Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

4-98

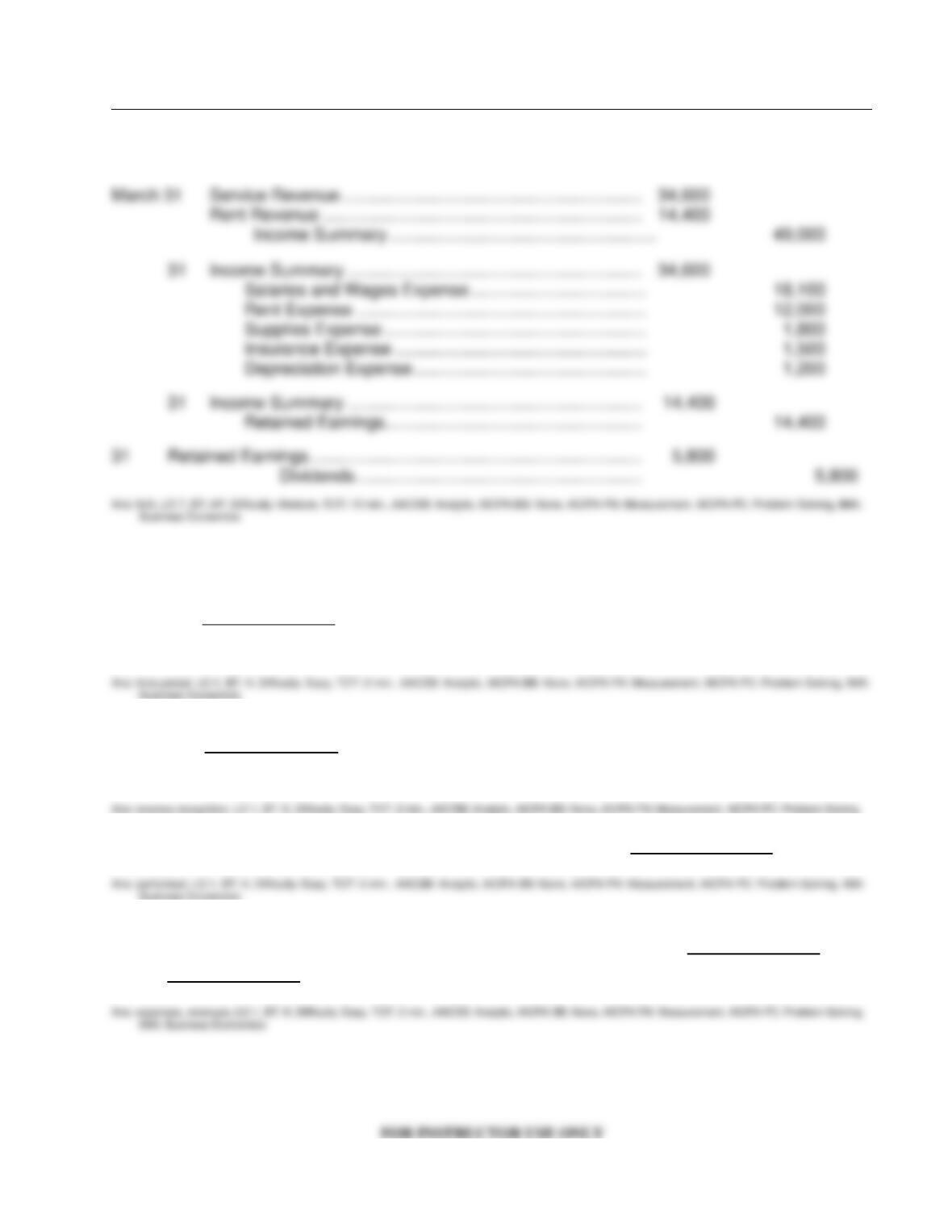

Ex. 278

The adjusted trial balance shown below is for Rich Company at the end of its fiscal year:

