10) An efficient portfolio is one that ________.

A) guarantees a predetermined rate of return

B) maximizes return for a given level of risk

C) consists of a single asset, which gives maximum return

D) maximizes return at all risk levels

11) An investment advisor has recommended a $50,000 portfolio containing assets R, J, and K; $25,000

will be invested in asset R, with an expected annual return of 12 percent; $10,000 will be invested in asset

J, with an expected annual return of 18 percent; and $15,000 will be invested in asset K, with an expected

annual return of 8 percent. The expected annual return of this portfolio is ________.

A) 12.67%

B) 12.00%

C) 10.00%

D) 11.78%

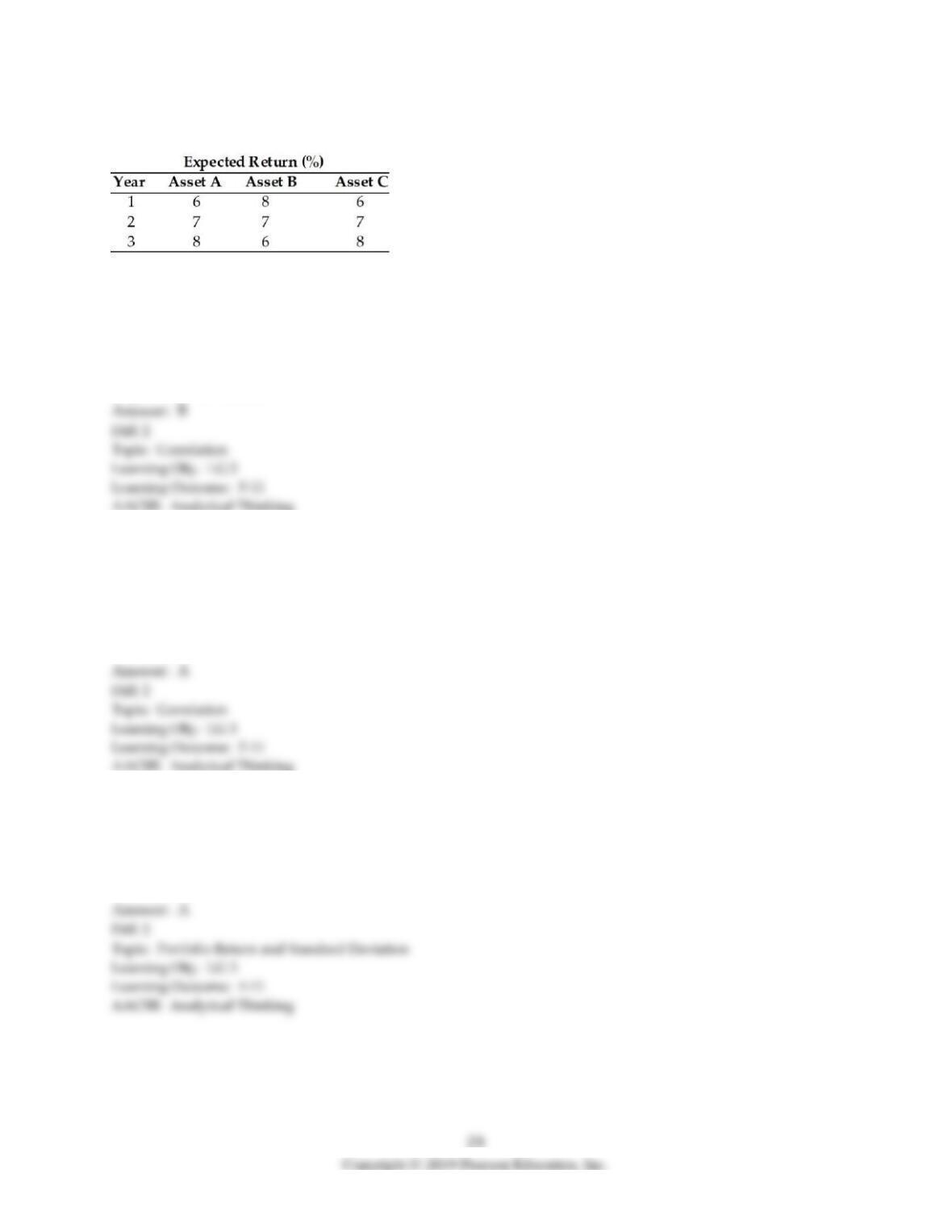

12) Given the returns of two stocks J and K in the table below over the next 4 years. Find the expected

return and standard deviation of holding a portfolio of 40% of stock J and 60% in stock K over the next 4

years:

Stock J

Stock K

2020

10%

9%

2021

12%

8%

2022

13%

10%

2023

15%

11%

A) 10.7% and 1.34%

B) 10.6% and 1.79%

C) 10.6% and 1.16%

D) 14.3% and 2.02%

13) ________ is a statistical measure of the relationship between any two series of numbers.

