Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-61

Solution 207 (Cont.)

(c) There are 120 units in ending inventory. They are comprised of the first units purchased

when LIFO is assumed.

3/1 100 @ $40 = $4,000

3/3 20 @ $50 = 1,000

120 units $5,000 = Ending inventory

Ex. 208

Torrey Company uses the periodic inventory system to account for inventories. Information

related to Torrey Company’s inventory at October 31 is given below:

October 1 Beginning inventory 400 units @ $10.00 = $ 4,000

8 Purchase 800 units @ $10.40 = 8,320

16 Purchase 600 units @ $10.80 = 6,480

24 Purchase 200 units @ $11.60 = 2,320

Total units and cost 2,000 units $21,120

Instructions

1. Show computations to value the ending inventory using the FIFO cost assumption if 500 units

remain on hand at October 31.

2. Show computations to value the ending inventory using the weighted-average cost method if

500 units remain on hand at October 31.

3. Show computations to value the ending inventory using the LIFO cost assumption if 500 units

remain on hand at October 31.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-62

Ex. 209

Hanlin Company uses the periodic inventory system to account for inventories. Information

related to Hanlin Company’s inventory at January 31 is given below:

January 1 Beginning inventory 400 units @ $12.00 = $ 4,800

8 Purchase 800 units @ $12.40 = 9,920

16 Purchase 600 units @ $12.80 = 7,680

24 Purchase 200 units @ $13.20 = 2,640

Total units and cost 2,000 units $25,040

Instructions

1. Show computations to value the ending inventory using the FIFO cost assumption if 600 units

remain on hand at January 31.

2. Show computations to value the ending inventory using the weighted-average cost method if

600 units remain on hand at January 31.

3. Show computations to value the ending inventory using the LIFO cost assumption if 600 units

remain on hand at January 31.

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-63

Ex. 210

Johnson Company reports the following for the month of June.

Date

Explanation

Units

Unit Cost

Total Cost

June 1

Inventory

225

$5

$1,125

12

Purchase

525

6

3,150

23

Purchase

750

7

5,250

30

Inventory

280

(a) Compute the cost of the ending inventory and the cost of goods sold under (1) FIFO, (2)

LIFO, and (3) average cost.

(b) Which costing method gives the highest ending inventory? The highest cost of goods sold?

Why?

(c) How do the average-cost values for ending inventory and cost of goods sold relate to ending

inventory and cost of goods sold for FIFO and LIFO?

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-64

Solution 210 (Cont.)

Ex. 211

Wolf Camera Shop Inc. uses the lower-of-cost-or-market basis for its inventory. The following

data are available at December 31.

Market

Units

Cost/Unit

Value/Unit

Cameras

Minolta

5

$175

$168

Canon

7

148

152

Light Meters

Vivitar

15

125

119

Kodak

10

120

135

Instructions

What amount should be reported on Wolf Camera Shop’s financial statements, assuming the

lower-of-cost-or-market rule is applied?

Ex. 212

This information is available for Groneman, Inc. for 2013 and 2014.

(in millions)

2013

2014

Beginning inventory

$ 2,290

$ 2,522

Ending inventory

2,522

2,618

Cost of goods sold

24,351

23,099

Sales

43,251

43,232

Instructions

Calculate the inventory turnover, days in inventory, and gross profit rate for Groneman., Inc. for

2013 and 2014. Comment on any trends.

