5) A firm has prepared the coming year’s pro forma balance sheet resulting in a plug figure in a

preliminary statement—called the external financing required—of $230,000. The firm should prepare to

________.

A) repurchase common stock totaling $230,000

B) arrange for a loan of $230,000

C) do nothing; the balance sheet balances

D) invest in marketable securities totaling $230,000

6) A firm has prepared the coming year’s pro forma balance sheet resulting in a plug figure in a

preliminary statement—called the external financing required—of negative $250,000. The firm may

prepare to ________.

A) sell common stock totaling $250,000

B) arrange for a loan of $250,000

C) do nothing; the balance sheet balances

D) invest in marketable securities totaling $250,000

7) One basic weakness of the simplified pro forma approaches lies in the assumption that the firm’s past

financial condition is an accurate indicator of its future.

8) A weakness of the percent-of-sales method of preparing a pro forma income statement is ________.

A) that it forecasts income and then expresses the various income statement items as percentages of

projected income

B) the assumption that the firm faces linear total revenue and total operating cost functions

C) the assumption that the firm’s past financial condition is an accurate predictor of its future

D) the difficulty faced in calculation and preparation of such statements

9) Utilizing past cost and expense ratios (percent–of-sales method) when preparing pro forma financial

statements will tend to ________.

A) understate profits when sales are decreasing

B) understate profits when sales are increasing

C) overstate profits when sales are increasing

D) neither understate nor overstate profits

10) Utilizing past cost and expense ratios (percent–of-sales method) when preparing pro forma financial

statements will tend to ________.

A) understate profits when sales are decreasing and overstate profits when sales are increasing

B) understate profits, no matter what the change in sales, as long as fixed costs are present

C) understate profits when sales are increasing and overstate profits when sales are decreasing

D) overstate profits, no matter what the change in sales, as long as fixed costs are present

11) The weakness of the judgmental approach to preparing a pro forma balance sheet is ________.

A) the assumption that the values of certain accounts can be forced to take on desired levels

B) the assumption that the firm faces linear total revenue and total operating cost functions

C) the assumption that the firm’s past financial condition is an accurate predictor of its future

D) ease of calculation and preparation

12) If transportation costs were a huge portion of a firm’s expenses and the firm expected gas prices to

increase greatly in the next year, then in preparing its pro forma income statement the firm should

________.

A) use the percentage of transportation costs from last year’s sales

B) decrease the percentage of transportation costs from the percentage of last year’s sales

C) increase the percentage of transportation costs from the percentage of last year’s sales

D) double the percentage of transportation costs from the percentage of last year’s sales

13) In the development of pro forma statements, a firm that requires external funds means that its

projected level of cash is in excess of its needs and that funds would therefore be available for repaying

debt, repurchasing stock, or increasing the dividend to stockholders.

