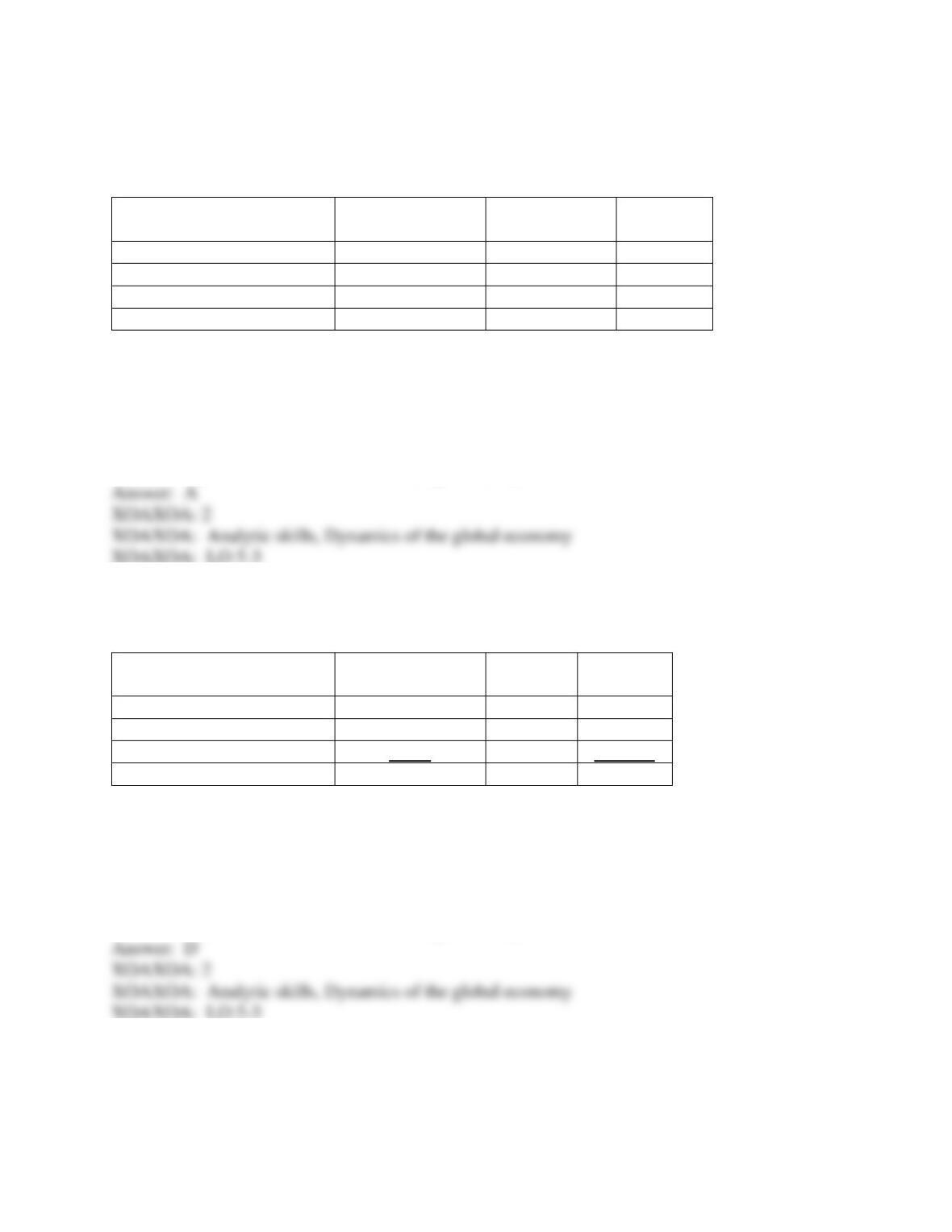

77) Idaho Company made the following purchases during the month of October.

October 6

Purchased $15,000 of merchandise, terms 2/10, n/30,

FOB destination, freight cost $100

October 14

Purchased $12,000 of merchandise, terms 2/15, n/60,

FOB shipping point, freight cost $100

October 22

Purchased $18,000 of merchandise, terms 3/10, n/20,

FOB destination, freight cost $100

October 31

Purchased $20,000 of merchandise, terms 1/15, n/45,

FOB shipping point, freight cost $100

Required:

1. Complete the chart below for each of the four purchases.

Oct. 6

Oct. 14

Oct. 22

Oct. 31

a. due date, assuming the

discount is taken

b. last day to pay if the

discount is NOT taken

c. amount of discount

$

$

$

$

d. freight cost paid by

Idaho Company

$

$

$

$

2. Assuming that the selling company accepts all discounts, what is the total cost of purchases for

the month?

b.

d.

