8-1

Chapter 8

Answers to Review Problems

Finance For Executives – 4th Edition

1. Pondering an investment offer.

The offer is not firidiculous.” The problem is that the cash flows in the deal have been incorrectly

specified. The $15,000 investment promises a $17,000 payoff in one year. The filess than 4 percent”

return calculation is presumably based on a payoff of $17,000 less 12 percent interest on $12,000 or a net

2. The effect of inflation on the investment decision.

The financial manager is correct. Why? The accountant is arguing that the projected cash flows (the

numerator in the equation) are nominal amounts. That is, they assume some rate of inflation. It is

impossible to predict inflation rates very far into the future, so taking the most recent government figures

3. Changing machines in a world without taxes.

For all questions from a. to d., the first issue is the estimation of the project’s economic or useful life. The

existing machine can last another 10 or more years. However, the new one, which will perform exactly

the same operations, has an economic life of only 5 years, which means that it will be obsolete within 5

8-2

a.

By changing machines, the cash position of Clampton will immediately decrease by $110,000, the

difference between the purchase price of the new machine ($110,000) and the resale price ($0) of the

existing one. And then, each year for the following 5 years, the cash flow of Clampton will increase by

$30,000.

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Cash flow from project

-$110,000

$30,000

$30,000

$30,000

$30,000

$30,000

4

According to the net present value rule, the machine should be changed. Note that the depreciation

expenses related to the new machine have no effect on the decision, although it will negatively affect its

net profit in the next 5 years. This is totally rational since depreciation expenses are not cash expenses.

b.

c.

