Multiple Choice Test Bank Questions No Feedback – Chapter 6

Correct answers denoted by an asterisk.

1. Consider the following model estimated for a time series

yt = 0.3 + 0.5 yt-1 – 0.4

t-1 +

t

where

t is a zero mean error process.

What is the (unconditional) mean of the series, yt ?

2. Consider the following single exponential smoothing model:

St =

Xt + (1–

) St-1

You are given the following data:

ˆ

=0.1, Xt=0.5,St-1=0.2

If we believe that the true DGP can be approximated by the exponential smoothing

model, what would be an appropriate 2-step ahead forecast for X? (i.e. a forecast of Xt+2

made at time t)

3. Consider the following MA(3) process.

yt = 0.1 + 0.4ut-1 + 0.2ut-2 – 0.1ut-3 + ut

What is the optimal forecast for yt, 3 steps into the future (i.e. for time t+2 if all

information until time t-1 is available), if you have the following data?

ut-1 = 0.3; ut-2 = -0.6; ut-3 = -0.3

4. Which of the following sets of characteristics would usually best describe an

autoregressive process of order 3 (i.e. an AR(3))?

5. A process, xt, which has a constant mean and variance, and zero autocovariance for all

non-zero lags is best described as

6. Which of the following conditions must hold for the autoregressive part of an ARMA

model to be stationary?

7. Which of the following statements are true concerning time-series forecasting?

(i) All time-series forecasting methods are essentially extrapolative.

(ii) Forecasting models are prone to perform poorly following a structural break in a

series.

(iii) Forecasting accuracy often declines with prediction horizon.

(iv) The mean squared errors of forecasts are usually very highly correlated with the

profitability of employing those forecasts in a trading strategy.

8. If a series, yt, follows a random walk (with no drift), what is the optimal 1-step ahead

forecast for y?

9. Consider a series that follows an MA(1) with zero mean and a moving average

coefficient of 0.4. What is the value of the autocorrelation function at lag 1?

10. Which of the following statements are true?

(i) An MA(q) can be expressed as an AR(infinity) if it is invertible

(ii) An AR(p) can be written as an MA(infinity) if it is stationary

(iii) The (unconditional) mean of an ARMA process will depend only on the intercept