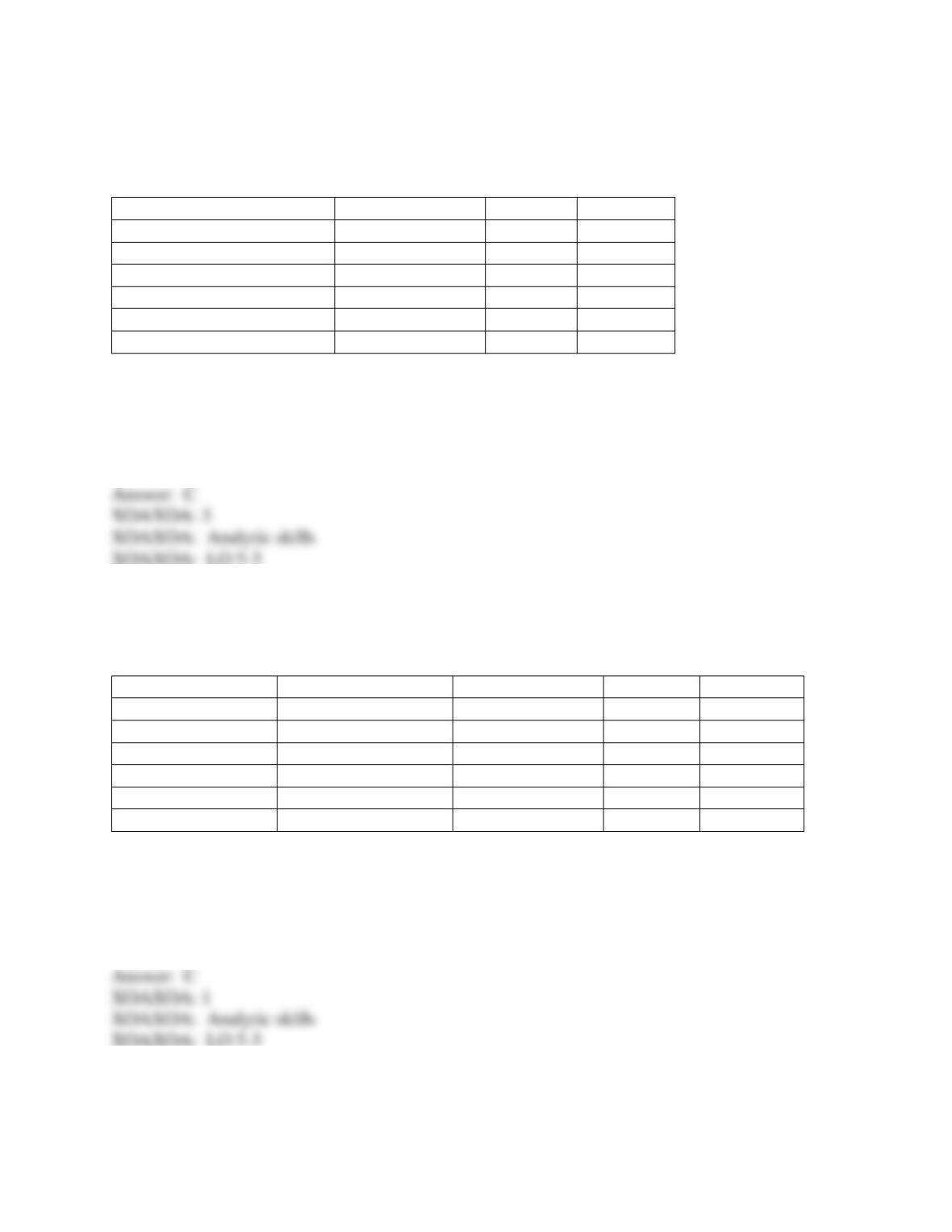

78) Tiny Toy Company makes toys and sells them to retail stores on account. The company has a

December 31 year-end. In the past, Tiny Toy always sold on account but never offered sales

discounts to its customers. However, this year on November 1, the beginning of the holiday sales

season, Tiny Toy began offering stores terms of 2/90, n/120. The stores can return anything, no

questions asked, but only AFTER December 31.

Required:

A. Why would Tiny Toy offer such a liberal credit and return policy?

B. Put an X in the appropriate box to describe the effect of this credit and return policy on Tiny

Toy’s financial statements for this year.