A) Coefficient of variation

B) Standard deviation

C) Correlation

D) Probability

14) Perfectly ________ correlated series move exactly together and have a correlation coefficient of

________, while perfectly ________ correlated series move exactly in opposite directions and have a

correlation coefficient of ________.

A) negatively; -1; positively; +1

B) negatively; +1; positively; -1

C) positively; -1; negatively; +1

D) positively; +1; negatively; –1

15) Combining negatively correlated assets having the same expected return results in a portfolio with

________ level of expected return and ________ level of risk.

A) a higher; a lower

B) the same; a higher

C) the same; a lower

D) a lower; a higher

Table 8.1

16) The correlation of returns between Asset A and Asset B can be characterized as ________. (See Table

8.1)

A) perfectly positively correlated

B) perfectly negatively correlated

C) uncorrelated

D) partially correlated

17) If you were to create a portfolio designed to reduce risk by investing equal proportions in each of two

different assets, which portfolio would you recommend? (See Table 8.1)

A) Assets A and B

B) Assets A and C

C) none of the available combinations

D) cannot be determined

18) The portfolio with a standard deviation of zero ________. (See Table 8.1)

A) is comprised of Assets A and B

B) is comprised of Assets A and C

C) is not possible

D) cannot be determined

19) Akai has a portfolio of three assets. Find the expected rate of return for the portfolio assuming he

invests 50 percent of its money in asset A with 10 percent rate of return, 30 percent in asset B with a rate

of return of 20 percent, and the rest in asset C with 30 percent rate of return.

20) Combining assets that are not perfectly positively correlated with each other can reduce the overall

variability of returns.

21) Even if assets are not negatively correlated, the lower the correlation between them, the lower the

resulting risk of the portfolio.

22) In general, the lower the correlation between asset returns, the greater the benefit of diversification.

23) A portfolio of two negatively correlated assets may have less risk than either of the individual assets.

24) Under no circumstance would adding an asset to a portfolio increase the risk of the portfolio above

the risk of the most risky asset in the portfolio.

25) A portfolio that combines two assets having perfectly positively correlated returns cannot reduce the

portfolio’s overall risk below the risk of the least risky asset.

26) A portfolio combining two assets with less than perfectly positive correlation can reduce total risk to a

level below that of either of the components.

27) Uncorrelated assets have correlation coefficient close to zero.

28) Combining uncorrelated assets can reduce risk—not as effectively as combining negatively correlated

assets, but more effectively than combining positively correlated assets.

29) A firm has high sales when the economy is expanding and low sales during a recession. This firm’s

overall risk will be higher if it invests in another product which is counter cyclical.

30) A portfolio combining two assets whose returns are less than perfectly positive correlated can

increase total risk to a level above that of either of the components.

31) The risk of a portfolio containing international stocks generally contains less nondiversifiable risk

than one that contains only domestic stocks.

32) The inclusion of assets from countries with business cycles that are not highly correlated with the U.S.

business cycle reduces the portfolio’s responsiveness to market movements.

33) Returns (relative to risk) from internationally diversified portfolios tend to be superior to those

yielded by purely domestic ones.

34) When the U.S. currency gains in value, the dollar value of a foreign-currency-denominated portfolio

of assets decline.

35) The risk of a portfolio containing international stocks generally does not contain less nondiversifiable

risk than one that contains only domestic stocks.

36) Combining two less than perfectly positively correlated assets to reduce risk is known as ________.

A) diversification

B) valuation

C) securitization

D) risk aversion

37) The lower the correlation between asset returns, the ________.