and on the AR coefficients and not on the MA coefficients

(iv) A random walk series will have zero pacf except at lag 1

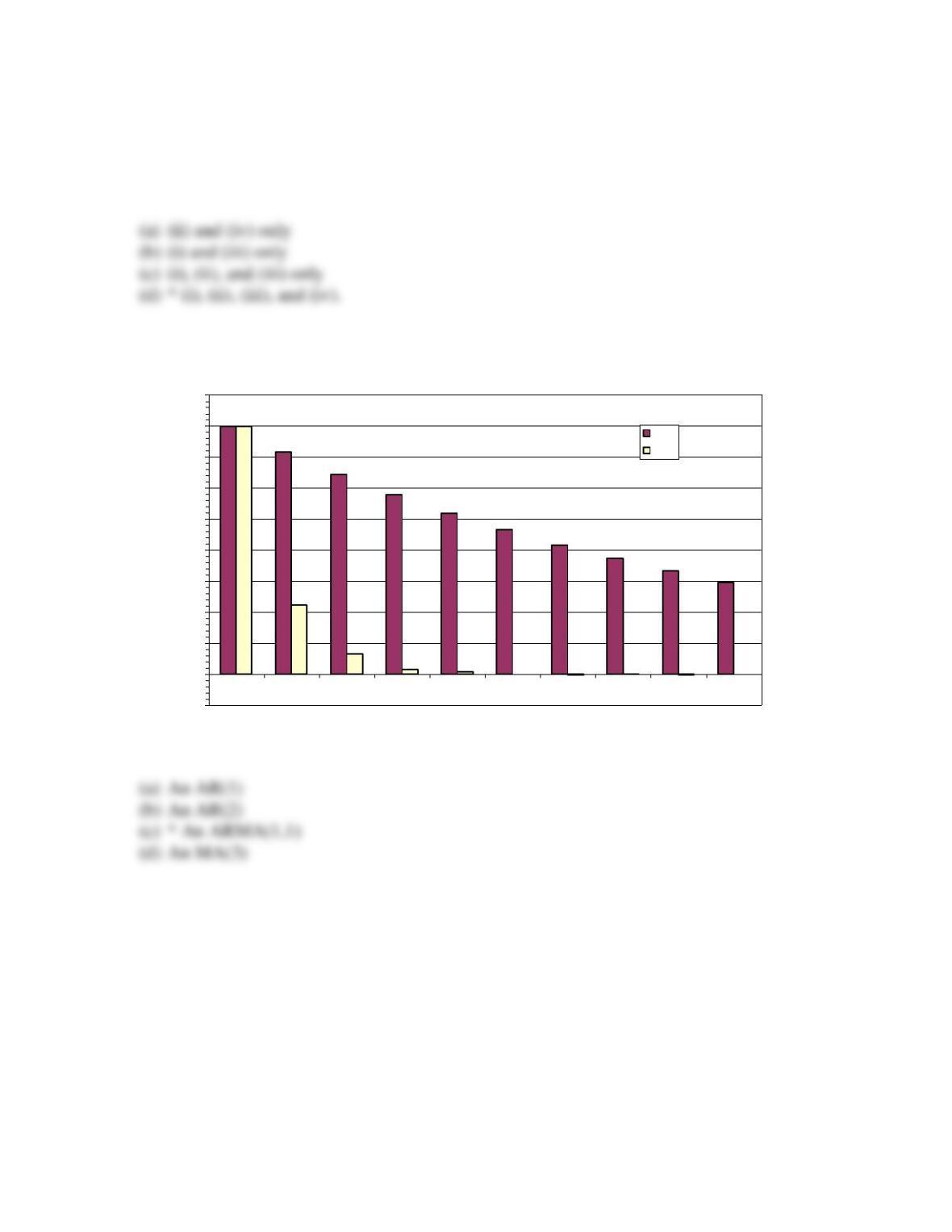

11. Consider the following picture and suggest the model from the following list that best

characterises the process:

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1 2 3 4 5 6 7 8 9 10

Lags

acf and pacf

acf

pacf

The acf is clearly declining very slowly in this case, which is consistent with their being

an autoregressive part to the appropriate model. The pacf is clearly significant for lags

one and two, but the question is does it them become insignificant for lags 2 and 4,

indicating an AR(2) process, or does it remain significant, which would be more

consistent with a mixed ARMA process? Well, given the huge size of the sample that

gave rise to this acf and pacf, even a pacf value of 0.001 would still be statistically

significant. Thus an ARMA process is the most likely candidate, although note that it

would not be possible to tell from the acf and pacf which model from the ARMA family

was more appropriate. The DGP for the data that generated this plot was y_t = 0.9 y_(t-1)

– 0.3 u_(t-1) + u_t.

12. Which of the following models can be estimated using ordinary least squares?

(i) An AR(1)

(ii) An ARMA(2,0)

(iii) An MA(1)

(iv) An ARMA(1,1)

13. If a series, y, is described as “mean–reverting”, which model from the following list is

likely to produce the best long-term forecasts for that series y?

14. Consider the following AR(2) model. What is the optimal 2-step ahead forecast for y

if all information available is up to and including time t, if the values of y at time t, t-1

and t-2 are –0.3, 0.4 and –0.1 respectively, and the value of u at time t-1 is 0.3?

yt = -0.1 + 0.75yt-1 – 0.125yt-2 + ut

15. What is the optimal three-step ahead forecast from the AR(2) model given in question

14?

16. Suppose you had to guess at the most likely value of a one hundred step-ahead

forecast for the AR(2) model given in question 14 – what would your forecast be?

17. Which of these is not a consequence of working with non-stationarity variables?

18. Three characteristics of a weakly stationary process are

(I)

( )

t

Ey

=

(II)

( )( )

2

tt

E y y

− − =

(III)

( )( )

1 2 2 1t t t t

E y y

−

− − =

12

,tt

What do the mathematical expressions I, II and III imply?

Use the following to answer questions 19 and 20. Suppose that you have estimated the

first five autocorrelation coefficients using a series of length 81 observations and found

them to be

Lag 1 2 3 4 5

Autocorrelation coefficient 0.412 -0.205 -0.332 0.005 0.543

19. Which autocorrelation coefficients are significantly different from zero at the 5%

level?

20. What is the appropriate Box-Pierce test statistic?

21. Consider the following MA(2) process

1 1 2 2t t t t

y u u u

−−

= + +

where the errors follow

a standard normal distribution. What is the variance of

t

y

?

22. A model where the current value of a variable depends upon only the values that the

variable took in previous periods plus an error term is called

23. Is the following process

3 2.75 0.75

y y y y u

= − + +

stationary?

24. What type of a process is

1 1 2 2 1 1 2 2

… …

t t t t p t p t t q t q t

y u y y y u u u u

− − − − − −

= + + + + + + + + +

?

25. Which of these is an appropriate way to determine the order of an ARMA model

required to capture the dynamic features of a given data?

26. A recursive forecasting framework is one where

27. A rolling window forecasting framework is one where

Use the following to answer questions 28 to 30.

A researcher is interested in forecasting the house price index in Country Z. The observed

price index values from 1996 to 2000 are 101, 103 104, 107 and 111. The researcher uses

two different forecasting models, A and B. The forecasts for the price index using Model

A are 100.5, 102.4, 103.2, 106 and 111 whilst the forecast using Model B are 100.8,

102.2, 104, 104.2 and 112.1.

28. What are the closest to the mean squared errors for model A and B’s forecasts?

29. What are the closest to the mean absolute errors from models A and B?

30. Based on the MAE and MSE forecast evaluation metrics, which of these statements

are true?