Chapter 5

Answers to Review Problems

Finance For Executives – 4th Edition

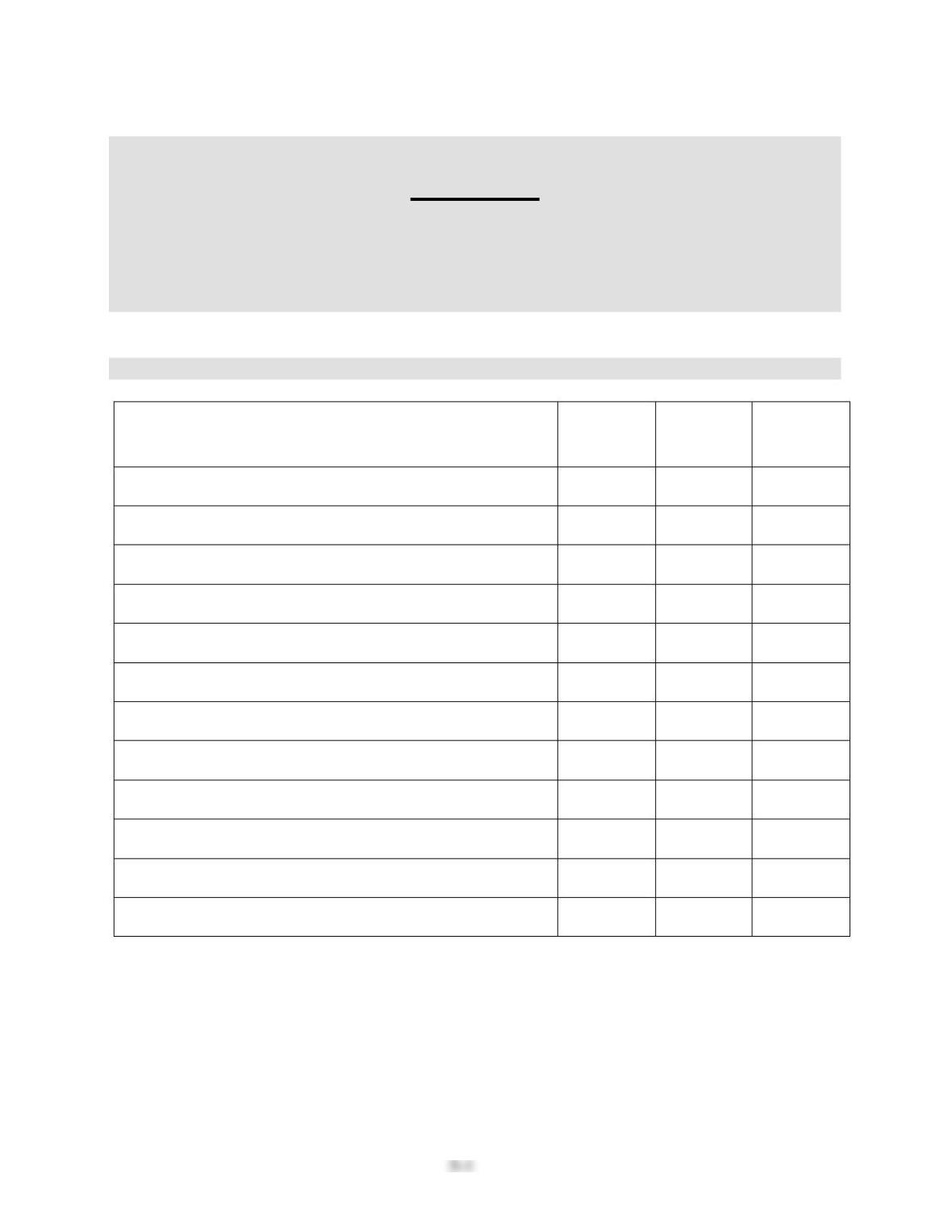

1. Transactions.

Operating

margin

Invested

capital

turnover

Debt

ratio

1. Shares are issued for cash.

0

–

–

2. Goods from inventory are sold for cash at a profit.

+

+

–

3. A fixed asset is sold for cash at its book value.

0

0

0

4. A fixed asset is sold for more than its book value.

0

–

–

5. A dividend is declared and paid.

0

+

+

6. Cash is obtained through a bank loan.

0

–

+

7. Accounts receivable are collected.

0

0

0

8. Minority interest in a firm is acquired for cash.

0

0

0

9. A fixed asset is depreciated.

–

+

+

10. Obsolete inventory is written off.

–

+

+

11. Merchandise is purchased on account.

0

0

0

12. Shares are repurchased.

0

+

+

5-2

2. ROICBT , ROCEBT, RONA, ROBA, and ROTA.

Measure

Definition

Value

ROICBT

EBIT/Invested capital

$24.0/$138.0 = 17.4%

ROCEBT

EBIT/Capital employed

$24.0/$138.0 = 17.4%

RONA

EBIT/Net assets

$24.0/$138.0 = 17.4%

ROBA

EBIT/Business assets

$24.0/($77.0 + $53.0) = 18.5%

ROTA

EBIT/Total assets

$24/$190.0 = 12.6%

3. Book versus market return on equity.

The two ratios are different because the book value is estimated using past data, up to the end of

the accounting period, while the market value is determined by the investors’ expectation

regarding future earnings/cash flows. Further, financial accounting data is very sensitive to the

accounting principles used to estimate it.

4. The structure of a firm profitability.

a. 7.5 percent (.075 × 2 = .15 or 15 percent)

b. The financial structure effect is 1.67 (.10 × .9 × 1.67 = .15 or 15 percent). Since the financial

5-3

5. Misuse of the structure of the return on equity.

