Reporting and Analyzing Inventory

6-41

168. Redeker Company had the following records:

2014 2013 2012

Ending inventory $34,580 $32,650 $30,490

Cost of goods sold 182,000 163,500 174,200

What is Redeker’s average days in inventory for 2014? (rounded)

a. 67.6 days

b. 66.4 days

c. 68.9 days

d. 68.25 days

169. Barnett Company had the following records:

2014 2013 2012

Ending inventory $34,580 $32,650 $30,490

Cost of goods sold 273,000 255,250 261,300

What is Barnett’s inventory turnover for 2013? (rounded)

a. 7.6 times

b. 8.1 times

c. 0.1 times

d. 7.8 times

170. Barnett Company had the following records:

2014 2013 2012

Ending inventory $34,580 $37,650 $30,490

Cost of goods sold 273,000 255,250 261,300

What is Barnett’s average days in inventory for 2013? (rounded)

a. 45.1 days

b. 48.0 days

c. 46.8 days

d. 365 days

171. The difference between ending inventory using LIFO and ending inventory using FIFO is

referred to as the

a. FIFO reserve.

b. inventory reserve.

c. LIFO reserve.

d. periodic reserve.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

6-42

172. The LIFO reserve is

a. the difference between the value of the inventory under LIFO and the value under

FIFO.

b. an amount used to adjust inventory to the lower of cost or market.

c. the difference between the value of the inventory under LIFO and the value under

average cost.

d. the amount used to adjust inventory to history cost.

173. Reporting which one of the following allows analysts to make adjustments to compare

companies using different cost flow methods?

a. FIFO reserve

b. Inventory turnover

c. LIFO reserve

d. Current replacement cost

174. Butler Company reported ending inventory at December 31, 2014 of $1,200,000 under

LIFO. It also reported a LIFO reserve of $210,000 at January 1, 2014, and $300,000 at

December 31, 2014. Cost of goods sold for 2014 was $4,600,000. If Butler Company had

used FIFO during 2014, its cost of goods sold for 2014 would have been

a. $4,900,000.

b. $4,690,000.

c. $4,510,000.

d. $4,300,000.

175. To adjust a company’s LIFO cost of goods sold to FIFO cost of goods sold

a. the ending LIFO reserve is added to LIFO cost of goods sold.

b. the ending LIFO reserve is subtracted from LIFO cost of goods sold.

c. an increase in the LIFO reserve is subtracted from LIFO cost of goods sold.

d. a decrease in the LIFO reserve is subtracted from LIFO cost of goods sold.

176. All of the following statements are true regarding the LIFO reserve except:

a. Companies using LIFO are required to report the LIFO reserve.

b. The equation (LIFO inventory – LIFO reserve = FIFO inventory) adjusts the inventory

balance from LIFO to FIFO.

c. The financial statement differences of using LIFO normally increase the longer a

company uses LIFO.

d. Current ratios and the inventory turnover can be significantly affected if a company

has material LIFO reserves.

Reporting and Analyzing Inventory

6-43

177. Use the following information for Boxter, Inc., Clifford Company, Danforth Industries, and

Evans Services to answer the question “What is Danforth’s LIFO reserve for 2013?”

(amounts in $ millions)

Boxter

Clifford

Danforth

Evans

Inventory Method for 2013 & 2014

LIFO

FIFO

LIFO

FIFO

2013 Ending inventory assuming LIFO

$324

N/A

$225

N/A

2013 Ending inventory assuming FIFO

$427

$535

$310

$663

2014 Ending inventory assuming LIFO

$436

N/A

$167

N/A

2014 Ending inventory assuming FIFO

$578

$612

$209

$542

2013 Current assets

(reported on balance sheet)

$1,677

$2,031

$1,308

$2,748

2013 Current liabilities

$987

$1,209

$545

$1,200

2014 Current assets

(reported on balance sheet)

$2,225

$2,605

$1,100

$2,390

2014 Current liabilities

$1,306

$1,410

$465

$1,000

2014 Cost of goods sold

$4,678

$5,042

$3,000

$7,000

a. $535

b. $85

c. $42

d. $58

178. Use the following information for Boxter, Inc., Clifford Company, Danforth Industries, and

Evans Services to answer the question “Using the LIFO reserve adjustment, which

company would has the strongest liquidity position for 2014 as expressed by the current

ratio?”

