19

Topic: Reducing Risk through Diversification

60. Systematic risk:

a. is the risk eliminated through diversification.

b. represents the risk affecting a specific company.

c. cannot be eliminated through diversification.

d. is another name for risk unique to an individual asset.

61. The Russian wheat crop fails, driving up wheat prices in the U.S. This is an example of:

a. idiosyncratic risk.

b. diversification.

c. systematic risk.

d. quantifiable risk.

62. If the returns of two assets are perfectly positively correlated, an investor who puts half of

his/her savings into each will:

a. reduce risk.

b. have a higher expected return.

c. not gain from diversification.

d. reduce risk but lower the expected return.

63. In order to benefit from diversification, the returns on assets in a portfolio must:

a. be perfectly positively correlated.

b. be perfectly negatively correlated.

c. positively correlated but not perfectly.

d. have the same idiosyncratic risks.

64. The main reason for diversification for an investor is to:

a. take advantage of the fact that returns of assets are perfectly positively correlated.

b. take advantage of the fact that returns on assets are not perfectly correlated.

c. lower transaction costs.

d. gain from the greater returns that come from greater risk.

65. If ABC Inc. and XYZ Inc. have returns that are perfectly positively correlated:

a. adding XYZ Inc to a portfolio that consists of only ABC Inc. will reduce risk.

b. adding ABC Inc to a portfolio that includes only XYZ Inc. will increase risk.

c. adding XYZ Inc. to a portfolio that consists of only ABC Inc. will neither increase nor

decrease the risk of the portfolio.

d. adding XYZ Inc to a portfolio that consists of only ABC Inc. will neither increase nor

decrease idiosyncratic risk but will lower systematic risk.

66. If an investment offered an expected payoff of $100 with $0 variance, you would know that:

a. half of the time the payoff is $100 and the other half it is $0.

b. the payoff is always $100.

c. half of the time the payoff is $200 and the other half it is $0.

d. half of the time the payoff is $200 and the other half it is $50.

21

67. The fact that not everyone places all of his/her savings in U.S. Treasury bonds indicates

that:

a. most investors are not risk averse.

b. many investors are actually risk seekers.

c. even risk-averse people will take risk if they are compensated for it.

d. most people are risk-neutral.

68. Hedging risk and spreading risk are two ways to:

a. increase expected returns from a portfolio.

b. diversify a portfolio.

c. lower transaction costs.

d. match up perfectly positively correlated assets.

69. Sometimes spreading has an advantage over hedging to lower risk because:

a. it can be difficult to find assets that move predictably in opposite directions.

b. it is cheaper to spread than hedge.

c. spreading increases expected returns, hedging does not.

d. spreading does not affect expected returns.

70. Spreading risk involves:

a. finding assets whose returns are perfectly negatively correlated.

b. adding assets to a portfolio that move independently.

c. investing in bonds and avoiding stocks during bad times.

d. building a portfolio of assets whose returns move together.

71. Investing in a mutual fund made up of hundreds of stocks of different companies is an

example of all of the following except:

a. spreading risk.

b. diversifying.

c. risk reduction.

d. increasing the variance of a portfolio.

72. An automobile insurance company that writes millions of policies is practicing a form of:

a. mutual fund.

b. hedging risk.

c. spreading risk.

d. eliminating systematic risk.

73. An automobile insurance company on average charges a premium that:

a. equals the expected loss from each driver.

b. is less than the expected loss from each driver.

c. is greater than the expected loss from each driver.

d. equals 1/(expected loss) of each driver.

23

74. The variance of a portfolio of assets:

a. decreases as the number of assets increases.

b. increases as the number of assets increase.

c. approaches 0 as the number of assets decreases.

d. approaches 1 as the number of assets increases.

75. In investment matters, generally young workers compared to older workers will:

a. minimize expected return and focus more on variability.

b. be less risk-averse.

c. have equal concern for expected return and

variabilit

y.

d. be more risk-averse.

76. The variance of a portfolio containing n assets with independent returns:

a. increases as n increases.

b. decreases as n increases.

c. is constant for any n greater than two.

d. does not change in a predictable way when n increases.

77. The expected return from a portfolio made up equally of two assets that move perfectly

opposite of each other would have a standard deviation equal to:

a. 1.0

b. -1.0

24

c. 0.0

d. 0.5

78. An individual who is risk-averse:

a. never takes risks.

b. accepts risk but only when the expected return is very small.

c. requires larger compensation when the risk increases.

d. will accept a lower return as risk rises.