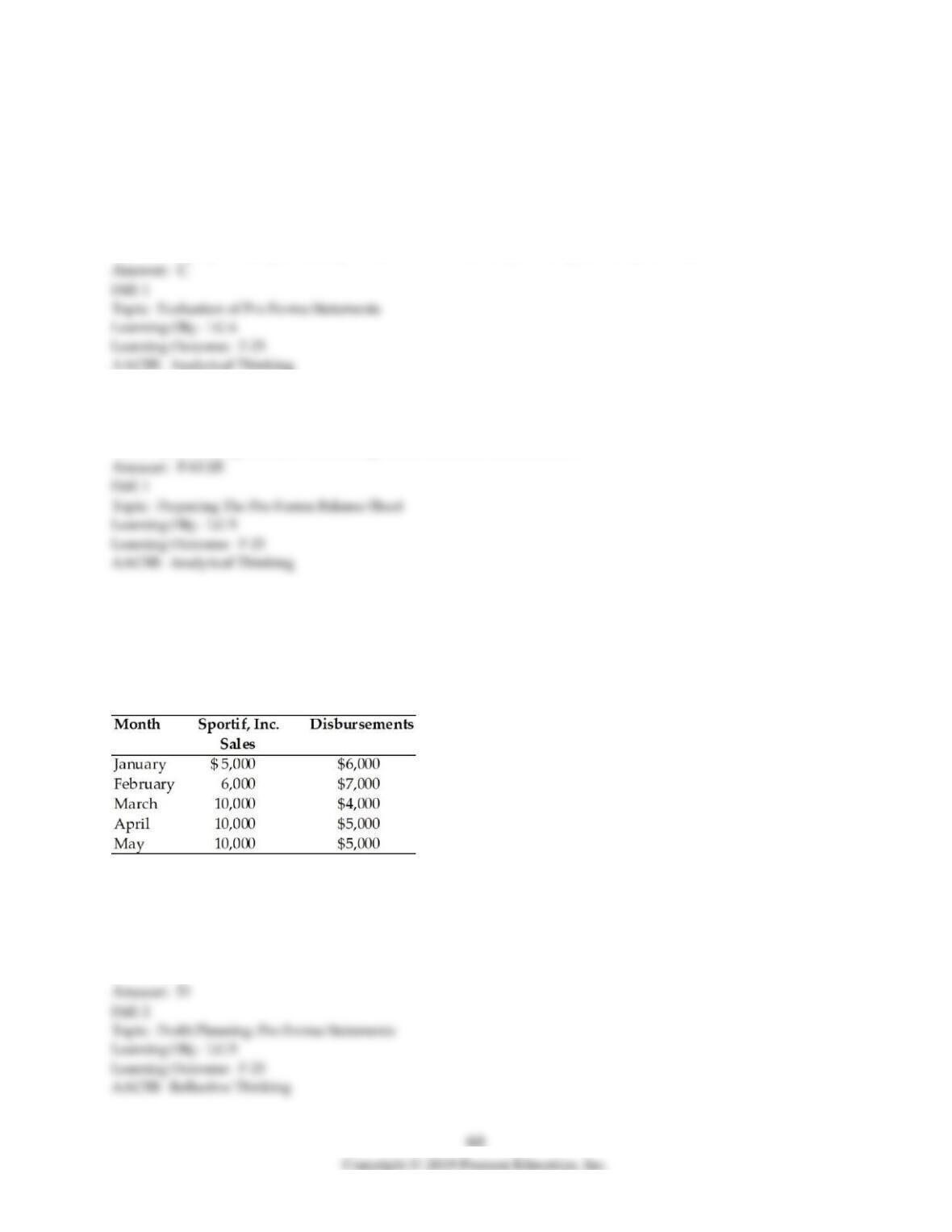

Table 4.3

The financial analyst for Sportif, Inc. has compiled sales and disbursement estimates for the coming

months of January through May. Historically, 75 percent of sales are for cash with the remaining 25

percent collected in the following month. The ending cash balance in January is $3,000.

14) The total cash receipts for April are ________. (See Table 4.3)

A) $5,000

B) $7,500

C) $9,250

D) $10,000

15) The net cash flow for February is ________. (See Table 4.3)

A) -$1,250

B) -$1,000

C) $5,750

D) $750

16) Calculate the amount of accounts receivable assuming that a pro forma balance sheet dated at the end

of May was prepared from the information presented. (See Table 4.3)

17) The firm has a negative net cash flow in the month(s) of ________. (See Table 4.3)

A) January, February, and March

B) February and March

C) January and February

D) February

18) The ending cash balance for March is ________. (See Table 4.3)

A) $250

B) $6,750

C) $2,500

D) $500

19) The ending cash balance for February is ________. (See Table 4.3)

A) $750

B) $1,750

C) $2,500

D) -$1,000

20) At the end of May, the firm has an ending cash balance of ________. (See Table 4.3)

A) $9,000

B) $16,750

C) $14,250

D) $12,000

21) The firm has a total financing requirement of ________ for the period from February through May.

(See Table 4.3)

A) $0

B) $1,750

C) $1,250

D) $ 750

22) If a pro forma balance sheet dated at the end of May was prepared from the information presented,

the marketable securities would total ________. (See Table 4.3)