RICH COMPANY

Trial Balance

March 31, 2014

__________________________________________________________________________

Debit Credit

Cash ………………………………………………………………………………………… $ 12,900

Accounts Receivable …………………………………………………………………. 9,400

Supplies …………………………………………………………………………………… 700

Prepaid Insurance ……………………………………………………………………… 2,500

Equipment ………………………………………………………………………………… 16,000

Accumulated Depreciation—Equipment ……………………………………….. $ 4,800

Accounts Payable ……………………………………………………………………… 5,800

Salaries and Wages Payable ………………………………………………………. 1,100

Unearned Rent Revenue ……………………………………………………………. 600

Common Stock ………………………………………………………………………….. 15,000

Retained Earnings …………………………………………………………………….. 5,600

Dividends …………………………………………………………………………………. 5,800

Service Revenue ……………………………………………………………………….. 34,600

Rent Revenue …………………………………………………………………………… 14,400

Salaries and Wages Expense ……………………………………………………… 18,100

Supplies Expense ……………………………………………………………………… 1,800

Rent Expense …………………………………………………………………………… 12,000

Insurance Expense ……………………………………………………………………. 1,500

Depreciation Expense …………………………………………………………………. 1,200

$81,900 $81,900

Instructions:

Prepare the closing entries for the temporary accounts at March 31.

Accrual Accounting Concepts

4-99

Solution 278

COMPLETION STATEMENTS

279. The ______________ assumption states that the economic life of a business can be divided

into artificial time periods.

280. The ______________ principle gives accountants guidance as to when revenue is to be

recorded.

281. In a service company, revenue is earned when the service is _______________.

282. The expense recognition principle attempts to match ______________ with

______________.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

4-100

283. Expenses paid and recorded in an asset account before they are used or consumed are

called _______________. Revenue received and recorded as a liability before it is earned is

referred to as _________________.

284. Failure to adjust a prepaid expense account for the amount expired will cause

_______________ to be understated and ________________ to be overstated.

285. Depreciation is an __________________ concept, not a ________________ concept.

286. An adjusting entry recording accrued salaries for a period indicates that Salaries and Wages

Expense has been ________________ but has not yet been ________________ or record-

ed.

287. An adjusted trial balance proves the ______________ of the total debit and credit balances

after all ______________ entries have been made.

288. In addition to updating Retained Earnings, ______________ entries produce a zero balance

in each ______________ account.

289. After all closing entries are journalized and posted, a _________________ trial balance is

prepared from the ledger.

Accrual Accounting Concepts

FOR INSTRUCTOR USE ONLY

4-101

Answers to Completion Statements

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

4-102

MATCHING

290. Match the items below by entering the appropriate code letter in the space provided.

A. Periodicity assumption F. Accrued revenues

B. Cash basis G. Depreciation

C. Revenue recognition principle H. Post-closing trial balance

D. Prepaid expenses I. Accrued expenses

E. Expense recognition principle J. Book value

___ 1. Events recorded only in periods the company receives or pays cash

___ 2. Expenses paid before they are incurred

___ 3. Cost less accumulated depreciation

___ 4. The economic life of a business can be divided into artificial time periods

___ 5. Efforts are related to accomplishments

___ 6. Includes only permanent—balance sheet—accounts

___ 7. Revenue is recognized when the performance obligation is satisfied.

___ 8. Revenues earned but not yet received

___ 9. Expenses incurred but not yet paid

___ 10. A cost allocation process

Answers to Matching

Accrual Accounting Concepts

FOR INSTRUCTOR USE ONLY

4-103

SHORT-ANSWER ESSAY QUESTIONS

S-A E 291

You are part of a group of individuals (incorporators) who want to form a new corporation. During

discussions on forming the business, Mark Adams makes this statement:

Our business will have accounts receivable and accounts payable. It will also acquire a substantial

amount of computers and equipment. Will it be acceptable to use the cash basis of accounting?

Prepare a response for Mark and the other incorporators.

Solution 291

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

4-104

S-A E 292

The income statement is an important financial statement used by individuals who are interested in

the operations of a business enterprise. Explain how the periodicity assumption and the revenue

recognition and expense recognition principles provide guidance to accountants in preparing an in-

come statement.

