51.

Forecasting Interest Rates Assume the current interest rate on a one-year Treasury bond

(1

R

1) is 5.00 percent, the current rate on a two-year Treasury bond (1

R

2) is 5.75 percent, and

the current rate on a three-year Treasury bond (1

R

3) is 6.25 percent. If the unbiased

expectations theory of the term structure of interest rates is correct, what is the one-year

interest rate expected on Treasury bills during year 3, 3

f

1?

52.

Forecasting Interest Rates A recent edition of

The Wall Street Journal

reported interest

rates of 3.10 percent, 3.50 percent, 3.75 percent, and 3.95 percent for three-year, four-year,

five-year, and six-year Treasury security yields, respectively, According to the unbiased

expectation theory of the term structure of interest rates, what are the expected one-year

rates for year 6?

53.

A particular security’s default risk premium is 3 percent. For all securities, the inflation risk

premium is 1.75 percent and the real interest rate is 4.2 percent. The security’s liquidity risk

premium is 0.35 percent and maturity risk premium is 0.95 percent. The security has no

special covenants. Calculate the security’s equilibrium rate of return.

54.

You are considering an investment in 30-year bonds issued by Moore Corporation. The bonds

have no special covenants.

The Wall Street Journal

reports that one-year T-bills are currently

earning 3.55 percent. Your broker has determined the following information about economic

activity and Moore Corporation bonds:

Real interest rate = 2.75 percent

Default risk premium = 1.05 percent

Liquidity risk premium = 0.50 percent

Maturity risk premium = 1.85 percent

What is the inflation premium?

55.

You are considering an investment in 30-year bonds issued by Moore Corporation. The bonds

have no special covenants.

The Wall Street Journal

reports that one-year T-bills are currently

earning 3.55 percent. Your broker has determined the following information about economic

activity and Moore Corporation bonds:

Real interest rate = 2.75 percent

Default risk premium = 1.05 percent

Liquidity risk premium = 0.50 percent

Maturity risk premium = 1.85 percent

What is the fair interest rate on Moore Corporation 30-year bonds?

56.

Dakota Corporation 15-year bonds have an equilibrium rate of return of 9 percent. For all

securities, the inflation risk premium is 1.95 percent and the real interest rate is 3.65 percent.

The security’s liquidity risk premium is 0.35 percent and maturity risk premium is 0.95

percent. The security has no special covenants. Calculate the bond’s default risk premium.

57.

A two-year Treasury security currently earns 5.13 percent. Over the next two years, the real

interest rate is expected to be 2.15 percent per year and the inflation premium is expected to

be 1.75 percent per year. Calculate the maturity risk premium on the two-year Treasury

security.

58.

Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill

rates over the following three years (i.e., years 2, 3 and 4, respectively) are as follows:

1R1 = 5 percent, E(2r1) = 7 percent, E(3r1) = 7.5 percent E(4r1) = 7.85 percent

Using the unbiased expectations theory, calculate the current (long-term) rates for one-year

and two-year –maturity Treasury securities.

59.

Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill

rates over the following three years (i.e., years 2, 3 and 4 respectively) are as follows:

1R1 = 5 percent, E(2r1) = 6 percent, E(3r1) = 7.5 percent E(4r1) = 7.85 percent

Using the unbiased expectations theory, calculate the current (long-term) rates for three-

year- and four-year-maturity Treasury securities.

60.

Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill

rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows:

1R1 = 5 percent, E(2r1) = 6 percent, E(3r1) = 7.5 percent E(4r1) = 6.85 percent

Using the unbiased expectations theory, calculate the current (long-term) rates for one-, two–

, three-, and four-year-maturity Treasury securities.

61.

One-year Treasury bills currently earn 3.75 percent. You expect that one year from now, one–

year Treasury bill rates will increase to 4.15 percent. If the unbiased expectations theory is

correct, what should the current rate be on two-year Treasury securities?

62.

