Achievement Test 3: Chapters 5 and 6 Name __________________________

Accounting Instructor _______________________

Kimmel, Weygandt, and Kieso Section # _______ Date _________

Part

I

II

III

IV

V

Total

Points

30

30

18

12

10

100

Score

PART I — MULTIPLE CHOICE (30 points)

Instructions: Designate the best answer for each of the following questions.

____ 1. A company returned goods for credit to the supplier. Which one of the following is a

portion of the journal entry required if a perpetual inventory system is used?

a. Credit Accounts Payable

b. Credit Purchase Returns and Allowances

c. Debit Accounts Receivable

d. Credit Inventory

____ 2. A company sells item on account with credit terms of 2/10, n/20. What is the meaning

of these terms?

a. An additional amount equal to 2 percent of the invoice price must be paid if

payment is not received within 10 days; the account is overdue after 20 days.

b. A 10 percent cash discount may be taken if payment is made immediately; a 2

percent discount if paid within 20 days.

c. A 2 percent cash discount may be taken if payment is made within 10 days of the

invoice date; otherwise the full amount is due within 20 days.

d. A 10 percent cash discount may be taken if payment is made within 2 days of the

invoice date; otherwise the full amount is due in 20 days.

____ 3. Which statement below is true concerning a perpetual inventory system?

a. It allows for the determination of cost of goods sold after each sale.

b. It requires a physical inventory count to determine the cost of goods on hand.

c. Cost of goods sold is determined based on a physical count at the end of the

period.

d. It is used infrequently due to the high cost of determining the cost of goods

acquired.

____ 4. An analyst calculated the quality of earnings ratio for a company and determined it to

be 2.7. What does this measure indicate?

a. The company may be using more aggressive accounting techniques in order to

accelerate income recognition.

b. The company’s net income significantly exceeds its net cash provided by operating

activities.

c. The company is relatively profitable.

d. The company’s net cash provided by operating activities significantly exceeds its

net income.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT3-2

____ 5. What does the inventory turnover measure?

a. The average amount of time inventory sits on a company’s shelves

b. The dollar amount of funds tied up in inventory

c. How quickly a company sells its goods

d. The profit generated from the selling of inventory

____ 6. Which of the following items are reported on a multiple-step income statement and on

a single-step income statement?

a. Cost of goods sold and sales

b. Gross profit and operating expenses

c. Operating expenses and total expenses

d. Sales and income from operations

____ 7. What do freight terms of FOB shipping point indicate?

a. The seller places the goods free on board the carrier, and the seller pays for the

goods.

b. Goods are placed free on board to the buyer’s place of business and the buyer

deducts the freight costs from the purchase price of the goods.

c. Goods are placed free on board to the buyer’s place of business and the seller

pays the freight costs. d. The seller places the goods free on

board the carrier, and the buyer pays for the freight costs.

____ 8. With regard to accounting for a merchandising company versus a service company,

which of the following is true?

a. Additional accounts and entries are typically required for a service company.

b. Retailers and wholesalers can be either service companies or merchandising

companies.

c. The operating cycle of a merchandising company is longer than that of a service

company.

d. Because inventory is an asset, it is recognized on the balance sheet by both

service and merchandising companies.

____ 9. In periods of rising prices, what will LIFO produce?

a. Lower income taxes than FIFO

b. Higher net income than FIFO

c. Higher net income than average costing

d. Lower cost of goods sold than FIFO

____ 10. Which of the following relationships is true concerning the Sales Returns and

Allowances account? a. It is a contra account that is reported on the

balance sheet as a deduction from the related sales.

b. It can flag problems of inferior merchandise, inefficiencies in filling orders, and

other mistakes.

c. It represents the cost of merchandise returned by customers.

d. It has a normal credit balance and is added to sales to determine net sales.

Achievement Test 3

AT3-3

____ 11. DynaTrue Industries reported net sales totaling $3,200,000 during the year. The

company’s gross profit rate was determined to be 41%. Which statement is true?

a. The company generated $1,312,000 of net income during the year.

b. The company generated 41 cents of net income out of each dollar of assets owned

by the company.

c. The company generated 41 cents out of every sales dollar that is available to

cover its operating expenses and contribute to profit.

d. The inventory cost is 41% of the sales price of the inventory items.

____ 12. Which statement is true regarding the lower–of-cost-or-market (LCM) method of

inventory?

a. LCM is an example of the revenue recognition principle.

b. LCM is departure from the cost basis of accounting.

c. Market is defined as current selling price.

d. Inventory is adjusted to market value each accounting period.