Financial statement item

Increase

Decrease

No effect

Sales

A/R

Inventory

C. Is Tiny Toy’s new credit and return policy ethical?

Financial statement item

No effect

A/R

Inventory

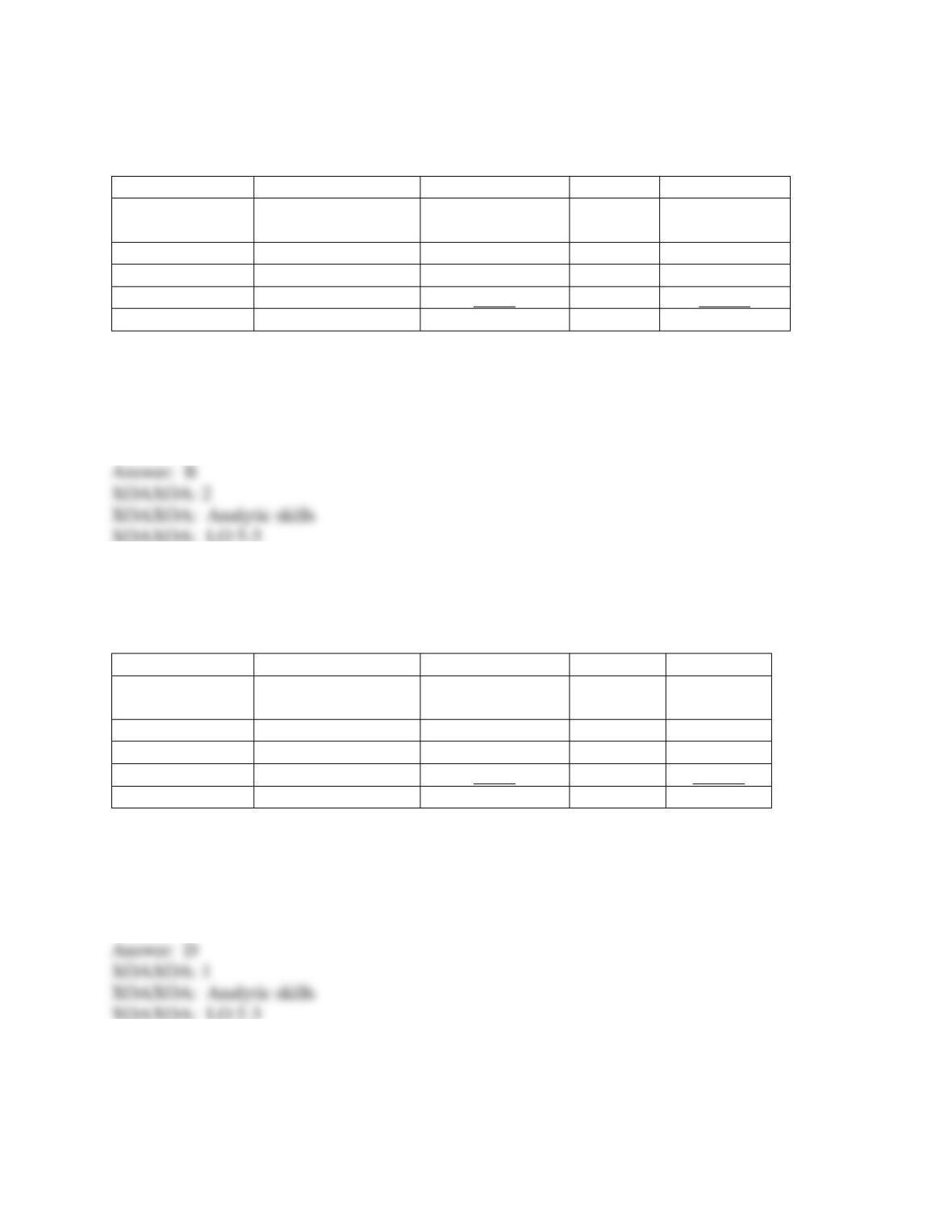

79) For each of the purchases below made by Daily Grind, Inc., fill in the inventory amount

NET of discounts, and then indicate with an “X” whether you should include or exclude the

purchase from Daily Grind’s inventory balance at DECEMBER 31.

Daily Grind purchased ON DECEMBER 31:

Amount

Include

Exclude

1. $5,000 of merchandise; terms 2/10, n/30,

FOB shipping point. The shipping cost $500.

The merchandise arrived on Jan. 2.

2. $8,000 of merchandise; terms 1/10, n/15,

FOB destination. The shipping cost $80.

The merchandise arrived on Jan 1.

80) Big Company has a policy of always taking the cash discounts offered by vendors, even if it

doesn’t pay within the discount period. Big Company thinks that many of the vendors won’t

notice, or if they do notice won’t bother to send another bill for a small amount.

On May 5, Big Company bought $5,000 of merchandise from Little Company, terms 2/10, n/30,

FOB destination. Freight on the shipment was $40.

A. How many days does Big Company have to pay the bill and legitimately take the discount?

B. If Big Company pays within the discount period, how much should it pay Little Company?

C. Who should pay the freight on the shipment, Big Company or Little Company?

D. Is it ethical for Big Company to take the cash discount even though it does not pay within the

discount period?