a. If the firm decides not to replace existing fixed assets, its invested capital will decrease as the

book value of fixed assets will decrease due to increased accumulated depreciation. Its capital

6. 6. Financial leverage.

When the cost of debt is lower than the return on invested capital before tax: it pays to borrow

when the cost of borrowing is lower than the return expected from the investment made by the

firm. A formal proof is given by equation 5.16 where the difference between ROICBT and the

7. Industry effect on the structure of the return on equity.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

Managerial balance sheets

in millions

Firm 1

Firm 2

Firm 3

Invested capital

Cash

$ 1,856

$ 485

$23,798

Working capital requirement (WCR)

2,105

456

(3,245)

Net fixed assets

45,993

13,816

21,842

Total invested capital

$49,954

$14,757

$42,395

5-4

b.

Operating margin = EBIT/Sales

Invested capital turnover = Sales/Invested capital

Firm 1

Operating margin = $10,105/$166,809 = 6.1% (rounded)

Invested capital turnover = $166,809/$49,954 = 3.34 (rounded)

Firm 2

Operating margin = $1,419/$7,132 = 19.9% (rounded)

Invested capital turnover = $7,132/$14,757 = .48

5-5

Firm 3

Operating margin = $10,937/$22,956 = 47.6%

c.

Firm 1 is in the retail (nongrocery) industry, Firm 2 is a utility firm, and Firm 3 is in the

computer (software industry).

The most striking feature of Firm 1 is its invested capital turnover of 3.34, which means that the

firm generates $3.34 of revenue per dollar of invested capital, while the other two firms generate

only around half a dollar of revenue. Among the three industries to which Firm 1 can belong,

only the retail industry can exhibit such a relatively high invested capital turnover.