One-year Treasury bills currently earn 4.5 percent. You expect that one year from now, one-

year Treasury bill rates will increase to 6.65 percent. The liquidity premium on two-year

securities is 0.05 percent. If the liquidity theory is correct, what should the current rate be on

two-year Treasury securities?

63.

Based on economists’ forecasts and analysis, one-year Treasury bill rates and liquidity

premiums for the next four years are expected to be as follows:

R1 = 5.95 percent

E(r2) = 6.25 percent L2 = 0.05 percent

E(r3) = 6.75 percent L3 = 0.10 percent

E(r4) = 7.15 percent L4 = 0.12 percent

Using the liquidity premium hypothesis, what should be the current rate on four-year

Treasury securities?

64.

The Wall Street Journal

reports that the rate on three-year Treasury securities is 7.00

percent, and the six-year Treasury rate is 6.20 percent. From discussions with your broker,

you have determined that expected inflation premium is 2.25 percent next year, 2.50 percent

in Year 2, and 2.50 percent in Year 3 and beyond. Further, you expect that real interest rates

will be 4.4 percent annually for the foreseeable future. Calculate the maturity risk premium on

the 3-year Treasury security.

65.

The Wall Street Journal

reports that the rate on three-year Treasury securities is 6.50

percent, and the six-year Treasury rate is 6.80 percent. From discussions with your broker,

you have determined that expected inflation premium is 2.25 percent next year, 2.50 percent

in Year 2, and 2.60 percent in Year 3 and beyond. Further, you expect that real interest rates

will be 3.4 percent annually for the foreseeable future. Calculate the maturity risk premium on

the three-year and the six-year Treasury security.

66.

Nikki G’s Corporation’s 10-year bonds are currently yielding a return of 9.25 percent. The

expected inflation premium is 2.0 percent annually and the real interest rate is expected to be

3.10 percent annually over the next 10 years. The liquidity risk premium on Nikki G’s bonds is

0.1 percent. The maturity risk premium is 0.10 percent on two-year securities and increases

by 0.05 percent for each additional year to maturity. Calculate the default risk premium on

Nikki G’s 10-year bonds.

67.

Suppose we observe the following rates: 1R1 = 12 percent, 1R2 = 15 percent. If the unbiased

expectations theory of the term structure of interest rates holds, what is the one-year interest

rate expected one year from now, E(2r1)?

68.

The Wall Street Journal

reports that the rate on four-year Treasury securities is 7.50 percent

and the rate on five-year Treasury securities is 9.15 percent. According to the unbiased

expectations hypotheses, what does the market expect the one-year Treasury rate to be four

years from today, E(5r1)?

69.

The Wall Street Journal

reports that the rate on three-year Treasury securities is 7.25 percent

and the rate on four-year Treasury securities is 8.50 percent. The one-year interest rate

expected in three years is E(4r1), 4.10 percent. According to the liquidity premium hypotheses,

what is the liquidity premium on the four-year Treasury security, L4?

70.

Suppose we observe the following rates: 1R1 = 13 percent, 1R2 = 16 percent, and E(2r1) = 10

percent. If the liquidity premium theory of the term structure of interest rates holds, what is

the liquidity premium for year 2, L2?

71.