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-65

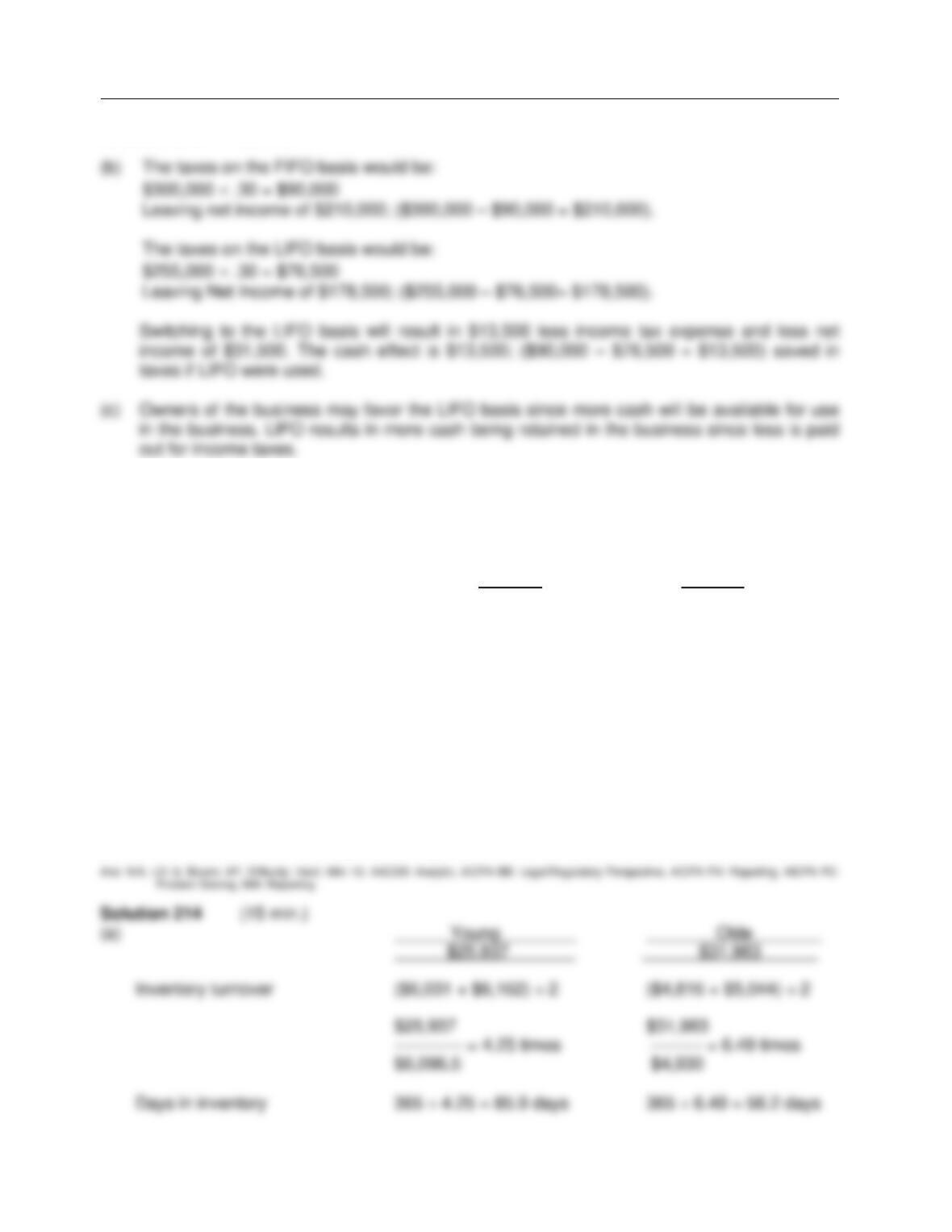

Ex. 213

Burnham Company reported the following summarized annual data at the end of 2014:

Sales revenue $1,600,000

Cost of goods sold* 900,000

Gross margin 700,000

Operating expenses 400,000

Income before income taxes $ 300,000

*Based on an ending FIFO inventory of $250,000.

The income tax rate is 30%. The controller of the company is considering a switch from FIFO to

LIFO. He has determined that on a LIFO basis, the ending inventory would have been $205,000.

Instructions

(a) Restate the summary information on a LIFO basis.

(b) What effect, if any, would the proposed change have on Burnham’s income tax expense, net

income, and cash flows?

(c) If you were an owner of this business, what would your reaction be to this proposed change?

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-66

Solution 213 (Cont.)

