7-1

Chapter 7

Answers to Review Problems

Finance For Executives – 4th Edition

1. Investment criteria.

a.

Impact on earnings per share (EPS) is an accounting measure of performance. Its main drawbacks

are that it ignores capital investment required for the project, penalizes projects whose earnings

are not immediately realized, and is subject to accounting manipulation. Yet there is a strong

b.

Global Chemicals uses all of these measures, no doubt, because the various managers (and also

board members for large project decisions) want them. Some of those taking part in the

investment decision process are more comfortable with certain measures than others. If the

7-2

2. Relationship between investment criteria.

The information given tells:

• Nothing about the discounted payback period

3. Net present value and payback period.

If the payback period is less than the economic life of the project, its net present value can be

either positive or negative. This is because the relevant cash flows in the computation of the

payback period are actual cash flows while those in the computation of the net present value are

discounted cash flows. The only certain case is the trivial case when the cost of capital of the

project is zero. In that case, the project’s net present value is, by definition, equal to zero at its

payback period. Since it lasts longer, its net present value is positive.

4. The internal rate of return of mutually exclusive projects.

a.

The intersection of Project A and Project B’s NPV lines represents the discount rate which

produces the same NPV for the two projects. Assuming the risk of each project is the same, and

the firm’s cost of capital is the discount rate at the intersection point, one should be indifferent

between the two projects.

d.

The choice depends on the cost of capital. When the cost of capital is lower than the break-even

rate (the point where the project NPV lines intersect), Project A is better, and Project B is better

when the cost of capital is higher than the break-even rate. Note that the choice between the two

projects cannot be made by comparing their internal rates of return because those rates have no

particular economic significance.

7-3

5. The case of multiple internal rate of return.

This project shows cash flows with alternating negative and positive signs. Though the project is

perhaps unrealistically simple, it is designed to illustrate a weakness of the internal rate of return

approach.

a. and b.

Using a spreadsheet

A B C D E F G

10 1 2

2 Cash flows -$200 $600 -$400

3

4 Cost of capital 0% 25% 50% 100%

5

There are two internal rates of return (IRR)—at 0 percent and 100 percent discount rates. Rates

between 0 percent and 100 percent produce positive net present values (NPV). Rates below 0

c.

The project should be accepted if its net present value is positive. This will be the case if the cost

of capital is above 0 percent and less than 100 percent.