Include

($5,000 x .98) + $500

($8,000 x .99)

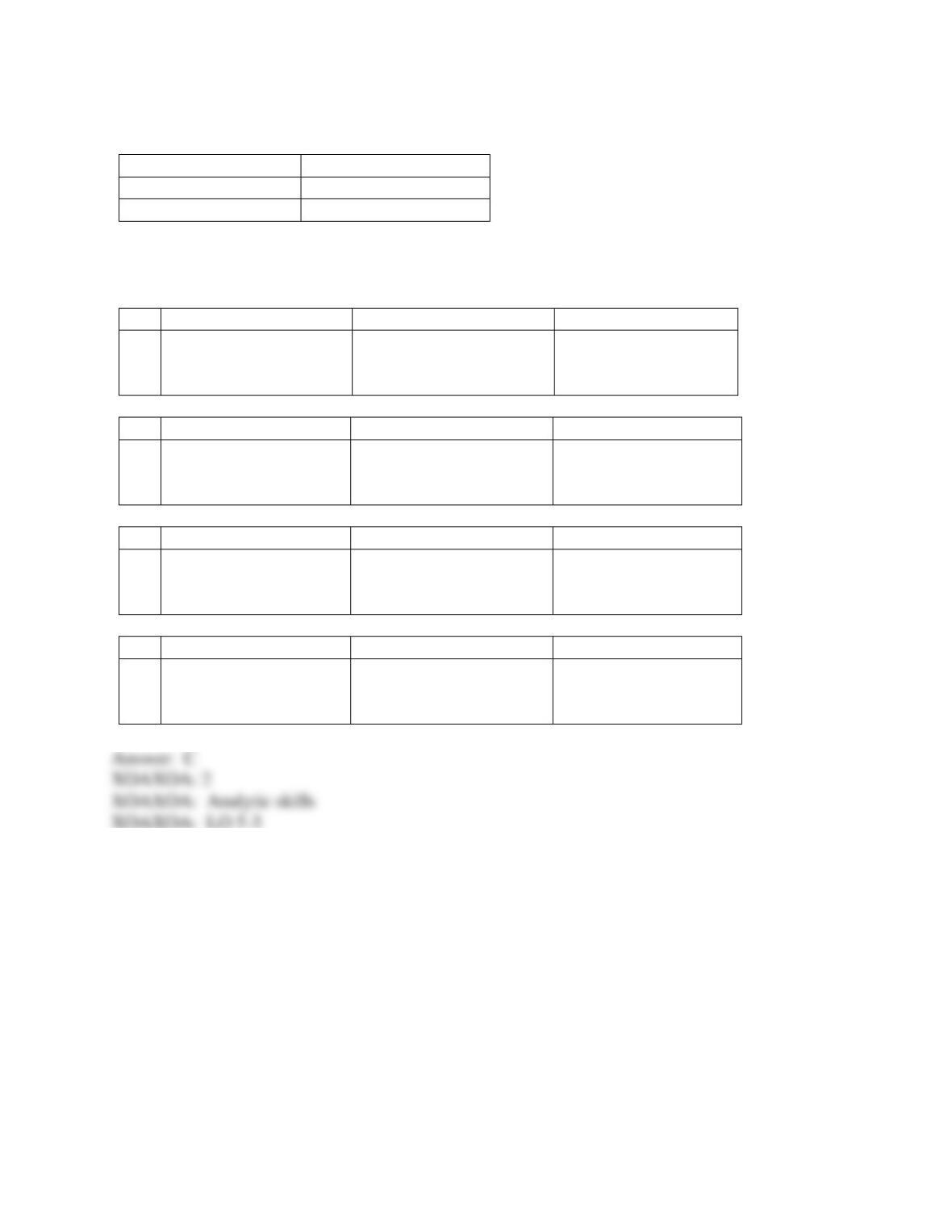

81) Match the items below with the appropriate statements.

I = The expenditure should be included in the inventory account.

X = The expenditure should NOT be included in the inventory account.

______ 1. ABC, Inc. purchases merchandise and pays $400 of shipping insurance.

______ 2. ABC, Inc. returned $200 of merchandise.

______ 3. ABC, Inc. paid $2,500 to a supplier for merchandise it had purchased on credit two

months earlier.

______ 4. ABC, Inc. purchases $2,000 of merchandise on account.

______ 5. ABC, Inc. pays $60 of import tariffs associated with a purchase of merchandise from

an overseas supplier.