79. A portfolio of assets has lower risk than holding one asset, but the same expected return and

higher transaction costs. Which of the following statements is most correct?

a. The portfolio is attractive to people who are risk-averse and risk-neutral, but not to risk

seekers. b. The portfolio is attractive to investors who are risk-neutral.

c. The portfolio is not attractive to investors who are risk–

neutral. d. The portfolio is attractive to investors who are risk

Short Answer Question

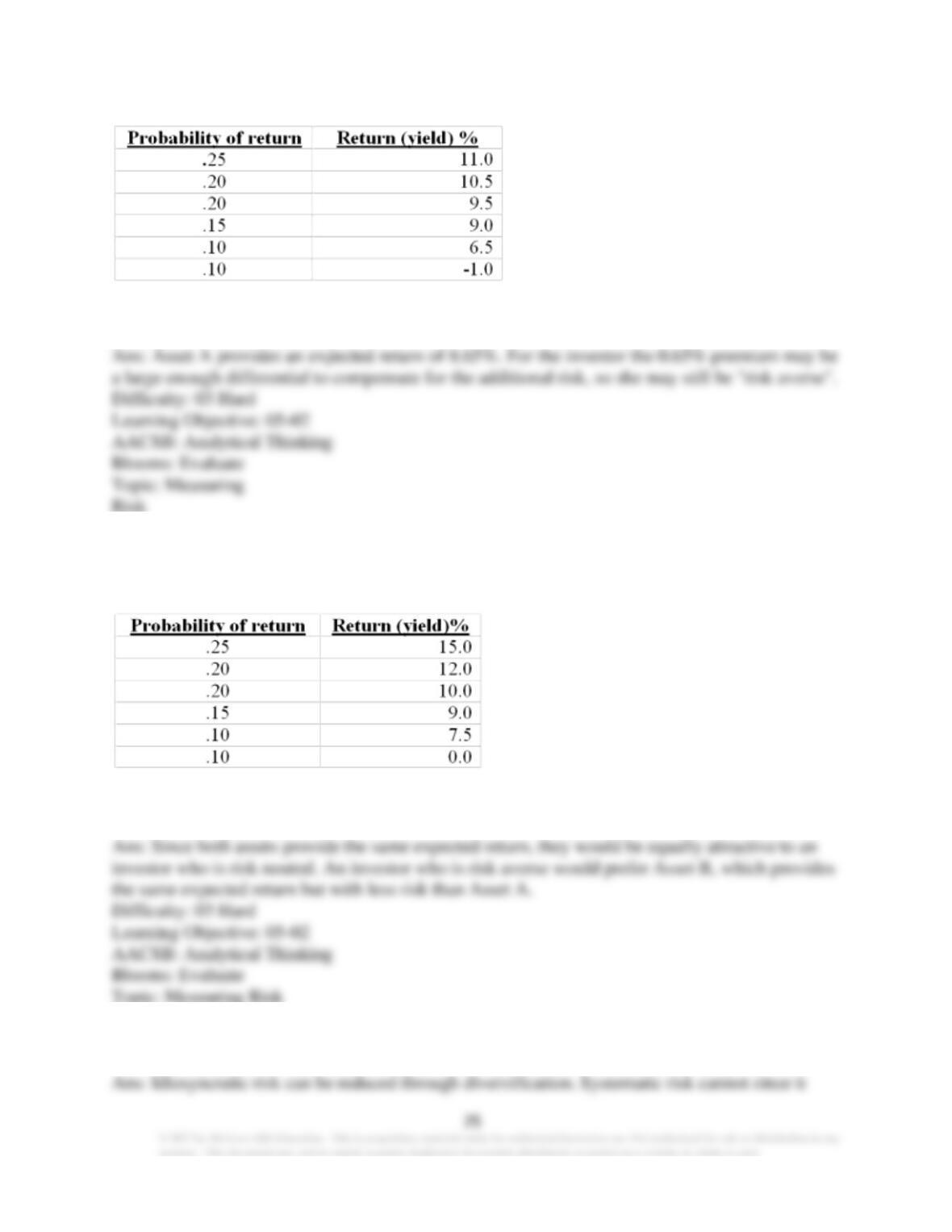

80. An individual faces two alternatives for an investment: Asset A has the following probability

return schedule:

Asset B has a certain return of 8.0%. If the individual selects asset A does she violate the

principle of risk aversion? Explain.

81. An individual faces two alternatives for an investment. Asset ‘A’ has the following

probability of return schedule:

Asset ‘B’ has a certain return of 10.25%. If this individual selects asset ‘A’ does it imply she is

risk averse? Explain.

82. Explain why returns on assets compensate for systematic risk but not for idiosyncratic risk.

83. Consider the following two assets with probability of return = Pi and return = Ri. Calculate

the expected return for each and the standard deviation. Which one carries the greatest risk?

Why?

84. Explain why a riskier asset offers a higher expected return.

85. What is the expected value of a $100 bet on a flip of a fair coin, where heads pays double

and tails pays zero?