7-4

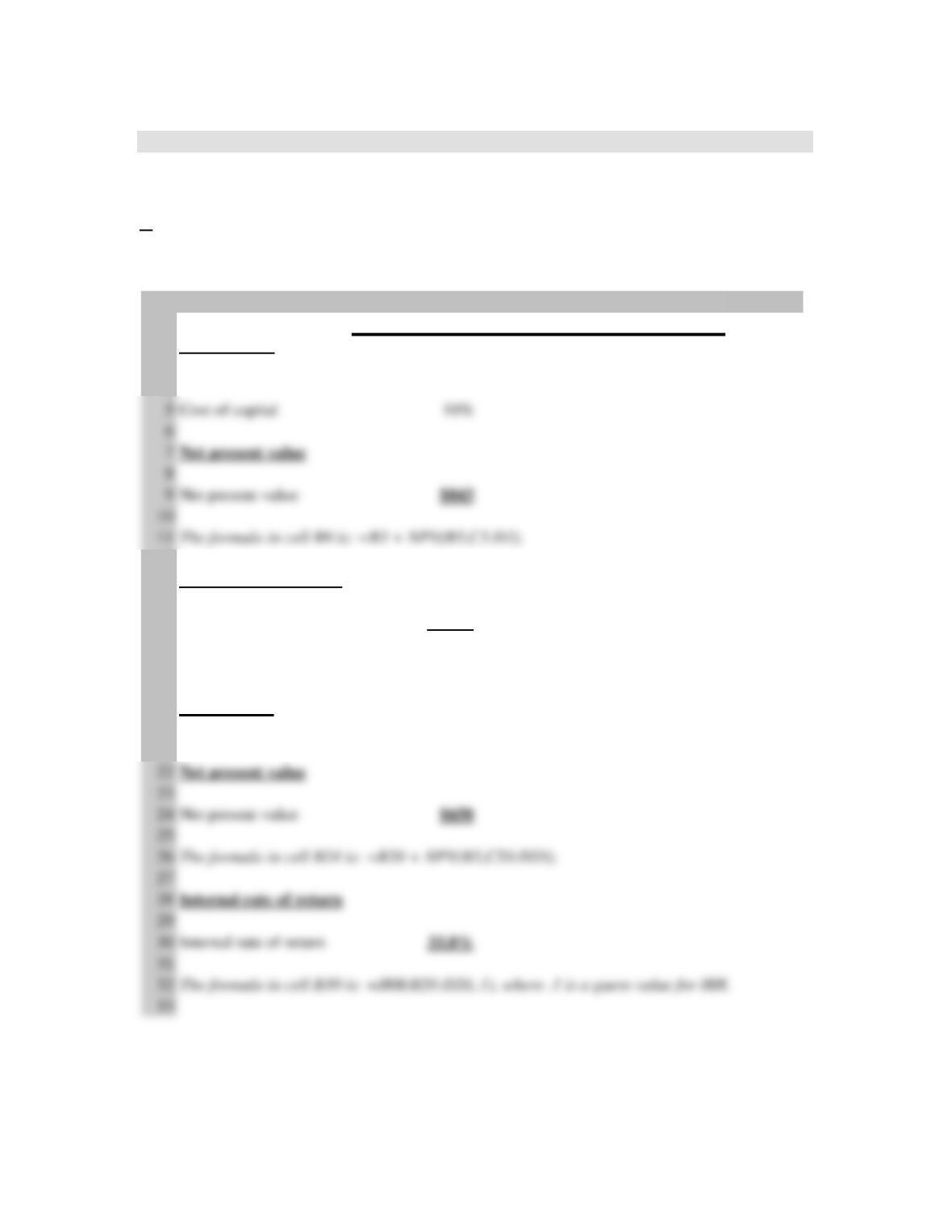

6. The net present value rule versus the internal rate of return.

Note that this is an “either or” type of problem and that the two projects are of different scale.

a.

Using a spreadsheet

A B C D

10 1 2

2PROJECT A

3 Cash flows -$12,000 $7,900 $6,850

4

12

13 Internal rate of return

14

15 Internal rate of return 15.3%

16

17 The formula in cell B15 is: =IRR(B3:D3,.1), where .1 is a guess value for IRR.

18

19 PROJECT B

20 Cash flows -$2,400 $2,500 $950

21

7-5

b.

Project B is a better choice based on internal rate of return, while project A is a better choice

based on net present value.

d.

The net present value rule is the least ambiguous assuming that the cost of capital rate has been

estimated correctly and that the firm does not have any capital constraints.

e.

The internal rate of return of the incremental cash flows (Project A’s minus Project B’s cash