(amounts in $ millions)

Boxter

Clifford

Danforth

Evans

Inventory Method for 2013 & 2014

LIFO

FIFO

LIFO

FIFO

2013 Ending inventory assuming LIFO

$324

N/A

$225

N/A

2013 Ending inventory assuming FIFO

$427

$535

$310

$663

2014 Ending inventory assuming LIFO

$436

N/A

$167

N/A

2014 Ending inventory assuming FIFO

$578

$612

$209

$542

2013 Current assets

(reported on balance sheet)

$1,677

$2,031

$1,308

$2,748

2013 Current liabilities

$987

$1,209

$545

$1,200

2014 Current assets

(reported on balance sheet)

$2,225

$2,605

$1,100

$2,390

2014 Current liabilities

$1,306

$1,410

$465

$1,000

2014 Cost of goods sold

$4,678

$5,042

$3,000

$7,000

a. Boxter

b. Clifford

c. Danforth

d. Evans

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

6-44

179. Use the following information for Boxter, Inc., Clifford Company, Danforth Industries, and

Evans Services to answer the question “Using the LIFO adjustment, what is Boxter’s

inventory turnover ratio for 2014 (to the closest decimal place)?”

(amounts in $ millions)

Boxter

Clifford

Danforth

Evans

Inventory Method for 2013 & 2014

LIFO

FIFO

LIFO

FIFO

2013 Ending inventory assuming LIFO

$324

N/A

$225

N/A

2013 Ending inventory assuming FIFO

$427

$535

$310

$663

2014 Ending inventory assuming LIFO

$436

N/A

$167

N/A

2014 Ending inventory assuming FIFO

$578

$612

$209

$542

2013 Current assets

(reported on balance sheet)

$1,677

$2,031

$1,308

$2,748

2013 Current liabilities

$987

$1,209

$545

$1,200

2014 Current assets

(reported on balance sheet)

$2,225

$2,605

$1,100

$2,390

2014 Current liabilities

$1,306

$1,410

$465

$1,000

2014 Cost of goods sold

$4,678

$5,042

$3,000

$7,000

a. 12.3 times

b. 9.3 times

c. 7.5 times

d. 6.4 times

180. Use the following information for Boxter, Inc., Clifford Company, Danforth Industries, and

Evans Services to answer the question “Using the LIFO adjustment, which company

shows the greatest improvement in its current ratio from 2013 to 2014?”

(amounts in $ millions)

Boxter

Clifford

Danforth

Evans

Inventory Method for 2013 & 2014

LIFO

FIFO

LIFO

FIFO

2013 Ending inventory assuming LIFO

$324

N/A

$225

N/A

2013 Ending inventory assuming FIFO

$427

$535

$310

$663

2014 Ending inventory assuming LIFO

$436

N/A

$167

N/A

2014 Ending inventory assuming FIFO

$578

$612

$209

$542

2013 Current assets

(reported on balance sheet)

$1,677

$2,031

$1,308

$2,748

2013 Current liabilities

$987

$1,209

$545

$1,200

2014 Current assets

(reported on balance sheet)

$2,225

$2,605

$1,100

$2,390

2014 Current liabilities

$1,306

$1,410

$465

$1,000

2014 Cost of goods sold

$4,678

$5,042

$3,000

$7,000

a. Boxter

b. Clifford

c. Danforth

d. Evans

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-45

*181. In a perpetual inventory system,

a. LIFO cost of goods sold will be the same as in a periodic inventory system.

b. average costs are based entirely on unit cost simple averages.

c. a new average is computed under the average cost method after each sale.

d. FIFO cost of goods sold will be the same as in a periodic inventory system.

