23) On January 1, 2011, Tiler Company purchased equipment that cost $30,000. The equipment

has an estimated useful life of 6 years and an estimated salvage value of $3,000.

Required:

1. Using the straight-line method, complete the chart below:

Year

Depreciation expense for the year

ended Dec. 31

Book value at Dec. 31

2011

$

$

2012

$

$

2013

$

$

2. Explain why long-term assets must be depreciated.

3. Explain why land is NOT depreciated while assets such as equipment are depreciated.

Answer:

2011

2012

2013

24) Describe the impact on the financial statements of buying a piece of factory equipment for

cash, using it, and then selling it for cash.

On the balance sheet:

On the income statement:

On the statement of cash flows:

25) A client has asked you to review the following situations related to long-term assets:

a. Ana, an inexperienced accountant, has calculated depreciation expense of $14,000 for the year

ended December 31, 2009, on an asset that was acquired on March 1, 2009. The asset cost

$150,000, has an estimated salvage value of $10,000 and a 10-year estimated useful life. Ana

used the straight-line method to depreciate the asset.

b. Ana also calculated depreciation expense of $2,000 on a patent that has a historical cost of

$5,000 and a 5-year estimated useful life. The patent has been used all year.

c. A client asked Ana if he could use the double-declining balance method to depreciate assets

for the external financial statements. Ana said, “No,” because she is pretty sure that the double–

declining balance method applies only to tax reporting.

d. Ana determined that the cost of equipment purchased in January was $18,000. The equipment

had an invoice price of $11,000, $1,500 of shipping charges, $1,000 of installation costs, and

$1,500 of testing, moving, and handling costs. During the first month the equipment was owned,

it used $2,000 of power and required a $1,000 tune-up to keep it running. Ana entered $18,000

as the original cost of the equipment.

e. Ana calculated a $4,000 gain on an asset that was sold on the last day of the year. The asset

had an original cost of $120,000, an estimated useful life of 8 years and a $10,000 salvage value.

The asset was depreciated using the straight-line method and had been owned for 6 full years.

The asset was sold for $30,000 cash.

Required: For each of these items, decide if the accounting treatment described is correct or

not.

If the treatment is correct, write “Correct”. If the current treatment is incorrect, provide the

correct answer.

26) On February 1, 2011, Delta Distribution Company purchased a delivery truck that cost

$30,000. The truck has an estimated useful life of 150,000 miles and an estimated salvage value

of $3,000. The truck is driven 10,000; 34,000; and 28,000 miles for the years 2011, 2012, and

2013, respectively.

Required:

1. Calculate the depreciation expense per mile using the activity (units-of-production) method.

2. Use the activity method to complete the chart below:

Year

Miles

driven

Depreciation expense

for the year ended Dec.

31

Book value at Dec. 31

2011

10,000

$

$

2012

34,000

$

$

2013

28,000

$

$

3. Explain why long-term assets must be depreciated, rather than recorded as expenses in the

period when the asset is purchased.

4. Explain why land is NOT depreciated when other assets, such as trucks, are depreciated.

$0.18

$0.18

$0.18

27) On January 1, 2011, Gamma Company purchased equipment that cost $30,000. The

equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000.

Required:

1. Use the double-declining balance method to complete the chart below:

Year

Depreciation expense for the year

ended Dec. 31

Book value at Dec. 31

2011

$

$

2012

$

$

2013

$

$

2. Explain why long-term assets must be depreciated.

3. Explain why land is NOT depreciated when assets like equipment are.

Year

2011

2012

2013

28) Indicate which financial statement would report the items listed in the table below.

Use the following code:

IS = Income statement

SE = Statement of changes in shareholders’ equity

BS = Balance sheet

CF = Statement of cash flows

NONE = The item does not appear on any financial statement.

Depreciation expense

Cash paid to purchase equipment

Accumulated depreciation

Cash received from selling land

Equipment book value

Cash paid to purchase a building

Cash paid to purchase new

computers

Cash received from selling 3-year

machinery

An asset’s estimated useful life

An asset’s estimated residual value

Cash paid to purchase land

Amortization expense

Depreciation expense

Cash paid to purchase equipment

Accumulated depreciation

Cash received from selling land

Equipment book value

Cash paid to purchase a building

computers

old machinery

life

An asset’s estimated residual value

Cash paid to purchase land

Amortization expense

29) Indicate which financial statement would report the items listed in the table below.