A) lesser the potential diversification of risk

B) greater the potential diversification of risk

C) lower the potential profit

D) lesser the assets have to be monitored

38) If two assets having perfectly negatively correlated returns are combined in a portfolio, then some

combination of those two assets will ________.

A) have more risk than either asset does on its own

B) have no risk at all

C) have a higher return than either asset does on its own

D) have a lower return than either asset does on its own

39) Asset 1 has an expected return of 10% and a standard deviation of 20%. Asset 2 has an expected

return of 15% and a standard deviation of 30%. The correlation between the two assets is 1.0. Portfolios

of these two assets will have an expected return ________.

A) between 0% and 15%

B) between 10% and 15%

C) below 10%

D) above 15%

40) Asset 1 has an expected return of 10% and a standard deviation of 20%. Asset 2 has an expected

return of 15% and a standard deviation of 30%. The correlation between the two assets is –1.0. Portfolios

of these two assets will have a standard deviation ________.

A) between 0% and 20%

B) between 0% and 30%

C) below 10%

D) between 20% and 30%

41) Asset 1 has an expected return of 10% and a standard deviation of 20%. Asset 2 has an expected

return of 15% and a standard deviation of 30%. The correlation between the two assets is –1.0. Portfolios

of these two assets will have an expected return ________.

A) between 0% and 15%

B) between 10% and 15%

C) below 10%

D) above 15%

42) Asset 1 has an expected return of 10% and a standard deviation of 20%. Asset 2 has an expected

return of 15% and a standard deviation of 30%. The correlation between the two assets is less than 1.0.

You form a portfolio by investing half of your money in asset 1 and half in asset 2. Which of the

following best describes the expected return and standard deviation of your portfolio?

A) The expected return is 12.5% and the standard deviation is less than 25%.

B) The expected return is between 10% and 15% and the standard deviation is greater than 30%.

C) The expected return is 12.5% and the standard deviation is 25%.

D) The expected return is 12.5% and the standard deviation is greater than 25%.

43) Combining two assets having perfectly positively correlated returns will result in the creation of a

portfolio with an overall risk that ________.

A) remains unchanged

B) decreases to a level below that of either asset

C) increases to a level above that of either asset

D) lies between the asset with the higher risk and the asset with the lower risk

8.4 Risk and return: The Capital Asset Pricing Model (CAPM)

1) The difference between the return on the market portfolio of assets and the risk-free rate of return

represents the premium the investor must receive for taking the average amount of risk associated with

holding the market portfolio of assets.

2) Total risk is the sum of a security’s nondiversifiable and diversifiable risk.

3) Total risk is attributable to firm-specific events, such as strikes, lawsuits, regulatory actions, or the loss

of a key account.

4) As any investor can create a portfolio of assets that will eliminate all, or virtually all, nondiversifiable

risk, the only relevant risk is diversifiable risk.

5) Diversifiable risk is the relevant portion of risk attributable to market factors that affect all firms.

6) Diversified investors should be concerned solely with nondiversifiable risk because they can easily

create a portfolio of assets that will eliminate all, or virtually all, diversifiable risk.

7) Nondiversifiable risk reflects the contribution of an asset to the risk, or standard deviation, of the

portfolio.

8) Systematic risk is that portion of an asset’s risk that is attributable to firm-specific, random causes.

9) Unsystematic risk can be eliminated through diversification.

10) Unsystematic risk is the relevant portion of an asset’s risk attributable to market factors that affect all

firms.

11) The required return on an asset is an increasing function of its nondiversifiable risk.

12) The empirical measurement of beta can be approached by using least-squares regression analysis to

find the regression coefficient (bj) in the equation for the slope of the “characteristic line.”

13) Investors should recognize that betas are calculated using historical data and that past performance

relative to the market average may not accurately predict future performance.

14) The beta coefficient is an index that measures the degree of movement of an asset’s return in response

to a change in the market return.

15) The beta coefficient is an index of the degree of movement of an asset’s return in response to a change

in the risk-free asset.

16) Systematic risk is also referred to as ________.

A) business specific risk

B) internal risk

C) nondiversifiable risk

D) maturity risk

17) Risk that affects all firms is called ________.

A) maturity risk

B) unsystematic risk

C) nondiversifiable risk

D) reinvestment risk

18) The portion of an asset’s risk that is attributable to firm-specific, random causes is called ________.