*182. Classic Floors has the following inventory data:

July 1 Beginning inventory 15 units at $6.00

5 Purchases 60 units at $6.60

14 Sale 40 units

21 Purchases 30 units at $7.20

30 Sale 28 units

Assuming that a perpetual inventory system is used, what is the cost of goods sold on a

LIFO basis for July?

a. $465.60

b. $236.40

c. $702.00

d. $348.00

*183. Classic Floors has the following inventory data:

July 1 Beginning inventory 15 units at $6.00

5 Purchases 60 units at $6.60

14 Sale 40 units

21 Purchases 30 units at $7.20

30 Sale 28 units

Assuming that a perpetual inventory system is used, what is the value of ending inventory

on a LIFO basis for July?

a. $465.60

b. $702.00

c. $354.00

d. $236.40

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-46

*184. Snug-As-A-Bug Blankets has the following inventory data:

July 1 Beginning inventory 15 units at $60

5 Purchases 90 units at $56

14 Sale 60 units

21 Purchases 45 units at $58

30 Sale 42 units

Assuming that a perpetual inventory system is used, what is the cost of goods sold on a

LIFO basis for July?

a. $5,802

b. $5,772

c. $5,796.

d. $5,916

*185. Snug-As-A-Bug Blankets has the following inventory data:

July 1 Beginning inventory 15 units at $60

5 Purchases 90 units at $56

14 Sale 60 units

21 Purchases 45 units at $58

30 Sale 42 units

Assuming that a perpetual inventory system is used, what is the ending inventory on a

LIFO basis for July?

a. $2,748

b. $2,754

c. $2,772.

d. $5,796

*186. Snug-As-A-Bug Blankets has the following inventory data:

July 1 Beginning inventory 15 units at $60

5 Purchases 90 units at $56

14 Sale 60 units

21 Purchases 45 units at $58

30 Sale 42 units

Assuming that a perpetual inventory system is used, what is ending inventory (rounded)

under the average cost method for July?

a. $2,750

b. $2,784

c. $2,406.

d. $2,772

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-47

*187. An error in the physical count of goods on hand at the end of a period resulted in a

$10,000 overstatement of the ending inventory. The effect of this error in the current

period is

Cost of Goods Sold Net Income

a. Understated Understated

b. Overstated Overstated

c. Understated Overstated

d. Overstated Understated

*188. If beginning inventory is understated by $10,000, the effect of this error in the current

period is

Cost of Goods Sold Net Income

a. Understated Understated

b. Overstated Overstated

c. Understated Overstated

d. Overstated Understated

*189. A company uses the periodic inventory method and the beginning inventory is overstated

by $4,000 because the ending inventory in the previous period was overstated by $4,000;

the ending inventory for this period is correct. The amounts reflected in the current end of

the period balance sheet are

Asset Stockholders’ Equity

a. Overstated Overstated

b. Correct Correct

c. Understated Understated

d. Overstated Correct

*190. An overstatement of the beginning inventory results in

a. no effect on the period’s net income.

b. an overstatement of net income.

c. an understatement of net income.

d. a need to adjust purchases.

*191. An overstatement of ending inventory in one period results in

a. no effect on net income of the next period.

b. an overstatement of net income of the next period.

c. an understatement of net income of the next period.

d. an overstatement of the ending inventory of the next period.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-48

Answers to Multiple Choice Questions

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-49

BRIEF EXERCISES

Be. 192

Shellan Kamp Company identifies the following items for possible inclusion in the physical

inventory. Indicate whether each item should be included or excluded from the inventory taking.