____ 13. Advantage Company’s ending inventory is overstated by $2,000. What is the effect of

this error on the current year’s cost of goods sold and net income, respectively?

a. Overstated and understated

b. Overstated and overstated

c. Understated and overstated

d. Understated and understated

____ 14. What is a LIFO reserve?

a. The tax savings resulting when LIFO is used during periods of rising prices

b. The difference in net income when a company uses LIFO as compared to FIFO

c. The difference between the inventory value and cost of goods sold when a

company uses LIFO

d. The difference between the inventory value under LIFO and FIFO

____ 15. A company uses LIFO to cost its inventory. Which statement is true?

a. The company must sell its newer inventory items before its older items.

b. The company will pay less income taxes in periods of rising prices compared to

using FIFO.

c. The cost of the company’s older inventory items are transferred to cost of goods

sold prior to the cost of the newly acquired items.

d. One way to think about the ending inventory under LIFO is the LISH assumption.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT3-4

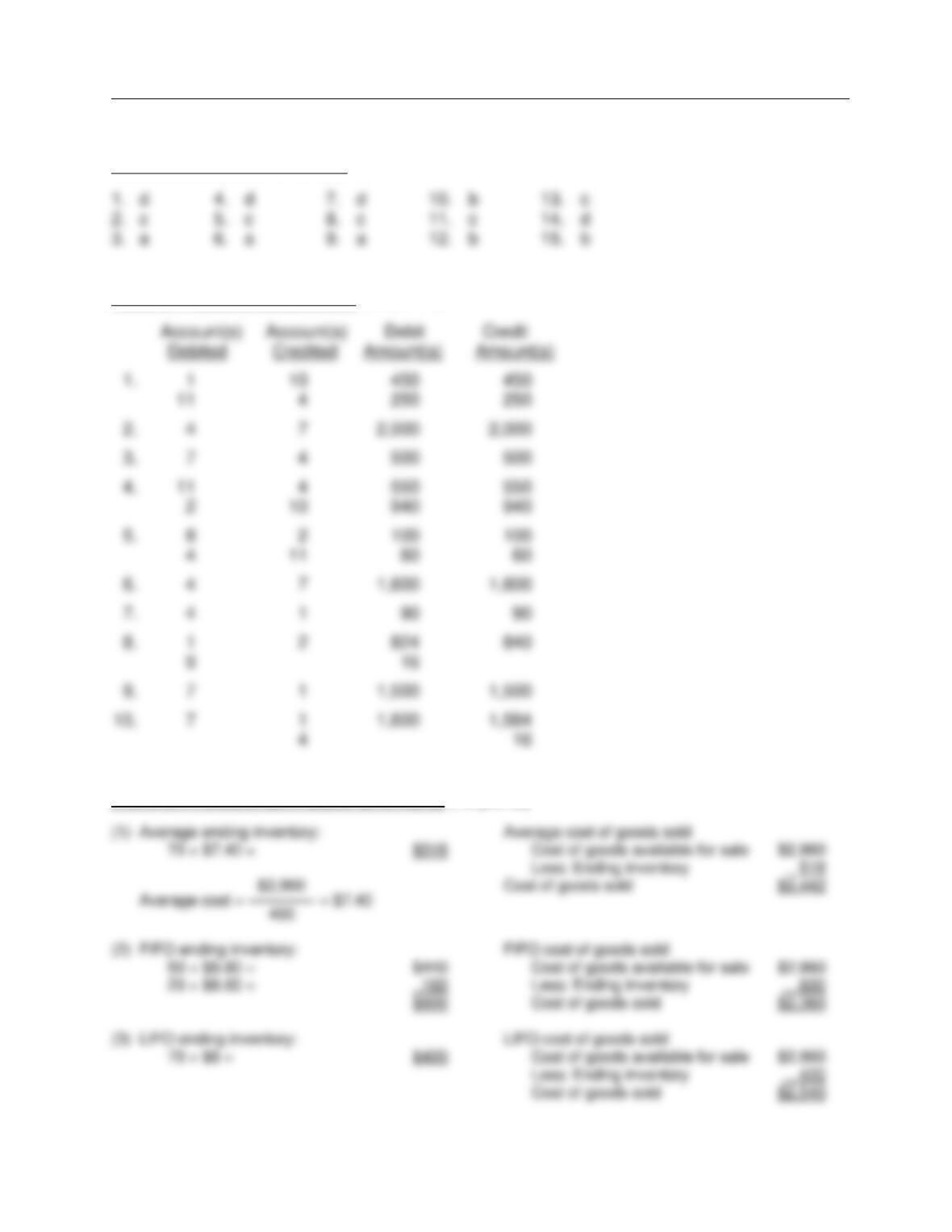

PART II — JOURNAL ENTRIES (30 points)

The ledger accounts given below, with an identification number for each, are used by Tactical

Supplies. The company uses a perpetual inventory system.