Using a spreadsheet

5

6

7

8

9

10

8-3

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Cash flow from project

-$150,000

$40,000

$40,000

$40,000

$40,000

$40,000

10

1

2

3

4

5

11

12

Discounted cash inflows

$36,364

$33,058

$30,053

$27,321

$24,837

13

14

Accumulated discounted

cash flows

$36,364

$69,421

$99,474

$126,795

$151,631

15

16

17

18

19

20

21

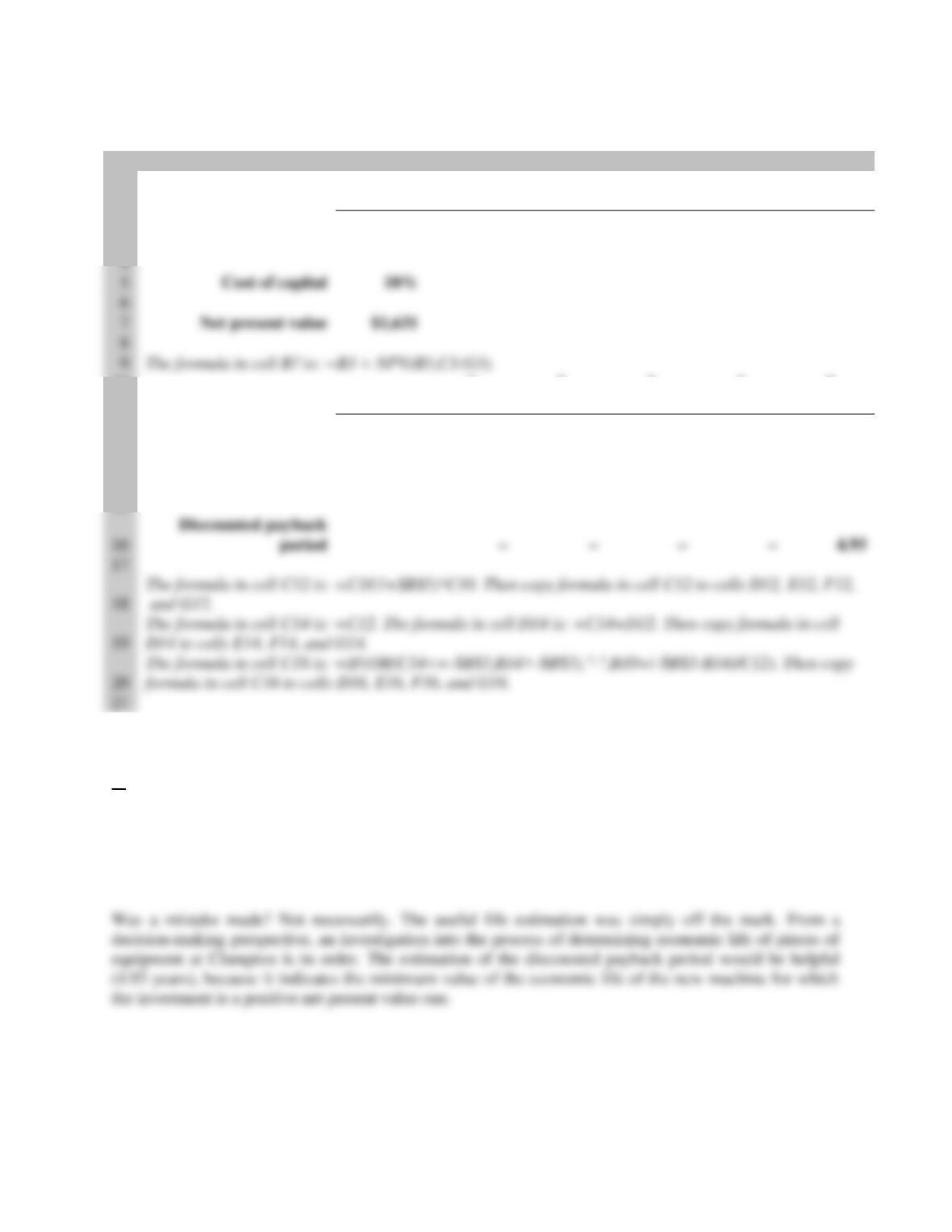

According to the net present value rule, machine B should be purchased.

d.

If a mistake has been made, it is in the estimation of the economic life of Machine A. The decision taken

two years ago was taken with the assumption that its economic life was 5 years, when actually it was 2

years. Had the net present value analysis been done for 2 years instead of 5 years, Machine A would not

have been a positive net present value proposition.

8-4

4. Changing machines in a world with taxes.

a.

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Purchase of new machine

-$110,000

Savings before depreciation

8

Change in Clampton’s

operating profit after tax

$4,800

$4,800

$4,800

$4,800

$4,800

9

Cash flow from project

-$110,000

$26,800

$26,800

$26,800

$26,800

$26,800

10

11

Cost of capital

8%

12

13

14

15

16

17

18

19

20

21

According to the net present value rule, the machine should not be changed, contrary to the case when the

company is not taxed, because the net present value is negative (minus $2,995). Taxes have three effects

on the estimation of the net present value:

• They decrease the cash flow after tax and before depreciation.

• They increase the cash flow by the amount of the depreciation tax shield (Tax rate × Depreciation

expenses).

5

depreciation allowances

6

operating profit

7

Tax rate

8-5

b.

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Purchase of new machine

-$110,000

4

Savings before depreciation and tax

$30,000

$30,000

$30,000

$30,000

$30,000

Increase in depreciation allowances

10

Change in Clampton’s operating

profit after tax

$9,600

$9,600

$9,600

$9,600

$9,600

11

Book value of old machine

$40,000

12

Tax credit from writing off old

machine

$16,000

13

Cash flow from project

-$94,000

$23,600

$23,600

$23,600

$23,600

$23,600

14

15

Cost of capital

8%

16

17

Net present value

$228

18

19

The values in rows 3, 4, 6, 9, 11, and 15 are data.

20

21

The formula in cell C7 is: =C5+C6. Then copy formula in cell C7 to cells D7, E7, F7, and G7.

22

The formula in cell C8 is: =C4-C7. Then copy formula in cell C8 to cells D8, E8, F8, and G8.

23

24

25

26

27

According to the net present value rule, the machine should be changed because the net present value is

positive, although nearly insignificantly positive ($228).