1. Goods shipped on consignment by Shellan Kamp to another company.

2. Goods in transit from a supplier shipped FOB destination.

3. Goods shipped via common carrier to a customer with terms FOB shipping point.

4. Goods held on consignment from another company.

Be. 193

In the first month of operations, Dieker Company made three purchases of merchandise in the

following sequence: (1) 200 units at $6, (2) 300 units at $7, and (3) 400 units at $8. Assuming

there are 250 units on hand, compute the cost of the ending inventory under (1) the FIFO method

and (2) the LIFO method. Dieker uses a periodic inventory system.

Be. 194

Hess Company’s inventory records show the following data for the month of September:

Units Unit Cost

Inventory, September 1 100 $3.00

Purchases: September 8 450 3.50

September 18 300 3.70

A physical inventory on September 30 shows 150 units on hand.

Calculate the value of ending inventory and cost of goods sold if the company uses FIFO

inventory costing and a periodic inventory system.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-50

Solution 194 (5 min.)

Be. 195

Hess Company’s inventory records show the following data for the month of September:

Units Unit Cost

Inventory, September 1 100 $3.00

Purchases: September 8 450 3.50

September 18 300 3.70

A physical inventory on September 30 shows 150 units on hand.

Calculate the value of ending inventory and cost of goods sold if the company uses LIFO

inventory costing and a periodic inventory system.

Be. 196

The management of Otto Corp. is considering the effects of various inventory costing methods on

its financial statements and its income tax expense. Assuming that the price the company pays

for inventory is increasing, which method will:

1. result in the lowest income tax expense?

2. provide the highest net income?

3. provide the highest ending inventory?

4. result in the most stable earnings over a number of years?

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-51

Be. 197

The Entertainment Center accumulates the following cost and market data at December 31.

Inventory Cost Market

Categories Data _ _ Data_

Camera $11,000 $10,200

Camcorders 8,000 8,500

DVDs 14,000 12,600

What is the lower-of-cost–or-market value of the inventory?

Be. 198

At December 31, 2014, the following information (in thousands) was available for Kitselman Inc.:

ending inventory $22,600; beginning inventory $21,400; cost of goods sold $198,000; and sales

revenue $430,000. Calculate the inventory turnover and days in inventory for Kitselman.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

6-52

EXERCISES

Ex. 199

The Cain Company has just completed a physical inventory count at year end, December 31,

2014. Only the items on the shelves, in storage, and in the receiving area were counted and

costed on the FIFO basis. The inventory amounted to $80,000. During the audit, the independent

CPA discovered the following additional information:

(a) There were goods in transit on December 31, 2014, from a supplier with terms FOB

destination, costing $10,000. Because the goods had not arrived, they were excluded from

the physical inventory count.

(b) On December 27, 2014, a regular customer purchased goods for cash amounting to $1,000

and had them shipped to a bonded warehouse for temporary storage on December 28, 2014.

The goods were shipped via common carrier with terms FOB shipping point. The customer

picked the goods up from the warehouse on January 4, 2015. Cain Company had paid $500 for

the goods and, because they were in storage, Cain included them in the physical inventory count.

(c) Cain Company, on the date of the inventory, received notice from a supplier that goods

ordered earlier, at a cost of $4,000, had been delivered to the transportation company on

December 28, 2014; the terms were FOB shipping point. Because the shipment had not

arrived on December 31, 2014, it was excluded from the physical inventory.

(d) On December 31, 2014, there were goods in transit to customers, with terms FOB shipping

point, amounting to $800 (expected delivery on January 8, 2015). Because the goods had

been shipped, they were excluded from the physical inventory count.

(e) On December 31, 2014, Cain Company shipped $2,500 worth of goods to a customer, FOB

destination. The goods arrived on January 5, 2014. Because the goods were not on hand,

they were not included in the physical inventory count.

(f) Cain Company, as the consignee, had goods on consignment that cost $3,000. Because these

goods were on hand as of December 31, 2014, they were included in the physical inventory

count.

Instructions

Analyze the above information and calculate a corrected amount for the ending inventory. Explain

the basis for your treatment of each item.