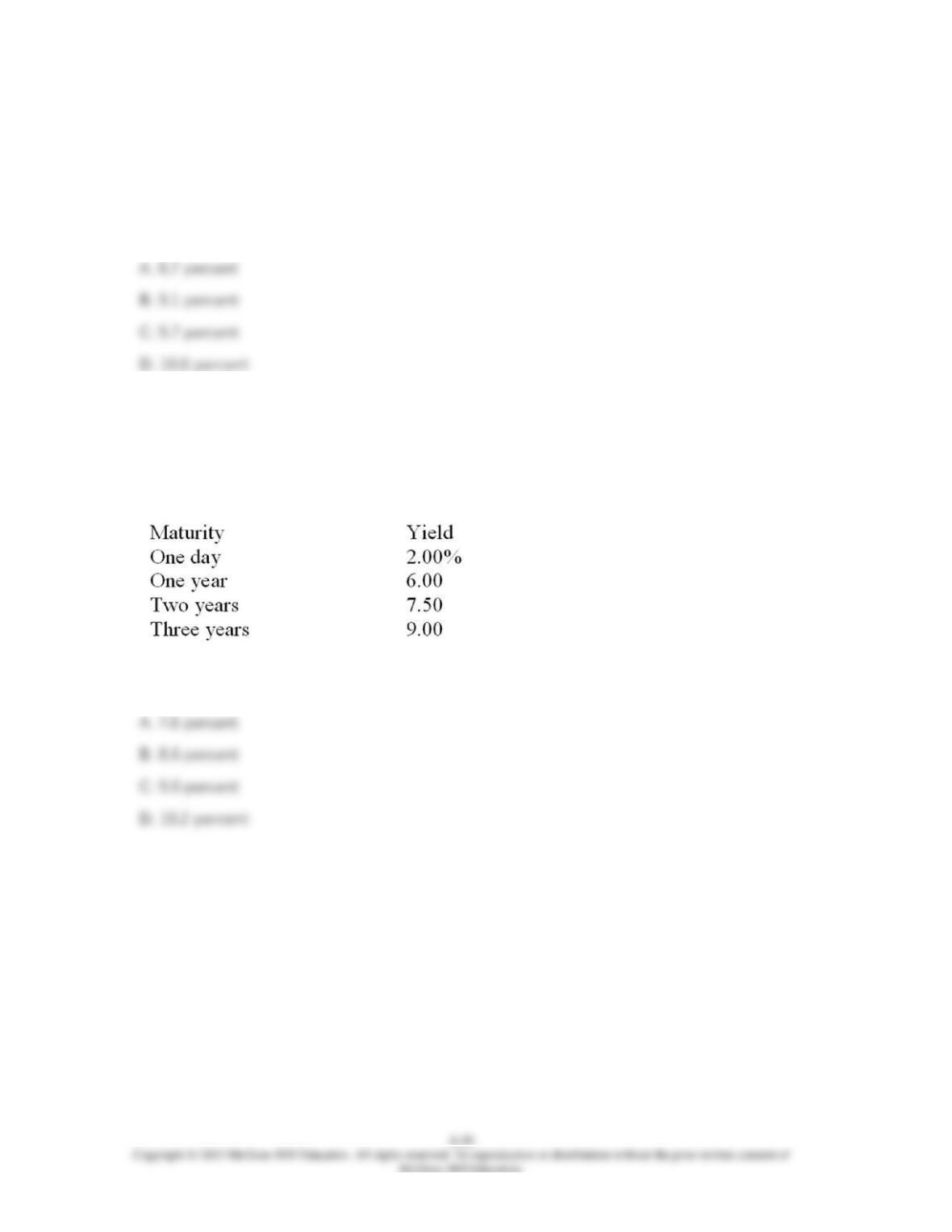

You note the following yield curve in

The Wall Street Journal.

According to the unbiased

expectations hypothesis, what is the one-year forward rate for the period beginning one year

from today, 2f1?

72.

On May 23, 20XX, the existing or current (spot) one–year, two-year, three-year, and four-year

zero-coupon Treasury security rates were as follows:

1R1 = 4.55 percent, 1R2 = 4.75 percent, 1R3 = 5.25 percent, 1R4 = 5.95 percent

Using the unbiased expectations theory, calculate the one-year forward rates on zero-coupon

Treasury bonds for years two, three, and four as of May 23, 20XX.

73.

The Wall Street Journal

reports that the current rate on 10-year Treasury bonds is 6.25

percent, on 20-year Treasury bonds is 7.95 percent, and on a 20-year corporate bond is 10.75

percent. Assume that the maturity risk premium is zero. If the default risk premium and

liquidity risk premium on a 10-year corporate bond is the same as that on the 20-year

corporate bond, calculate the current rate on a 10-year corporate bond.