Use the following code:

IS = Income statement

SE = Statement of changes in shareholders’ equity

BS = Balance sheet

CF = Statement of cash flows

NONE = The item does not appear on any financial statement.

Accumulated depreciation

Cash paid to purchase machinery

Cash received from selling an

old building

The current fair market value of land

owned

Cash received from selling

10-year old machinery

Cash paid to purchase a building

The historical cost of

equipment owned

Depreciation expense

The amount of revenue a

specific asset generates

Cash paid to purchase office

furniture

Cash paid to buy other

businesses

Accumulated depreciation

Cash paid to purchase machinery

old building

owned

Cash received from selling

10-year old machinery

Cash paid to purchase a building

The historical cost of

equipment owned

Depreciation expense

The amount of revenue a

specific asset generates

Cash paid to purchase office

furniture

Cash paid to buy other

businesses

30) Robin Blind, Inc. recorded the following entries during the year. Put an X in the appropriate

box to indicate whether each entry caused net income and total assets to be overstated,

understated, or correctly stated.

1. Recorded depreciation for the year using $0 salvage value when the salvage value was

expected to be $5,000.

Overstated

Understated

Correctly stated

Net income

Total assets

2. Depreciated its airplanes over a life of 35 years, which is 10 years longer than the average life

of airplanes.

Overstated

Understated

Correctly stated

Net income

Total assets

3. Recorded ordinary repairs as capital expenditures.

Overstated

Understated

Correctly stated

Net income

Total assets

4. Recorded the purchase of patents as an expense. The purchase should have been capitalized.

Overstated

Understated

Correctly stated

Net income

Total assets

5. Recorded its research and development costs as expenses.

Overstated

Understated

Correctly stated

Net income

Total assets

Overstated

Understated

Correctly stated

Net income

Total assets

Overstated

Understated

Correctly stated

Net income

Total assets

31) KenCo bought a new packaging machine on September 15. By October 1, the machine had

been installed, all the employees had been trained to use it, and it was in full operational use. The

factory manager told the accountant: “I know the machine is running the way we hoped it would.

But I want you to capitalize all of the machine’s operating expenses through our December 31

yearend.”

Required:

1. What would be the effect on the company’s income statement and balance sheet for the

current year if three months of operating expenses are capitalized? Why would the company

manager want to do this?

2. Is it ethical to capitalize costs that should be expensed?

32) A client has asked you to review and correct the following income statement:

Ted Williams Construction

Income Statement

For the Year Ended October 31, 2011

Revenues $900,000

Expenses

Rent $120,000

Utilities 180,000

Equipment expense 120,000

Salaries 220,000

Depreciation 100,000

Total expenses 740,000

Net income $160,000

Additional information:

a. A $3,500 machine tune-up was recorded as an asset.

b. The costs of buying a $120,000 piece of equipment on the last day of the fiscal year were

treated as equipment expense.

c. An asset with a cost of $230,000, a 10-year useful life, and a zero salvage value was

depreciated $23,000 for the full year.

d. The power and electricity costs of running a machine were treated as an expense for the year.

The costs amounted to $56,000.

e. The costs of insuring a piece of equipment while it was in transit amounted to $5,000, and

those costs were capitalized.

Required:

1. List any errors that you find.

2. Correct the errors and prepare another income statement.

33) A client has asked you to review and correct the following income statement.

CD Manufacturing

Income Statement

For the Year Ended September 30, 2011

Revenues $800,000

Expenses

Rent $100,000

Utilities 50,000

Equipment expense 90,000

Salaries 200,000

Depreciation 100,000

Total expenses 540,000

Net income $260,000

Additional information:

a. A $5,500 machine tune-up was recorded as an asset.

b. The costs of buying a $90,000 piece of equipment on the last day of the fiscal year were

treated as equipment expense.

c. An asset with a cost of $230,000, an estimated useful life of ten years, and a $20,000 salvage

value was depreciated $23,000 for the full year.

d. The power and electricity costs of running a machine were treated as an asset for the year. The

costs amounted to $16,000.

e. The $10,000 costs of installing the factory equipment in part b were treated as part of Rent

expense.