Reporting and Analyzing Inventory

6-53

Ex. 200

Dalton Company was undergoing an end of year audit of its financial records. The auditors were

in the process of reviewing Dalton’s inventory for year end, December 31, 2014. They completed

an end of year inventory. The value of the ending inventory prior to any adjustments was

$185,000, but before finishing up they had a few questions. Discussion with Dalton’s accountant

revealed the following:

(a) Dalton sold goods costing $60,000 to Summey Company FOB shipping point on December

28. The goods are not expected to reach Summey until January 12. The goods were not

included in the physical inventory because they were not in the warehouse.

(b) The physical count of the inventory did not include goods costing $95,000 that were shipped

to Dalton FOB destination on December 27 and were still in transit at year–end.

(c) Dalton received goods costing $25,000 on January 2. The goods were shipped FOB

shipping point on December 26 by Strong Company. The goods were not included in the

physical count.

(d) Dalton sold goods costing $40,000 to Hampton Company FOB destination on December 30.

The goods were received by Hampton Company on January 8. Because the goods had

been shipped, they were excluded from the physical inventory count.

(e) Dalton received goods costing $42,000 on January 2 that were shipped FOB destination on

December 29. The shipment was a rush order that was suppose to arrive December 31.

This purchase was included in the ending inventory of $192,000.

(f) Dalton Company, as the consignee, had goods on consignment that cost $3,000. Because

these goods were on hand as of December 31, they were included in the physical inventory

count.

Instructions

Analyze the above information and calculate a corrected amount for the ending inventory. Explain

the basis for your treatment of each item.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-54

Solution 200 (20 min.)

Ex. 201

Dennis Lee, an auditor with Knapp CPAs, is performing a review of Dobson Company’s inventory

account. Dobson did not have a good year, and top management is under pressure to boost

reported income. According to its records, the inventory balance at year-end was $640,000.

However, the following information was not considered when determining that amount.

1. Included in the company‘s count were goods with a cost of $200,000 that the company is

holding on consignment. The goods belong to Agler Corporation.

2. The physical count did not include goods purchased by Dobson with a cost of $40,000 that

were shipped FOB shipping point on December 28 and did not arrive at Dobson’s warehouse

until January 3.

3. Included in the inventory account was $22,000 of office supplies that were stored in the

warehouse and were to be used by the company’s supervisors and managers during the

coming year.

4. The company received an order on December 29 that was boxed and was sitting on the

loading dock awaiting pick-up on December 31. The shipper picked up the goods on January

1 and delivered them on January 6. The shipping terms were FOB shipping point. The goods

had a selling price of $40,000 and a cost of $30,000. The goods were not included in the

count because they were sitting on the dock.

5. On December 29, Dobson shipped goods with a selling price of $90,000 and a cost of

$70,000 to Central Sales Corporation FOB shipping point. The goods arrived on January 3.

Central Sales had only ordered goods with a selling price of $10,000 and a cost of $8,000.

However, a sales manager at Dobson had authorized the shipment and said that if Central

wanted to ship the goods back next week, it could.

6. Included in the count was $50,000 of goods that were parts for a machine that the company

no longer made. Given the high-tech nature of Dobson’s products, it was unlikely that these

obsolete parts had any other use. However, management would prefer to keep them on the

books at cost, “since that is what we paid for them, after all.”

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-55

Ex. 201 (Cont.)

Instructions

Prepare a schedule to determine the correct inventory amount. Provide explanations for each

item above, saying why you did or did not make an adjustment for each item.

Ex. 202

Grother Company uses the periodic inventory method and had the following inventory information

available:

Units Unit Cost Total Cost

1/1 Beginning Inventory 100 $4 $ 400

1/20 Purchase 500 $5 2,500

7/25 Purchase 100 $7 700

10/20 Purchase 300 $8 2,400

1,000 $6,000

A physical count of inventory on December 31 revealed that there were 350 units on hand.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-56

Ex. 202 (Cont.)

Instructions

Answer the following independent questions and show computations supporting your answers.