Solution 292

S-A E 293

As a recent graduate in accounting, and the financial director of a political candidate in a current

election, you have been asked to explain many questions concerning how governmental accounting

differs from corporate accounting.

Required:

(a) Discuss the differences between cash basis and accrual−basis accounting.

(b) Prepare a memo to your candidate explaining why governmental entities favor the cash basis of

accounting.

Accrual Accounting Concepts

FOR INSTRUCTOR USE ONLY

4-105

Solution 293

S-A E 294

The long-term liability section of Alpha Corporation’s Balance Sheet includes the following accounts

Notes Payable

$100,000

Mortgage Payable

250,000

Salaries and Wages Payable

75,000

Accumulated Depreciation

125,000

Total Long-Term Liabilities

$550,000

Alpha Corporation is an established company and does not experience any financial difficulties or

have any cash flow problems. Discuss at least two items that are questionable as long-term liabilities.

Solution 294

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

4-106

S-A E 295

What is the purpose of the preparation of adjusting entries?

Solution S-A E 295

S-A E 296

Briefly distinguish between a deferral and an accrual.

Solution 296

S-A E 297

In developing an accounting information system, it is important to establish procedures whereby all

transactions that affect the components of the accounting equation are recorded. Why then, is it of-

ten necessary to adjust the accounts before financial statements are prepared even in a properly

designed accounting system? Identify the major types of adjustments that are frequently made and

give a specific example of each.

Solution 297

Accrual Accounting Concepts

FOR INSTRUCTOR USE ONLY

4-107

S-A E 298

Companies are continually under pressure to “Make the Numbers” – to have earnings that are in line

with expectations. Explain the terms earnings management and quality of earnings.

Solution 298

S-A E 299 (Ethics)

Benson and Jencks is a manufacturing company that specializes in writing instruments. The past

year was a difficult one for the company, as it sought to retain its share in a market in which the

largest competitors were also rapid innovators. Benson and Jencks introduced a new product late in

the year, even though testing was not complete. It was a pen designed with two cartridges: one sup-

plying ink and the other correction fluid. A person could then switch easily between writing and

correcting errors. It was priced fairly high, and was never heavily advertised. Even so, the Correct-O-

Pen, as the product was named, was an overwhelming success.

The success of the product has Fern Donald, the manager of the New Products division, worried,

however. She was concerned that quality problems would begin occurring, since the longevity of the

pen and stability of the correction fluid formulation had not been tested. She did not want sales per-

sonnel to get the bonuses that appeared to be indicated, since they might aggressively promote a

product that would fail in use. She preferred to complete testing of the pen first, so that more confi-

dence could be placed in the results.

Top management, however, declined the tests. Ms. Donald then instructed you, the accountant, not

to prorate payroll taxes or rent expense for the rest of the year, but to show them as current expens-

es in total. In this way, the new product would appear to be only slightly profitable.

Required:

1. Describe the alternatives that you as an accountant would have in this situation.

2. Indicate which alternative is best.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

4-108

Solution 299

S-A E 300 (Communication)

A new sales representative, Eddy Wherli, has just received his copy of the month-end financial re-

ports. He is puzzled by the term “unearned revenue.” He left the following e-mail message for you

on the company’s bulletin board system:

What is this??? Creative Accounting, or what??? Line item 12 on year-to-date financials

shows over $25Gs in Unearned Revenue!!! Come on, guys! Either we earned it, or we didn’t .

. . Right??! Is this how you guys lower our commissions? Reply to e.wherli@sbd

Required:

Write a response to send to Eddy. (Since the answer is being prepared for a “bulletin board” type

system, it can be in informal language and can respond in kind to the humor. However, proper

grammar and spelling are essential, as is the message about what unearned revenue really is.)

Accrual Accounting Concepts

FOR INSTRUCTOR USE ONLY

4-109

Solution 300

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

4-110

International Financial Reporting Standards

True-False Statements

1. The cash basis of accounting is not in accordance with IFRS.

2. The expense recognition principle requires that efforts be matched with accomplishments.

3. Adjusting entries are needed to enable financial statements to conform to International Fi-

nancial Reporting Standards (IFRS).