5-6

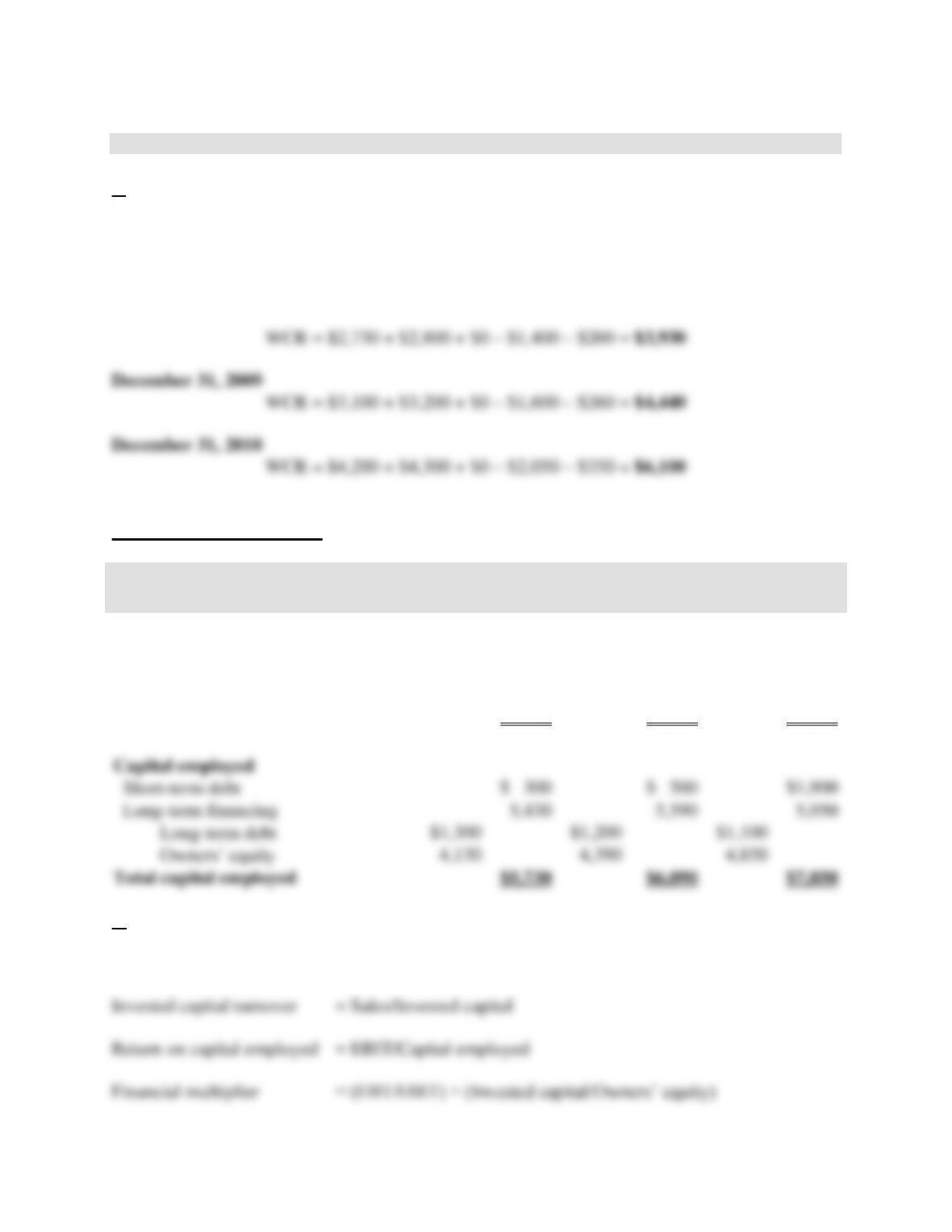

8. The effect of the management of the operating cycle on the firm’s profitability.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

December 31, 2008

Managerial balance sheets

in thousands

December 31,

2008

December 31,

2009

December 31,

2010

Invested capital

Cash

$ 600

$ 350

$ 300

Working capital requirement (WCR)

3,930

4,440

6,100

Net fixed assets

1,200

1,300

1,450

Total invested capital

$5,730

$6,090

$7,850

Capital employed

Short-term debt

$ 300

$ 500

$1,900

Long-term financing

Long-term debt

Owners’ equity

Total capital employed

$5,730

$7,850

b.

Operating margin = EBIT/Sales

5-7

2008

Operating margin = $650/$22,100 = 2.94%

Invested capital turnover = $22,100/$5,730 = 3.86

2009

Operating margin = $900/$24,300 = 3.70%

Invested capital turnover = $24,300/$6,090 = 3.99

2010

Operating margin = $1,350/$31,600 = 4.27%

Invested capital turnover = $31,600/$7,850 = 4.03

5-8

The relationship between these ratios and the firm’s return on equity is that ROE is simply equal

to the product of the operating margin, invested capital turnover, financial multiplier, and tax

effect.

c.

