Achievement Test 4: Chapters 7 and 8 Name __________________________

Accounting Instructor _______________________

Kimmel, Weygandt, & Kieso Section # _______ Date _________

Part

I

II

III

IV

V

VI

Total

Points

30

12

18

11

20

9

100

Score

PART I — MULTIPLE CHOICE (30 points)

Instructions: Designate the best answer for each of the following questions.

____ 1. Which of the following represent the three classifications of receivables?

a. Accounts receivable, notes receivable, and other receivables

b. Accounts to be collected, accounts estimated that will not be collected, accounts

that were not collected

c. Receivables that are recognized, receivables that are valued, receivables that are

accelerated

d. Interest-related receivables, receivables from customers, receivables from

employees/officers

____ 2. Days of Slumber sells mattress for cash and on credit. At the end of 2014, the

following appeared in the company’s balance sheet:

Accounts receivable, net of $2,460 allowance……………………$166,200

Which one of the following statements for Days of Slumber is correct?

a. Customers owe $168,660 to Days of Slumber

b. Days of Slumber expects to collect $163,470 from customers.

c. Days of Slumber wrote off $2,460 of uncollectible accounts during 2014.

d. The net realizable value of Days of Slumber’s accounts receivable totals $163,740.

____ 3. Which of the following is not an element of fraud in a business environment?

a. Financial pressure

b. Rationalization

c. Opportunity

d. Risk assessment

____ 4. Which of the following is one reason that companies estimate uncollectible accounts?

a. To identify which customers’ accounts will become uncollectible

b. To write off the amounts which will not be collected from customers

c. To match the expense associated with receivables against the related revenues

d. To determine the total amount owed by customers

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT4-2

____ 5. Which of the following is a basic principle of cash management?

a. Increase the speed of receivables collection

b. Keep inventory levels high

c. Maintain a high cash balance for unanticipated emergencies

d. Defer the timing of major expenditures

____ 6. Which one of the following is not an objective of internal control?

a. To ensure compliance with laws and regulations

b. To guarantee the accuracy of the accounting records

c. To enhance the reliability of financial statements

d. To safeguard assets

____ 7. Which one of the following is provided by the cash budget?

a. It can indicate the profitability of a company.

b. It can identify projected expenses.

c. It can identify when a company will need additional financing.

d. It can identify if a company has adequate internal controls.

____ 8. Which of the following items may cause the cash balance per bank to differ from the

cash balance per books?

a. Time lags and bank errors

b. Bank errors and the existence of multiple bank accounts

c. Time lags and the existence of multiple bank accounts

d. Existence of amounts not yet paid by customers and time lags

____ 9. Which of the following items is not considered to be a cash equivalent?

a. Short-term highly liquid investments maturing in 30 days

b. Commercial paper

c. Restricted cash funds

d. Money market funds

____ 10. Which one of the following is not a reason that a company may sell it receivables?

a. The amount due from customers is relatively large compared to other assets

owned by a company.

b. A company determines it will be unable to collect all amounts due from customers.

c. Selling receivables is a reasonable source of cash, often less costly than loans.

d. Billing and collecting amounts due from customers is time-consuming and costly.

Achievement Test 4

AT4-3

PART II — INTERNAL CONTROL OVER CASH RECEIPTS AND DISBURSEMENTS (12 points)

Six internal control principles related to cash transactions are discussed in the textbook. These

principles, with code letters, are:

Code Internal Control Principle

A Establishment of responsibility

B Segregation of duties

C Documentation procedures

D Physical controls

E Independent internal verification

F Human resource controls

Instructions: Match the above principles to the following applications related to cash receipts

and cash disbursements by placing the code in the space provided. Each code letter can be used

once, more than once, or not at all.

____ 1. The duties of approving an item for payment and paying the item should be performed

by different individuals.

____ 2. Cash register tapes should be used for over–the-counter receipts.

____ 3. Each check should be compared with approved invoices before being issued.

____ 4. Only the treasurer should be authorized to sign checks.

____ 5. All personnel who handle cash should be bonded.

____ 6. All checks should be prenumbered.

____ 7. After payment, an invoice should be stamped “PAID.”

____ 8. Blank checks should be stored in a safe, and access should be restricted.

____ 9. Daily cash counts should be made by cashier department supervisors.

____ 10. Only designated personnel should be authorized to handle and have access to cash

receipts.

