9-1

Chapter 9

Answers to Review Problems

Finance For Executives – 4th Edition

1. Structure and characteristics of financial markets.

a.

In a rights offering, shares are issued exclusively to the firm’s existing shareholders, whereas in a

general cash offering they are sold to any interested buyer.

b.

c.

The originating house is the investment bank that has initiated the issue, whereas the selling

group consists of a number of banks which are brought in to help distribute portions of the shares

that have been allocated to them by the originating house or lead manager.

d.

e.

Credit risk refers to the ability of a firm to service the bonds it has issued (pay interest and repay

the principal) while market risk refers to the unexpected changes in the price of bonds in response

to changes in the rates of interest.

f.

9-2

2. Rights issue.

a.

The number of rights MEC will grant must be equal to the number of MEC’s shares outstanding,

that is, 50 million rights.

b.

c.

The price will drop to $25 to reflect the fact that the share has gone ex-rights, that is, it entitles the

holder to buy new shares at $20. The ex-rights price is (see equation 9.2):

d.

The value of one right is simply $1, the difference between the rights-on price ($26) and the ex-

rights price ($25). It can also be calculated directly with the formula in footnote 13:

9-3

3. Leasing versus borrowing.

The relevant cash flows and the computation of the net present value of lease versus buy are

presented in a spreadsheet format.

A

B

C

D

E

F

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

9

10

Scrap value

-$3,000

11

12

Cash saved from not buying the truck

24,000

13

14

Total differential cash flow

$20,100

-$6,300

-$6,300

-$6,300

-$5,400

15

16

Cost of debt

6%

17

18

19

20

21

22

23

24

a.

Discounting the total differential cash flows at the after-tax cost of debt of 6% yields a negative

net present value, or net advantage of leasing, of –$1,017.

b.

OS Distributors will be indifferent between buying or leasing if the net advantage of leasing

(NAL) is zero, that is, if the present value at 6% of the differential cash flows from year 1 to year

4 is equal to $20,100 (the difference between the cash saved from not buying the truck and the

after tax lease payment now, cell B14) :

Lease payments

-$6,500

-$6,500

-$6,500

4

Tax rate

5

After-tax lease payments

Depreciation expenses

8

Loss of tax savings on depreciation

9-4

4. Leasing.

Using a spreadsheet, the following table shows the after-tax cash flows to Thorenberg Inc. and for

Thorsten Leasing Corporation and the net advantage to leasing to Thorenberg Inc.

A

B

C

D

E

F

G

1

Now

Year 1

Year 2

Year 3

Year 4

Year 5

2

Cash flows to Thorenberg

3

Purchase price

$100,000

4

Depreciation expenses

$20,000

$20,000

$20,000

$20,000

$20,000

5

Lease payments

$25,000

$25,000

$25,000

$25,000

$25,000

6

Corporate tax rate

7

After-tax lease payments

$16,000

$16,000

$16,000

$16,000

$16,000

8

depreciation

9

Differential cash flow

84,000

-23,200

-23,200

-23,200

-23,200

-7,200

10

11

Interest rate

8.00%

12

After-tax interest rate

5.12%

13

14

Net advantage to leasing

-$3,647

15

16

17

18

19

20

21

22

9-5

23

24

Cash flows to Foster

Now

Year 1

Year 2

Year 3

Year 4

Year 5

25

a.

The net advantage to leasing is negative for Thorenberg Inc.: –$3,646. Thus, the firm should buy

rather than lease the equipment.

b.

c.

Leasing cannot take place if the cash flows to the lessee and the lessor are exactly the opposite

and if their borrowing rate is the same. The leasing will take place only if any of these two

conditions is not met. That would happen if:

• The two firms are subject to different effective tax rates

5. Bond valuation.

The market value of a bond is the present value of the bond’s future coupons and principal

repayment discounted at the market interest rate relevant to the risk and maturity of the bond:

26

Purchase price

$100,000

27

Tax savings on depreciation

28

After-tax lease receipts

29

$23,200

$23,200

$7,200

9-6

End of Year

1

….

9

10

11

…..

19

20

Bond A

$100

….

$100

$1,100

Bond B

0

….

$0

$1,000

Bond C

100

….