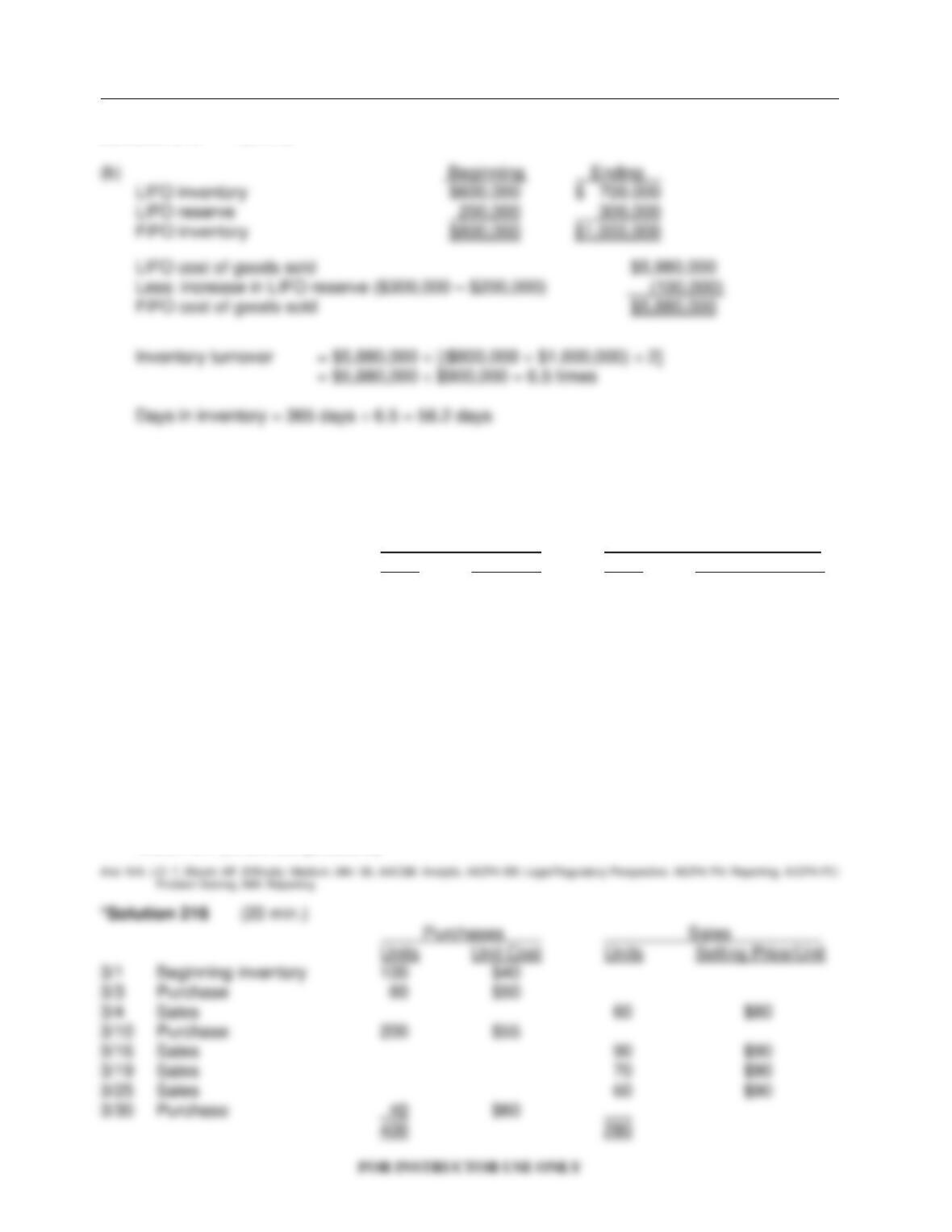

Ex. 214

The following information is available from the annual reports of Young and Olde:

(Amounts in millions)

Young Olde

2014 ending Inventory $ 6,031 $ 4,816

2013 ending inventory 6,162 5,044

Cost of goods sold 25,937 31,983

Sales revenue 29,656 36,704

2014 LIFO reserve 227 —

2013 LIFO reserve 225 —

Instructions

(a) Calculate the inventory turnover and days in inventory for both companies.

(b) Calculate Young’s inventory turnover after adjusting for the LIFO reserve. Young uses the

LIFO inventory method.

(c) What conclusion concerning the management of inventory can be drawn from these data?

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-67

Solution 214 (Cont.)

Ex. 215

The following information is available for Wallace Company for 2014. Wallace uses the LIFO

inventory method.

Beginning inventory $ 600,000

Ending inventory 700,000

Beginning LIFO reserve 200,000

Ending LIFO reserve 300,000

Cost of goods sold 5,980,000

Sales 8,000,000

Instructions

(a) Calculate the inventory turnover and days in inventory for Wallace Company based on LIFO.

(b) Calculate the inventory turnover and days in inventory after adjusting for the LIFO reserve.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

6-68

Solution 215 (Cont.)

*Ex. 216

Woodson Company sells many products. Gizmo is one of its popular items. Below is an analysis

of the inventory purchases and sales of Gizmo for the month of March. Woodson Company uses

the perpetual inventory system.