86. An individual owns a $100,000 home. She determines that her chances of suffering a fire in

any given year to be 1/1000 (0.001). She correctly calculates her expected loss in any year to be

$100. Explain why this really isn‘t a good way to measure her potential for loss.

87. Identify at least three possible sources for a risk an individual may face in planning for

retirement.

88. What is the probability of tossing a pair of dice once and getting a 1? How about a 7?

28

89. If there are 1,000 people, each of whom owns a $100,000 house, and they each stand a

1/1,000 chance each year of suffering a fire that will totally destroy their house, what is the

minimum that they would have to pay annually for fire insurance?

90. Calculate the expected value, the expected return, the variance and the standard deviation of

an asset that requires a $1000 investment, but will return $850 half of the time and $1,250 the

other half of the time.

91. Explain the following: Risk results from the fact that more outcomes could happen than will

happen.

92. Calculate the expected value of an investment that has the following payoff frequency: a

quarter of the time it will pay $2,000, half of the time it will pay $1,000 and the remaining time it

will pay $0.

93. Consider the following two investments. One is a risk-free investment with a $100 return.

The other investment pays $2,000 20% of the time and a $375 loss the rest of the time. Based

on this information, answer the following:

(i) Compute the expected returns and standard deviations on these two investments individually.

(ii) Compute the value at risk for each investment.

(iii) Which investment will risk-averse investors prefer, if either? Which investment will risk–

neutral investors prefer, if either?

94. Compute the expected return, standard deviation, and value at risk for each of the following

investments:

Investment (A): Pays $800 three-fourths of the time and a $1,200 loss

otherwise. Investment (B): Pays $1,000 loss half of the time and a $1,600 gain

otherwise.

State which investment will be preferred by each of the following investors, and explain why.

(i) a risk-neutral investor

(ii) an investor who seeks to avoid the worst-case scenario.

(iii) a risk-averse investor.

95. You do some research and find for a driver of your age and gender the probability of

havi

ng

an accident that results in damage to your automobile exceeding $100 is 1/10 per year. Your auto

insurance company will reduce your annual premium by $40 if you will increase your collision

deductible from $100 to $250. Should you? Explain.

96. What would be the standard deviation for a $1,000 risk-free asset that returns $1,100?

97. You buy an asset for $2,500. The asset will return $3,300 half of the time and $2,700, the

other half. The expected return is 20% (a gain of $500) and the standard deviation is 12% ($300).

How would using $1,250 of borrowed funds change the expected return and standard deviation

specifically?

98. What would be the impact of leverage on the expected return and standard deviation of

purchasing an asset with 10% of the owner’s funds and 90% borrowed funds?

99. Why isn’t it correct to say that people who are risk averse avoid risk?

100. Briefly explain the difference between idiosyncratic risk and systematic risk. Provide an

example of each.

101. Explain why a company offering homeowners insurance policies would want to insure

homes across a wide geographic area.

102. Explain the rapid rise in popularity of mutual funds.

103. Considering leverage, can you explain why a mortgage lender would want borrowers to

have larger down payments, and when the borrower doesn’t the mortgage lender may require

mortgage insurance?

104. You study horse racing avidly and discover for this year’s Kentucky Derby you think you

have the field pretty well figured out. In fact, you calculate the expected return and it is the same

as the expected return you are getting from the stock market. Is this investment in the race

valuable to you?

105. Consider an individual who plans to buy a new home. He has two options: (i) pay for

mortgage insurance (that insures the lender in case the borrower defaults), or (ii) pay the lender a

higher interest rate for the mortgage. Describe how these two options are related to the concept

of risk premium and the lender’s aversion to risk. Why does the interest rate on the mortgage

differ in these two options?

106. How are the decisions of government policy makers, such as the Federal Reserve, related to

risk and an individual investor’s portfolio?

Essay Questions

107. Apply the definition of risk provided in the textbook to an individual‘s decision to purchase

a car insurance policy. Suppose that the individual has two possibilities: no accident ($0

gain/l

oss) and accident (-$30,000 loss). If the probability of an accident is lower than the

probability of an accident occurring (say the probability of an accident is 10%), then why do

people buy car insurance? How is this related to the concept of value at risk and the time horizon

of investment decisions?

108. What is the difference between standard deviation and value at risk? Consider the

difference between purchasing a one-year bank CD compared with purchasing a homeowner’s

insurance policy. Which scenario do you believe is more likely to consider value at risk over

standard deviation? Explain.

109. Explain why insurance companies may find themselves at times having to refuse business.

110. Suppose a saver is looking for the opportunity to make a very large return in a very short

period of time. Would you recommend diversification for this individual?