Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 8: Operating Assets: Property, Plant and Equipment, and Intangibles

© 2017 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

219. A company purchased an asset on January 1, 2014, for $10,000. The asset was expected to have a ten-year life and a

$1,000 salvage value. The company uses the straight-line method of depreciation. On January 1, 2016, the company made

a major repair to the asset of $5,000, extending its life. The asset is expected to last ten years from January 1, 2016.

Calculate the amount of depreciation for 2016.

ANSWER:

Original cost, January 1, 2014

$10,000

Less: Accumulated depreciation (2 years at $900 per year)

(1,800)

Book value, January 1, 2016

$ 8,200

Plus: Major overhaul

5,000

Less: Residual value

(1,000)

Remaining depreciable amount

$12,200

Depreciation = Remaining Depreciable Amount/Remaining Life

Depreciation per Year = $12,200/10 years = $1,220

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-07 - LO: 08-07

KEYWORDS:

Bloom's: Analyzing

220. Assume that Rocket Company purchased an asset on January 1, 2014, for $62,400. The asset had an estimated life of

eight years and an estimated residual value of $8,000. The company used the straight-line method to depreciate the asset.

On July 1, 2016, the asset was sold for $52,000.

Required:

1. Make the journal entry to record depreciation for 2016. Record all transactions necessary for the sale of the asset.

2. How should the gain or loss on the sale of the asset be presented on the income statement?

ANSWER:

1.

July 1

Depreciation Expense

3,400

Accumulated Depreciation—Asset

3,400

To record depreciation of asset to July 1 for 1/2 year 2016.

($62,400 – $8,000)/8 years = $6,800 per year.

221. Assume that Halpern Company purchased an asset on January 1, 2015, for $122,800. The asset had an estimated life

of six years and an estimated residual value of $2,200. The company used the straight-line method to depreciate the asset.

Assume that Halpern Company sold the asset on July 1, 2016, and received $96,000 cash and a note for an additional

$22,000.

Required:

1. Make the journal entry to record depreciation for 2016. Record all transactions necessary for the sale of the asset.

2. How should the gain or loss on the sale of the asset be presented on the income statement?

ANSWER:

1.

July 1

Depreciation Expense

10,050

Accumulated Depreciation—Asset

10,050

To record depreciation to July 1 for 1/2 year

in 2016

($122,800 – $2,200)/6 years = $20,100 per

Chapter 8: Operating Assets: Property, Plant and Equipment, and Intangibles

© 2017 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

222. Below are several accounts and balances from the 2016 financial statements for Torrent, Inc. Prepare the intangible

asset section of the company’s balance sheet, as well as a partial income statement in the space provided below using the

accounts provided.

Amortization expense

$ 32,000

Amortization since inception

89,000

Loss on sale of copyright

12,000

Copyright

120,000

Patents

60,000

Land

80,000

Goodwill

140,000

Research and development costs

160,000

BALANCE SHEET

INCOME STATEMENT

ANSWER:

BALANCE SHEET

Intangible Assets:

Copyright

$120,000

Patents

60,000

Goodwill

140,000

Total Intangible assets

$320,000

Less: Accumulated amortization

(89,000)

Total Intangible Assets

$231,000

INCOME STATEMENT

Operating Expenses:

Amortization expense

$ 32,000

Research and development costs

160,000

Other Income and Expenses

Loss on sale of copyright

$(12,000)

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-09 - LO: 08-09

FACC.PONO.13.08-10 - LO: 08-10

KEYWORDS:

Bloom's: Analyzing

© 2017 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

223. Given below are costs incurred by Bunker Company during 2016 and 2017. Bunker follows the policy of decreasing

the intangible asset account directly as amortized.

Research was conducted to discover a new product and costs of $200,000 in 2016 and $80,000 in 2017 were incurred.

After several months, a product was created and a patent secured for a cost of $150,000, effective as of July 1, 2017. The

company expects to have increased revenues of $500,000 over the next several years. The patent is expected to be useful

for the next 10 years.

A.

Prepare a partial income statement for the year ended December 31, 2017.

B.

How should the $80,000 cost incurred in 2017 be reported on the financial statements?

ANSWER:

A. Income Statement:

Operating expenses:

Research and development costs

$80,000

Patent amortization expense

7,500

([$150,000 cost/10 years] × 1/2 year)

B. The costs to discover the new product are considered research and development costs

which are reported on the income statement as an expense. These costs should be expensed

when incurred since future benefits are not predictable.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-09 - LO: 08-09

FACC.PONO.13.08-10 - LO: 08-10

KEYWORDS:

Bloom's: Analyzing

224. Wang Fitness Co. purchased a patent at the beginning of 2016 for $120,000. Economic benefits were expected for

only 12 years, but the patent's legal life is 17 years. Also during 2016, the company incurred research and development

costs of $50,000.