A) $9,000

B) $9,500

C) $12,000

D) $16,750

63

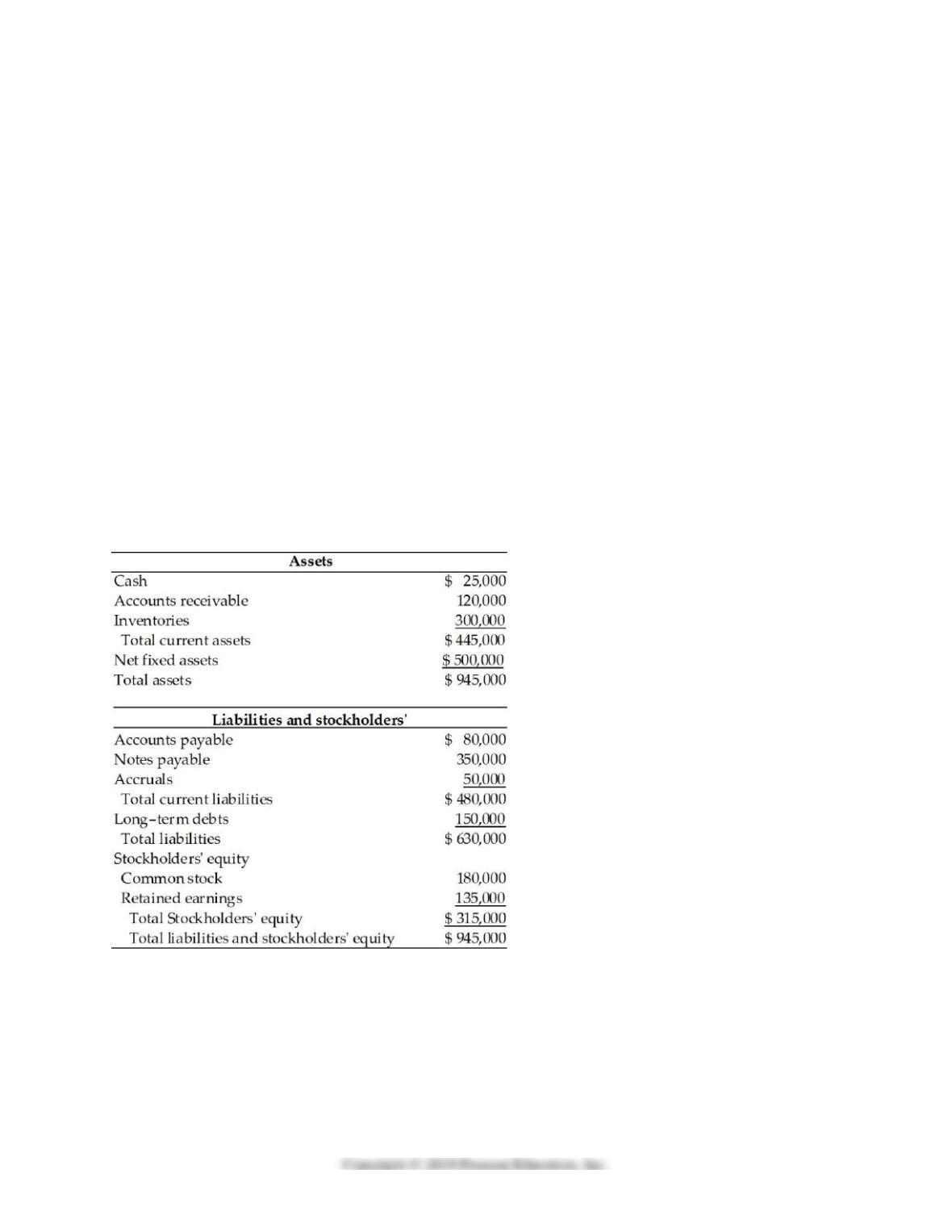

Table 4.5

A financial manager at General Talc Mines has gathered the financial data essential to prepare a pro

forma balance sheet for cash and profit planning purposes for the coming year ended December 31, 2019.

Using the percent-of-sales method and the following financial data, prepare the pro forma balance sheet

in order to answer the following multiple choice questions.

(a) The firm estimates sales of $1,000,000.

(b) The firm maintains a cash balance of $25,000.

(c) Accounts receivable represents 15 percent of sales.

(d) Inventory represents 35 percent of sales.

(e) A new piece of mining equipment costing $150,000 will be purchased in 2019.

Total depreciation for 2019 will be $75,000.

(f) Accounts payable represents 10 percent of sales.

(g) There will be no change in notes payable, accruals, and common stock.

(h) The firm plans to retire a long term note of $100,000.

(i) Dividends of $45,000 will be paid in 2019.