82) Match the descriptions below with the correct credit or shipping terms. Some terms may be

used more than once and others may not be used at all.

a. 2/10, n/30

b. 1/15, n/45

c. n/60

d. 3/10, n/60

e. FOB destination

f. FOB shipping point

______ 1. credit terms that do not provide a discount for early payment

______ 2. credit terms that allow for a 1% discount for early payment

______ 3. shipping terms that would typically mean that the buyer has to pay the freight charges

______ 4. shipping terms that would typically mean that the seller has to pay the freight charges

______ 5. credit terms that provide for a maximum of one and a half months to satisfy the debt

______ 6. credit terms that provide for a 2% discount for early payment

83) Match the items below with the appropriate statements.

A = The expenditure should be included in the inventory account.

B = The expenditure should NOT be included in the inventory account.

______ 1. UIO Co. pays $330 to insure merchandise while it is on the shelves waiting to be sold.

______ 2. RXD was billed $500 for merchandise that it had already returned to the vendor.

______ 3. YUH Company paid $12,600 to a supplier for merchandise it had purchased on credit

two months earlier.

______ 4. TGF Company purchases 500 units of merchandise at a cost of $1.40 each.

______ 5. GLO Company pays $560 of import tariffs associated with a purchase of merchandise

from an overseas supplier.

______ 6. EOP Inc. pays for freight on goods that it purchased with credit terms of FOB

shipping point.

______ 7. RFV Company pays the purchasing manager a $70,000 annual salary.

84) Match the descriptions below to the correct credit or shipping terms. Some terms may be

used more than once. Others may not be used at all.

a. 2/10, n/30

b. 1/15, n/45

c. n/30

d. 3/10, n/60

e. FOB destination

f. FOB shipping point

______ 1. would result in a $200 discount for early payment of a $10,000 purchase

______ 2. shipping terms that would typically mean that the buyer has to pay the freight charges

______ 3. credit terms that allow the buyer a maximum of two months to pay the debt

______ 4. credit terms that do not allow a discount for early payment

______ 5. would result in a $150 discount for early payment of a $5,000 purchase

______ 6. credit terms that would set May 2 as the latest payment date to take a discount on an

April 17 purchase

Learning Objective 5-2

1) The perpetual inventory method is a method of record keeping that ________.

A) maintains a constant record of the inventory balance

B) updates the inventory records only at the end of the accounting period

C) can be used only in a computerized accounting system

D) involves calculating cost of goods sold only at the end of the period

2) The periodic inventory method is a method of record keeping that ________.

A) maintains a constant record of the inventory balance

B) updates the inventory records only when a sale is made

C) can be used only in a computerized accounting system

D) involves calculating cost of goods sold only at the end of the period

3) Which of the following is an advantage of a perpetual inventory system over a periodic

system?

A) Cost of goods sold will be less.

B) Sales will be greater.

C) Inventory shrinkage is separately identified.

D) Sales returns will be less.

4) Two systems of inventory record keeping are ________.

A) periodic and perpetual

B) computerized and database

C) purchase returns and purchase discounts

D) merchandising and manufacturing

5) How does a perpetual inventory system differ from a periodic system?

A) Sales are increased only at the end of the accounting period in a perpetual system.

B) Cost of goods sold is increased only after an inventory count in a perpetual system.

C) Inventory is reduced after each sale in a perpetual system.

D) Inventory is increased after each sale in a periodic system.

6) In which way is a perpetual inventory system similar to a periodic system?

A) Sales are increased at the time of sale.

B) Cost of goods sold is increased after an inventory count.

C) Inventory is reduced after each sale.

D) Cost of goods sold is increased after each sale.

7) With a perpetual inventory system, cost of goods sold is calculated only when the firm is

ready to prepare financial statements.

8) The periodic inventory system is a record keeping system that involves calculating cost of

goods sold only at the end of the period.

9) A company that uses a perpetual inventory system must calculate cost of goods sold each time

it records a sale.

10) Compare and contrast the perpetual and periodic inventory systems.

1) FIFO means that the costs of the oldest items in inventory are ________.

A) the costs that attach to ending inventory at the end of the period

B) the costs that attach to the inventory sold during the period

C) reduced to the lower of cost or market value during the period

D) expensed when purchased

2) Which method results in the cost of goods sold equaling the exact cost of the actual goods that

have been sold?

A) FIFO

B) LIFO

C) Weighted average method

D) Specific identification

3) Which method requires the unit cost is calculated by dividing the total cost of goods available

for sale by the total number of units available for sale?

A) FIFO

B) LIFO

C) Weighted average method

D) Specific identification

4) GAAP for inventory costs ________.

A) allow two cost flow assumptions: FIFO and LIFO

B) require companies to report the same net income regardless of which inventory cost flow

assumption is used. This is called the income conformity rule

C) allow for only one inventory cost flow assumption to enhance comparability

D) allow for more than two inventory cost flow assumptions

5) Vango, Inc. sells part number 86Z to auto parts stores around the world. Information about

part number 86Z is contained in the table below. Vango uses a FIFO periodic inventory system.