Required:

1. List as many errors as you can find.

2. Prepare a correct income statement.

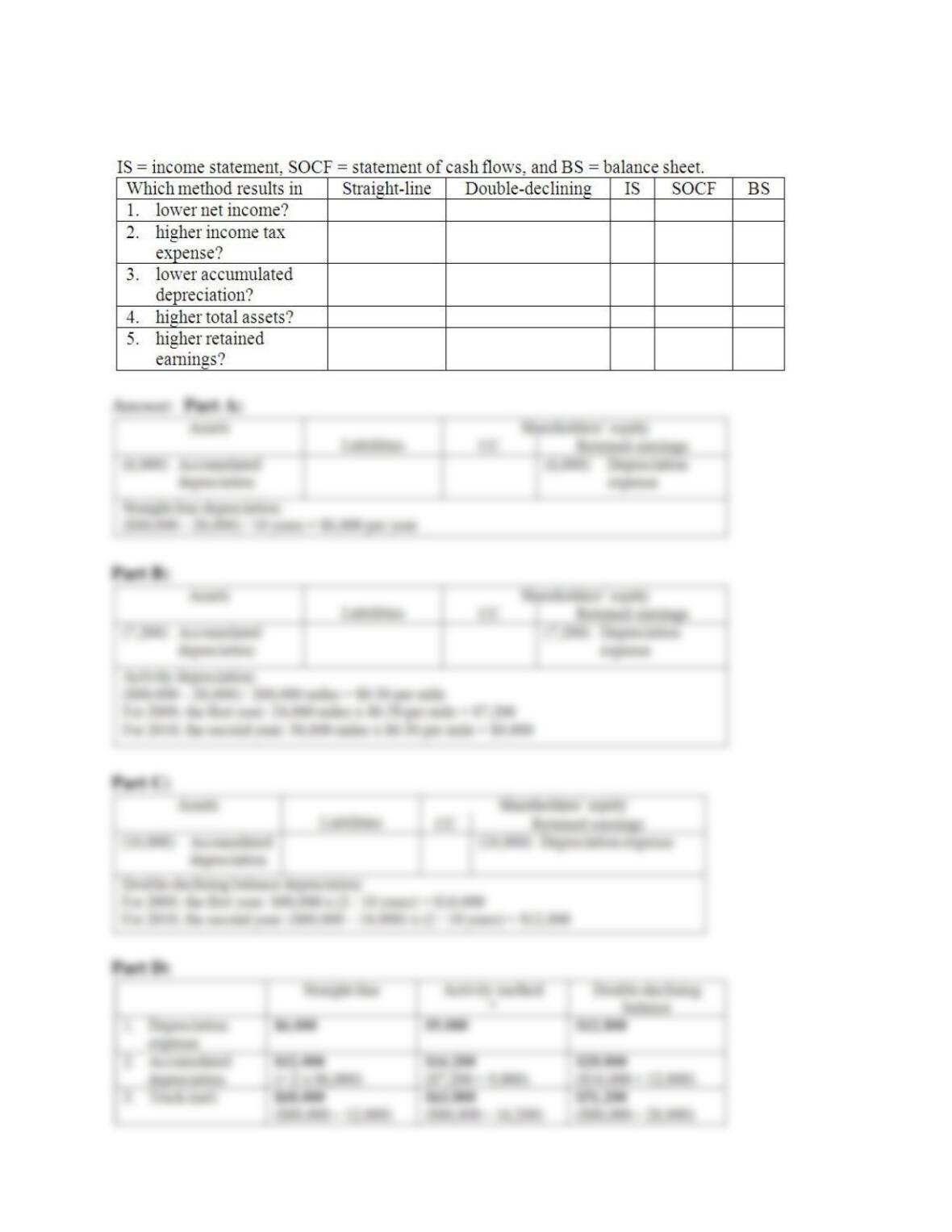

34) On January 1, 2011, Keep Trucking, Inc. purchased a truck for $80,000 that has an estimated

useful life of 10 years or 200,000 miles and a salvage value of $20,000. The truck was driven

24,000 miles in 2011 and 30,000 miles in 2012. Write in both the correct dollar amounts and the

account titles involved.

Part A: Show the effect of the adjusting entry for the FIRST YEAR of depreciation using the

straight-line depreciation method.