$100

$100

$100

$100

$100

$1,100

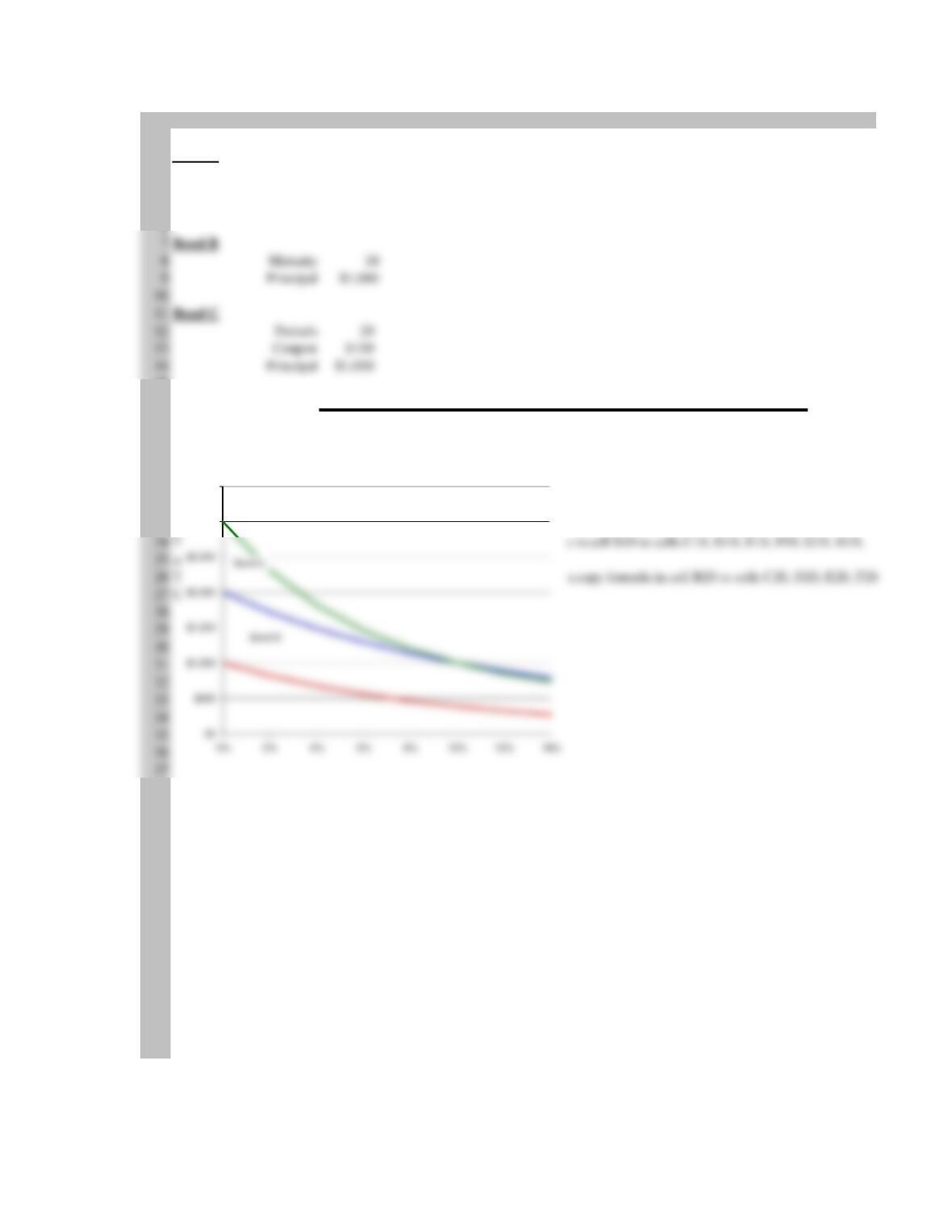

9-7

A B C D E F G H I

1

2Bond A

3 Periods 10

4 Coupon $100 100

5 Principal $1,000

15

16

Market interest rate 0% 2% 4% 6% 8% 10% 12% 14%

17

18 Price Bond A $2,000 $1,719 $1,487 $1,294 $1,134 $1,000 $887 $791

19 Price Bond B $1,000 $820 $676 $558 $463 $386 $322 $270

20 Price Bond C $3,000 $2,308 $1,815 $1,459 $1,196 $1,000 $851 $735

21

22 The formula in cell B18 is: =-PV(B16,$B$3,$B$4,$B$5,1). Then copy formula in cell B18 to cells C18, D18, E18, F18, G18,

23 H18, and I18.

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

$3,000

$3,500

Bond C

9-8

6. Bond valuation.

The rate on the new bond must be the same as the current market yield on the outstanding bond

since both bonds have the same maturity (10 years) and same credit risk (they are both issued by

the same firm). Note that the announcement that the firm’s target debt–to-equity ratio is not going

to change is a signal that the firm’s financial risk is not going to be affected by the bond issue.

