Multiple Choice Test Bank Questions No Feedback – Chapter 8

Correct answers denoted by an asterisk.

1. Which of the following are probably valid criticisms of the Dickey Fuller

methodology?

(i) The tests have a unit root under the null hypothesis and this may not be rejected due to

insufficient information in the sample

(ii) the tests are poor at detecting a stationary process with a unit root close to the non–

stationary boundary

(iii) the tests are highly complex to calculate in practice

(iv) the tests have low power in small samples

2. Which of the following are problems associated with the Engle-Granger approach to

modelling using cointegrated data?

(i) The coefficients in the cointegrating relationship are hard to calculate

(ii) This method requires the researcher to assume that one variable is the dependent

variable and the others are independent variables

(iii) The Engle-Granger technique can only detect one cointegrating relationship

(iv) Engle-Granger does not allow the testing of hypotheses involving the actual

cointegrating relationship.

3. Consider the following vector error correction (VECM) model:

yt = yt-5 + 1yt-1 + 2yt-2 + 3yt-3 + 4yt-4 + ut

where yt is a k 1 vector of variables, and ut is a k 1 vector of disturbances.

Which of the following statements is true of the VECM?

4. Consider the following matrix:

X=

3 6

1 2

What are its characteristic roots?

5. You have the following data for Johansen’s

max rank test for cointegration between 4

international equity market indices:

r

max

5% Critical Value

0

40.03

30.26

1

26.81

23.84

2

13.42

17.72

3

8.66

10.71

How many cointegrating vectors are there?

6. Which criticism of Dickey-Fuller (DF) -type tests is addressed by stationarity tests,

such as the KPSS test?

7. Consider the following data generating process for a series yt:

ttt uyy ++= −1

5.1

Which one of the following most accurately describes the process for yt?

8. Which one of the following best describes most series of asset prices?

9. If there are three variables that are being tested for cointegration, what is the maximum

number of linearly independent cointegrating relationships that there could be?

10. If the number of non-zero eigenvalues of the pi matrix under a Johansen test is 2, this

implies that

11. If a Johansen “max” test for a null hypothesis of 1 cointegrating vectors is applied to

a system containing 4 variables is conducted, which eigenvalues would be used in the

test?

12. Consider the testing of hypotheses concerning the cointegrating vector(s) under the

Johansen approach. Which of the following statements is correct?

13. Which of these is a characteristic of a stationary series?

14. Which of the following are consequences of using non-stationary data in regressions?

(I) Shocks will be persistent

(II) It can lead to spurious regressions

(III) t-ratios will not follow a t-distribution

(IV) F-Statistic will not follow an F-distribution

15. What is the impact of shocks to an AR(1) with no drift

1t t t

y y u

−

= + +

if

1

?

16. What is the impact of shocks to an AR(1) with no drift

1t t t

y y u

−

= + +

if

1

=

?

17. To induce stationarity in a deterministic trend-stationary process

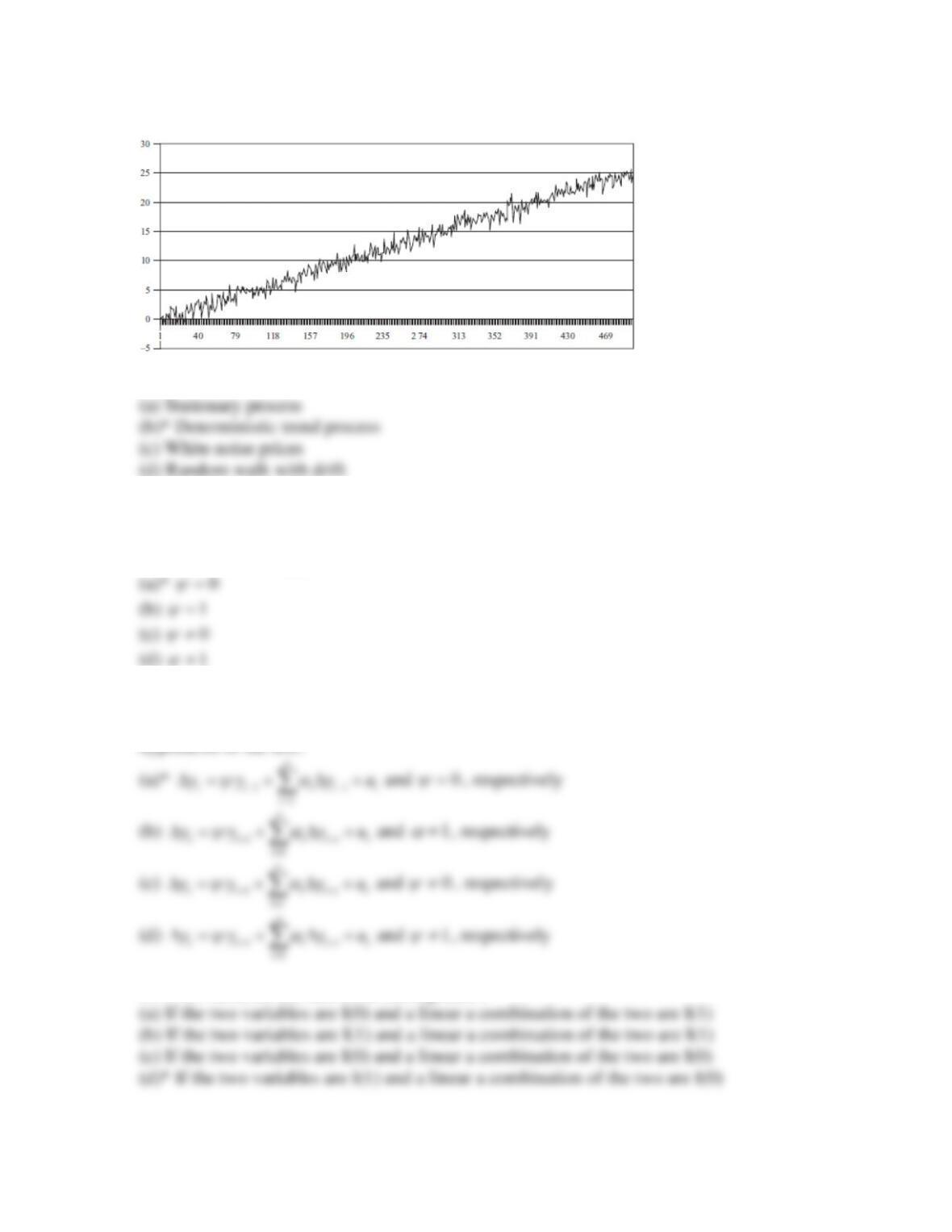

18. The plotted series in the following graph is an example of a:

19. A researcher would like to test for a unit root in a series. She runs the regression

1t t t

y y u

−

= +

. What should her null hypothesis be assuming that she adopts the

Dickey-Fuller test approach?

20. Assuming the researcher in question 19 would like to run an augmented Dickey-

Fuller test instead. What is the appropriate regression she would have to run and the null

hypothesis of the test?

21. Two variables are said to be cointegrated if

22. Assume that you are trying to model the relationship between house prices and rents.

If you find that both series are non-stationary and a linear combination of the two series is

stationary, which of the following is true?

(I) Regressing the levels of house prices on the levels of rents could lead to spurious

regressions

(II) House prices and rents are cointegrated

(III) An appropriate linear combination of house prices and rents is I(1)

(IV) House prices and rents are not cointegrated