Part B: Show the effect of the adjusting entry for the FIRST YEAR of depreciation using the

activity method.

Part C: Show the effect of the adjusting entry for the FIRST YEAR of depreciation using the

double-declining balance method.

Part D: Show the amounts that would appear on the annual financial statements for December

31, 2012 (the SECOND YEAR) for each method. PUT AN ASTERISK(*) BY THE

METHOD THAT BEST REPRESENTS THE ACTUAL USE OF THE TRUCK.

Part E: For the first two years of the equipment’s life determine which method gives the dollar

amount described AND indicate the financial statement where the information would be found.

35) During 2011, Rob M. Clean Company recorded the following business events. For each,

determine whether the accounting treatment was correct, and show the effect of any errors on the

accounting equation.

Rob M. Clean:

Assets

Liabilities

Shareholders’ equity

CC

Retained earnings

1. recorded $5,000

of advertisements

run in 2009 as

expenses

___ overstated

___understated

___correctly stated

___ overstated

___understated

___correctly stated

___ overstated

___understated

___correctly stated

2. recorded $4,000

of installation costs

for new equipment

as an expense

___ overstated

___understated

___correctly stated

___ overstated

___understated

___correctly stated

___ overstated

___understated

___correctly stated

3. depreciates its

building over 20

years rather than 5

years, which is the

building’s estimated

useful life given the

company’s growth

___ overstated

___understated

___correctly stated

___ overstated

___understated

___correctly stated

___ overstated

___understated

___correctly stated

Assets

Liabilities

Shareholders’ equity

1

correctly stated

correctly stated

correctly stated

2

understated

correctly stated

understated

3

overstated

correctly stated

overstated

36) On January 1, 2011. Hula Hoops, Inc. purchased a $40,000 machine for cash. The company

uses straight-line depreciation, an estimated useful life of 5 years, and a $2,000 salvage value.

Treat each of the following scenarios independently. For each, write in the amount in the column

that represents the one financial statement where the amount is found. Round your answers to the

nearest whole dollar. The company’s yearend is December 31.

Part A: On December 31, 2011, the company was told by an appraiser that the machine is in

such great condition it could be sold for $38,000.

As of or for the

year ended 2011:

Income

Statement

Statement of

Cash Flows

Balance

Sheet

1. Depreciation expense

2. Accumulated depreciation

3. Equipment (net)

4. Purchase of equipment

Part B: In December 2012, the company decided that the machine’s original estimated useful

life of 5 years should be revised to a total of 8 years since the machine is in such good condition.

Salvage value is still $2,000.

As of or for the

year ended 2012:

Income

Statement

Statement of

Cash Flows

Balance

Sheet

1. Depreciation expense

2. Accumulated depreciation

3. Equipment (net)

37) On January 1, 2011, Crunch Company paid $100,000 for equipment with an estimated useful

Statement of

Cash Flows

Balance

Sheet

1. Depreciation expense

2. Accumulated depreciation

3. Equipment (net)

4. Purchase of equipment

Depreciation expense: ($40,000 — 2,000) / 5 years = $7,600Equipment (net):

$40,000 — 7,600 = $32,400

1. Depreciation expense

2. Accumulated depreciation

3. Equipment (net)

life of 5 years and no residual value.

Part A: Calculate the financial statement amounts using each of the depreciation methods

below:

2011 financial statement line items:

Straight-line

Double-declining balance

1. Depreciation expense

$

$

2. Accumulated depreciation

$

$

3. Equipment (net of accumulated

depreciation)

$

$

2012 financial statement line items:

Straight-line

Double-declining balance

4. Depreciation expense

$

$

5. Accumulated depreciation

$

$

6. Equipment (net of accumulated

depreciation)

$

$

Part B:

1. On January 1, 2013, Crunch Company sold the equipment for $62,000 cash. Assume straight-

line depreciation was used. For each financial statement line item, write in the correct amount in

the column that represents the financial statement where the information is found:

2013 financial statement line items:

Income

Statement

Statement of

Cash Flows

Balance Sheet

a. Proceeds from sale of equipment

b. Gain (loss) from sale of equipment

2. Show the effect if the truck had been sold for $45,000 cash.

2013 financial statement line item:

Straight-line

Double-declining balance

Gain (loss) from sale of equipment

$

$