Number of Units

Unit Cost

Total

Cost

Beginning inventory

2,000

$8.00

$16,000

Purchase

3,000

$8.20

$24,600

Purchase

5,000

$8.60

$43,000

Totals

10,000

$83,600

Determine the cost of goods sold and ending inventory value of part 86Z, if 4,000 units remain

unsold in inventory at the end of the accounting period.

A) Cost of goods sold is $49,200 and ending inventory is $34,400.

B) Cost of goods sold is $34,400 and ending inventory is $49,200.

C) Cost of goods sold is $50,160 and ending inventory is $33,440.

D) Cost of goods sold is $51,200 and ending inventory is $32,400.

6) Vango, Inc. sells part number 86Z to auto parts stores around the world. Information about

part number 86Z is contained in the table below. Vango uses a FIFO perpetual inventory

system.

Number of Units

Unit

Cost/Price

Total Cost

Beginning inventory

2,000

$8.00

$16,000

Purchase

3,000

$8.20

$24,600

Sale

(6,000)

$15.00

Purchase

5,000

$8.60

$43,000

Determine the cost of goods sold and ending inventory value of part 86Z, if 4,000 units remain

unsold in inventory at the end of the accounting period.

A) Cost of goods sold is $49,200 and ending inventory is $34,400.

B) Cost of goods sold is $34,400 and ending inventory is $49,200.

C) Cost of goods sold is $50,160 and ending inventory is $33,440.

D) Cost of goods sold is $51,200 and ending inventory is $32,400.

7) Vango, Inc. sells part number 86Z to auto parts stores around the world. Information about

part number 86Z is contained in the table below. Vango uses a LIFO periodic inventory system.

Number of Units

Unit Cost

Total

Cost

Beginning inventory

2,000

$8.00

$16,000

Purchase

3,000

$8.20

$24,600

Purchase

5,000

$8.60

$43,000

Totals

10,000

$83,600

Determine the cost of goods sold and ending inventory value of part 86Z, if 4,000 units remain

unsold in inventory at the end of the accounting period.

A) Cost of goods sold is $49,200 and ending inventory is $34,400.

B) Cost of goods sold is $34,400 and ending inventory is $49,200.

C) Cost of goods sold is $50,160 and ending inventory is $33,440.

D) Cost of goods sold is $51,200 and ending inventory is $32,400.

8) Vango, Inc. sells part number 86Z to auto parts stores around the world. Information about

part number 86Z is contained in the table below. Vango uses a weighted average cost periodic

inventory system.

Number of Units

Unit Cost

Total Cost

Beginning inventory

2,000

$8.00

$16,000

Purchase

3,000

$8.20

$24,600

Purchase

5,000

$8.60

$43,000

Totals

10,000

$83,600

Determine the cost of goods sold and ending inventory value of part 86Z, if 4,000 units remain

unsold in inventory at the end of the accounting period.

A) Cost of goods sold is $49,200 and ending inventory is $34,400.

B) Cost of goods sold is $34,400 and ending inventory is $49,200.

C) Cost of goods sold is $50,160 and ending inventory is $33,440.

D) Cost of goods sold is $51,200 and ending inventory is $32,400.

9) Fargo Engines Incorporated sells part number 45G to toy manufacturers around the world.

Information about part number 45G is contained in the table below. Fargo uses a LIFO periodic

inventory system.

Number of Units

Unit Cost

Total Cost

Beginning inventory

2,000

$8.00

$16,000

Purchase

3,000

$8.20

$24,600

Purchase

5,000

$8.60

$43,000

Totals

10,000

$83,600

Determine the cost of goods sold and ending inventory cost of part 45G, if 2,000 units remain

unsold in inventory at the end of the accounting period.

A) Cost of goods sold is $67,600 and ending inventory is $16,000.

B) Cost of goods sold is $66,600 and ending inventory is $17,000.

C) Cost of goods sold is $66,200 and ending inventory is $17,400.

D) Cost of goods sold is $8,000 and ending inventory is $2,000.

10) Fargo Engines Incorporated sells part number 45G to toy manufacturers around the world.

Information about part number 45G is contained in the table below. Fargo uses a weighted-

average periodic inventory system.

Number of Units

Unit Cost

Total Cost

Beginning inventory

2,000

$8.00

$16,000

Purchase

3,000

$8.20

$24,600

Purchase

5,000

$8.60

$43,000

Totals

10,000

$83,600

Determine the cost of goods sold and ending inventory cost of part 45G if 2,000 units remain

unsold in inventory at the end of the accounting period.