Purchases Sales

Units Unit Cost Units Selling Price/Unit

3/1 Beginning inventory 100 $40

3/3 Purchase 60 $50

3/4 Sales 60 $80

3/10 Purchase 200 $55

3/16 Sales 90 $90

3/19 Sales 70 $90

3/25 Sales 60 $90

3/30 Purchase 40 $60

Instructions

(a) Using the FIFO assumption, calculate the amount charged to cost of goods sold for March.

(Show computations)

(b) Using the LIFO assumption, calculate the amount assigned to the inventory on hand on

March 31. (Show computations)

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-69

*Solution 216 (Cont.)

*Ex. 217

Grayson Company sells many products. Gizmo is one of its popular items. Below is an analysis of

the inventory purchases and sales of Gizmo for the month of March. Grayson Company uses the

perpetual inventory system.

Purchases Sales

Units Unit Cost Units Selling Price/Unit

3/1 Beginning inventory 100 $55

3/3 Purchase 60 $60

3/4 Sales 60 $120

3/10 Purchase 200 $65

3/16 Sales 90 $130

3/19 Sales 70 $130

3/25 Sales 50 $130

3/30 Purchase 40 $75

Instructions

(a) Using the FIFO assumption, calculate the amount charged to cost of goods sold for March.

(Show computations)

(b) Using the FIFO assumption, calculate the value of ending inventory for March.

(c) Using the moving average cost method, calculate the amount assigned to the inventory on

hand on March 31. (Show computations)

(d) Using the LIFO assumption, calculate the amount assigned to the inventory on hand on

March 31. (Show computations)

(e) Using the LIFO assumption, calculate the amount charged to cost of goods sold for March.