Note the drastic increase of the return on equity which nearly doubles between 2008 and 2010,

from 7.75 percent to 13.61 percent. This change in profitability can be attributed either to the tax

effect, a change in the financial policy or in the return on invested capital.

The return on invested capital (ROIC), which increased drastically from 11.34 percent in 2008 to

17.20 percent in 2010, was the main driver of the increase of the firm’s profitability during that

period. Furthermore, most of the ROIC increase comes from the operating margin which went up

from 2.94 percent in 2008 to 4.27 percent in 2010, while the invested capital turnover increased

only marginally from 3.86 to 4.03 during the same period.

d.

5-9

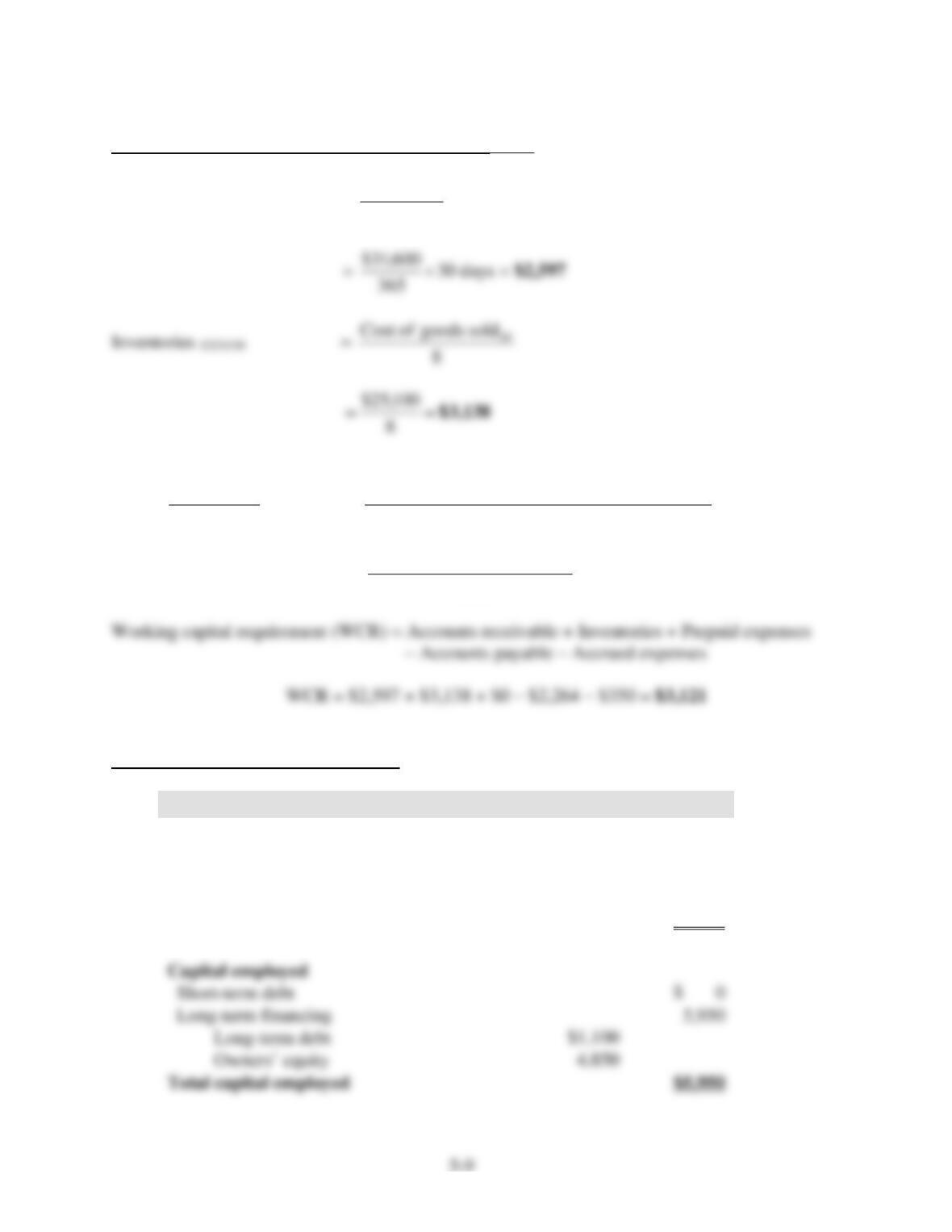

Pro forma working capital requirement (WCR)12/31/10

Accounts receivable12/31/10 =

365

salesNet 10

30 days

Accounts payable12/31/10 =

365

Purchases10

33 days =

+

365

sinventoriein Changesold goods ofCost 1010

33 days

=

−+

365

)200,3$138,3($100,25$

33 days = $2,264

Pro forma managerial balance sheet

in thousands

December 31, 2010

Invested capital

Cash

$ 1,379

Working capital requirement (WCR)

3,121

Net fixed assets

1,450

Total invested capital

$5,950

Capital employed

Short-term debt

Long-term financing

Long-term debt

Owners’ equity

Total capital employed

$5,950

5-10

Note that the amount of long-term financing ($5,950) would have been higher than the

investment in fixed assets and in the operating cycle ($1,450 + $3,121 = $4,571). Sentec Inc.

would not have needed any short-term debt, and had $1,379 million (5,950 – $4,571) in cash.

The structure of the pro forma return on equity

2010

Operating margin

EBIT/Sales

4. 27%

multiplied by

Invested capital turnover

Sales/Invested Capital

5.31

equals

Note the drastic impact of a better management of the operating cycle on the return on invested

capital, which would have jumped from 4.03 to 5.31. As a result, the return on invested capital

would have reached 22.7 percent and the return on equity 16.05 percent, instead of 17.2 percent

and 13.61 percent, respectively. This improvement would have been realized with a financial

multiplier not significantly different from what it was at the end of 2008 (1.18 vs 1.15). In other