Multiple Choice Questions

4. Which of the following are in accordance with IFRS?

a. Accrual basis accounting

b. Cash basis accounting

c. Both accrual basis and cash basis accounting

d. Neither accrual basis nor cash basis accounting

5. Wong Ho Company had the following transactions during 2013:

• Sales of ¥11,000 on account

• Collected ¥4,000 for services to be performed in 2014

• Paid ¥1,250 cash in salaries

• Purchased airline tickets for ¥500 in December for a trip to take place in 2014

What is Wong Ho’s 2013 net income using accrual accounting?

a. ¥9,750.

b. ¥13,750.

c. ¥13,250.

d. ¥9,250.

6. Under International Financial Reporting Standards (IFRS)

a. The cash-basis method of accounting is accepted.

b. Events are recorded in the period in which the event occurs.

c. Interim period financial statements are either a calendar year or a fiscal year.

d. A fiscal year is an accounting time period encompassing less than 12 months.

Accrual Accounting Concepts

4-111

7. What is the proper adjusting entry at June 30, the end of the fiscal year, based on a prepaid

insurance account balance before adjustment, € 20,500, and unexpired amounts per analysis

of policies of €4,000?

a. Debit Insurance Expense, € 4,000; Credit Prepaid Insurance, € 4,000.

b. Debit Insurance Expense, € 20,500; Credit Prepaid Insurance, € 20,500.

c. Debit Prepaid Insurance, € 16,500; Credit Insurance Expense, € 16,500.

d. Debit Insurance Expense, € 16,500; Credit Prepaid Insurance, € 16,500.

8. Karcan, Inc. purchased supplies costing ₤2,500 on January 1, 2014 and recorded the trans-

action by increasing assets. At the end of the year ₤1,100 of the supplies are still on hand.

How will the adjusting entry impact Karcan, Inc.’s statement of financial position at December

31, 2014?

a. Decreased assets ₤ 1,100.

b. Increased equity ₤ 1,100.

c. Increased liabilities ₤ 1,400.

d. Decreased assets ₤ 1,400.

9. Karcan, Inc. purchased supplies costing ₤2,500 on January 1, 2014 and recorded the trans-

action by increasing assets. At the end of the year ₤1,100 of the supplies are still on hand. If

Karcan, Inc. does not make the appropriate adjusting entry, what is the impact on its state-

ment of financial position at December 31, 2014?

a. Assets overstated by ₤ 1,400.

b. Equity understated by ₤ 1,400.

c. Equity overstated by ₤ 1,100.

d. Assets overstated by ₤ 1,100.

10. Similarities between International Financial Reporting Standards (IFRS) and U.S. GAAP in-

clude all of the following except

a. Cash-basis accounting is not in accordance with either IFRS or U.S. GAAP.

b. Both IFRS and U.S. GAAP allow revaluation of items such as land and buildings to fair

value.

c. Both IFRS and U.S. GAAP divide the economic life of companies into artificial time peri-

ods.

d. The form and content of financial statements are very similar under IFRS and U.S.

GAAP.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

4-112

Brief Exercises

11. The statements of financial position of Rocky Acre Spread Ltd. include the following:

12/31/14 12/31/13

Interest Receivable €4,300 € -0-

Supplies 5,000 3,000

Salaries and Wages Payable 3,600 3,800

Unearned Service Revenue -0- 4,000

The income statement for 2014 shows the following:

Interest Revenue €14,400

Service Revenue 75,700

Supplies Expense 8,700

Salaries and Wages Expense 36,000

Instructions

Calculate the following for 2014:

1. Cash received for interest.

2. Cash paid for supplies.

3. Cash paid for salaries and wages.

4. Cash received for service revenue.

Solution 11 (15 min.)

Accrual Accounting Concepts

FOR INSTRUCTOR USE ONLY

4-113

12. Use the following income statement for the year 2013 for Haggrad Ltd. to prepare entries to

close the revenue and expense accounts for the company.

Service revenue €90,300

Expenses:

Salaries and Wages Expense €45,000

Rent Expense 25,000

Insurance Expense 6,500

Total expenses 76,500

Net income (loss) €13,800