____ 11. The duties of receiving and recording cash should be assigned to different individuals.

____ 12. Small bills and coins on hand to resupply cash registers should be kept in a safe.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT4-4

PART III — BANK RECONCILIATION WITH ENTRIES (18 points)

Alykhan Industries provided the following information for the month of February.

1. Balance per bank on February 28—$31,080

2. Balance per books on February 28—$32,210

3. Total outstanding checks at February 28—$2,100

4. Debit memoranda:

a. NSF check from Sanderson, Inc.—$450

b. Printing company checks—$20

c. Electronic payment to bank for a loan—$2,220. Of this amount, $90 is interest.

5. Credit memorandum: EFT from customer for $1,450

6. A check written this month to City Utilities and cleared the bank at the correct amount of

$1,790, but was recorded at $1,870.

7. The bank charged a $270 check of ABC Company against Alykhan Industries’ account.

8. Deposit in transit on February 28—$1,800

Instructions

A. Prepare a bank reconciliation in proper format.

B. Record the necessary journal entries for the month of February for Alykhan Industries.

1. Bank Reconciliation

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

Achievement Test 4

AT4-5

2. Journal Entries:

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT4-6

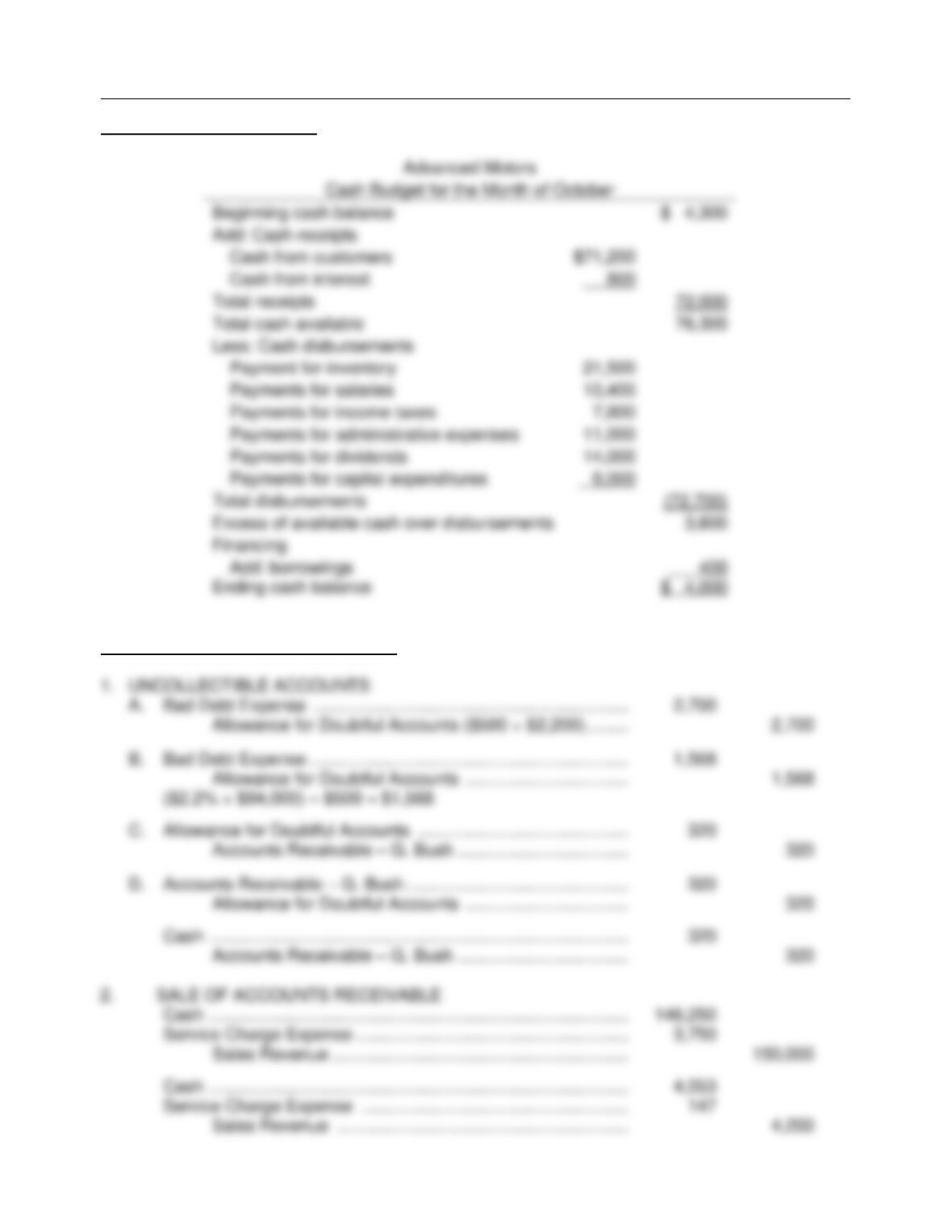

PART IV — CASH BUDGET (11 points)

The following estimated information is available for Advanced Motors for the month of October:

Cash receipts from customers $71,200

Payments for inventory 21,500

Payments for salaries 10,400

Receipt of interest on investments 800

Cash payments of income taxes 7,800

Cash payments of administrative expenses 11,000

Dividends to be paid 14,000

Capital expenditures 8,000

Depreciation expense 4,200

The cash balance at September 30 is $4,300. Management wishes to maintain a minimum cash

balance of $4,000.

Instructions

Prepare a basic cash budget for the month of October.

Achievement Test 4

AT4-7

PART V — ACCOUNTS RECEIVABLE (20 points)

1. ACCOUNTS RECEIVABLE—UNCOLLECTIBLE ACCOUNTS

Instructions: Present the journal entries specified below. Show supporting calculations. Each