1. Assume that the company uses the FIFO method. The value of the ending inventory at

December 31 is $__________.

2. Assume that the company uses the average cost method. The value of the ending inventory

on December 31 is $__________.

3. Assume that the company uses the LIFO method. The value of the ending inventory on

December 31 is $__________.

4. Determine the difference in the amount of income that the company would have reported if it

had used the FIFO method instead of the LIFO method. Would income have been greater or

less?

Reporting and Analyzing Inventory

6-57

Ex. 203

Hansen Company uses the periodic inventory method and had the following inventory information

available:

Units Unit Cost Total Cost

1/1 Beginning Inventory 100 $3 $ 300

1/20 Purchase 500 $4 2,000

7/25 Purchase 100 $5 500

10/20 Purchase 300 $6 1,800

1,000 $4,600

A physical count of inventory on December 31 revealed that there were 380 units on hand.

Instructions

Answer the following independent questions and show computations supporting your answers.

1. Assume that the company uses the FIFO method. The value of the ending inventory at

December 31 is $__________.

2. Assume that the company uses the average cost method. The value of the ending inventory

on December 31 is $__________.

3. Assume that the company uses the LIFO method. The value of the ending inventory on

December 31 is $__________.

4. Determine the difference in the amount of income that the company would have reported if it

had used the FIFO method instead of the LIFO method. Would income have been greater or

less?

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-58

Solution 203 (Cont.)

Ex. 204

Faster Company uses the periodic inventory method and had the following inventory information

available:

Units Unit Cost Total Cost

1/1 Beginning Inventory 15 $8.00 $ 120

1/20 Purchase 60 $8.80 528

7/25 Purchase 30 $8.40 252

10/20 Purchase 45 $9.60 432

150 $1,332

A physical count of inventory on December 31 revealed that there were 55 units on hand.

Instructions

Answer the following independent questions and show computations supporting your answers.

1. Assume that the company uses the FIFO method. The value of the ending inventory at

December 31 is $__________.

2. Assume that the company uses the Average Cost method. The value of the ending inventory

on December 31 is $__________.

3. Assume that the company uses the LIFO method. The value of the ending inventory on

December 31 is $__________.

4. Assume that the company uses the FIFO method. The value of the cost of goods sold at

December 31 is $__________.

Ans: N/A, LO: 2, Bloom: AP, Difficulty: Medium, Min: 20, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