(Show computations)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-70

Reporting and Analyzing Inventory

6-71

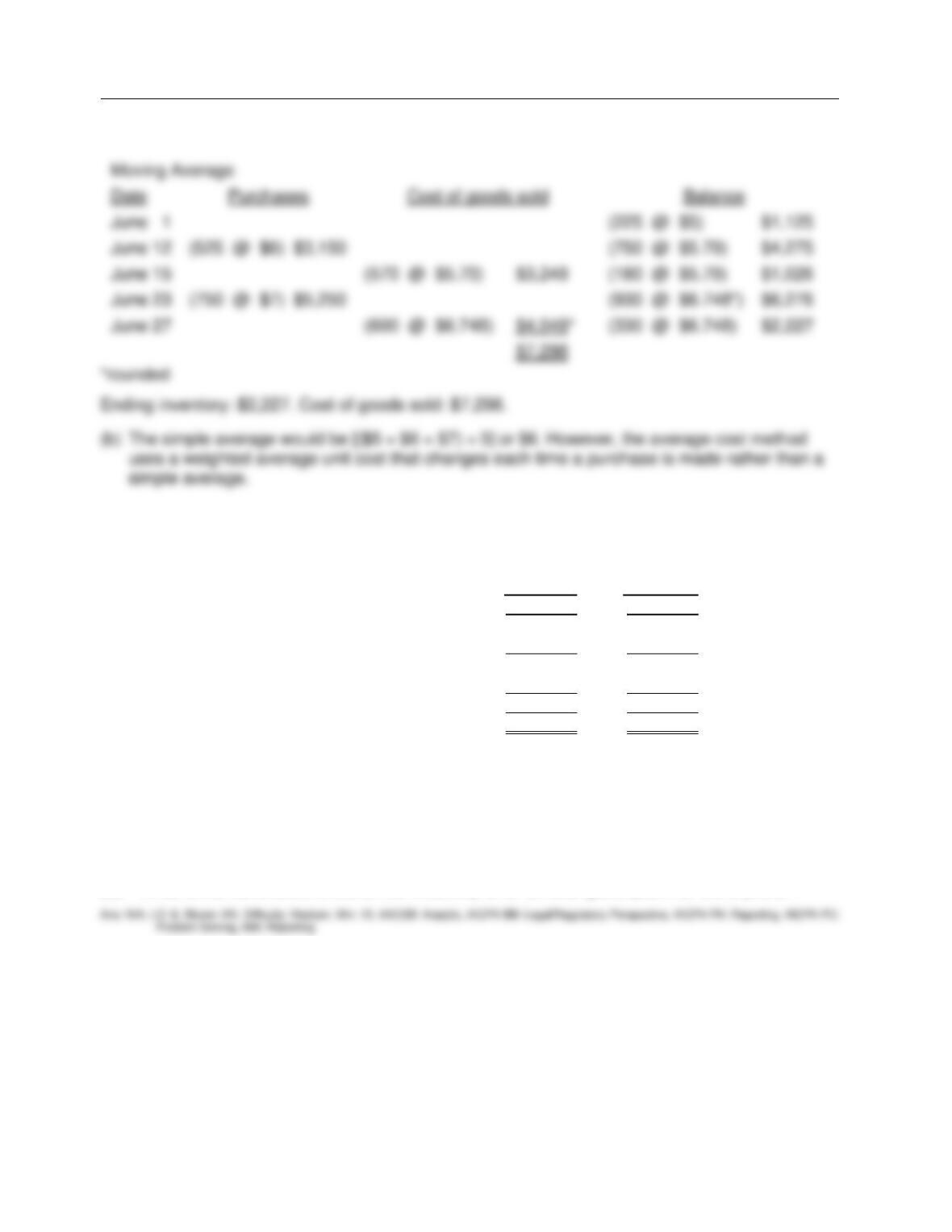

*Ex. 218

Plato Company reports the following for the month of June.

Date

Explanation

Units

Unit Cost

Total Cost

June 1

Inventory

225

$5

$1,125

12

Purchase

525

6

3,150

23

Purchase

750

7

5,250

30

Inventory

330

Instructions

(a) Calculate the cost of the ending inventory and the cost of goods sold for each cost flow

assumption, using a perpetual inventory system. Assume a sale of 570 units occurred on

June 15 for a selling price of $8 and a sale of 600 units on June 27 for $9. (Note: For the

average-cost method, round unit cost to three decimal places.)

(b) Why is the average unit cost not $6 [($5 + $6 + $7) 3 = $6]?

Date

June 12

(525 @ $6) $3,150

(225 @ $5)

June 15

(225 @ $5)

June 23

(750 @ $7) $5,250

(180 @ $6)

June 27

(180 @ $6)

Date

June 12

(525 @ $6) $3,150

(225 @ $5)

June 15

(525 @ $6)

June 23

(750 @ $7) $5,250

(180 @ $5)

(180 @ $5)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-72

*Solution 218 (Cont.)