A. Determine the following amounts:

1.

Research and development expense for 2016

2.

Patent amortization expense for 2016

B. Prepare the intangible assets section of the balance sheet at December 31, 2016.

ANSWER:

A. Expense amounts for 2016

Research and development expense

$ 50,000

Patent amortization expense

10,000

B. Intangible Assets section of balance sheet at December 31, 2016

Patents

$110,000

[$120,000 – ($10,000 × 1)]

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-09 - LO: 08-09

© 2017 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

225. Glitch Company incurred the following costs during 2016 and 2017:

a. Research and development costing $40,000 was conducted on a new product to sell in future years. A product was

successfully developed, and a patent for it was granted during 2016. Glitch is unsure of the period benefited by the

research, but believes the product will result in increased sales over the next five years.

b. Legal costs and application fees of $25,000 for the 20-year patent were incurred on January 1, 2016.

c. A patent infringement suit was successfully defended at a cost of $24,000. Assume that all costs were incurred on

January 1, 2017.

Required:

Determine how the costs in (a) and (b) should be presented on Glitch’s financial statements as of December 31, 2016.

Also determine the amount of amortization of intangible assets that Glitch should record in 2016 and 2017.

ANSWER:

a. All research and development costs should be treated as an expense. The 2016 income

statement should reflect an expense of $40,000.

b. Patent costs should be treated as an asset. The 2016 balance sheet should reflect a Patent

account of $25,000 – ($25,000/5 years) = $20,000.

c. The $24,000 cost of defending the patent should be added to the Patent account and

reflected in the 2017 balance sheet.

2016 amortization

= $25,000/5 years = $5,000

2017 amortization

= $25,000 – $5,000 amortization from 2016 + $24,000

infringement

= $44,000

$44,000/4 years

= $11,000 amortization for 2017

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-09 - LO: 08-09

FACC.PONO.13.08-10 - LO: 08-10

KEYWORDS:

Bloom's: Analyzing

226. Several years ago, Laurel Company purchased a patent and has since been amortizing it on a straight-line basis over

its estimated useful life. The company's comparative balance sheets contain the following items:

(In thousands)

December 31, 2017

December 31, 2016

Patent, less accumulated amortization of

$70,000 (2017) and $52,500 (2016)

$280,000

$297,500

A.

How much amortization expense was recorded during 2017?

B.

How is the amortization expense reported on the company's statement of cash flows?

C.

How much was the original cost of the patent?

D.

How many years has the patent been amortized?

ANSWER:

A.

$70,000 – $52,500 = $17,500

B.

If the company uses the indirect method of reporting operating activities on the

statement of cash flows, the amount of amortization will be added in the operating

activities category. This is done because the expense was deducted in determining net

income, although no cash was used.

C.

$280,000 + $70,000 = $350,000

D.

$70,000/$17,500 per year = 4.0 years

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-09 - LO: 08-09

FACC.PONO.13.08-10 - LO: 08-10

KEYWORDS:

Bloom's: Analyzing

227. Racer Company acquired patent rights on January 1, 2013 for $1,080,000. The patent has a useful life equal to its

legal life of 15 years. On January 2, 2016, Racer successfully defended the patent in a lawsuit at a cost of $78,000.

Required:

(1)

Determine the patent amortization expense for the current year ended December 31, 2016.

(2)

Journalize the adjusting entry to recognize the amortization.

ANSWER:

(1)

($1,080,000/15) + ($78,000/12) = $78,500 total patent

expense

(2)

Amortization Expense—Patents

78,500

Patents

78,500

Amortized patent rights ($72,000 + $6,500).

Balance Sheet

Income Statement

Assets

=

Liabilities

+

Stockholders’

Equity

Revenues

–

Expenses

=

Net

Income

Amortized

Patent

Rights (78,500)

Amortization

Expense-

Patents

78,500

(78,500)

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-10 - LO: 08-10

KEYWORDS:

Bloom's: Analyzing

228. For each of the following intangible assets, indicate the amount of amortization expense that should be recorded for

the year 2016 and the amount of accumulated amortization on the balance sheet as of December 31, 2016.

Trademark

Patent

Copyright

Cost

$66,000

$75,000

$96,000

Date of Purchase

1/1/09

1/1/11

1/1/14

Useful life

Indefinite

10 years

20 years

Legal life

Undefined

20 years

50 years

Method

Straight-line

Straight-line

Straight-line

ANSWER:

Trademark is not amortized because it has an indefinite life.

© 2017 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

229. Fill in the table shown below indicating the period of time over which each intangible asset should be amortized, and

indicate the amount of amortization expense that should be reported for 2016.