74.

The Wall Street Journal

reports that the current rate on five-year Treasury bonds is 6.45

percent and on 10-year Treasury bonds is 7.75 percent. Assume that the maturity risk

premium is zero. Calculate the expected rate on a five-year Treasury bond purchased five

years from today, E(5r5).

75.

Suppose we observe the three-year Treasury security rate (1R3) to be 11 percent, the

expected one-year rate next year E(2r1) to be 4 percent, and the expected one-year rate the

following year E(3r1) to be 5 percent. If the unbiased expectations theory of the term structure

of interest rates holds, what is the one-year Treasury security rate, 1R1?

76.

Assume the current interest rate on a one-year Treasury bond (1R1) is 5.50 percent, the

current rate on a two-year Treasury bond (1R2) is 5.95 percent, and the current rate on a

three-year Treasury bond (1R3) is 8.50 percent. If the unbiased expectations theory of the

term structure of interest rates is correct, what is the one-year interest rate expected on

Treasury bills during year 3, 3f1?

77.

If the yield curve is downward sloping, what is the yield to maturity on a 30-year Treasury

bond relative to a 10-year Treasury bond?

78.

One-year Treasury bill rates in 20XX averaged 5.15 percent and inflation for the year was 7.3

percent. If investors had expected the same inflation rate as that realized, calculate the real

interest rate for 20XX according to the Fisher effect.

79.

Assume that you observe the following rates on long-term bonds:

U.S. Treasury bonds = 4.15 percent

AAA Corporate bonds = 6.2 percent

BBB Corporate bonds = 7.15 percent

The main reason for the differences in the interest rates is:

80.

Which of the following statements is correct?

81.

One-year interest rates are 3 percent. The market expects one-year rates to be 5 percent one

year from now. The market also expects one-year rates to be 7 percent two years from now.

Assume that the unbiased expectations theory holds. Which of the following is correct?

82.

Which of the following statements is correct?

83.

The Wall Street Journal

states that the yield curve for Treasuries is downward sloping and

there is no liquidity premium or maturity risk premium. Given this information, which of the

following statements is correct?

84.

Which of the following statements is correct?

85.

In 20XX, the 10-year Treasury rate was 4.5 percent while the average 10-year Aaa corporate

bond debt carried an interest rate of 6.0 percent. What is the average default risk premium on

Aaa corporate bonds?

86.

Which of the following statements is correct?

87.

All of the following are types of financial institutions EXCEPT:

88.

All of the following are benefits that financial institutions provide to our economy EXCEPT:

89.

All of the following are factors that affect nominal interest rates EXCEPT:

90.

Which of the following statements is correct?

91.

Which of the following statements is incorrect?

92.

The theory that argues that individual investors and financial institutions have specific

maturity preferences is called the:

93.

The theory that states that the yield curve reflects the market’s current expectations of future

short-term rates is called the:

94.

Which of the following statements is incorrect?

95.

All of the following are secondary market transactions EXCEPT:

96.

Which of the following is NOT correct with respect to derivative securities?

97.

Which of the following is NOT correct with respect to financial institutions?

98.

All of the following are factors that influence interest rates for individual securities EXCEPT:

99.

The real interest rate is:

100.

All of the following special provisions benefit security holders EXCEPT:

101.

An example of an illiquid asset is:

102.

All of the following are common shapes for the yield curve EXCEPT:

103.

Determinants of Interest Rates for Individual Securities

The Wall Street Journal

reports

that the current rate on five-year Treasury bonds is 2.85 percent and on 10-year Treasury

bonds is 4.35 percent. Assume that the maturity risk premium is zero. Calculate the expected

rate on a five-year Treasury bond purchased five years from today, E(5

r

5).