*Ex. 219

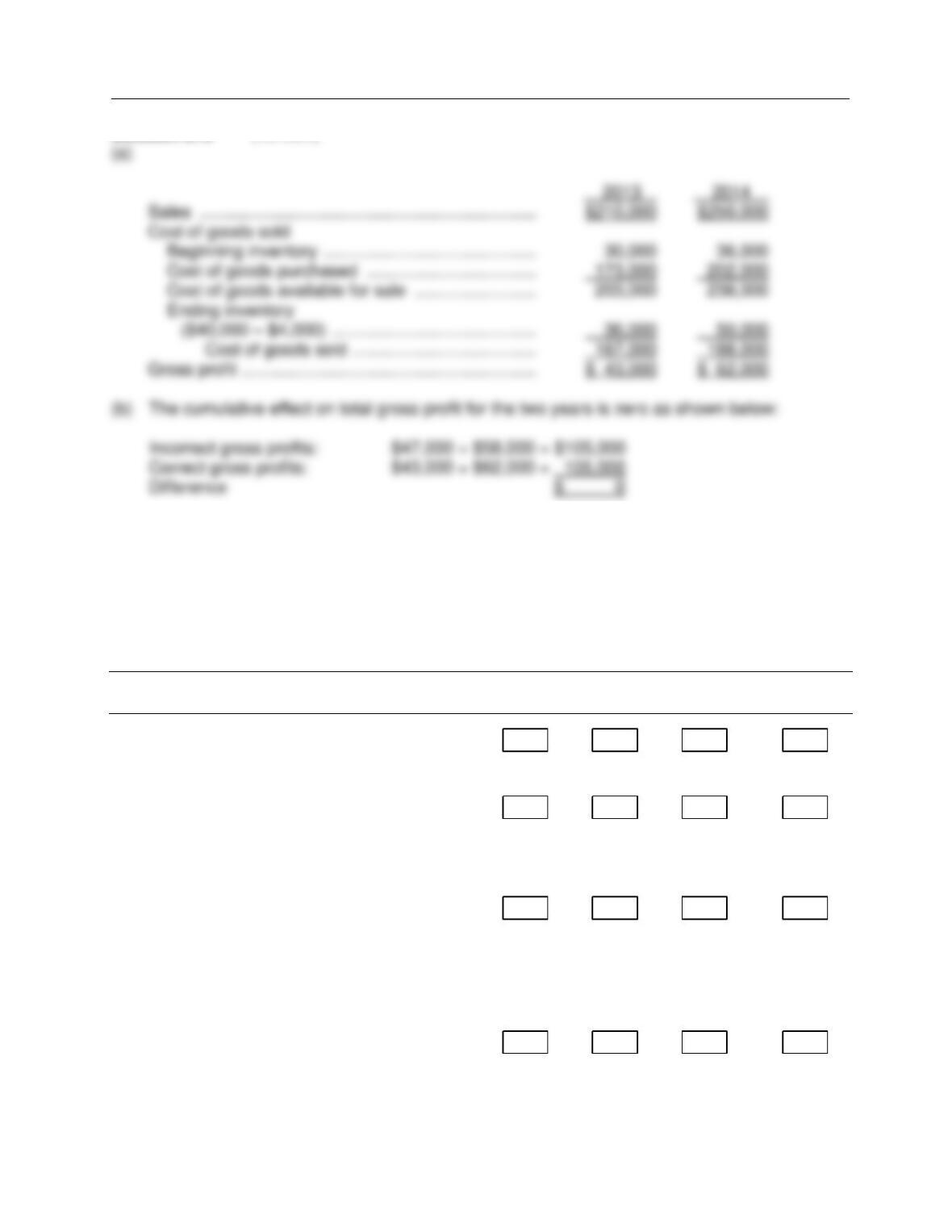

Carter Company reported these income statement data for a 2-year period.

2014

2013

Sales

$250,000

$210,000

Beginning inventory

40,000

30,000

Cost of goods purchased

202,000

173,000

Cost of goods available for sale

242,000

203,000

Ending inventory

50,000

40,000

Cost of goods sold

192,000

163,000

Gross profit

$ 58,000

$ 47,000

Carter Company uses a periodic inventory system. The inventories at January 1, 2013, and

December 31, 2014, are correct. However, the ending inventory at December 31, 2013, is

overstated by $4,000.

Instructions

(a) Prepare correct income statement data for the 2 years.

(b) What is the cumulative effect of the inventory error on total gross profit for the 2 years?

Reporting and Analyzing Inventory

FOR INSTRUCTOR USE ONLY

6-73

Solution 219 (15 min.)

*Ex. 220

For each of the independent events listed below, analyze the impact on the indicated items at the

end of the current year by placing the appropriate code letter in the box under each item.

Code: O = item is overstated

U = item is understated

NA = item is not affected

Items

Stockholders’ Cost of Net

Events Assets Equity Goods Sold Income

1. The ending inventory in the previous period

was overstated.

_______________________________________________________________________________________________________________________

2. A physical count of goods on hand at the

end of the current year resulted in some

goods being counted twice.

_______________________________________________________________________________________________________________________

3. Goods purchased on account in December

of the current year and shipped FOB

shipping point were recorded as purchases,

but were not included in the count of goods

on hand on December 31 because they had

not arrived by December 31.

_______________________________________________________________________________________________________________________

4. Goods purchased on account in December

of the current year and shipped FOB

destination were recorded as purchases, but

were not included in the count of goods on

hand on December 31 because they had not

arrived by December 31.

_______________________________________________________________________________________________________________________

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

6-74

*Ex. 220 (Cont.)

5. The internal auditors discovered that the

ending inventory in the previous period was

understated $15,000 and that the ending

inventory in the current period was

overstated $25,000.

*Ex. 221

Condensed income statements for Swift Corporation are shown below for two years.

2013 2014

Sales $75,000 $90,000

Cost of Goods Sold 45,000 54,000

Gross Profit $30,000 $36,000

Operating Expense 15,000 15,000

Net Income $15,000 $21,000

Compute the corrected net income for 2013 and 2014 assuming that the inventory as of the end

of 2013 was mistakenly understated by $7,000.

2013 $ __________ 2014 $__________