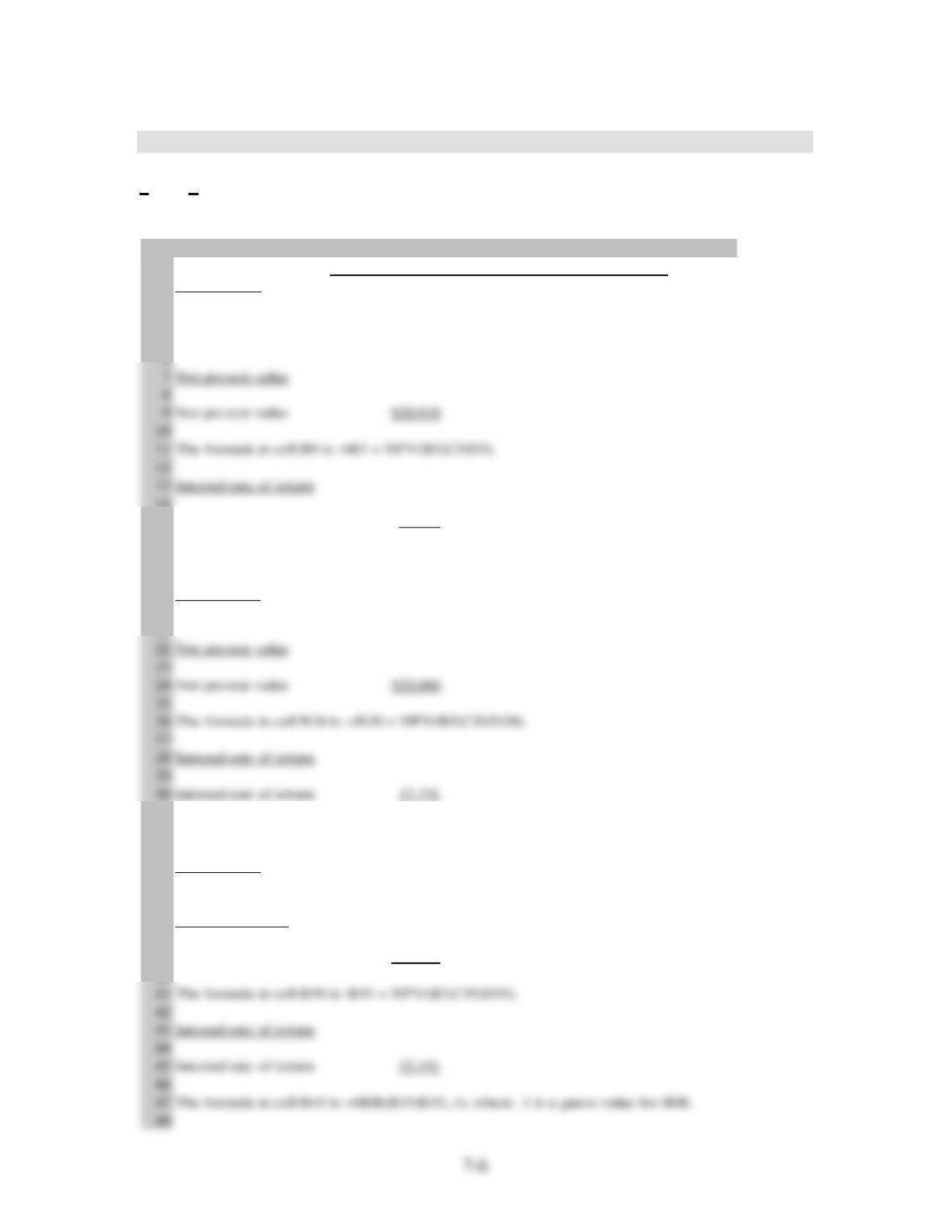

7. The internal rate of return rule and the net present value rule.

a and b

Using a spreadsheet

A B C D

10 1 2

2 PROJECT A

3 Cash flows -$150,000 $120,000 $80,000

4

5 Cost of capital 12%

14

15 Internal rate of return 23.3%

16

17 The formula in cell B15 is: =IRR(B3:D3,.1), where .1 is a guess value for IRR.

18

19 PROJECT B

20 Cash flows -$300,000 $200,000 $180,000

21

31

32 The formula in cell B30 is: =IRR(B20:D20,.1), where .1 is a guess value for IRR.

33

34 PROJECT C

35 Cash flows -$150,000 $110,000 $90,000

36

37 Net present value

38

39 Net present value $19,962

40

7-7

c.

The three projects should be accepted since their net present value is positive and their internal

rate of return is higher than the cost of capital (12 percent).

8. The net present value rule versus the profitability index rule.

Note that this is an “either or” type of problem and that the two projects are of different scale.

a.

7-8

A B C D E

1 0 1 2 3

2 PROJECT A

3 Cash flows -$16,000 $10,500 $9,100 $3,000

4

5 Cost of capital 10%

6

16

17 The formula in cell B15 is: =NPV(B5,C3:E3)/-B3.

18

19 PROJECT B

20 Cash flows -$3,200 $3,300 $1,260 $600

21

22 Net present value

23

24 Net present value $1,292

b.

Project B is a better choice based on the profitability index rule, while project A is a better choice

based on net present value.

9. The average accounting return

Using a spreadsheet

A B C D E F G

1 1 2 3 4 5

2 Initial cash outlay $2,000,000

3

7

8 The formula in cell B4 is: +SLN(B2,0,5), where 0 is the salvage value of the machine at the end of year 5 and 5 is the life of the machine.

9 The formula in cell C5 is: =B5-$B$4. Then copy formula in cell C5 to cells D5, E5, F5, and G5.

10 The formula in cell B6 is: =average(B5:G5).

11

12 Earnings after-tax – Year 1 $200,000

13 Growth rate after Year 1 10%

14 Earnings after-tax $200,000 $220,000 $242,000 $266,200 $292,820

According to the average accounting return rule, the machine should be bought since the average

accounting return is higher than the target return (24.4 percent versus 20 percent). However, you

should question the approach on the basis of the following considerations:

1. The approach ignores the time value of money. To account for it, the approach should

have used cash flows instead of earnings and discount those cash flows to present.

7-10

10. 10. Investment criteria.

a.

Using a spreadsheet

A B C D E F G

10 1 2 3 4 5

2 Cash flows -$18,000 $5,200 $5,200 $5,200 $5,200 $7,200

3

4 Payback period

5

6 Accumulated cash inflows $5,200 $10,400 $15,600 $20,800 $28,000

16

17 Discounted cash inflows $4,727 $4,298 $3,907 $3,552 $4,471

18 Accumulated discounted cash flows $4,727 $9,025 $12,932 $16,483 $20,954

19

20 Discounted payback period – – – – 4.34

28 Net present value $2,954

29

30 The formula in cell B28 is: =B2 + NPV(B15,C2:G2).

31

32 Internal rate of return

33

34 Internal rate of return 16.0%

35

7-11

b.

Considering the above measures, the project appears to be satisfactory since the net present value

is positive, the profitability index is greater than 1.0, the internal rate of return is above 10 percent

(assuming that 10 percent is the cost of capital), and the payback periods indicate the investment

outlay will be recovered during the life of the project.