Year

1

2

….

9

10

Cash flow

$100

$100

….

$100

$1,100

The bond’s yield kD is the solution of the following equation:

Using a spreadsheet with the formula mentioned in the section “Finding the Yield of a Bond

When Its Price Is Known” gives the same rate:

A

B

C

D

E

F

G

H

1

Number of periods

10

2

3

Coupon payment

$100

4

5

Market price

$1,065

6

7

Principal repayment

8

9

10

11

9-9

7. Valuation of bonds.

a.

Using a spreadsheet as in the chapter the market prices of the three bonds are calculated as

follows:

A

B

C

D

E

F

G

1

2

Coupon bond

3

Periods

5

10

11

Perpetual bond

12

Coupon

$60

13

14

Market price

15

Market rate

7.0%

7.5%

16

Coupon bond

17

Zero-coupon bond

18

Perpetual bond

19

20

Percentage change

21

Coupon bond

-2.05%

22

Zero-coupon bond

-2.30%

23

Perpetual bond

-6.67%

24

25

26

27

28

29

b.

Bond values are below their face values because the market yield (7%) is above the coupon rate

(6%). Rates have gone up (from 6% to 7%) and, hence, bond values have gone down.

4

Coupon

$60

Zero-coupon bond

9-10

c.

d.

Value of option = Value of convertible – Value if nonconvertible = $1,040 – $959 = $81

e.

8. Common stock valuation.

In an efficient market, the market value of a security is the present value of the cash-flow stream

that is expected from the security’s issuer discounted at the market required rate of return (12

percent).

The payments expected from Therol Co. to the current and future owners of a firm’s share of

common stock are the expected dividends. They can be computed as follows:

Year-end

1

2

3

Dividend

$1.2 (1 + .16) = $1.392

$1.2 (1 + .16)2 = $1.615

$1.2 (1 + .16)3 = $1.873

Year-end

Dividend

$1.873 (1 + .12) = $2.098

After the end of year 5, the dividend is expected to grow forever at a constant rate of six percent.

Since the dividend at that point in time is expected to be $2.350, the expected share price at the

end of year 5 is simply the present value of an annuity of $2.350 × (1+.06) growing at 6 percent

forever. At the required rate of 12 percent, this is $ 41.517, which is $2.491/(12%-6%).