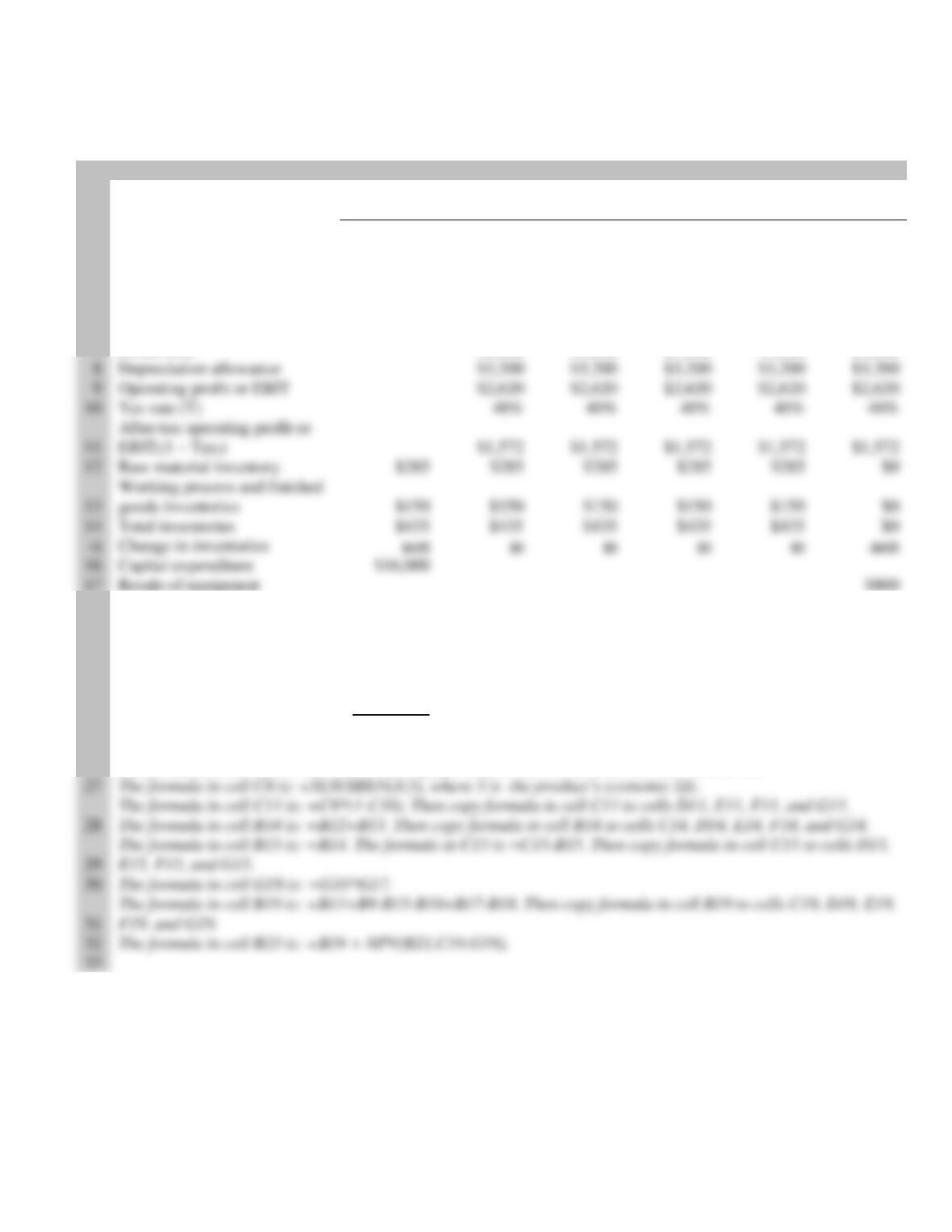

5

from new machine

7

allowances

$14,000

$14,000

$14,000

$14,000

$14,000

8

Change in Clampton’s operating

profit

$16,000

$16,000

$16,000

$16,000

$16,000

9

Tax rate

8-6

5. Investing in the production of toys.

a.