Instructions: Prepare appropriate entries for the month of May by placing the appropriate

identification number(s) in the debit and credit columns provided and the dollar amounts

pertaining to each account in the adjoining columns. Item 0 is given as an example.

1.

Cash

5.

Supplies

9.

Sales Discounts

2.

Accounts Receivable

6.

Land

10.

Sales Revenue

3.

Notes Receivable

7.

Accounts Payable

11.

Cost of Goods Sold

4.

Inventory

8.

Sales Returns and Allowances

12.

Freight-Out

Entry Information

Account(s)

Debited

Account(s)

Credited

Debit

Amount

Credit

Amount

0

Purchased merchandise for cash of $200

4

1

$ 200

$ 200

1

May 1: Sold merchandise with a cost of

$250 for cash of $450, terms net 30

2

May 2: Purchased merchandise from

Supplier, Inc. on account for $2,000,

terms 2/10, n/30

3

May 7: Returned $500 of merchandise

that had been purchased from Supplier,

Inc. on May 2

4

May 12: Sold merchandise costing $550

to Bike World on account for $900, terms

2/10, n/30. Bike World will pay $40 freight

costs per the shipping terms

5

May 13: Accepted a return of

merchandise from Bike World with a cost

of $60. Granted a credit on account of

$100

6

May 19: Purchased merchandise from AB

Supply on account for $1,600; terms 1/10,

n/30

7

May 20: Paid freight of $90 on the

shipment from Supplier, Inc. per the

shipping terms of purchase on May 3

8

May 21: Received payment in full from

Bike World

9

May 23: Paid Supplier, Inc. in full

10

May 28: Paid AB Supply in full

Achievement Test 3

AT3-5

PART III — INVENTORY COMPUTATIONS (18 points)

Lan Enterprises uses a periodic inventory system for buckets it sells. It had a beginning inventory

on April 1 of 80 units at a cost of $6 per unit. During April, the following purchases and sales were

made.

Purchases Sales

April 7 60 units at $7.00 April 5 120 units at $20

13 120 units at $7.50 11 90 units at $20

23 90 units at $8.00 20 80 units at $20

29 50 units at $8.80 30 40 units at $20

320 330

Instructions: Compute the April 30 ending inventory and April cost of goods sold under (a)

average cost, (b) FIFO, and (c) LIFO. Provide appropriate supporting calculations.

(1) Average – Ending Inventory = $_________; Cost of Goods Sold = $_________.

(2) FIFO – Ending Inventory = $_________; Cost of Goods Sold = $_________.

(3) LIFO – Ending Inventory = $_________; Cost of Goods Sold = $_________.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT3-6

PART IV — RATIOS (12 points)

Sanders Enterprises reported the following information for 2014:

Beginning inventory $ 32,000

Cost of goods sold 404,000

Ending inventory 45,000

Net income 28,000

Net sales 750,000

Operating expenses 220,000

Sales revenue 765,000

Instructions: Compute each of the following ratios:

(1) Gross profit rate

(2) Inventory turnover

(3) Days in inventory

(4) Profit margin

PART V — COMPUTATION OF NET PURCHASES/COST OF GOODS SOLD (10 points)

Journey Luggage uses a periodic inventory system and has the following account balances:

Beginning Inventory $31,000 Ending Inventory $ 18,000

Purchase Discounts 2,000 Purchases 240,000

Purchase Returns and Allowances 3,000 Freight-In 11,000

Operating Expenses 88,000 Net sales 489,000

Instructions: Compute each of the following:

(1) Net purchases

(2) Cost of goods available for sale

(3) Cost of goods sold

Achievement Test 3

AT3-7

Solutions — Achievement Test 3: Chapters 5 and 6

PART I — MULTIPLE CHOICE (30 points)

PART II — JOURNAL ENTRIES (30 points)

PART III — INVENTORY COMPUTATIONS (18 points)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

AT3-8

PART IV — RATIOS (12 points)

PART V — COMPUTATION OF NET PURCHASES/COST OF GOODS SOLD (10 points)