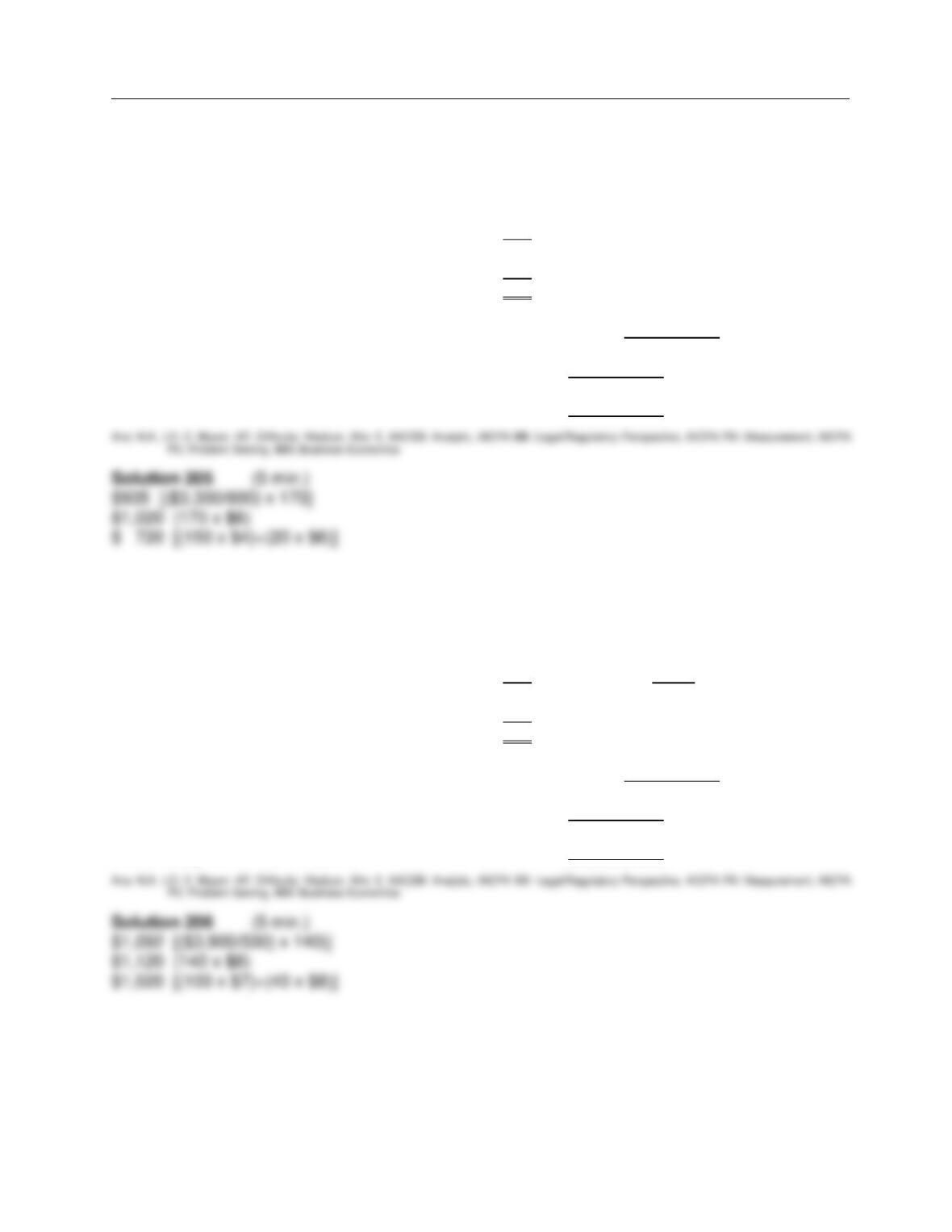

Solution 204 (20 min.)