The cash flows (CFt) generated by the project can be estimated from equation (8.2):

CFt = EBITt(1 – Taxt) + Dept – WCRt – Capext

Using a calculator

$ thousands

Now

Year 1 to 4

Year 5

1. Revenues

$10,800

$10,800

2. Unit produced in thousands (3,000 per month)

36

36

3. Raw material cost per thousand units

$95

$95

4. Total material cost (line 2 × line 3)

$3,420

$3,420

5. Direct cost ($130,000 per month)

$1,560

$1,560

6. Depreciation expenses ($16 million/5)

$3,200

$3,200

7. EBIT (line 1 – line 4 – line 5 – line6)

$2,620

$2,620

8. Tax rate (Taxt)

9. EBITt(1 – Taxt) (line 7 (line 1 – line 8))

$0

$800

$4,772

$5,687

b.

The net present value (NPV) in thousand dollars of the project is:

8-7

Using a spreadsheet

A

B

C

D

E

F

G

1

in thousands

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Revenues

$10,800

$10,800

$10,800

$10,800

$10,800

4

Units produced

36

36

36

36

36

5

Raw material cost per

thousand units

$95

$95

$95

$95

$95

6

Total material cost

$3,420

$3,420

$3,420

$3,420

$3,420

7

Direct cost

$1,560

$1,560

$1,560

$1,560

$1,560

18

Tax on resale of equipment

$320

19

Total cash flow

-$16,435

$4,772

$4,772

$4,772

$4,772

$5,687

20

21

Cost of capital

12%

22

23

Net present value

$1,286.188

24

25

The values in rows 3, 4, 5, 7, 10, 12, 13, 16, 17, and 21 are data.

26

The formula in cell C6 is: =C4*C5. Then copy formula in cell C6 to cells D6, E6, F6, and G6.

27

The formula in cell C8 is: =SLN($B$16,0,5), where 5 is the product’s economic life.

The formula in cell C11 is: =C9*(1-C10). Then copy formula in cell C11 to cells D11, E11, F11, and G11.

28

The formula in cell B14 is: =B12+B13. Then copy formula in cell B14 to cells C14, D14, E14, F14, and G14.

29

E15, F15, and G15.

30

The formula in cell G18 is: =G10*G17.

31

32

The formula in cell B23 is: =B19 + NPV(B21,C19:G19).

33

8

Depreciation allowance

9

Operating profit or EBIT

$2,620

$2,620

$2,620

$2,620

$2,620

10

Tax rate (T)

11

$1,572

$1,572

$1,572

$1,572

$1,572

12

Raw material inventory

$0

13

Working process and finished

goods inventories

$0

14

Total inventories

$435

$435

$435

$435

Change in inventories

16

Capital expenditure

17

Resale of equipment

$800

8-8

6. The effect of accounts receivables, accounts payables, overhead, and financial costs on

the investment decision.

a.

The new product would increase both accounts receivable and accounts payable. Annual sales of $12

million spread evenly over the year would mean $32,877 per day ($12 million/365 days). If the collection

period on average were 50 days, this would mean an extra investment (an increase in the firm’s accounts

receivable) of $1,643,836 ($32,877 50). For simplicity, let us assume that this would take place at time

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Increase in firm’s accounts

receivable

$1,643,836

$0

$0

$0

$0

–

$1,643,836

4

Increase in firm’s accounts

payable

$394,521

$0

$0

$0

$0

-$394,521

5

6

7

9

10

11

12

14

15

Increase in firm’s

working capital

–

b.

The standard charge of one percent of revenues needs a careful look. While it is reasonable to expect

some impact on general overheads from the addition of a new product, an incremental cost amounting to

8-9

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Overhead charges increase

$120,000

$120,000

$120,000

$120,000

$120,000

c.

The financing charge of 10 percent levied against the book value of assets used in the project is a fired

herring.” We should not bring financing costs into the cash flows since they are already included in the

discount rate. To deduct them from the cash flows would result in double-counting.