A) Cost of goods sold is $66,133 and ending inventory is $17,467.

B) Cost of goods sold is $66,267 and ending inventory is $25,733.

C) Cost of goods sold is $65,803 and ending inventory is $26,197.

D) Cost of goods sold is $66,880 and ending inventory is $16,720.

11) One difference between U.S. GAAP and IFRS is ________.

A) U.S. GAAP allows LIFO and IFRS does not

B) IFRS allows LIFO and U.S. GAAP does not

C) U.S. GAAP allows FIFO and IFRS does not

D) IFRS allows FIFO and U.S. GAAP does not

12) Grand Forks Enterprises sells toy airplanes to retailers such as K-Mart and Wal-Mart.

Information about inventory is contained in the table below. The company uses a FIFO perpetual

inventory system.

Number of Units

Unit Cost

Total Cost

Beginning inventory

2,000

$2.00

$4,000

Sale

(1,200)

Purchase

4,000

$2.25

$9,000

Sale

(2,500)

Purchase

5,000

$2.40

$12,000

Sale

(6,000)

Determine the cost of goods sold.

A) $20,800

B) $21,200

C) $21,880

D) $19,400

13) Grand Forks Enterprises sells toy airplanes to retailers such as K-Mart and Wal-Mart.

Information about inventory is contained in the table below. The company uses a LIFO perpetual

inventory system and sells inventory for $5.00 per unit.

Date

Number of Units

Unit Cost

Total Cost

January 01

Beginning inventory

2,000

$2.00

$4,000

January 10

Sale

1,200

January 15

Purchase

4,000

$2.25

$9,000

January 20

Sale

2,500

January 25

Purchase

5,000

$2.40

$12,000

January 30

Sale

6,000

Determine the cost of goods sold for the January 10th sale.

A) $6,000

B) $3,600

C) $2,400

D) $2,600

14) Grand Forks Enterprises sells toy airplanes to retailers such as K-Mart and Wal-Mart.

Information about inventory is contained in the table below. The company uses a LIFO perpetual

inventory system and sells inventory for $5.00 per unit.

Date

Number

of Units

Unit Cost

Total

Cost

January 01

Beginning inventory

2,000

$2.00

$4,000

January 10

Sale

1,200

January 15

Purchase

4,000

$2.25

$9,000

January 20

Sale

2,500

January 25

Purchase

5,000

$2.40

$12,000

January 30

Sale

6,000

Determine the cost of goods sold for the January 20th sale.

A) $5,425

B) $5,850

C) $5,625

D) $5,725

15) Grand Forks Enterprises sells toy airplanes to retailers such as K-Mart and Wal-Mart.

Information about inventory is contained in the table below. The company uses a LIFO perpetual

inventory system and sells inventory for $5.00 per unit.

Date

Number of

Units

Unit Cost

Total Cost

January 01

Beginning inventory

2,000

$2.00

$4,000

January 10

Sale

1,200

January 15

Purchase

4,000

$2.25

$9,000

January 20

Sale

2,500

January 25

Purchase

5,000

$2.40

$12,000

January 30

Sale

6,000

Determine the ending inventory for the period.

A) $2,925

B) $2,600

C) $2,725

D) $3,120

16) Philipsburg Corporation sells mugs to fine retailers across the world. Data from its periodic

inventory system is presented in the table below. Inventory is sold for $170 per unit. Operating

expenses, excluding cost of goods sold, totaled $40,000.

Date

Number of

Units

Unit

Cost

Total Cost

January 1

Beginning

inventory

300

$100

$30,000

January 13

Purchase

400

$110

$44,000

January 22

Purchase

500

$120

$60,000

Which cost flow method would result in the HIGHEST taxable income for the period?

A) FIFO

B) LIFO

C) Weighted average method

D) Each of the methods would have equal net income for the period.

17) Philipsburg Corporation sells mugs to fine retailers across the world. Data from its periodic

inventory system is presented in the table below. Inventory is sold for $170 per unit. Operating

expenses excluding cost of goods sold totaled $40,000.

Date

Number of Units

Unit Cost

Total Cost

January 1

Beginning inventory

300

$100

$30,000

January 13

Purchase

400

$110

$44,000

January 22

Purchase

500

$120

$60,000

Which cost flow method would result in the LOWEST taxable income for the period?

A) FIFO

B) LIFO

C) Weighted average method

D) Only the LIFO cost flow method can be used for tax returns.

18) Inventory information for Great Falls Merchandising, Inc. is provided below. Sales for the

period were 2,800 units for $8 each. The company uses a FIFO periodic inventory system.

Date

Number of

Units

Unit Cost

Total Cost

January 1

Beginning

inventory

1,000

$3.00

$3,000

January

Purchase

600

$3.50

$2,100

February

Purchase

800

$4.00

$3,200

March

Purchase

1,200

$4.25

$5,100

Totals

3,600

$13,400

Determine the ending inventory at March 31.