Goodwill

Trademark

Cost

$80,000

$55,000

Date of purchase

June 30, 2016

January 1, 2016

Legal life

Forever

20 years

Useful life

60 years

10 years

2016 Amortization expense

ANSWER:

Goodwill = $ -0-

Trademark = $55,000/10 years = $5,500

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.08-10 - LO: 08-10

KEYWORDS:

Bloom's: Analyzing

Chapter 8: Operating Assets: Property, Plant and Equipment, and Intangibles

© 2017 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

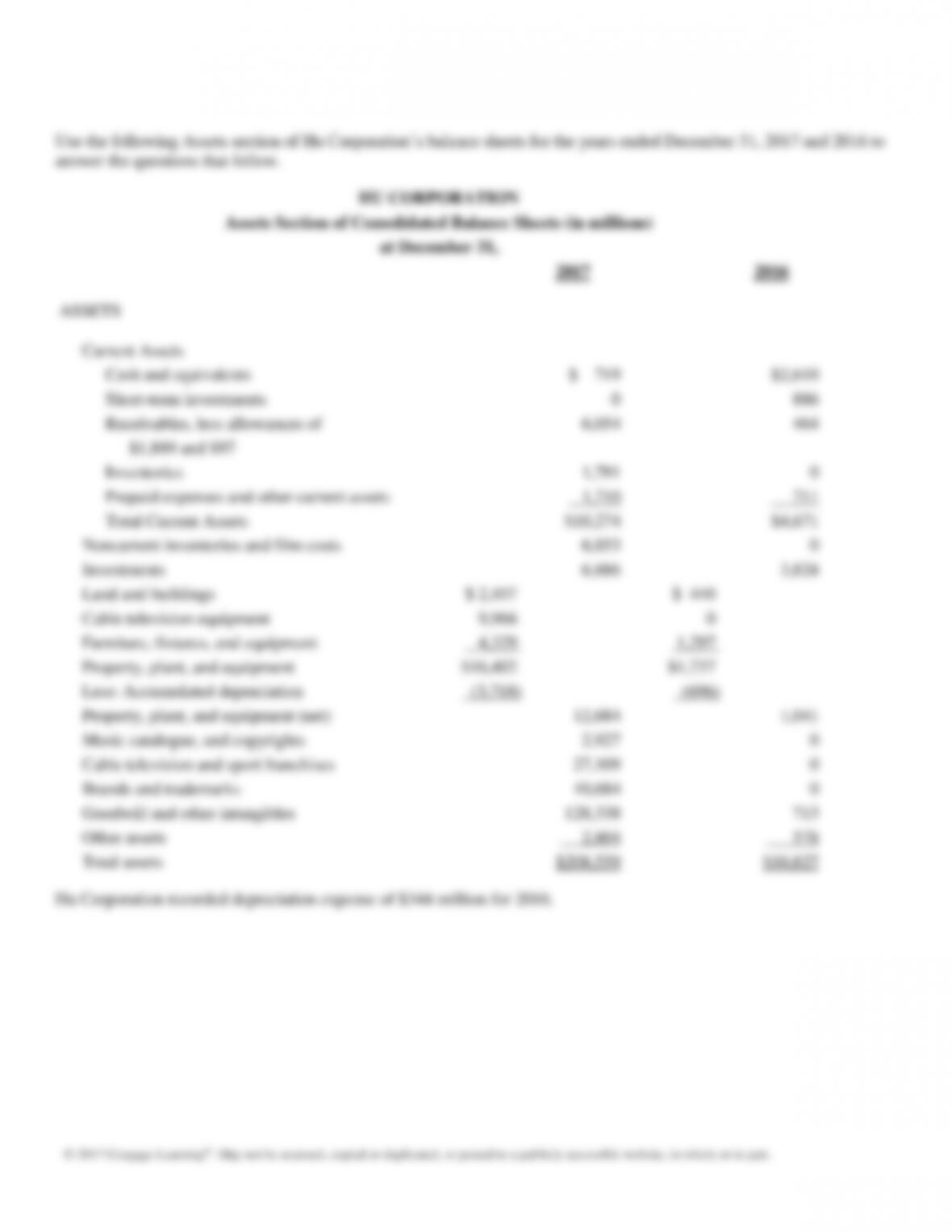

Hu Corporation

Use the following Assets section of Hu Corporation’s balance sheets for the years ended December 31, 2017 and 2016 to

answer the questions that follow.

HU CORPORATION

Assets Section of Consolidated Balance Sheets (in millions)

at December 31,

2017

2016

ASSETS

Current Assets

Cash and equivalents

$ 719

$2,610

Short-term investments

0

886

Receivables, less allowances of

6,054

464