7. The effect of depreciation for tax purposes.

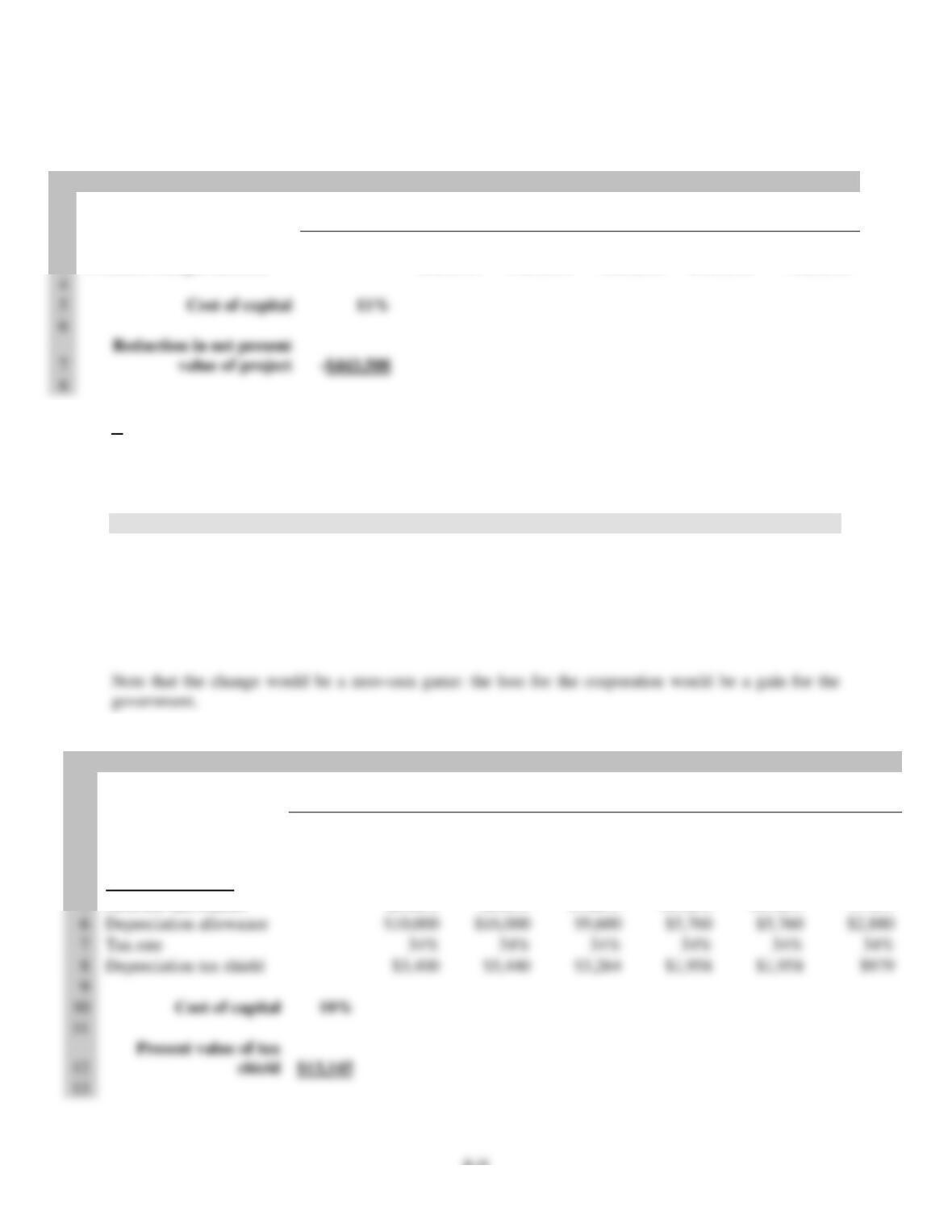

Using a spreadsheet

A move imposed by the tax authorities from MACRS to the straight-line method of depreciation will

systematically decrease the net present value of any investment project. In our case, the net present value

will decrease by $805 ($13,145 – $12,340) for an investment of $50,000.

A

B

C

D

E

F

G

H

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

Year-end

6

2

3

Cost of automobile

$50,000

4

I. Under MACRS

5

MACRS allowances

20.00%

32.00%

19.20%

11.52%

11.52%

5.76%

6

Depreciation allowance

7

Tax rate

7

-$443,508

8-10

14

II. Under straight-line system

15

Depreciation allowance

$8,333

$8,333

$8,333

$8,333

$8,333

$8,333

16

Depreciation tax shield

$2,833

$2,833

$2,833

$2,833

$2,833

$2,833

17

18

Present value of tax

shield

$12,340

19

20

The values in rows 3, 5, 7, and10 are data

8. The effect of cannibalization.

These three items must each be handled differently. The $500,000 market study is a sunk cost. It has

already been made and paid for. Whether the new project is taken or not, the cash flow has occurred.