A) $3,400

B) $3,800

C) $9,200

D) $10,000

19) Tarheel Company purchases inventory from McGardy Wholesalers. The per unit cost of the

items purchased during the current accounting period was $5.50, $5.70, $5.90 and $6.23. Which

statement below regarding Tarheel’s choice of inventory cost flow methods is TRUE?

A) Net income will be the same regardless of the cost flow assumption adopted. The choice of an

accounting method can’t affect net income.

B) Net income will be greater than taxable income regardless of the inventory method chosen by

Tarheel Company.

C) If Tarheel Company uses the LIFO method for financial reporting, then it must also use the

LIFO method for tax reporting.

D) If Tarheel Company selects the FIFO method, it will result in a lower net income than the

LIFO method would have produced.

20) Inventory information for Great Falls Merchandising, Inc. is provided below. Sales for the

period were 2,800 units for $8 each. The company uses a LIFO periodic inventory system.

Date

Number of Units

Unit Cost

Total Cost

January 1

Beginning

inventory

1,000

$3.00

$3,000

January

Purchase

600

$3.50

$2,100

February

Purchase

800

$4.00

$3,200

March

Purchase

1,200

$4.25

$5,100

Totals

3,600

$13,400

Determine the ending inventory at March 31.

A) $3,400

B) $2,400

C) $10,200

D) $800

21) Inventory information for Missoula Merchandising, Inc. is provided below. Sales for the

period were 2,800 units for $8 each. The company uses a weighted average periodic inventory

system.

Date

Number of Units

Unit Cost

Total Cost

January 1

Beginning

inventory

1,000

$2.20

$2,200

January

Purchase

600

$3.50

$2,100

February

Purchase

800

$4.00

$3,200

March

Purchase

1,200

$4.25

$5,100

Totals

3,600

$12,600

Determine the ending inventory at March 31.

A) $2,300

B) $3,300

C) $9,800

D) $2,800

22) A company would choose to use LIFO so that it can ________.

A) report inventory that best reflects current costs on its balance sheet

B) report lower cost of goods sold and higher income

C) pay less income tax

D) pay less for its purchases of inventory

23) On June 1, beginning inventory consists of ten items that cost $100 each. On June 8, ten

more items are purchased at $120 each. On June 12, fifteen items are sold for $200 each. On

June 28, ten items are purchased at $130 each. Using perpetual FIFO, cost of goods sold for the

month ended June 30 equals ________.

A) $1,500

B) $1,600

C) $1,800

D) $3,000

24) On June 1, beginning inventory consists of ten items that cost $100 each. On June 8, ten

more items are purchased at $120 each. On June 12, fifteen items are sold for $200 each. On

June 28, ten items are purchased at $130 each. Using periodic FIFO, cost of goods sold for the

month ended June 30 equals ________.

A) $1,500

B) $1,600

C) $1,800

D) $3,000

25) On June 1, beginning inventory consists of ten items that cost $100 each. On June 8, ten

more items are purchased at $120 each. On June 12, fifteen items are sold for $200 each. On

June 28, ten items are purchased at $130 each. Using periodic LIFO, cost of goods sold for the

month ended June 30 equals ________.

A) $1,600

B) $1,800

C) $1,900

D) $1,950

26) On June 1, beginning inventory consists of ten items that cost $100 each. On June 8, ten

more items are purchased at $120 each. On June 12, fifteen items are sold for $200 each. On

June 28, ten items are purchased at $130 each. Using perpetual LIFO, cost of goods sold for the

month ended June 30 equals ________.

A) $1,700

B) $1,800

C) $1,900

D) $1,950

27) Mighty Ducks, Inc.’s inventory activity in October 2011 was as follows:

Inventory, October 1

11 units @ $8 each

Purchase, October 12

22 units @ $11 each

Sale, October 25

23 units @ $24 each

Which of the following shows the correct effect on the accounting equation of the October 25

sale on account using the perpetual FIFO method of accounting for inventory?

A)

Assets

Liabilities

Shareholders’ equity

(220) Inventory

552 Accounts payable

552 Sales

(220) Cost of goods

sold

B)

Assets

Liabilities

Shareholders’ equity

552 Accounts

receivable

(250) Inventory

No effect

552 Sales

(250) Cost of goods

sold

C)

Assets

Liabilities

Shareholders’ equity

552 Accounts

receivable

(220) Inventory

No effect

552 Sales

(220) Cost of goods

sold

D)

Assets

Liabilities

Shareholders’ equity

(230) Inventory

552 Accounts payable

552 Sales

(230) Cost of goods

sold