9. Seasonal business.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

Return on invested capital

EBIT/Invested capital

multiplied by

multiplied by

Tax effect

EAT/EBT

equals

Return on equity

5-11

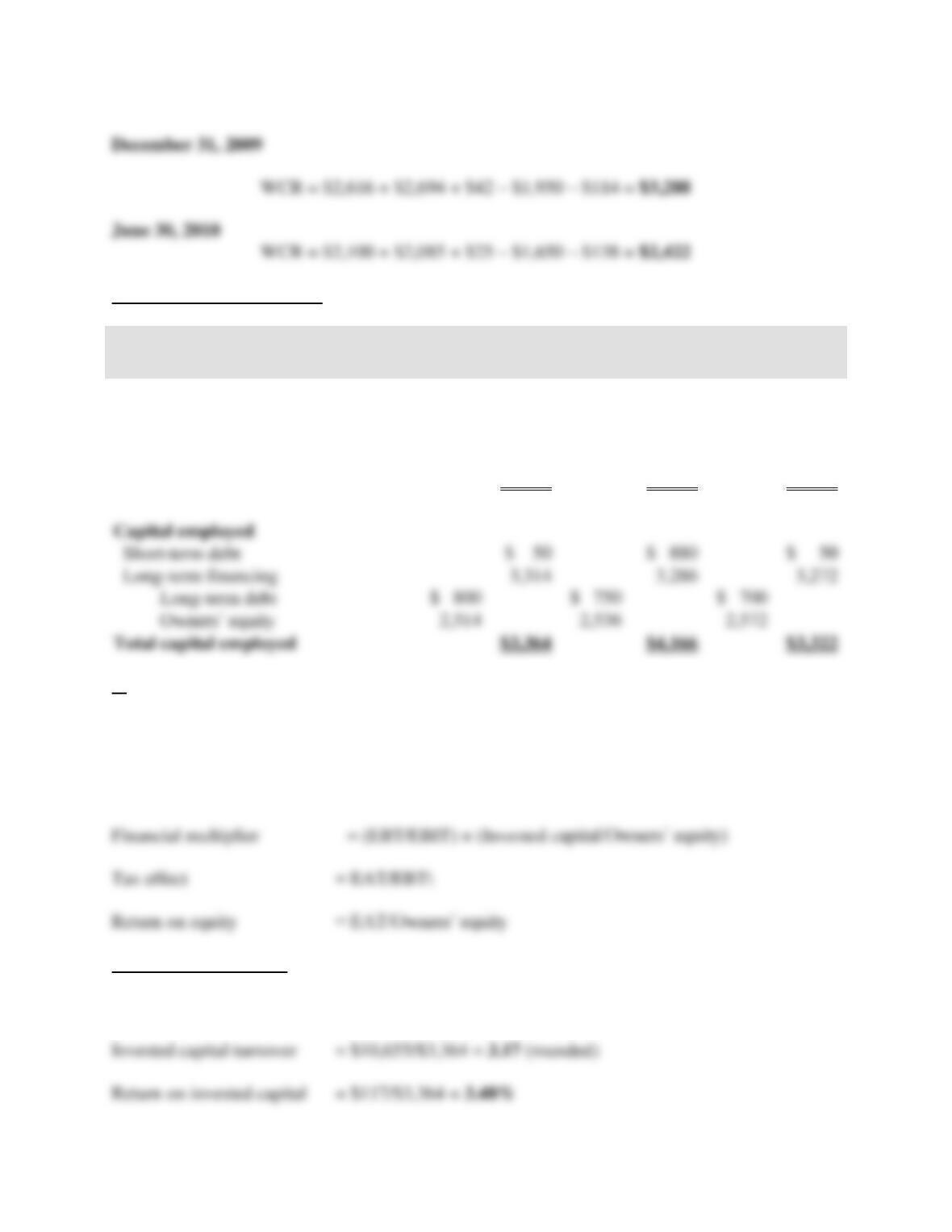

Managerial balance sheets

in thousands

June 30,

2009

December 31,

2009

June 30,

2010

Invested capital

Cash

$ 160

$ 60

$ 70

Working capital requirement (WCR)

2,471

3,288

2,422

Net fixed assets

733

818

830

Total invested capital

$3,364

$4,166

$3,322

Capital employed

Short-term debt

$ 880

$ 50

Long-term financing

Long-term debt

Owners’ equity

Total capital employed

$3,364

$3,322

b.

Operating margin = EBIT/Sales

Invested capital turnover = Sales/Invested capital

Return on invested capital = EBIT/Invested capital

6 Months to 6/30/2009

Operating margin = $117/$10,655 = 1.1% (rounded)

5-12

6 Months to 12/31/2009

Operating margin = $200/$13,851 = 1.4%

Invested capital turnover = $13,851/$4,166 = 3.32

6 Months to 6/30/2010

Operating margin = $133/$11,720 = 1.1%

Invested capital turnover = $11,720/$3,322 = 3.53 (rounded)

c.

Return on equity is higher in the second part of the year than in the first half (2.6 percent versus

1.3/1.4 percent) for the following reasons:

5-13

10. Self-sustainable growth rate.

a.

The five percent target growth rate would be attainable only if the firm’s self-sustainable growth

rate is at least equal to 5 percent. Ambersome’s self-sustainable rate can be computed as follows:

1. Assets turnover ratio

Sales/Total assets

.9

2. Profit margin

Earnings before interest and tax/Sales

8%

3. Return on equity

Earnings after tax/ Owners’ equity [(2) (1-.4) (1)]1

4.32%

4. Payout ratio

Dividends/ Earnings after tax

.4

5. Self-sustainable growth rate

[(3) [1 – (4)]

2.59%

c.

The firm’s return on equity, and as a result, its self-sustainable rate, would increase through debt

financing only if the rate at which the firm can borrow is lower than the return on assets. Since

the interest rate after tax that will be charged to Ambersome is 10 percent, and its return on

assets before tax is 7.2 percent, borrowing will not help in meeting the sales target of 5 percent.