(j) The firm predicts a 4 percent net profit margin.

Balance Sheet

General Talc Mines

December 31, 2018

23) The pro forma total current assets amount is ________. (See Table 4.5)

A) $470,900

B) $500,000

C) $525,000

D) $575,000

24) The pro forma net fixed assets amount is ________. (See Table 4.5)

A) $500,000

B) $575,000

C) $600,000

D) $650,000

25) The pro forma current liabilities amount is ________. (See Table 4.5)

A) $400,000

B) $450,000

C) $475,000

D) $500,000

26) The pro forma total liabilities amount is ________. (See Table 4.5)

A) $500,000

B) $550,000

C) $700,000

D) $650,000

27) The pro forma accumulated retained earnings amount is ________. (See Table 4.5)

A) $90,000

B) $175,000

C) $140,000

D) $130,000

28) The external financing required in 2019 will be ________. (See Table 4.5)

A) $230,000

B) $240,000

C) $0

D) $195,000

29) General Talc Mines may prepare to ________. (See Table 4.5)

A) arrange for a loan equal to the external funds requirement

B) eliminate the dividend to cover the needed financing

C) cancel the retirement of the long term note to cover the needed financing

D) repurchase common stock equal to the external funds requirement

30) The external funds requirement results primarily from ________. (See Table 4.5)

A) the payment of dividends

B) the retirement of debt and purchase of new fixed assets

C) low profit margin

D) high cost of sales

31) If General Talc Mines cannot raise the external financing required through traditional credit channels,

the firm may ________. (See Table 4.5)

