for a stock with lower current earnings.

C) A firm’s P/E ratio is equal to the share price divided by its earnings per share.

D) The intuition behind the use of the P/E ratio is that when you buy a stock, you are in sense buying

the rights to the firm‘s future earnings and differences in the scale of the firms’ earnings are likely to

persist.

3) Which of the following statements is FALSE?

A) We can estimate the value of a firm’s shares by multiplying its current earnings per share by the

average P/E ratio of comparable firms.

B) For valuation purposes, the trailing P/E ratio is generally preferred, since it is based on actual not

expected earnings.

C) Forward earnings are the expected earnings over the coming 12 months.

D) Trailing earnings are the earnings over the previous 12 months.

4) Which of the following statements is FALSE?

A) Because the enterprise value represents the entire value of the firm before the firm pays its debt, to

form an appropriate multiple, we divide it by a measure of earnings or cash flows after interest

payments are made.

B) We can compute a firm’s P/E ratio by using either trailing earnings or forward earnings with the

resulting ratio called the trailing P/E or forward P/E.

C) It is common practice to use valuation multiples based on the firm’s enterprise value.

D) Using a valuation multiple based on comparables is best viewed as a “shortcut” to the discounted

cash flow method of valuation.

5) Which of the following statements is FALSE?

A) The fact that a firm has an exceptional management team, has developed an efficient manufacturing

process, or has just secured a patient on a new technology is ignored when we apply a valuation

multiple.

B) Valuation multiples have the advantage that they allow us to incorporate specific information about

the firm’s cost of capital or future growth.

C) For firms with substantial tangible assets, the ratio of price to book value of equity per share is

sometimes used.

D) Using multiples will not help us determine if an entire industry is overvalued.

6) Which of the following statements is FALSE?

A) Because capital expenditures can vary substantially from period to period, most practitioners rely on

enterprise value to free cash flow multiples.

B) Common multiples to consider are enterprise value to EBIT, EBITDA, and free cash flow.

C) If two stocks have the same payout and EPS growth rates as well as equivalent risk, then they should

have the same P/E ratio.

D) Looking at enterprise value as a multiple of sales can be useful if it is reasonable to assume that the

firms will maintain similar margins in the future.

7) Which of the following formulas is INCORRECT?

A) Forward =

B) Forward =

C) =

D) Forward =