A) unsystematic risk

B) nondiversifiable risk

C) market risk

D) political risk

19) The relevant portion of an asset’s risk, attributable to market factors that affect all firms, is called

________.

A) credit risk

B) diversifiable risk

C) systematic risk

D) maturity risk

20) ________ risk represents the portion of an asset’s risk that can be eliminated by combining assets with

less than perfect positive correlation.

A) Diversifiable

B) Market

C) Systematic

D) Economic

21) Unsystematic risk ________.

A) does not change

B) can be eliminated through diversification

C) cannot be estimated

D) affects all firms in a market

22) Strikes, lawsuits, regulatory actions, or the loss of a key account are all examples of ________.

A) diversifiable risk

B) market risk

C) economic risk

D) systematic risk

23) War, inflation, and the condition of the foreign markets are all examples of ________.

A) business specific risk

B) nondiversifiable risk

C) internal risk

D) unsystematic risk

24) A beta coefficient of +1 represents an asset that ________.

A) has a higher expected return than the market portfolio

B) has the same expected return as the market portfolio

C) has a lower expected return than the market portfolio

D) is unaffected by market movement

25) A beta coefficient of –1 represents an asset that ________.

A) is more responsive than the market portfolio

B) has the same response as the market portfolio but in opposite direction

C) is less responsive than the market portfolio

D) is unaffected by market movement

26) The purpose of adding an asset with a negative or low positive beta to a portfolio is to ________.

A) reduce profit

B) reduce risk

C) increase profit

D) increase risk

27) The beta associated with a risk-free asset ________.

A) is greater than 1

B) is less than 1

C) is equal to 0

D) is between 0 and 1

28) A beta coefficient of 0 represents an asset that ________.

A) has an expected return greater than the market portfolio

B) has the same expected return as the market portfolio

C) has returns that do not fluctuate at all

D) has an expected return equal to the risk-free rate

29) An investment banker has recommended a $100,000 portfolio containing assets B, D, and F. $20,000

will be invested in asset B, with a beta of 1.5; $50,000 will be invested in asset D, with a beta of 2.0; and

$30,000 will be invested in asset F, with a beta of 0.5. The beta of the portfolio is ________.

A) 1.25

B) 1.33

C) 1.45

D) 1.85

30) The higher an asset’s beta, ________.

A) the more responsive it is to changing market returns

B) the less responsive it is to changing market returns

C) the higher the expected return will be in a down market

D) the lower the expected return will be in an up market

31) An increase in nondiversifiable risk would ________.

A) cause an increase in the beta and would lower the required return

B) have no effect on the beta and would, therefore, cause no change in the required return

C) cause an increase in the beta and would increase the required return

D) cause a decrease in the beta and would, therefore, lower the required rate of return

32) An increase in the Treasury Bill rate ________.

A) has no effect on the required rate of return of a common stock

B) increases the required rate of return of a common stock

C) doubles the required rate of return of a common stock

D) increases the beta of a common stock

33) The beta of a portfolio ________.

A) is the sum of the betas of all assets in the portfolio

B) is the product of the betas of the individual assets in the portfolio

C) is the median of the range of beta of the portfolio

D) is the weighted average of the betas of the individual assets in the portfolio