item should be considered independently.

The trial balance of Priority Paints at December 31, 2014, includes the following:

Debits Credits

Accounts Receivable ……………………………………………………….. $94,000

Allowance for Doubtful Accounts ………………………………………. 500

Sales (all on credit) …………………………………………………………. $550,000

A. If Priority Paints uses the aging method and estimates that $2,200 of receivables will be

uncollectible, prepare the adjusting entry.

B. If Priority Paints estimates uncollectibles at 2.2% of accounts receivable and the

allowance account had a $500 credit balance instead of a $500 debit balance, prepare

the appropriate adjusting entry.

C. Assume that on February 3, 2015, the specific account of George Bush with a balance

of $320 is deemed uncollectible. Record the write-off.

D. Assume that on May 4, 2015, George Bush pays the above balance in full. Record the

appropriate entries.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT4-8

2. SALE OF ACCOUNTS RECEIVABLE

Instructions: Present the journal entries specified below.

A. Hardy Lumber Company sells $150,000 of accounts receivable to Buyout Factors Inc.

for cash less a 2.5% service charge. Record the sale.

B. Hardy Lumber Company sold merchandise for $4,200 and accepted the customer’s

VISA card. VISA charges a 3.5% service charge. Record the sale.

PART VI — NOTES RECEIVABLE (9 points)

Instructions: Prepare journal entries to record the following events. Round amounts to the

nearest whole dollar:

June 1 Hanalia Collision received a 5%, 4-month $5,000 note dated June 1 from a customer

for the balance due.

Sept.30 The note is honored and no interest has been accrued previously.

If Hanalia Collision has a fiscal year end at June 30, how much is the net realizable value of the

note on that date?

Achievement Test 4

AT4-9

Solutions — Achievement Test 4: Chapters 7 and 8

PART I — MULTIPLE CHOICE (30 points)

PART II — INTERNAL CONTROL OVER CASH RECEIPTS AND DISBURSEMENTS (12 points)

PART III — BANK RECONCILIATION WITH ENTRIES (16 points)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT4-10

PART IV — CASH BUDGET (14 points)

PART V — ACCOUNTS RECEIVABLE (16 points)

Achievement Test 4

AT4-11

PART VI — NOTES RECEIVABLE (12 points)