A) increase sales

B) purchase additional fixed assets to raise productivity

C) sell common stock

D) factor accounts receivable

67

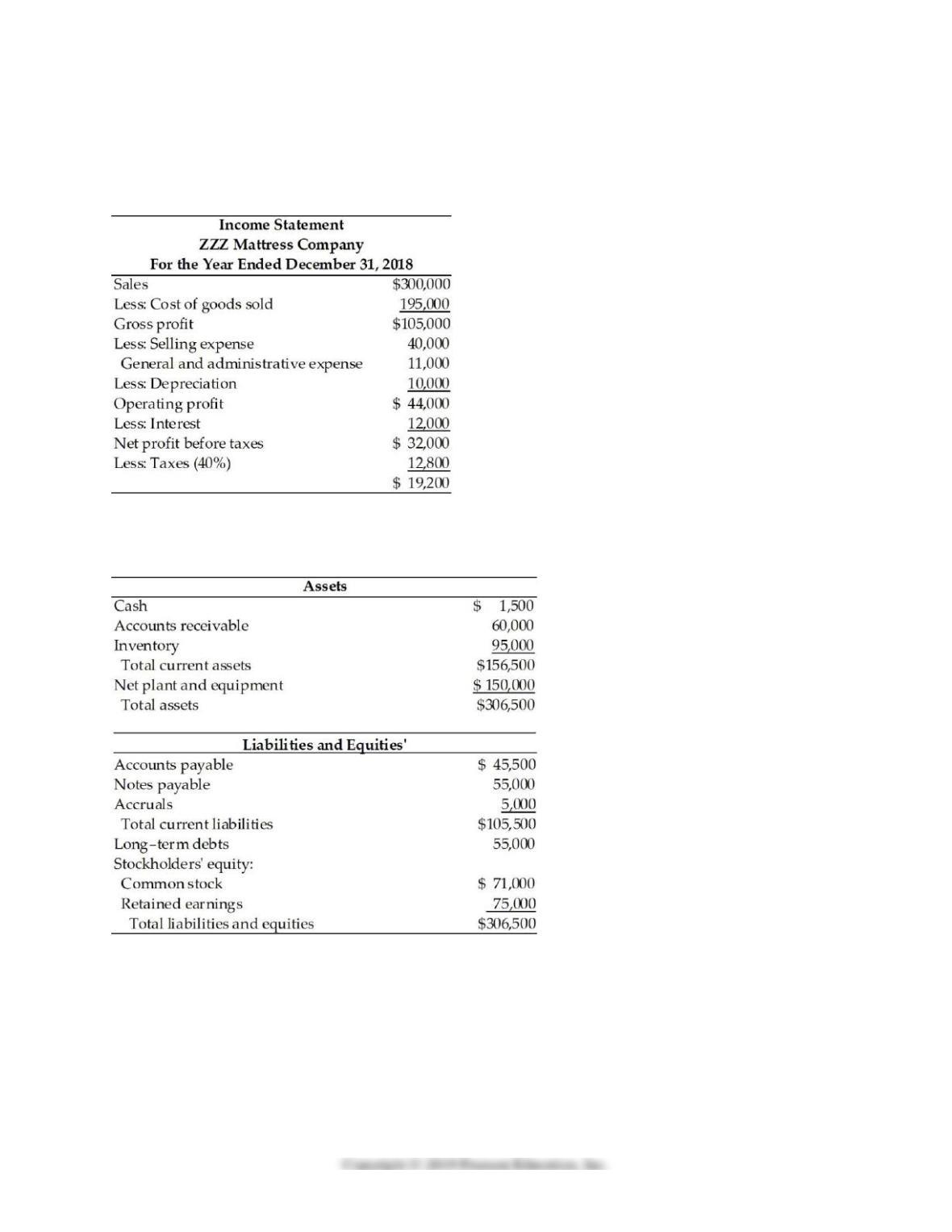

Table 4.7

The income statement and balance sheet for the ZZZ Mattress Co. for the year ended December 31, 2018

follow.

Balance Sheet

ZZZ Mattress Company

December 31, 2018

68

32) The ZZZ Mattress Co. has been requested by the 1st National Bank, a major creditor, to prepare a pro

forma balance sheet for the year ending, December 31, 2019. Using the percent–of-sales method and the

following financial data, prepare the pro forma income statement and balance sheet and discuss the

resulting external financing required. (See Table 4.7)

∙ 2019 sales are estimated at $330,000.

∙ Accounts receivable represent 20 percent of sales.

∙ A minimum cash balance of $1,650 is maintained.

∙ Inventory represents 32 percent of sales.

∙ Fixed-asset outlays in 2019 are $20,000. Total depreciation expense for 2019 will be $15,000.

∙ Accounts payable represents 15 percent of sales.

∙ Notes payable and accruals will remain the same.

∙ No long-term debt will be retired in 2019.

∙ No common stock will be repurchased in 2019.

∙ The firm will pay dividends equal to 50 percent of its earnings after taxes.

70

Table 4.8

71

33) The Wirl-Wind Company of America is trying to plan for the next year. Using the current income

statement and balance sheet given in Table 4.8, and the additional information provided, prepare the

company’s pro forma statements.

∙ Sales are projected to increase by 15 percent.

∙ Total of $75,000 in dividends will be paid.

∙ A minimum cash balance of $650,000 is desired.

∙ A new asset for $50,000 will be purchased.

∙ Depreciation expense for next year is $50,000.

∙ Marketable securities will remain the same.

∙ Accounts receivable, inventory, accounts payable, notes payable, and accruals will increase by 15

percent.

∙ $30,000 new issue of bond will be sold.

∙ No new stock will be issued.

4.7 Evaluation of pro forma statements

1) The two main weaknesses of pro forma financial statements are ________.

A) they produce inaccurate forecasts and they cannot be used by anyone outside the firm

B) they assume that the firm’s past financial condition is an accurate indicator of its future and that

managers can force particular accounts to take on particular desired values

C) stockholders take the pro forma forecasts too seriously, which causes volatility in stock prices when

actual outcomes deviate from forecasts

D) pro forma statements provide useful forecasts of profits, but not cash flows, and they rely too much on

the assumption that income statement items will grow at the same rate as sales

2) By necessity, building pro forma financial statements requires that managers make many assumptions

which will not turn out to be true. Therefore, pro forma financial statements are of little use as a financial

management tool.

3) Pro forma financial statements highlight situations in which actual outcomes deviate from projections,

which in turn helps managers understand why a firm’s results are not in alignment with its forecasts.

4) In the next planning period, a firm plans to change its policy of all cash sales and initiate a credit policy

requiring payment within 30 days. The statements that will be directly affected immediately are the

________.

A) pro forma income statement, balance sheet, and cash budget

B) pro forma balance sheet and cash budget

C) cash budget and statement of retained earnings

D) pro forma income statement and pro forma balance sheet