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-59

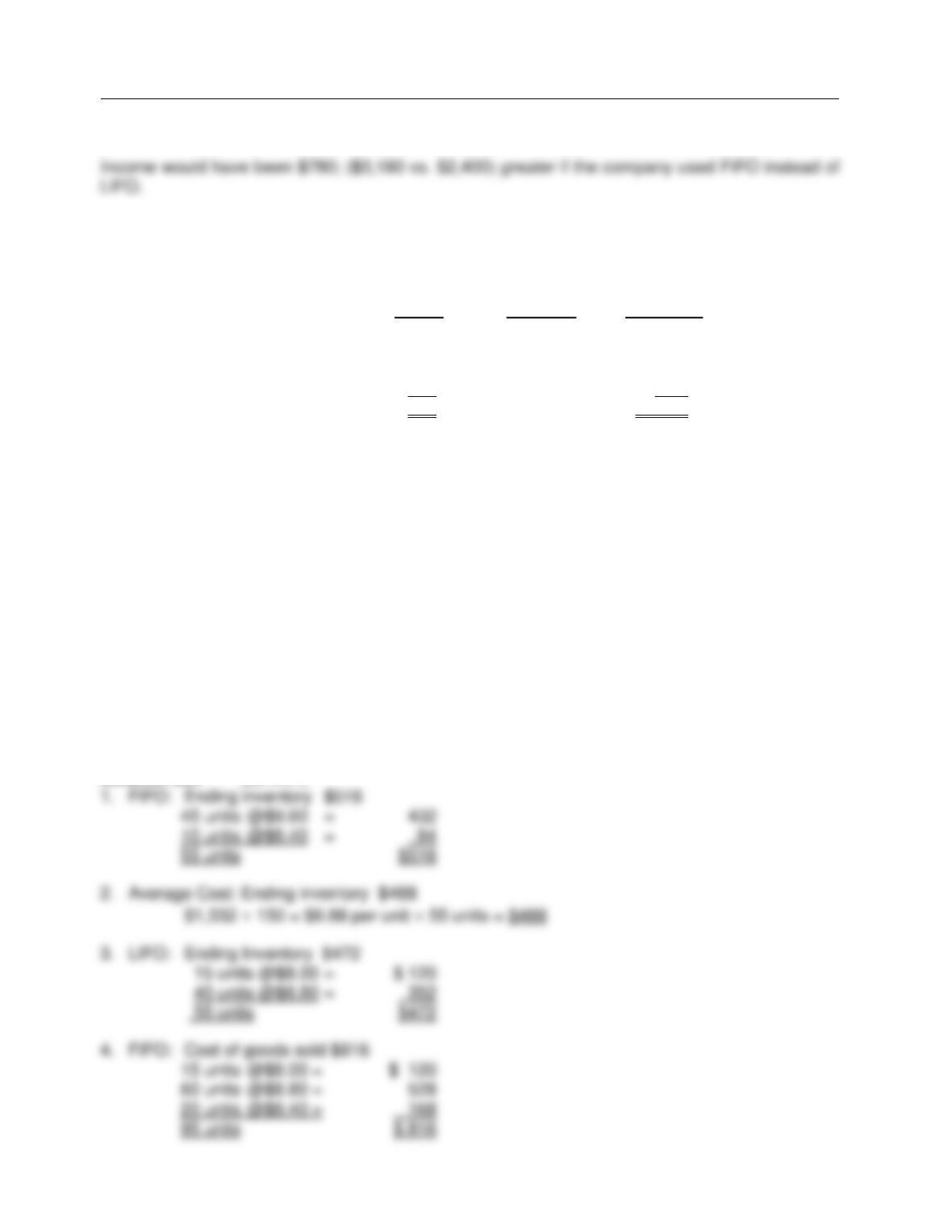

Ex. 205

Compute the cost to be assigned to ending inventory for each of the methods indicated given the

following information about purchases and sales during the year.

January 1 Beginning Inventory 150 items @ $4 = $ 600

May 1 Purchases 450 items @ $6 = 2,700

Total Available 600 items $3,300

Total Sales 430 items

December 31 Ending Inventory 170

Cost assigned on an average cost basis $__________

Cost assigned on a FIFO basis $__________

Costs assigned on a LIFO basis $__________

Ex. 206

Compute the cost to be assigned to ending inventory for each of the methods indicated given the

following information about purchases and sales during the year.

January 1 Beginning Inventory 100 items @ $7 = $ 700

May 1 Purchases 400 items @ $8 = 3,200

Total Available 500 items $3,900

Total Sales 360 items

December 31 Ending Inventory 140

Cost assigned on an average cost basis $__________

Cost assigned on a FIFO basis $__________

Costs assigned on a LIFO basis $__________

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-60

Ex. 207

Wooderson Company sells many products. Gizmo is one of its popular items. Below is an analysis of

the inventory purchases and sales of Gizmo for the month of March. Wooderson Company uses the

periodic inventory system.

Purchases Sales

Units Unit Cost Units Selling Price/Unit

3/1 Beginning inventory 100 $40

3/3 Purchase 60 $50

3/4 Sales 60 $80

3/10 Purchase 200 $55

3/16 Sales 70 $90

3/19 Sales 90 $90

3/25 Sales 60 $90

3/30 Purchase 40 $60

Instructions

(a) Using the FIFO assumption, calculate the amount charged to cost of goods sold for March.

(Show computations)

(b) Using the weighted-average method, calculate the amount assigned to the inventory on

hand on March 31. (Show computations)

(c) Using the LIFO assumption, calculate the amount assigned to the inventory on hand on

March 31. (Show computations)