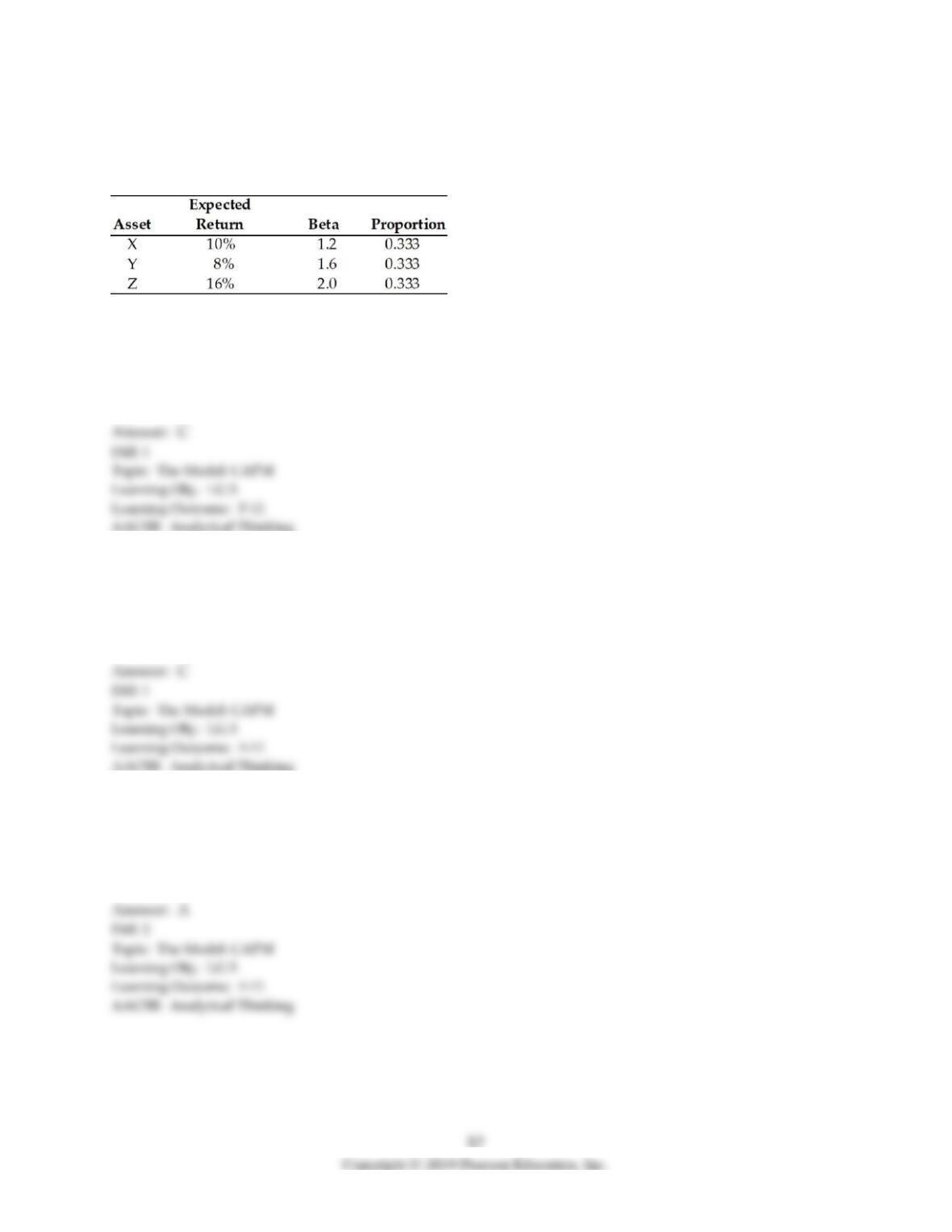

Table 8.2

You are going to invest $20,000 in a portfolio consisting of assets X, Y, and Z, as follows:

34) Given the information in Table 8.2, what is the expected return of this portfolio?

A) 11.40%

B) 10.00%

C) 11.33%

D) 11.70%

35) The beta of the portfolio in Table 8.2, containing assets X, Y, and Z is ________.

A) 1.5

B) 2.4

C) 1.6

D) 2.0

36) The beta of the portfolio in Table 8.2 indicates this portfolio ________.

A) has more risk than the market

B) has less risk than the market

C) has an unrelated amount of risk compared to the market

D) has the same risk as the market

37) As randomly selected securities are combined to create a portfolio, the ________ risk of the portfolio

decreases. The portion of the risk eliminated is ________ risk, while that remaining is ________ risk.

A) diversifiable; nondiversifiable; total

B) relevant; irrelevant; total

C) total; diversifiable; nondiversifiable

D) total; nondiversifiable; diversifiable

38) Nicole holds three stocks in her portfolio: A, B, and C. The portfolio beta is 1.40. Stock A comprises 15

percent of the dollar value of her holdings and has a beta of 1.0. If Nicole sells all of her investment in A

and invests the proceeds in the risk-free asset, her new portfolio beta will be ________.

A) 0.60

B) 0.88

C) 1.00

D) 1.25

39) If you expect the market to increase which of the following portfolios should you purchase?

A) a portfolio with a beta of 1.9

B) a portfolio with a beta of 1.0

C) a portfolio with a beta of 0

D) a portfolio with a beta of -0.5