Therefore, this sum should be left out of the analysis.

21

The formula in cell C6 is: =C5*$B$3. Then copy formula in cell C6 to cells D6, E6, F6, G6, and H6.

22

The formula in cell C8 is: =C6*C7. Then copy formula in cell C8 to cells D8, E8, F8, G8, and H8.

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

3

Loss of rental revenue

$100,000

$100,000

$100,000

$100,000

$100,000

4

5

Cost of capital

11%

6

7

8

9

Loss to cannibalization

10

11

12

9. Break-even analysis.

Using a spreadsheet

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

2

I. Base case

3

Initial investment

–

$1,000,000

4

Number of snowmobiles sold

100

100

100

100

100

5

Unit sale price

6

Revenues

$1,000,000

$1,000,000

$1,000,000

$1,000,000

7

Variable costs per unit

8

Total variable costs

$500,000

$500,000

$500,000

$500,000

$500,000

9

Total fixed costs

$125,000

$125,000

$125,000

$125,000

$125,000

10

Depreciation expense

$200,000

$200,000

$200,000

$200,000

$200,000

11

Operating profit (EBIT)

$175,000

$175,000

$175,000

$175,000

$175,000

12

Tax rate

40%

40%

40%

40%

40%

13

Operating profit after tax

$105,000

$105,000

$105,000

$105,000

$105,000

14

Cash flow from the project

–

$1,000,000

$305,000

$305,000

$305,000

$305,000

$305,000

15

16

Cost of capital

17

18

$156,190

19

20

21

8-12

22

The formula in cell C8 is: =C7*C4. Then copy formula in cell C8 to cells D8, E8, F8, and G8.

28

29

II. Break- even analysis

30

Number of snowmobiles

sold per year

50

60

70

80

90

100

31

Net present value

-$412,428

-$298,704

-$184,981

-$71,257

$42,466

$156,190

32

33

34

a.

The spreadsheet analysis indicates that the project should be undertaken for the expected sale of 100

snowmobiles per year since the net present value is positive under this assumption ($156,190).

b.

The graph shows that the break-even sales level, which is the number of snowmobiles to sell every year

Net present value

Number of units

23

24

25

26

27

8-13

so that

Cash flow = [Revenues – Variable costs – Fixed costs – Depreciation expenses] × (1 – Tax rate) +

Depreciation expenses

Let Q be the number of snowmobiles sold per year. Then:

Unit sales price = $10

Unit variable cost = $5

Tax rate = 40 percent

Fixed costs = $125

Depreciation expenses = $200

Replacing the variables in the above equation by their values, we get:

Q = [$1,000 – PV($5)]/PV($3)

The present value of an annuity of $5 per year at 10 percent is $18.95, that of an annuity of $3 is $11.37,

so that:

Q = [$1,000 – $18.95]/$11.37 = 87

10. Bid price.

The cash flows of the project are:

A

B

C

D

E

F

G

1

Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

3

capital requirement

4

After-tax cash flow

5

The value of the cash flow, CF, for which the project’s net present value is zero, must verify the following

equation:

55432 )10.1(

000,30$

)10.1(

CF

)10.1(

CF

)10.1(

CF

)10.1(

CF

)10.1(

CF

000,130$0 +

+

+

+

+

+

+

+

+

+

+

+−=

or

From equation 8.2:

CF = EBIT (1 – Tax) + Depreciation expenses

(Note there is no change in working capital requirement nor any new capital expenditure expected over

the five-year period.)

8-15

so that

$15,633 = Revenues – $80,000 – $20,000

Revenues = $80,000 + $20,000 + $15,633 = $115,633

Maintainit Inc. must submit a bid of no less than $115,633 per year for the project to have a positive net

present value.