9-11

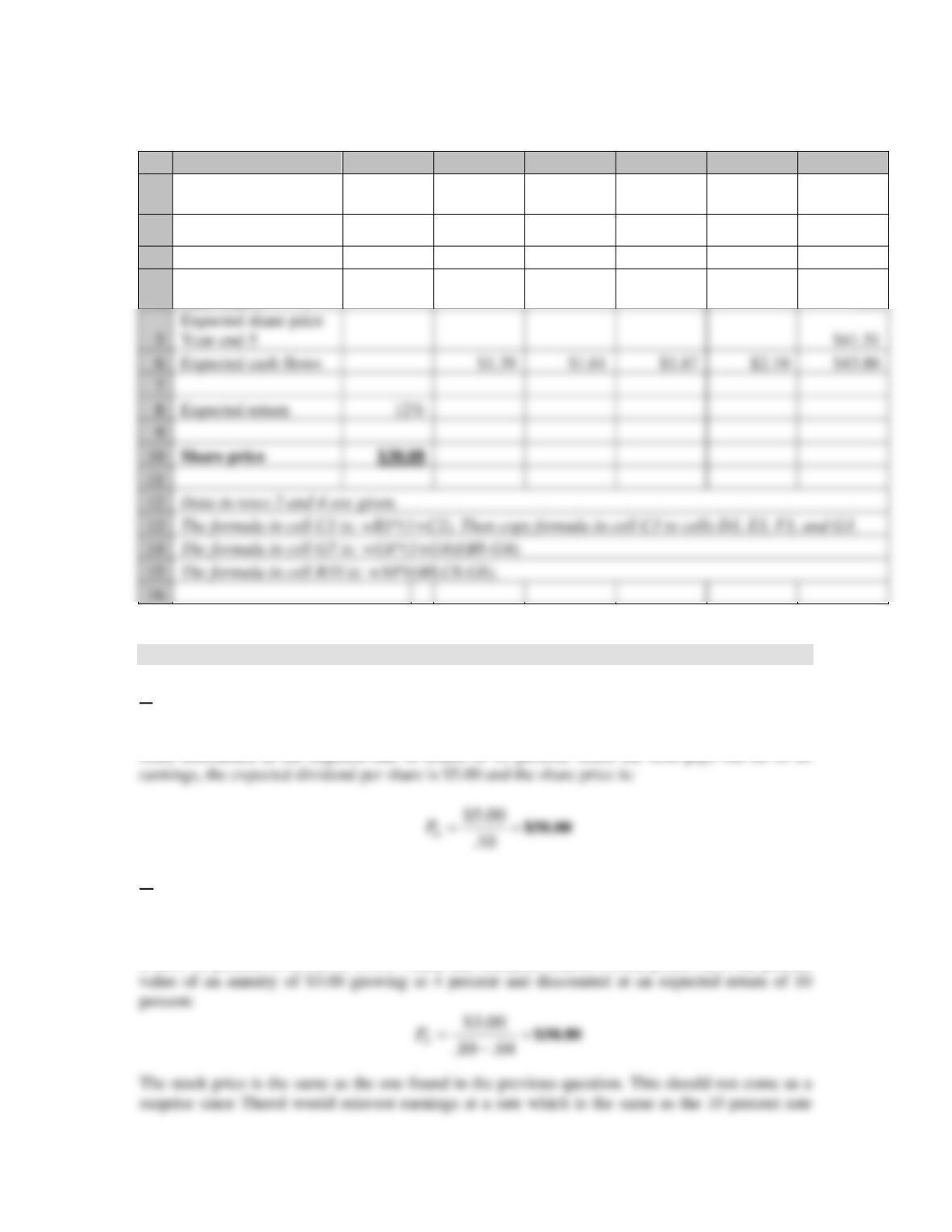

The same calculations could have been done with a spreadsheet as follows:

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

Expected growth rate

16%

16%

16%

12%

12%

3

Expected dividend

$1.20

$1.39

$1.61

$1.87

$2.10

$2.35

4

Expect growth rate

after Year 5

6%

9. Growth stocks versus income stocks.

a.

Therol’s stock price, P0, is the value of a constant annuity equal to the expected dividend per

share discounted at the required rate of return of 10 percent. Since the firm pays out all of its

b.

If the firm plows back 40 percent of its earnings with an expected return of 10 percent, its

earnings will grow at a rate of 10 percent .40 = 4 percent. So will its dividend per share, which

is now 60 percent of $5.00, or $3.00. Under this scenario, Therol’s stock price, P0, is the present

5

Expected share price

Year-end 5

6

Expected cash flows

7

8

Expected return

9

10

11

12

13

14

15

16

9-12

c.

If the return on 40 percent of earnings is 15 percent instead of 10 percent, then dividends can be

expected to grow at a rate of 15 percent .40 = 6 percent and Therol’s stock price, P0, would be:

10. Valuation of preferred shares and common stocks.

a.

Value of the preferred =

51.46$

086.0

4$ =

b.

c.

A

B

C

D

E

F

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

2

Expected growth rate

8%

8%

8%

4%

3

Expected dividend

$3.50

$3.78

$4.08

$4.41

$4.59

4

Share price – End-of-Year 4

$59.67

5

Expected cash flows

$3.78

$4.08

$4.41

$64.19

6

Expected return

7

8

9

9-13

d.

The observed market price of $53.24 is 5.3% higher than the estimated value of $50.56. This can

be interpreted as follows. If we assume that the estimated value is “correct,” then the shares are

overpriced and should be sold. If we assume that the price is “correct,” then the model and the

assumptions we have used to estimate the value of a share are incorrect and should be revised.